1. What is the projected Compound Annual Growth Rate (CAGR) of the Pharmaceutical Primary Packaging Lable?

The projected CAGR is approximately 15.8%.

Pharmaceutical Primary Packaging Lable

Pharmaceutical Primary Packaging LablePharmaceutical Primary Packaging Lable by Type (Solvent Acrylic, Hotmelt Rubber, Water Base Emulsion Acrylic, UV Curable), by Application (Prescription Primary Container, OTC Primary Container), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

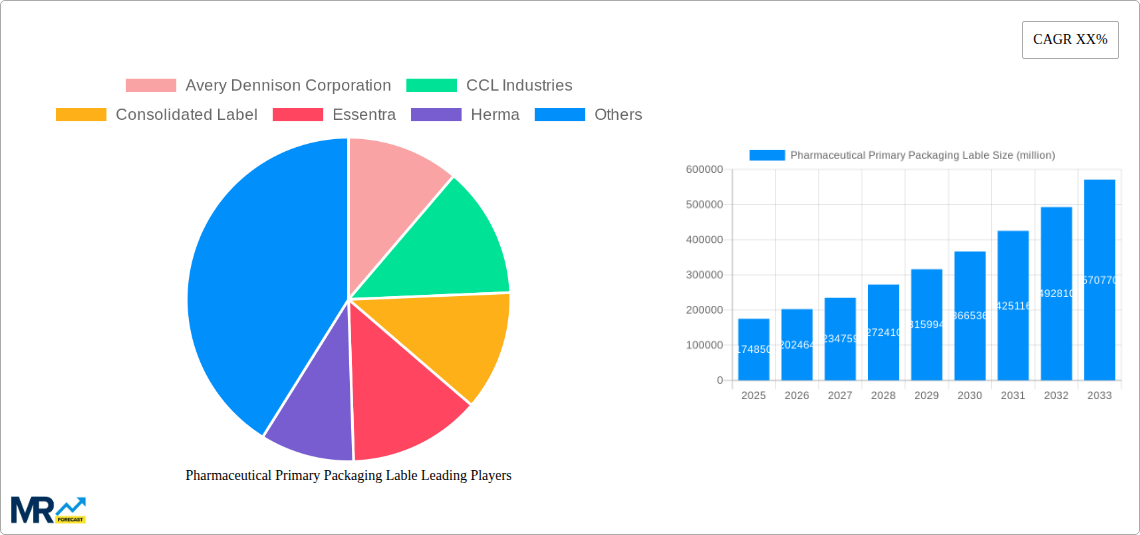

The global Pharmaceutical Primary Packaging Label market is poised for significant expansion, projected to reach approximately \$174.85 billion by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 15.8% throughout the forecast period from 2025 to 2033. This impressive growth is underpinned by several key drivers, most notably the escalating demand for safe and compliant pharmaceutical packaging, driven by stringent regulatory frameworks worldwide. The increasing prevalence of chronic diseases, an aging global population, and the continuous launch of new pharmaceutical products are further fueling the need for high-quality primary packaging labels that ensure product integrity, provide crucial patient information, and facilitate track-and-trace functionalities. Furthermore, advancements in label material technology, including the development of more durable, chemically resistant, and eco-friendly options, are catering to the evolving needs of the pharmaceutical industry.

The market segmentation reveals a dynamic landscape with diverse product types and applications. Solvent Acrylic and Hotmelt Rubber labels are expected to maintain significant market share due to their established reliability and cost-effectiveness in various pharmaceutical applications. However, the growing emphasis on sustainability and advanced functionalities is driving the adoption of Water Base Emulsion Acrylic and UV Curable labels, which offer improved environmental profiles and specialized performance characteristics. In terms of applications, both Prescription Primary Container and OTC Primary Container labels are critical components, with growth in both segments mirroring the overall expansion of the pharmaceutical sector. Major industry players like Avery Dennison Corporation, CCL Industries, and UPM are actively investing in innovation and strategic collaborations to capitalize on these market opportunities, focusing on enhancing product offerings and expanding their global reach to cater to the diverse regional demands across North America, Europe, Asia Pacific, and other emerging markets.

This report delves into the dynamic and critical market for Pharmaceutical Primary Packaging Labels, offering a detailed analysis of trends, drivers, challenges, and future growth trajectories. The study encompasses a comprehensive Study Period: 2019-2033, with a Base Year: 2025 and an Estimated Year: 2025, providing in-depth insights into the Historical Period: 2019-2024 and projecting future market performance through the Forecast Period: 2025-2033. The global market for pharmaceutical primary packaging labels is a robust and indispensable component of the healthcare industry, ensuring product integrity, patient safety, and regulatory compliance. The market is characterized by a continuous evolution of material science, printing technologies, and the ever-increasing demand for sophisticated labeling solutions that can withstand harsh environments and provide essential information.

