1. What is the projected Compound Annual Growth Rate (CAGR) of the Carbon Stee Drum?

The projected CAGR is approximately 4%.

Carbon Stee Drum

Carbon Stee DrumCarbon Stee Drum by Type (Up To 10 Gallons, 10-30 Gallons, 30-50 Gallons, 50-80 Gallons And Above, World Carbon Stee Drum Production ), by Application (Agriculture, Building And Construction, Chemicals & Solvents, Food & Beverages, Healthcare & Pharmaceuticals, Oils & Lubricants, Others, World Carbon Stee Drum Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

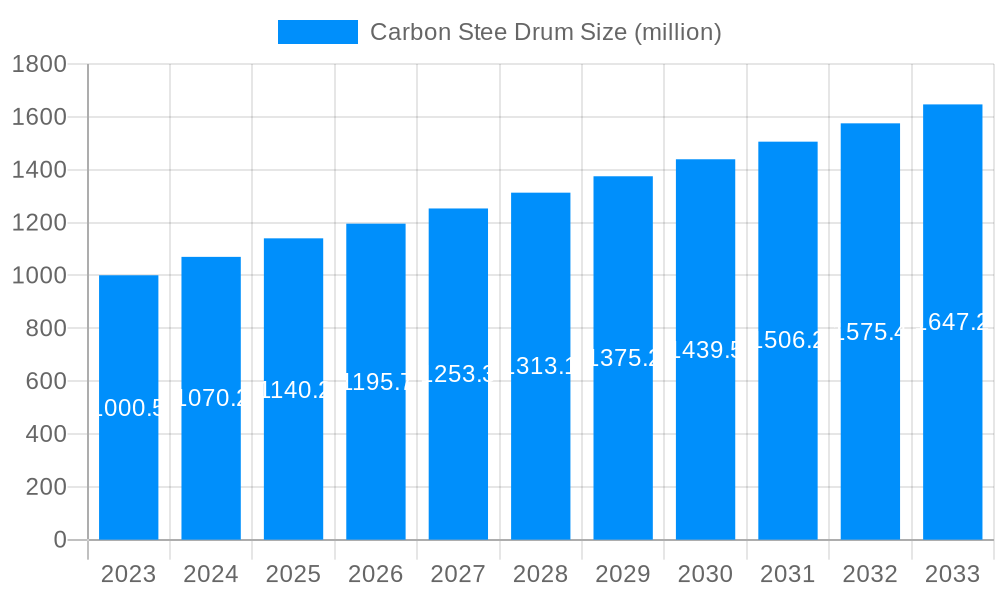

The global Carbon Steel Drum market is poised for steady growth, projected to reach approximately USD 1140.2 billion by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 4% throughout the forecast period of 2025-2033. This sustained expansion is driven by the intrinsic durability, cost-effectiveness, and robust containment capabilities of carbon steel drums, making them indispensable across a multitude of industrial sectors. Key applications in agriculture, building and construction, chemicals and solvents, food and beverages, healthcare and pharmaceuticals, and oils and lubricants underscore the market's fundamental reliance on these containers for safe storage and transportation. The increasing global industrial output and the stringent regulatory landscape surrounding the handling and transit of hazardous and non-hazardous materials are further bolstering demand. Emerging economies, with their burgeoning manufacturing bases and expanding infrastructure projects, represent significant growth avenues.

