1. What is the projected Compound Annual Growth Rate (CAGR) of the Electronic Components Paper Carrier Tape?

The projected CAGR is approximately 6.2%.

Electronic Components Paper Carrier Tape

Electronic Components Paper Carrier TapeElectronic Components Paper Carrier Tape by Type (Slitting Paper Carrier Tape, Punched Paper Carrier Tape, Embossed Paper Carrier Tape), by Application (Capacitor, Resistor, Inductors, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

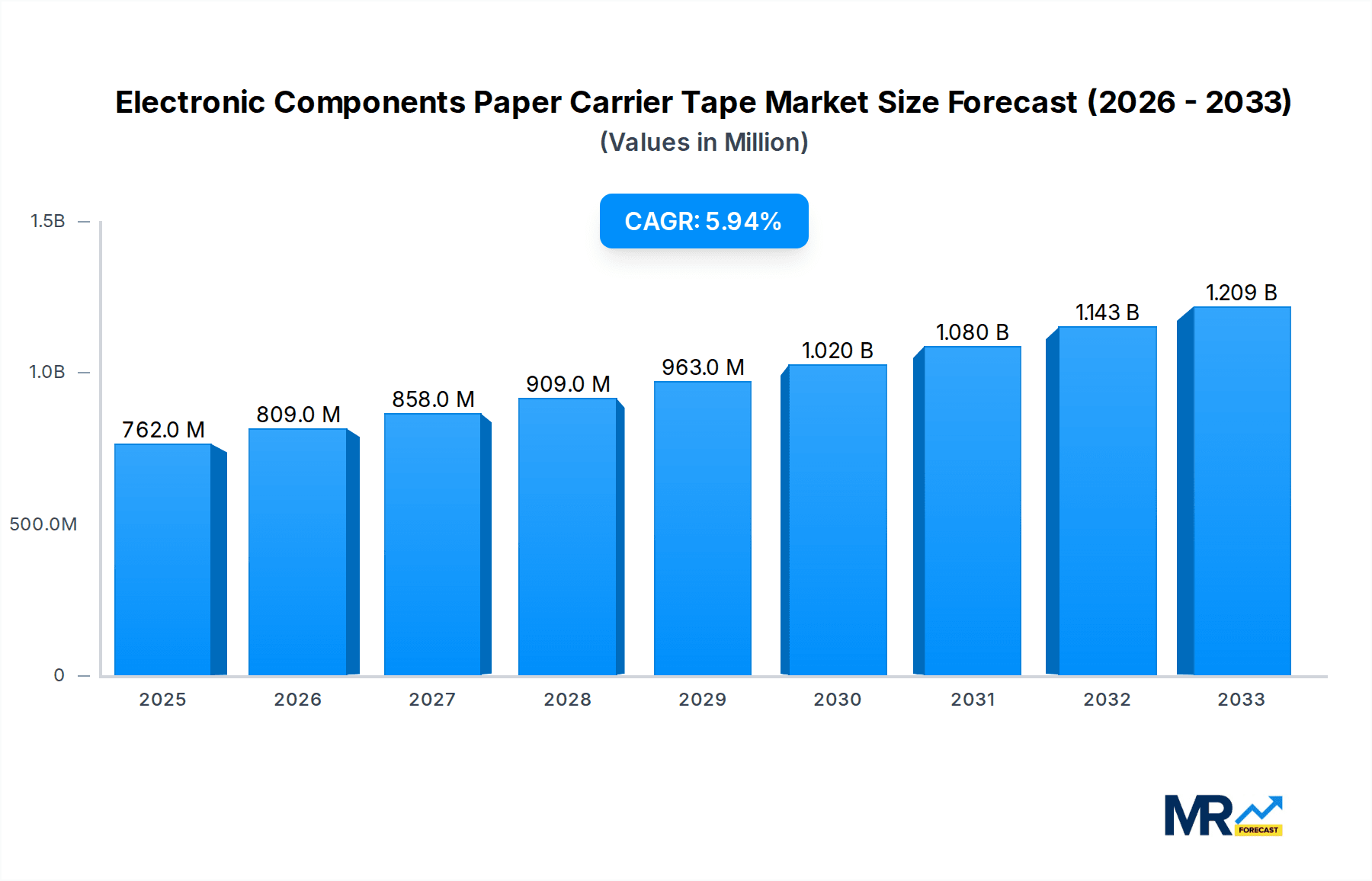

The global Electronic Components Paper Carrier Tape market is poised for robust expansion, driven by the escalating demand for electronic components across diverse industries. Valued at an estimated USD 762 million in the base year of 2025, the market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% through 2033. This sustained growth is underpinned by the indispensable role of paper carrier tapes in the automated packaging and handling of miniature electronic components like capacitors, resistors, and inductors. The increasing miniaturization of electronic devices, coupled with the rapid adoption of 5G technology, electric vehicles, and the Internet of Things (IoT), directly fuels the need for high-precision and reliable carrier tape solutions. Furthermore, the growing emphasis on sustainable and eco-friendly packaging materials is a significant tailwind, positioning paper-based carrier tapes as a preferred alternative to traditional plastic options. Leading companies such as Zhejiang Jiemei Electronic And Technology, SEWATE, and Oji F-Tex are actively investing in innovation and capacity expansion to cater to this burgeoning demand.

