1. What is the projected Compound Annual Growth Rate (CAGR) of the Glass Packaging for Food and Beverages?

The projected CAGR is approximately 5%.

Glass Packaging for Food and Beverages

Glass Packaging for Food and BeveragesGlass Packaging for Food and Beverages by Type (/> Bottles, Vials, Jars, Others), by Application (/> Hot Drinks, Packaged Drinks, Milk and Dairy Drinks, CSD, Beer and Cider, Juice Drinks, Iced Tea and Coffee, Spirits, Wine), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

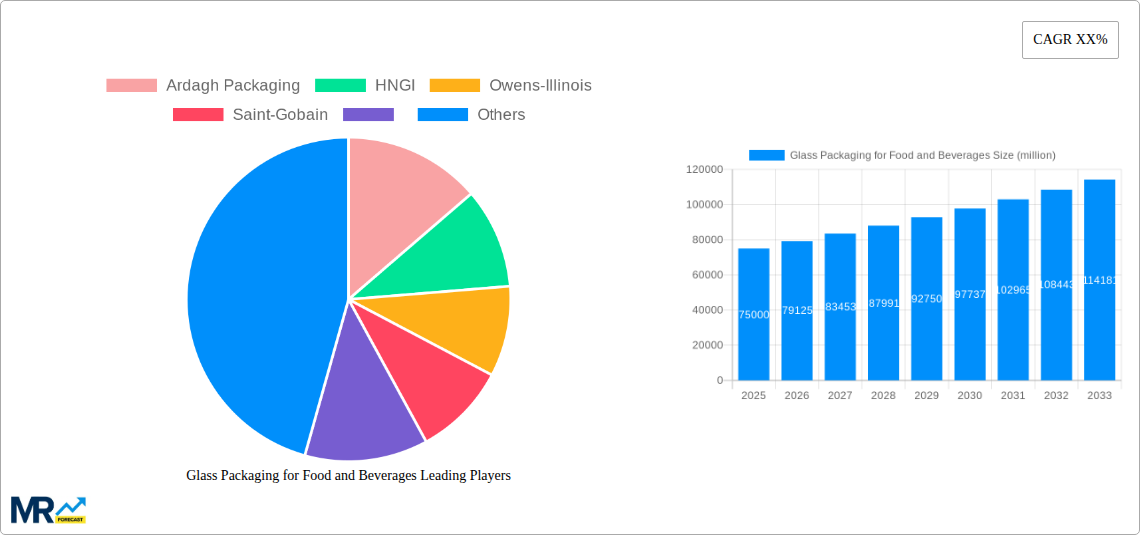

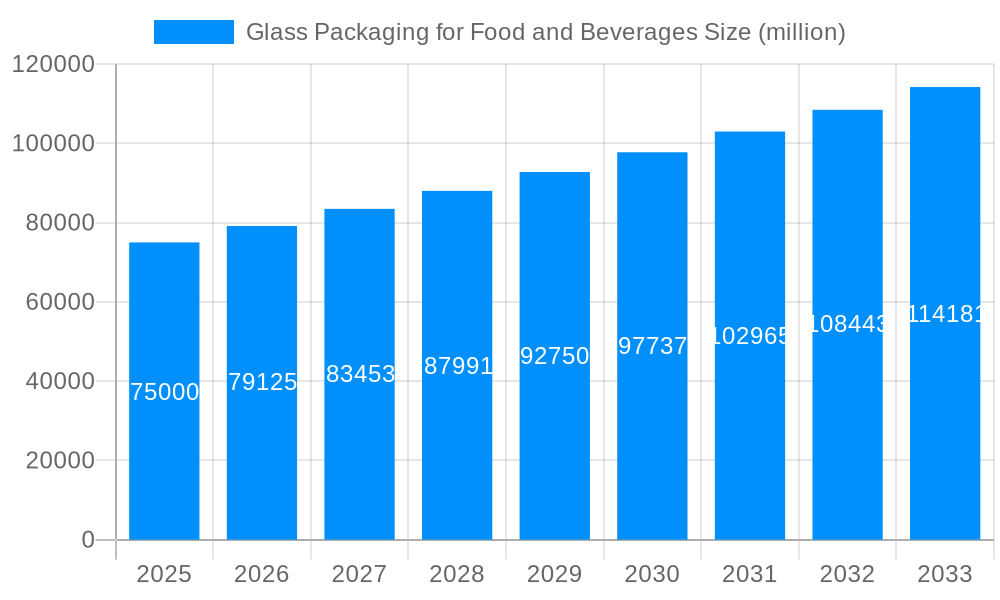

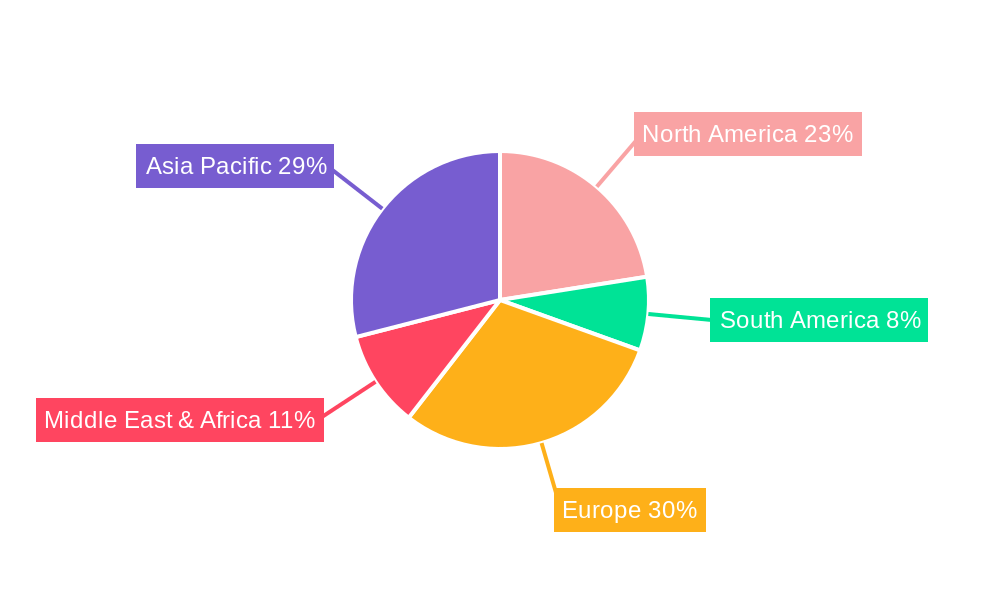

The global glass packaging market for food and beverages is experiencing robust growth, driven by increasing consumer preference for sustainable and eco-friendly packaging solutions. The market, estimated at $85 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 5% from 2025 to 2033, reaching approximately $120 billion by 2033. This growth is fueled by several factors, including the rising demand for premium food and beverage products, which often utilize glass packaging for its perceived quality and aesthetic appeal. Furthermore, the increasing awareness of the negative environmental impact of plastic packaging is driving a shift towards sustainable alternatives like glass, further boosting market expansion. Segmentation analysis reveals strong performance across various applications, with hot drinks, packaged drinks, and milk and dairy products representing significant market segments. Bottles continue to dominate the product type segment, reflecting the widespread use of glass bottles for a variety of beverages. Key players like Ardagh Packaging, HNGI, Owens-Illinois, and Saint-Gobain are actively contributing to market growth through innovation in glass production technology and expansion of their product portfolios to cater to evolving consumer preferences. Geographic analysis shows strong growth in North America and Europe, driven by high consumer spending and established infrastructure. However, Asia Pacific is poised for significant expansion due to rapid economic growth and increasing adoption of Western lifestyle trends. Market restraints include the relatively higher cost of glass production compared to other packaging materials and concerns surrounding glass breakage during transportation and handling.