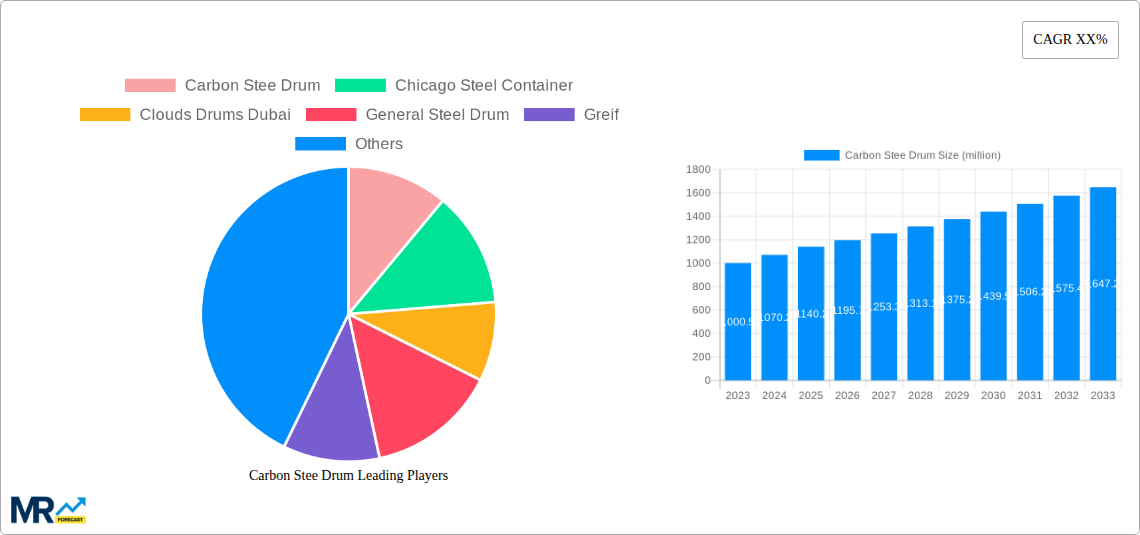

The market segmentation by type, including drums ranging from "Up To 10 Gallons" to "80 Gallons And Above," caters to diverse storage needs, from small-scale laboratory use to large industrial shipments. The "World Carbon Steel Drum Production" explicitly highlights the core manufacturing activity, indicating a focus on efficient production processes and supply chain optimization. While the market benefits from strong demand drivers, potential restraints such as the fluctuating prices of raw materials, specifically steel, and the increasing adoption of alternative packaging materials like plastic or fiber drums in certain niche applications, warrant close monitoring. Nevertheless, the inherent recyclability and superior strength of carbon steel drums are likely to sustain their market dominance. Key players like Greif, Mauser Group, and Chicago Steel Container are instrumental in shaping market dynamics through innovation and strategic expansions, ensuring the continued relevance and evolution of the carbon steel drum industry.

This comprehensive report offers an in-depth analysis of the global carbon steel drum market, projecting its trajectory from 2019 to 2033. With a base year of 2025, the study provides granular insights into market dynamics, key drivers, potential restraints, and future growth opportunities. The report leverages data from the historical period (2019-2024) and provides robust estimations for the forecast period (2025-2033). The global carbon steel drum market is a critical component of the industrial packaging sector, facilitating the safe and efficient transportation and storage of a vast array of products across diverse industries. The estimated market size for carbon steel drums is expected to reach billions of dollars by the end of the forecast period, indicating substantial growth and sustained demand. This report delves into the intricate factors shaping this valuation, including technological advancements, evolving regulatory landscapes, and fluctuating raw material costs, all of which contribute to the intricate financial projections presented.

The report segments the market by Type, including:

And by Application, encompassing:

Furthermore, the report scrutinizes World Carbon Steel Drum Production volumes and explores significant Industry Developments.

The global carbon steel drum market is experiencing a confluence of trends that are reshaping its landscape and driving its evolution. A primary trend is the increasing demand for sustainable packaging solutions, which, while seemingly counterintuitive for a steel product, is manifesting in the form of enhanced recyclability and extended reusability of carbon steel drums. Manufacturers are investing in technologies that improve the lifespan of these drums and streamline their recycling processes, responding to growing environmental consciousness among consumers and stringent regulations. This focus on circular economy principles is creating opportunities for innovation in coatings, linings, and overall drum design to further minimize environmental impact. Concurrently, the rising industrial output across emerging economies is a significant market driver. As manufacturing sectors expand in regions like Asia-Pacific and parts of Africa, the demand for robust and reliable packaging solutions, such as carbon steel drums, for chemicals, oils, and other industrial goods, is escalating. This geographical shift in manufacturing is directly translating into increased production and consumption of carbon steel drums in these developing markets.