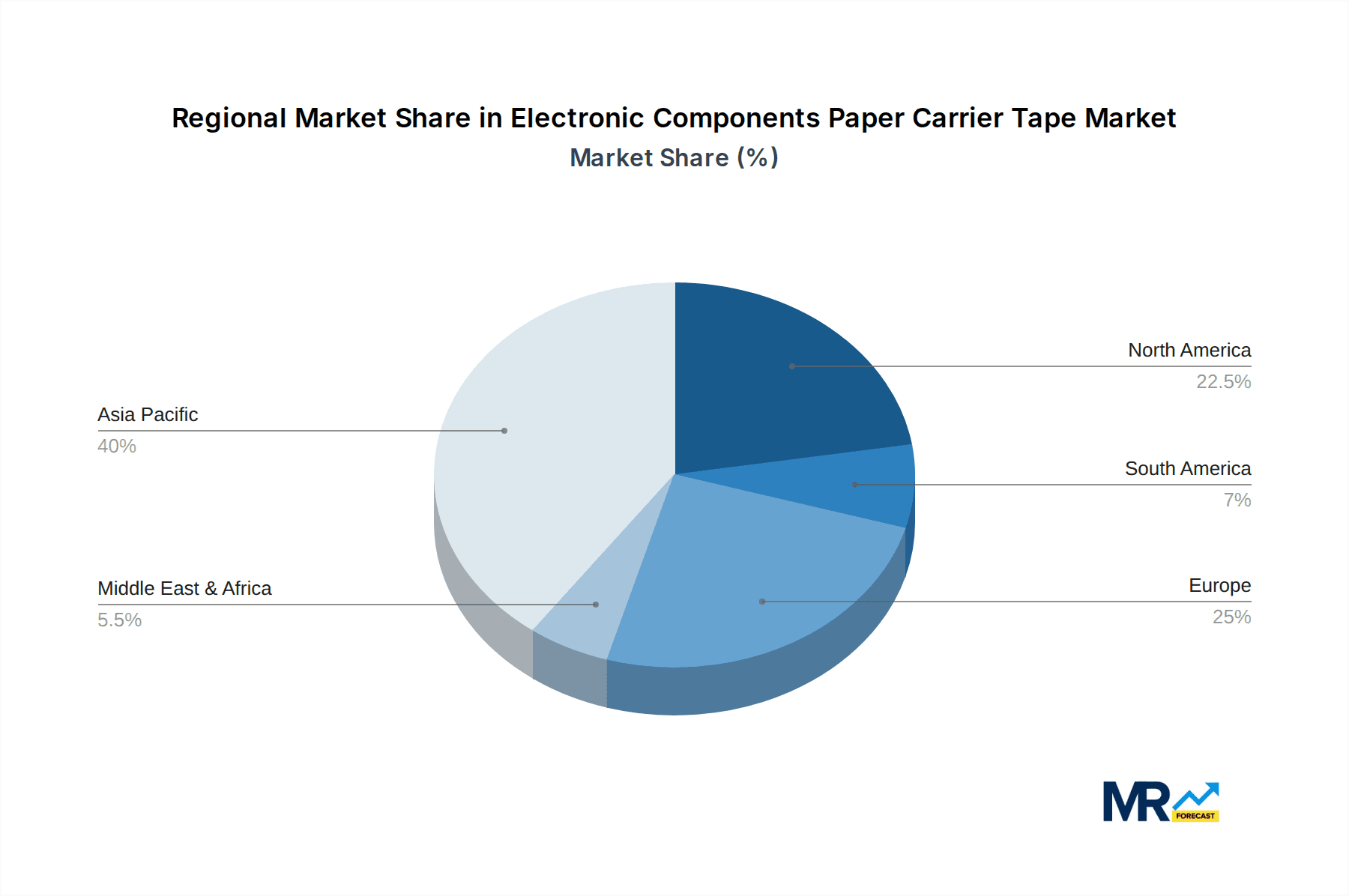

The market's trajectory is characterized by evolving trends, including advancements in material science for enhanced tape strength and dimensional stability, as well as the development of specialized carrier tapes for highly sensitive or irregularly shaped components. The integration of automation in electronics manufacturing processes necessitates carrier tapes that offer optimal performance in high-speed pick-and-place machines, thereby ensuring efficient production and minimizing component damage. While the market exhibits strong growth potential, certain restraints such as fluctuating raw material costs and the competitive landscape with alternative packaging solutions could present challenges. However, the inherent recyclability and biodegradability of paper carrier tapes align perfectly with global sustainability initiatives, providing a distinct competitive advantage. Geographically, the Asia Pacific region, led by China and Japan, is expected to dominate the market owing to its massive electronics manufacturing base. North America and Europe also represent significant markets due to their advanced technological infrastructure and substantial consumption of electronic components.

