1. What is the projected Compound Annual Growth Rate (CAGR) of the Conductive FIBC?

The projected CAGR is approximately 4.88%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Conductive FIBC

Conductive FIBCConductive FIBC by Type (Woven, Non-woven), by Application (Food and Beverages, Agricultural Products, Chemicals, Building and Construction, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

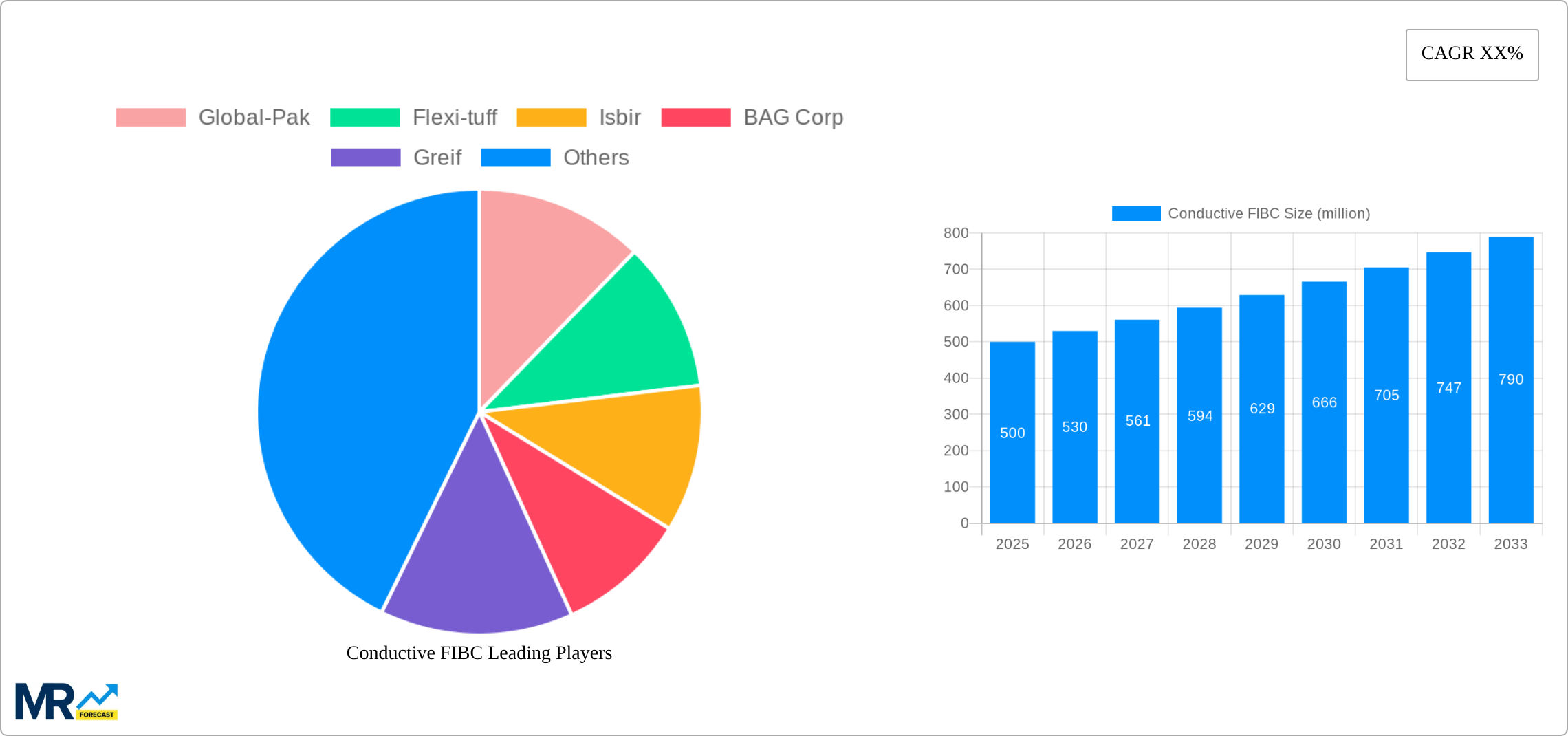

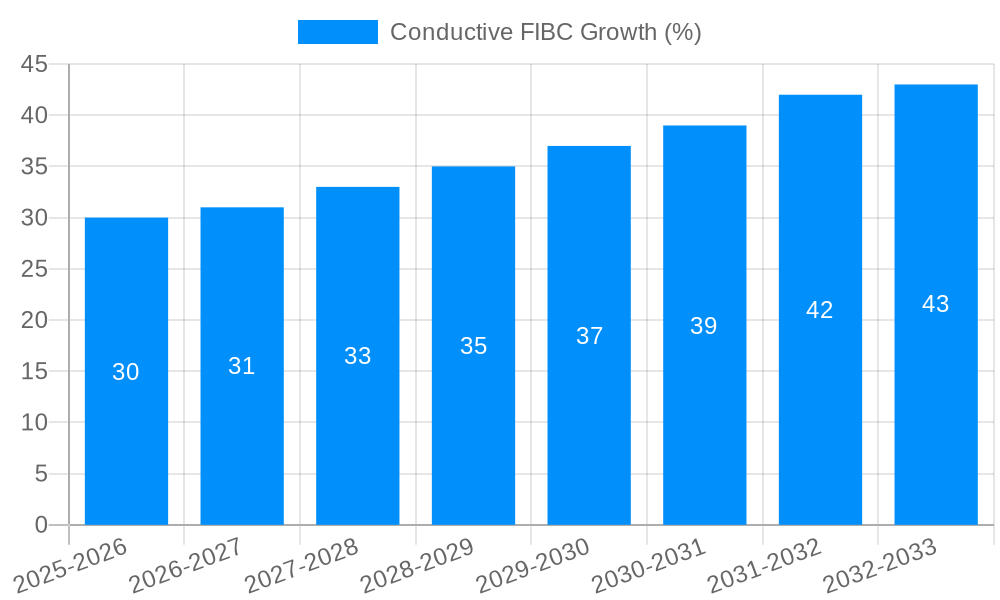

The global Conductive FIBC (Flexible Intermediate Bulk Container) market is poised for robust expansion, currently valued at an estimated $8.63 billion in 2025. This growth is propelled by a Compound Annual Growth Rate (CAGR) of 4.88% anticipated throughout the forecast period of 2025-2033. The increasing demand for safe and efficient handling of hazardous materials across various industries, including chemicals and agriculture, serves as a primary driver. Conductive FIBCs are essential for preventing electrostatic discharge (ESD), a critical safety measure in environments where flammable or explosive substances are present. The rising stringency of safety regulations globally further underpins the market's upward trajectory, compelling businesses to adopt these specialized packaging solutions. Innovations in material science and manufacturing processes are also contributing to the development of more durable, cost-effective, and high-performance conductive FIBCs, expanding their application scope.