Another discernible trend is the technological advancement in manufacturing processes. Automation, improved welding techniques, and enhanced quality control measures are leading to the production of more durable, leak-proof, and cost-effective carbon steel drums. These advancements not only improve the efficiency of drum production but also enhance their performance in challenging logistical environments, thereby bolstering their appeal across various industries. The stringent safety and regulatory requirements governing the transportation of hazardous materials are also playing a pivotal role. Carbon steel drums, known for their inherent strength and resistance to puncture and impact, are well-suited to meet these exacting standards. Compliance with regulations like UN certification for dangerous goods transportation is a non-negotiable aspect, and manufacturers are continuously innovating to ensure their products exceed these benchmarks. The fluctuating raw material costs, particularly steel prices, introduce a dynamic element to market trends. While steel is the primary raw material, its price volatility necessitates strategic procurement and production planning. This also encourages exploration of alternative materials or optimized material usage without compromising structural integrity. The integration of smart technologies, such as RFID tags for inventory management and tracking, is also beginning to emerge, promising greater supply chain visibility and efficiency. These trends collectively paint a picture of a market that is both mature in its core functionality and dynamically adapting to evolving economic, environmental, and technological imperatives. The overall market value is poised for significant growth, reaching billions of dollars as these trends continue to shape demand and supply.

The growth trajectory of the global carbon steel drum market is primarily propelled by an escalating demand for safe and reliable containment for a wide spectrum of industrial products. Industries such as chemicals, petrochemicals, and lubricants, which often deal with hazardous or sensitive substances, rely heavily on the robust nature of carbon steel drums to ensure product integrity and prevent environmental contamination during transit and storage. The inherent strength and durability of steel provide superior protection against punctures, corrosion, and impact, making it the preferred choice for these high-stakes applications. This fundamental advantage is amplified by the increasing global trade and the subsequent surge in logistics and transportation activities. As economies become more interconnected, the movement of goods across borders and continents intensifies. Carbon steel drums, with their standardized dimensions and stackability, facilitate efficient loading, unloading, and warehousing, thereby playing a crucial role in optimizing supply chains. The expansion of the manufacturing sector in emerging economies, particularly in Asia-Pacific, is another significant propellant. Rapid industrialization in these regions necessitates a corresponding increase in the demand for industrial packaging to handle the growing output of chemicals, paints, adhesives, and processed food products. Carbon steel drums, being a cost-effective and long-lasting solution, are ideally positioned to cater to this burgeoning demand.

Furthermore, stringent regulatory frameworks governing the transportation of hazardous materials act as a powerful driver. International and national regulations mandate the use of specific types of packaging that can withstand extreme conditions and prevent leaks, especially for dangerous goods. Carbon steel drums, often meeting rigorous UN certification standards, are inherently compliant with these requirements, providing manufacturers with peace of mind and ensuring safe operations. The growing emphasis on reusability and recyclability within the sustainability agenda is also contributing to the market's momentum. While steel itself is a sustainable material, the industry is witnessing a push towards extended drum lifecycles through improved coatings, maintenance services, and efficient recycling programs. This not only aligns with environmental goals but also offers long-term cost benefits for users. Finally, technological advancements in drum manufacturing, such as improved welding techniques, enhanced coating technologies, and automated production lines, are leading to the creation of more efficient, durable, and cost-competitive carbon steel drums, further solidifying their market position and contributing to the projected billions in market value.

Despite the robust growth and inherent advantages of carbon steel drums, the market faces several significant challenges and restraints that can temper its expansion and influence market valuation. A primary concern revolves around the volatility of raw material prices, particularly steel. Fluctuations in the global steel market, driven by factors such as supply-demand imbalances, geopolitical events, and trade policies, can significantly impact the cost of production for carbon steel drums. This price unpredictability can make it difficult for manufacturers to maintain stable pricing, potentially affecting profit margins and influencing purchasing decisions by end-users who might explore more price-stable alternatives. The increasing competition from alternative packaging materials presents another substantial restraint. While carbon steel drums offer unmatched durability for certain applications, materials like high-density polyethylene (HDPE) drums and intermediate bulk containers (IBCs) are gaining traction due to their lighter weight, corrosion resistance, and in some cases, lower initial cost, especially for non-hazardous or less critical applications. The ease of handling and transportation of lighter alternatives can be a deciding factor for some industries.