Despite these challenges, the long-term outlook for the glass packaging market for food and beverages remains positive. The ongoing shift towards sustainability, the premiumization of food and beverage products, and the continuous innovation in glass manufacturing technologies are expected to drive market expansion in the coming years. Regional differences in growth rates will likely persist, reflecting varying levels of economic development and consumer preferences. The industry is expected to witness increased consolidation among major players, as companies seek to enhance their market share and expand their product offerings. Focus on lightweight glass containers and improved recycling infrastructure will be crucial to mitigating environmental concerns and ensuring long-term sustainability of the industry.

The global glass packaging market for food and beverages is experiencing robust growth, driven by increasing consumer demand for sustainable and premium packaging solutions. The market witnessed a significant expansion during the historical period (2019-2024), exceeding several million units annually. This upward trajectory is projected to continue throughout the forecast period (2025-2033), with an estimated value of XXX million units in 2025, fueled by several key factors. The rising preference for eco-friendly packaging options, coupled with the inherent properties of glass – its recyclability, inertness, and ability to preserve product quality – are major contributors to this growth. Consumers are increasingly aware of the environmental impact of their choices, and glass, with its high recyclability rate, aligns perfectly with this growing consciousness. Furthermore, the premium image associated with glass packaging is driving its adoption by brands aiming to elevate their product perception and command higher price points in the market. This trend is particularly visible in the spirits, wine, and premium food segments where glass is often the preferred choice. The increasing demand for convenience and the rise in e-commerce also positively impact glass packaging, as it offers excellent protection during shipping and handling. However, challenges remain, such as the higher cost of glass production compared to other materials and concerns about its fragility and transportation complexities. Nevertheless, the overall market sentiment remains positive, suggesting a continued expansion in the coming years. The market segmentation analysis reveals that bottles continue to dominate, followed by jars and vials, with "others" representing niche applications. Within applications, the CSD (carbonated soft drinks), beer and cider, and wine sectors show significant growth potential. The competitive landscape is characterized by established players such as Ardagh Packaging, HNGI, Owens-Illinois, and Saint-Gobain, constantly innovating to meet evolving market demands.