XXX The global pharmaceutical primary packaging label market is witnessing a significant upward trajectory, driven by a confluence of factors including an aging global population, a rising prevalence of chronic diseases, and increasing healthcare expenditure worldwide. The market is projected to reach substantial figures, with unit volumes expected to surge into the billions as demand for essential medicines and innovative therapies continues to grow. A key trend is the increasing emphasis on patient safety and counterfeit prevention, leading to a higher adoption of advanced labeling technologies such as serialization and track-and-trace solutions. These technologies, often integrated into the primary packaging label, are crucial for regulatory compliance and supply chain security. Furthermore, there is a discernible shift towards more sustainable and eco-friendly labeling materials. Manufacturers are actively exploring and implementing biodegradable substrates and low-VOC (Volatile Organic Compound) inks to minimize environmental impact, aligning with global sustainability initiatives and growing consumer preference for green products. The demand for high-performance labels that can endure diverse storage conditions, including extreme temperatures and humidity, is also on the rise, particularly for biologics and specialty pharmaceuticals. This necessitates the use of specialized adhesives and durable filmic materials. The integration of smart labeling features, such as QR codes and NFC tags, is another emerging trend, facilitating enhanced patient engagement, medication adherence, and easy access to product information and verification. The growth in the generics market, coupled with the expanding pharmaceutical manufacturing base in emerging economies, further bolsters the demand for primary packaging labels. As regulatory frameworks around the world become more stringent, the need for compliant, secure, and informative labeling solutions will only intensify, shaping the future landscape of this vital market segment. The market is experiencing a constant innovation cycle, with a strong focus on developing labels that offer improved readability, tamper-evidence, and enhanced resistance to chemical interactions with the pharmaceutical product itself.

The pharmaceutical primary packaging label market is propelled by several powerful forces. Foremost among these is the ever-growing global demand for pharmaceuticals, directly linked to an aging global population and the increasing incidence of chronic diseases. This burgeoning demand necessitates a proportional increase in the production of medicines, thereby driving the consumption of primary packaging labels. Furthermore, stringent regulatory mandates worldwide concerning drug safety, traceability, and anti-counterfeiting measures are instrumental in shaping market dynamics. Governments and health authorities are increasingly emphasizing serialization and track-and-trace capabilities to combat the pervasive issue of counterfeit drugs, which poses a significant threat to public health. This regulatory pressure compels pharmaceutical manufacturers to invest in advanced labeling solutions that facilitate the tracking of products throughout the supply chain. The expanding generics market also plays a pivotal role. As more pharmaceutical products go off-patent, the production of affordable generic alternatives surges, leading to higher unit volumes of packaged medicines and, consequently, a greater demand for primary packaging labels. Moreover, the continuous innovation in drug delivery systems and the development of complex biologics and specialty pharmaceuticals often require highly specialized and robust primary packaging labels capable of withstanding challenging storage conditions and ensuring product integrity. This pushes manufacturers to develop and utilize advanced materials and adhesives.

Despite its robust growth, the pharmaceutical primary packaging label market faces several significant challenges and restraints. One of the primary hurdles is the stringent regulatory landscape, which, while a driver, also poses compliance challenges for label manufacturers. Adhering to diverse and evolving international regulations, such as those concerning data security, traceability standards, and material safety, can be complex and costly. The need for specialized materials that are inert, resistant to pharmaceutical ingredients, and capable of withstanding various environmental conditions adds to the production complexity and cost. For instance, labels for sensitive biologics or sterile injectables require specific substrates and adhesives that do not degrade or leach into the product. Fluctuations in raw material prices, particularly for polymers, inks, and specialty chemicals used in label production, can impact profit margins and create price volatility. The highly competitive nature of the market, with numerous global and regional players, intensifies price pressures and demands continuous innovation to maintain market share. Furthermore, the increasing demand for sustainable labeling solutions, while a positive trend, presents a challenge in terms of sourcing cost-effective and readily available eco-friendly materials that meet all regulatory and performance requirements. The integration of sophisticated technologies like serialization and smart labels requires significant upfront investment in machinery and expertise, which can be a barrier for smaller manufacturers. Finally, the growing concern over data security and privacy associated with smart labeling technologies needs careful consideration and robust solutions to prevent breaches and maintain trust.