Moreover, the environmental impact and disposal considerations associated with steel, despite its recyclability, can pose a challenge. The energy-intensive nature of steel production and the potential for rust or corrosion in certain environments necessitate careful handling and disposal. While recycling is a strong point, the logistical challenges and costs associated with collecting and reprocessing used steel drums can sometimes outweigh the perceived benefits for certain users, especially in regions with less developed recycling infrastructures. The growing trend towards lightweighting and miniaturization in certain sectors, such as electronics and specialized chemicals, might lead to a reduced demand for larger, heavier steel drums. End-users are increasingly seeking packaging solutions that are tailored to specific product volumes and shipping requirements, potentially favoring smaller or more adaptable packaging formats. The perceived higher initial investment cost compared to some plastic alternatives can also be a barrier for small and medium-sized enterprises (SMEs) or those with tight budgets, especially when the long-term benefits of steel's durability and reusability might not be immediately apparent or financially accessible. Finally, evolving regulatory landscapes and the potential for stricter environmental regulations related to industrial waste and emissions could impose additional compliance costs on manufacturers, potentially influencing production costs and market competitiveness, impacting the overall market valuation projected in billions.

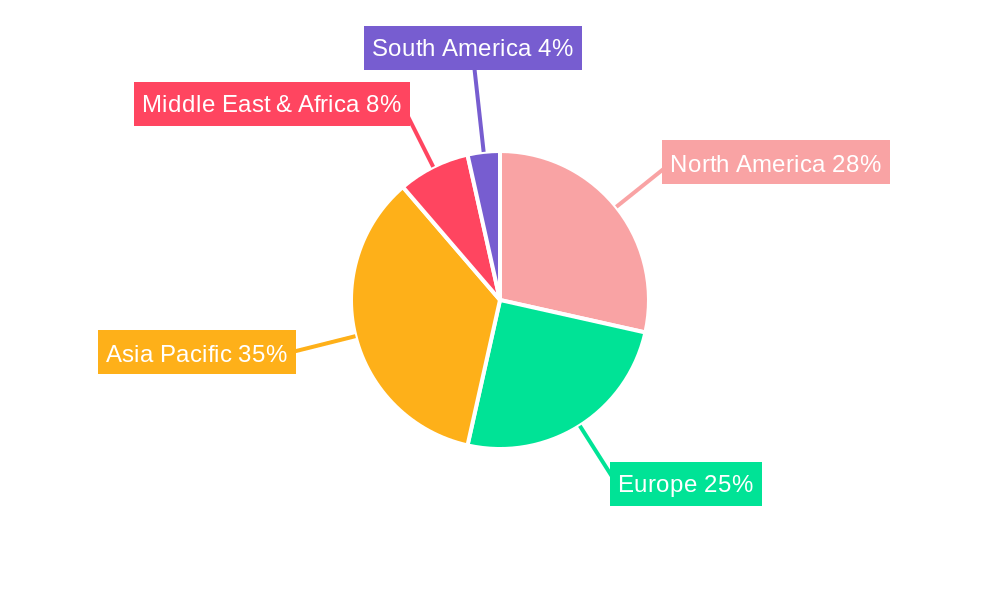

The global carbon steel drum market's dominance is intricately linked to a combination of regional industrial prowess and the specific characteristics of certain product segments. Among the various geographical areas, Asia-Pacific is poised to emerge as a dominant region, driven by its status as a manufacturing powerhouse and its burgeoning industrial sectors. The rapid expansion of chemical, petrochemical, automotive, and food and beverage industries in countries like China, India, and Southeast Asian nations fuels an insatiable demand for robust and reliable packaging solutions. These economies are experiencing significant growth in their industrial output, requiring substantial volumes of carbon steel drums for the safe transportation and storage of a diverse range of products, from bulk chemicals and solvents to lubricants and food ingredients. The region's commitment to infrastructure development and increasing export activities further bolsters the need for efficient and durable packaging.