This report delves into the intricate landscape of the Electronic Components Paper Carrier Tape market, meticulously analyzing its trajectory from 2019 to 2033. With a base year of 2025, the study offers in-depth insights into historical performance (2019-2024) and projects future trends, with a particular focus on the estimated year of 2025 and the extensive forecast period spanning 2025-2033. The market is segmented by tape type, application, and further analyzed across key geographical regions. Our comprehensive coverage aims to provide stakeholders with actionable intelligence for strategic decision-making in this dynamic sector.

The global Electronic Components Paper Carrier Tape market is experiencing a period of robust expansion, driven by the ever-increasing demand for miniaturized and high-density electronic devices. A key insight into this market is the significant shift towards Embossed Paper Carrier Tape, which currently holds a commanding presence and is projected to maintain its dominance throughout the forecast period. This segment alone is estimated to account for over 700 million units in 2025, reflecting its suitability for accommodating a wide array of sensitive electronic components, from delicate capacitors to intricate resistors and inductors. The precision offered by embossed pockets ensures component protection during automated handling and transportation, a critical factor in high-volume manufacturing. Furthermore, the continuous innovation in the design and manufacturing of embossed tapes, leading to improved dimensional stability and ESD (Electrostatic Discharge) protection, further solidifies its market leadership. Another notable trend is the sustained growth of Slitting Paper Carrier Tape, driven by its cost-effectiveness and versatility for simpler components. While not as high in unit volume as embossed tape, it is anticipated to contribute a substantial 250 million units in 2025, catering to the vast production of basic electronic elements like resistors and some types of capacitors. The demand for slitting tape is intrinsically linked to the sheer scale of consumer electronics production, where cost efficiency remains a paramount consideration. The market also witnesses a steady, albeit smaller, demand for Punched Paper Carrier Tape, particularly for components requiring specific seating arrangements or where moderate protection is sufficient. This segment is projected to contribute approximately 150 million units in 2025, serving niche applications and older component designs. Overall, the market trends are characterized by a growing preference for specialized tape solutions that enhance automated assembly processes and safeguard delicate electronic components, with embossed tape leading the charge in terms of volume and technological advancement. The continuous miniaturization of electronic devices, coupled with the increasing complexity of integrated circuits and passive components, directly fuels the demand for paper carrier tapes that offer superior protection, precise component placement, and compatibility with high-speed pick-and-place machines. The industry is witnessing a sustained upward trajectory, with the total market volume for electronic components paper carrier tapes projected to reach well over 1.1 billion units in 2025. This growth is not merely in quantity but also in sophistication, as manufacturers develop tapes with enhanced features such as improved ESD shielding, greater thermal resistance, and customized pocket designs to accommodate next-generation components. The unwavering demand from the consumer electronics, automotive, and industrial sectors for increasingly smaller and more powerful devices is a fundamental driver. For instance, the burgeoning IoT (Internet of Things) market, with its proliferation of smart devices, necessitates a vast supply of precisely packaged electronic components, directly impacting the paper carrier tape market. Similarly, the automotive industry's push towards electrification and advanced driver-assistance systems (ADAS) relies heavily on miniaturized and high-performance electronic components, further bolstering demand. The ongoing technological advancements in manufacturing processes for paper carrier tapes, including improved material science and precision engineering, are also contributing to market expansion by offering higher quality and more cost-effective solutions. The shift towards automated manufacturing across various industries worldwide has created a symbiotic relationship, where the efficiency of automated assembly lines is directly dependent on the reliability and suitability of the carrier tapes used for component delivery. The increasing adoption of advanced packaging technologies for semiconductors and other electronic components further necessitates specialized carrier tapes capable of handling these intricate and often delicate parts, ensuring their integrity from manufacturing to final assembly.