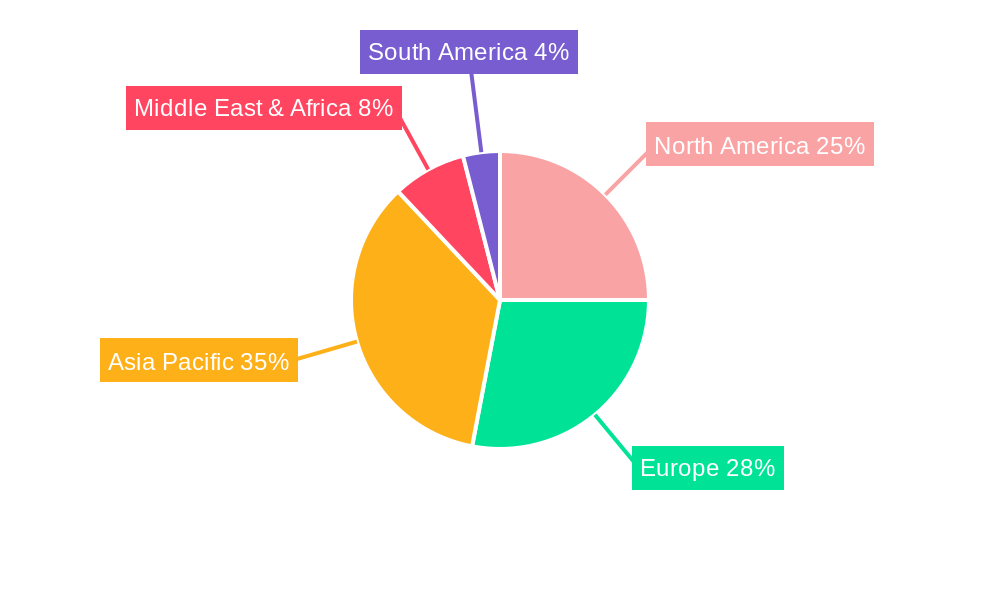

The market is segmented by type into woven and non-woven conductive FIBCs, with woven types currently dominating due to their superior strength and durability. Application-wise, the food and beverage, agricultural products, and chemicals sectors are leading the charge in adoption, driven by the need for secure and static-free containment. The building and construction industry also presents a growing opportunity. Geographically, Asia Pacific is expected to be a significant growth engine, fueled by rapid industrialization, a burgeoning manufacturing sector, and increasing awareness of safety standards in countries like China and India. North America and Europe, with their well-established chemical and manufacturing industries and stringent regulatory frameworks, will continue to represent substantial market shares. The competitive landscape is characterized by the presence of numerous global and regional players, fostering innovation and driving market dynamics.

This comprehensive report offers an in-depth analysis of the Conductive FIBC (Flexible Intermediate Bulk Container) market, spanning the Historical Period: 2019-2024, with a Base Year: 2025 and an extensive Forecast Period: 2025-2033. The study meticulously examines the market dynamics, identifying key trends, driving forces, and prevailing challenges that shape the industry. With an estimated market value projected to reach billions by the end of the forecast period, this report provides invaluable insights for stakeholders navigating this dynamic sector.

The Conductive FIBC market is experiencing a significant upward trajectory, driven by an increasing emphasis on safety protocols across various industries. During the Study Period: 2019-2033, the demand for FIBCs capable of dissipating static electricity has surged, particularly in sectors where flammable materials are handled. The Estimated Year: 2025 marks a pivotal point, with the market poised for robust expansion. Key market insights reveal a growing adoption of Type: Woven conductive FIBCs, which offer superior tensile strength and durability, making them ideal for demanding applications. The market's segmentation by Application showcases a substantial contribution from the Chemicals sector, where the risk of electrostatic discharge is a paramount concern, leading to the adoption of these specialized containers. The Building and Construction segment also represents a considerable share, with conductive FIBCs being utilized for the safe transport and storage of fine powders and potentially combustible materials. Furthermore, industry developments indicate a trend towards the integration of advanced conductive materials and enhanced manufacturing processes, aiming to improve the efficacy and reliability of these safety-critical products. The report anticipates that the global market value will reach several billions within the forecast horizon, reflecting the growing recognition of conductive FIBCs as essential safety equipment. Innovations in material science and design are expected to further enhance performance, driving market penetration into new and existing applications. The increasing stringency of safety regulations worldwide acts as a powerful impetus, compelling manufacturers and end-users alike to invest in superior static control solutions. The adoption of these specialized FIBCs is no longer a niche requirement but is becoming a standard practice for many hazardous material handlers, thereby broadening the market's scope and potential. The continuous research and development efforts are focused on achieving higher conductivity levels, improved tear resistance, and enhanced UV stability, all contributing to a more comprehensive and reliable solution for static hazard mitigation.

The burgeoning demand for Conductive FIBCs is primarily propelled by an unwavering commitment to industrial safety and regulatory compliance. As industries increasingly handle volatile and flammable substances, the potential for electrostatic discharge (ESD) to ignite these materials presents a significant hazard. Conductive FIBCs are specifically engineered to dissipate static electricity safely, thereby mitigating the risk of catastrophic accidents. The Study Period: 2019-2033 has witnessed a growing awareness among end-users regarding the detrimental consequences of static electricity, ranging from product damage to severe safety incidents. This heightened awareness, coupled with stricter governmental regulations and international safety standards, is a major catalyst for the widespread adoption of conductive FIBCs. The Chemicals and Pharmaceuticals sectors, in particular, are at the forefront of this adoption, driven by the inherent risks associated with handling fine powders and solvents. Furthermore, advancements in material science have led to the development of more effective and cost-efficient conductive materials, making these FIBCs more accessible and appealing to a broader range of industries. The increasing globalization of manufacturing and supply chains also contributes to this growth, as companies strive to maintain consistent safety standards across their international operations. The market's projected value in the billions underscores the significant impact of these driving forces.