Several key factors are driving the growth of the glass packaging market for food and beverages. Firstly, the rising consumer awareness of environmental sustainability and the growing preference for eco-friendly packaging solutions are significantly boosting demand. Glass's inherent recyclability and biodegradability make it a highly attractive option compared to plastics, which are increasingly viewed with concern due to their environmental impact. Secondly, the superior barrier properties of glass ensure product quality and freshness, preserving flavors and aromas, especially crucial for sensitive food and beverages. This quality preservation, particularly important for premium products, supports a higher price point and contributes significantly to the market's value. Furthermore, the versatility of glass packaging allows for diverse shapes, sizes, and designs, catering to the varied needs of different product categories and branding strategies. This adaptability enables manufacturers to differentiate their products and appeal to specific consumer preferences. Lastly, the increasing demand for convenience and e-commerce is also driving the market. Glass, while requiring careful handling, provides excellent protection during shipping and handling, making it a suitable choice for online sales, particularly in the premium segment. These factors, combined with continuous innovations in glass manufacturing techniques, will propel the market's expansion in the coming years.

Despite the positive growth trajectory, the glass packaging market faces several challenges. The relatively high cost of glass production compared to other materials like plastic or aluminum represents a significant barrier to entry for some manufacturers and limits its adoption in price-sensitive markets. This cost disadvantage is further exacerbated by the energy-intensive nature of glass manufacturing, contributing to its carbon footprint, although significantly offset by its recyclability. The fragility of glass is another significant issue. It is susceptible to breakage during transportation and handling, resulting in increased logistical costs and waste. This fragility also necessitates robust packaging and shipping processes, adding to the overall cost and complexity. Moreover, the weight of glass packaging contributes to higher transportation costs compared to lighter alternatives. Finally, the availability of substitute materials like PET plastic, which are cheaper and lighter, represents a competitive challenge. While glass possesses clear advantages in terms of sustainability and product preservation, overcoming these challenges through innovations in manufacturing, logistics, and recycling infrastructure is crucial for sustained market growth.

The global market for glass packaging in food and beverages is diverse, with various regions and segments exhibiting significant growth potential. However, several key areas stand out as dominant forces.

Bottles: This segment consistently holds the largest market share, driven by the widespread use of glass bottles across numerous beverage categories, including CSDs, alcoholic beverages (beer, wine, spirits), and juice drinks. The large-scale adoption across various product categories establishes its dominance.

Wine: The premium nature of wine necessitates high-quality packaging, making glass the preferred material due to its aesthetic appeal and ability to preserve the product's integrity. The increasing demand for premium wines globally drives this segment's considerable contribution to overall market growth.

North America and Europe: These regions demonstrate mature markets with established recycling infrastructure and a strong consumer preference for sustainable packaging. The high awareness of environmental sustainability and the willingness to pay a premium for eco-friendly products solidify these regions' leading positions.

Asia-Pacific (Specific Countries): While a diverse region, specific countries like China and India, with their rapidly expanding middle classes and increasing consumption of packaged food and beverages, show remarkable growth potential in the glass packaging sector. However, infrastructure development and increased consumer awareness regarding sustainability remain pivotal factors influencing market penetration.

In summary, while other segments like jars, vials, and various beverage types contribute considerably, the combined influence of bottles, wine applications, and strong performance from developed markets like North America and Europe—along with emerging markets like China and India—indicates clear leaders in terms of market dominance within the glass packaging sector.

The glass packaging industry is experiencing significant growth driven by several factors. The burgeoning demand for sustainable packaging solutions, fueled by heightened consumer environmental awareness, is a key catalyst. Consumers increasingly prefer glass due to its recyclability and reduced environmental impact. This trend is further amplified by the premium image associated with glass packaging, particularly for high-value products like wine and spirits. Furthermore, continuous innovation in glass manufacturing techniques, focusing on lighter weight and improved durability, contributes to cost reduction and enhances its competitiveness. The rising e-commerce sector also fuels demand, as glass offers robust protection during shipping.

This report provides a comprehensive overview of the glass packaging market for food and beverages, analyzing market trends, driving forces, challenges, and key players. It offers detailed insights into market segmentation, regional performance, and future growth projections, providing valuable information for businesses operating in this dynamic sector. The report's data-driven approach and in-depth analysis offer actionable insights for strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5%.

Key companies in the market include Ardagh Packaging, HNGI, Owens-Illinois, Saint-Gobain.

The market segments include Type, Application.

The market size is estimated to be USD 70.23 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Glass Packaging for Food and Beverages," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Glass Packaging for Food and Beverages, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.