Within the Application segments, Chemicals & Solvents and Oils & Lubricants are projected to hold significant sway in dictating market dominance. The inherent properties of carbon steel drums—their strength, chemical resistance, and ability to prevent leaks and contamination—make them indispensable for the safe handling and transportation of a vast array of hazardous and non-hazardous chemicals, solvents, paints, adhesives, and various grades of oils and lubricants. These industries often operate under stringent regulatory compliance for the transportation of dangerous goods, and carbon steel drums, with their proven reliability and UN certification capabilities, are the preferred choice. The sheer volume of these products manufactured and traded globally ensures a consistent and substantial demand for these types of drums.

Furthermore, considering the Type segmentation, the 30-50 Gallons and 50-80 Gallons categories are expected to dominate the market share. These drum sizes represent the most common and versatile capacities for industrial packaging across various applications. They offer a practical balance between volume, handling ease, and storage efficiency, making them ideal for a wide range of industrial operations. The 50-80 Gallons segment, in particular, is crucial for bulk transportation of chemicals, lubricants, and certain food products, where larger volumes are required for economic efficiency. The 30-50 Gallons segment serves a broad spectrum of applications, including smaller batches of chemicals, specialized solvents, and various industrial fluids. The widespread adoption and versatility of these drum sizes across numerous industries contribute significantly to their market dominance.

In essence, the confluence of a high-growth manufacturing hub in Asia-Pacific, the critical demand from the Chemicals & Solvents and Oils & Lubricants sectors, and the ubiquitous utility of the 30-50 and 50-80 Gallons drum types collectively underpins the market's dominance. The substantial projected market value in billions is a testament to the sustained and critical role these regions and segments play in the global carbon steel drum ecosystem. The report will delve into the specific market share, growth rates, and influencing factors for each of these key areas, providing a granular understanding of where the market's power lies and where future growth is most likely to be concentrated. The interplay between these regional and segmental dynamics is crucial for stakeholders seeking to understand the competitive landscape and identify lucrative opportunities within the world carbon steel drum production and consumption.

The carbon steel drum industry is propelled by several key growth catalysts that ensure its continued expansion. A primary driver is the ever-increasing global demand for industrial goods, which directly translates into a higher need for efficient and secure packaging. As manufacturing output rises across sectors like chemicals, petrochemicals, and food processing, so does the requirement for reliable containers. Furthermore, stringent regulations governing the transportation of hazardous materials necessitate the use of robust and compliant packaging solutions. Carbon steel drums, with their inherent strength and UN certification capabilities, are ideally suited to meet these demands, making them a preferred choice for many industries. The growing emphasis on sustainability and the circular economy is also a significant catalyst. Steel's high recyclability rate and the potential for extended drum lifespan through improved coatings and maintenance programs are aligning with environmental concerns, driving demand from eco-conscious businesses.

This report provides an all-encompassing analysis of the global carbon steel drum market, offering unparalleled insights into its past, present, and future. It meticulously examines the market dynamics, identifying the critical forces driving its growth, such as escalating industrial production and stringent safety regulations. Simultaneously, it delves into the challenges and restraints, including raw material price volatility and competition from alternative materials, offering a balanced perspective on the market's complexities. The report highlights key regions and segments poised for dominance, providing a strategic roadmap for stakeholders. Furthermore, it outlines significant industry developments and showcases the leading players, offering a comprehensive understanding of the competitive landscape. The detailed segmentation by type and application, coupled with extensive market sizing and forecasting from 2019 to 2033, ensures that this report serves as an indispensable resource for informed decision-making within the multi-billion dollar carbon steel drum industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4%.

Key companies in the market include Carbon Stee Drum, Chicago Steel Container, Clouds Drums Dubai, General Steel Drum, Greif, Industrial Container Services, Izvar Ambalaj Sanayi VE Ticaret, James G Carrick, Mauser Group, Metal Drum, North Coast Container, Rahway Steel Drum, Chicago Steel Container.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Carbon Stee Drum," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Carbon Stee Drum, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.