Despite the robust growth, the Conductive FIBC market is not without its challenges. One significant restraint is the higher cost associated with conductive FIBCs compared to their standard counterparts. The specialized materials and manufacturing processes required to achieve conductivity add a premium, which can deter some price-sensitive customers, particularly in markets with less stringent safety regulations. Another hurdle is the awareness and education gap that persists in certain regions. While major industries understand the necessity of static control, smaller enterprises or those in emerging economies may lack the knowledge or perceived need for conductive FIBCs. This necessitates concerted efforts in market education and outreach. Technical limitations can also pose a challenge. While conductive FIBCs are designed to dissipate static, their effectiveness can be influenced by environmental factors such as humidity, and the type and quantity of material being handled. Ensuring consistent performance across all scenarios requires careful product selection and application guidelines. Furthermore, the availability of alternatives, such as static dissipative packaging or specialized grounding equipment, can sometimes present a competitive landscape, although conductive FIBCs offer an integrated and convenient solution. The global supply chain disruptions experienced in recent years, impacting raw material availability and logistics, have also had a ripple effect, potentially affecting production timelines and costs for conductive FIBC manufacturers. Overcoming these restraints will be crucial for unlocking the full market potential, which is estimated to be in the billions.

The Conductive FIBC market is poised for significant dominance in specific regions and segments, driven by a confluence of industrial activity, regulatory frameworks, and safety consciousness.

Dominant Regions/Countries:

North America: This region, encompassing the United States and Canada, is a frontrunner in the adoption of conductive FIBCs.

Europe: Similar to North America, Europe exhibits strong market dominance due to its advanced industrial infrastructure and stringent environmental and safety directives, such as REACH and ATEX.

Dominant Segments:

Application: Chemicals: This segment is a primary driver of the conductive FIBC market's growth.

Type: Woven: Woven conductive FIBCs are expected to continue their dominance.

The synergy between these regions and segments creates a powerful market dynamic, where the demand for safety and efficiency in handling hazardous materials drives the adoption of conductive FIBCs. The continuous evolution of industrial processes and the ever-increasing emphasis on risk mitigation solidify the position of these regions and segments as market leaders for the foreseeable future, contributing to the market's expected valuation in the billions.

Several key growth catalysts are propelling the Conductive FIBC industry forward. The escalating stringency of global safety regulations and industry-specific standards for handling hazardous and flammable materials is a primary driver. Increased awareness among industries regarding the significant risks and financial implications of electrostatic discharge (ESD) incidents is fostering a proactive approach to safety. Furthermore, advancements in material science are leading to the development of more efficient and cost-effective conductive materials, making these specialized FIBCs more accessible. The growing globalization of supply chains and the standardization of safety practices across diverse geographical locations also contribute to market expansion.

This comprehensive report provides an exhaustive exploration of the Conductive FIBC market, encompassing a detailed analysis from the Historical Period: 2019-2024 through to the Forecast Period: 2025-2033, with 2025 serving as the Base Year and Estimated Year. It delves into the intricate market dynamics, meticulously identifying the key trends, potent driving forces, and significant challenges that collectively shape the industry's trajectory. With an anticipated market value projected to reach billions by the conclusion of the forecast period, this report serves as an indispensable resource for stakeholders seeking to navigate and capitalize on the opportunities within this dynamic and safety-critical sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.88% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.88%.

Key companies in the market include Global-Pak, Flexi-tuff, Isbir, BAG Corp, Greif, Conitex Sonoco, Berry Plastics, AmeriGlobe, LC Packaging, RDA Bulk Packaging, Sackmaker, Langston, Taihua Group, Intertape Polymer, Lasheen Group, MiniBulk, Emmbi Industries, Dongxing Plastic, Yantai Haiwan, Kanpur Plastipack, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Conductive FIBC," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Conductive FIBC, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.