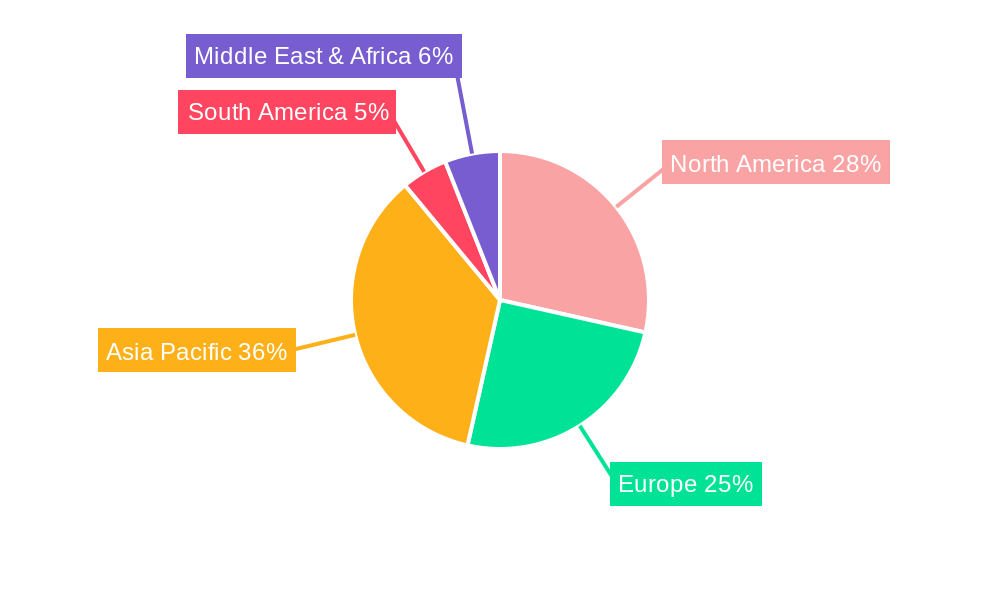

The North America region, encompassing the United States and Canada, is poised to continue its dominance in the pharmaceutical primary packaging label market. This leadership is attributed to several compounding factors. Firstly, North America boasts the largest pharmaceutical market globally, characterized by high healthcare spending, a robust research and development ecosystem, and a significant presence of major pharmaceutical companies. The region's advanced healthcare infrastructure and the high prevalence of chronic diseases contribute to a consistently high demand for pharmaceuticals, directly translating into substantial consumption of primary packaging labels. Secondly, regulatory frameworks in North America, particularly those enforced by the U.S. Food and Drug Administration (FDA), are among the most stringent in the world. The FDA's unwavering focus on drug safety, serialization, and track-and-trace mandates, such as the Drug Supply Chain Security Act (DSCSA), necessitates the use of sophisticated and compliant labeling solutions. This regulatory imperative drives the adoption of advanced labeling technologies and high-quality materials, solidifying North America's position as a market leader.

Within the North American market, the Prescription Primary Container segment is expected to be a significant revenue generator. This is due to the sheer volume of prescription medications dispensed daily, ranging from life-saving drugs for acute conditions to long-term treatments for chronic ailments. The critical nature of prescription drugs demands the highest standards of packaging and labeling to ensure efficacy, prevent errors, and protect patients from counterfeit products. Labels for prescription primary containers must be durable, legible, and often incorporate features like tamper-evidence and specific patient information.

Geographically, the dominance is further amplified by specific countries within the region:

The segment of Water Base Emulsion Acrylic adhesives is anticipated to play a pivotal role in the dominance of these regions and applications. These adhesives offer an excellent balance of performance and cost-effectiveness, making them highly suitable for the high-volume production of pharmaceutical labels. They provide good adhesion to a wide range of substrates, including glass and plastic primary containers, and are known for their good resistance to water and chemicals, which are crucial properties for pharmaceutical packaging. Furthermore, water-based adhesives are generally considered more environmentally friendly compared to solvent-based alternatives, aligning with the growing trend towards sustainability in the packaging industry. Their versatility allows them to be used in various printing processes, catering to the diverse needs of pharmaceutical manufacturers. The ability to achieve strong and reliable bonds on diverse primary container types, from vials and bottles to pre-filled syringes, ensures product integrity and patient safety. This makes water-based emulsion acrylics a preferred choice for both prescription and OTC primary containers in high-demand markets like North America, underpinning the region's market leadership.

Several factors are acting as significant growth catalysts for the pharmaceutical primary packaging label industry. The relentless pursuit of innovation in pharmaceutical research and development, leading to new drug formulations and complex biologics, necessitates the development of specialized and high-performance labels. Increased government initiatives and international regulations focused on combating counterfeit drugs and enhancing drug traceability are driving the adoption of advanced labeling technologies like serialization and tamper-evident features. The expanding healthcare infrastructure and rising pharmaceutical consumption in emerging economies, particularly in Asia-Pacific and Latin America, are creating new avenues for market growth. Furthermore, the growing consumer awareness regarding medication safety and the demand for transparent supply chains are indirectly pushing manufacturers to invest in more secure and informative labeling solutions.

This report provides an exhaustive analysis of the pharmaceutical primary packaging label market, offering a granular breakdown of market segmentation, regional dynamics, and key industry trends. It delves into the intricate interplay of various label types, including Solvent Acrylic, Hotmelt Rubber, Water Base Emulsion Acrylic, and UV Curable adhesives, and their specific applications in Prescription Primary Container and OTC Primary Container segments. The report meticulously examines the driving forces, challenges, and restraints impacting market growth, alongside identifying pivotal industry developments and growth catalysts. It also presents a comprehensive overview of leading market players and their strategic initiatives. This detailed coverage aims to equip stakeholders with the critical insights necessary to navigate this complex and evolving market landscape, enabling informed strategic decision-making and identifying lucrative opportunities within the pharmaceutical primary packaging label sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 15.8%.

Key companies in the market include Avery Dennison Corporation, CCL Industries, Consolidated Label, Essentra, Herma, Lintec Corporation, MCC Label, ProMach, UPM, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Pharmaceutical Primary Packaging Lable," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pharmaceutical Primary Packaging Lable, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.