The electronic components paper carrier tape market is experiencing a significant upswing, propelled by a confluence of powerful driving forces. At the forefront is the relentless pace of miniaturization in electronic devices. As smartphones, wearables, and IoT devices shrink, so too must the components they house. Paper carrier tapes are indispensable for accurately and safely transporting these increasingly small and delicate parts, with embossed varieties playing a crucial role in providing customized pockets for precise component retention. This inherent need for precision packaging, especially for high-value semiconductor components and sensitive capacitors, ensures a consistent demand. Furthermore, the exponential growth of the global electronics manufacturing industry, particularly in Asia, acts as a major catalyst. The sheer volume of production for consumer electronics, automotive components, and industrial automation systems necessitates an equally massive supply of efficient and cost-effective packaging solutions like paper carrier tapes. The adoption of automation in manufacturing processes is another critical driver. High-speed pick-and-place machines, the backbone of modern electronics assembly, rely heavily on standardized and reliable carrier tapes to feed components seamlessly. Paper carrier tapes, with their excellent dimensional stability and compatibility with these machines, are therefore essential enablers of efficient automated production lines. The increasing integration of advanced functionalities and higher component densities within electronic devices also fuels demand. As more sophisticated features are packed into smaller form factors, the need for carrier tapes that can protect a wider variety of component types, including specialized resistors, inductors, and custom ICs, becomes paramount. This pushes innovation in carrier tape design to accommodate diverse shapes and sizes.

Despite the burgeoning growth, the electronic components paper carrier tape market is not without its challenges and restraints. A primary concern is the fluctuating raw material costs, particularly the price of paper pulp and the specialized coatings used for ESD protection. Volatility in these input prices can significantly impact the profit margins of manufacturers and subsequently lead to price increases for end-users. This can be particularly problematic for high-volume, cost-sensitive applications. Another significant challenge is the increasing competition from alternative packaging solutions, most notably plastic carrier tapes. While paper tapes offer environmental benefits and certain performance advantages, plastic tapes often provide superior moisture resistance and durability in harsh environments, posing a competitive threat, especially for certain component types and applications. The stringent quality control and regulatory compliance requirements within the electronics industry also present a hurdle. Manufacturers must adhere to strict standards for component protection, dimensional accuracy, and ESD integrity, which necessitates continuous investment in advanced manufacturing technologies and rigorous testing protocols. Failure to meet these standards can lead to product rejection and reputational damage. Moreover, the global supply chain disruptions, as witnessed in recent years, can affect the availability of raw materials and the timely delivery of finished carrier tapes. Geopolitical factors, natural disasters, and logistical challenges can all create bottlenecks, impacting production schedules and customer satisfaction. Finally, disposal and recycling complexities associated with certain coated paper carrier tapes, particularly those with embedded conductive layers, can be a concern for environmentally conscious manufacturers, although efforts are underway to develop more sustainable solutions.

Asia Pacific is poised to be the dominant region in the Electronic Components Paper Carrier Tape market, driven by its status as the global manufacturing hub for electronics. Countries like China, South Korea, Taiwan, and Japan are home to a vast number of semiconductor manufacturers, passive component producers, and electronics assembly plants, creating an insatiable demand for these essential packaging materials. The sheer scale of production, estimated to involve billions of units of electronic components annually, translates directly into a colossal requirement for paper carrier tapes. The region's strong focus on Embossed Paper Carrier Tape is particularly noteworthy. This segment is expected to lead the market dominance within Asia Pacific, driven by the increasing complexity and miniaturization of components used in consumer electronics, smartphones, and wearable devices manufactured in the region. For instance, companies are producing millions of units of embossed tape to package tiny surface-mount capacitors and resistors that are integral to these devices. The ability of embossed tapes to create precise, component-specific pockets is crucial for protecting these delicate parts during high-speed automated assembly processes, which are ubiquitous in Asian manufacturing facilities. The demand for embossed tape in Asia Pacific alone is projected to exceed 500 million units in 2025.

Furthermore, the region's robust growth in the automotive electronics sector, with an increasing number of electric vehicles and advanced driver-assistance systems (ADAS) being developed and manufactured, is another significant contributor. These applications require a high density of sophisticated electronic components, necessitating reliable and precisely engineered carrier tapes.

Within the segments, the Capacitor application is expected to be a major driver of market dominance, particularly in the Asia Pacific region. The vast production of a wide range of capacitors, from small ceramic capacitors for consumer electronics to larger electrolytic capacitors for power applications, means an enormous demand for suitable carrier tapes. It is estimated that the capacitor segment will consume over 350 million units of paper carrier tape in 2025. The trend towards smaller capacitor sizes to enable further miniaturization of electronic devices directly amplifies the need for precisely designed paper carrier tapes that can securely hold these components.

The Resistor segment also plays a vital role, contributing an estimated 300 million units in 2025. The sheer volume of resistors produced globally, especially for the ubiquitous printed circuit boards found in almost every electronic device, ensures a consistent and substantial demand for paper carrier tapes. While often simpler in design compared to capacitors, the need for mass handling and protection during transit remains critical.

The Inductors segment, while smaller in volume compared to capacitors and resistors, is also experiencing growth, estimated at around 150 million units in 2025. The increasing complexity of power management circuits in modern electronics, including those in electric vehicles and high-performance computing, drives the demand for specialized inductors that require precise and secure packaging.

The dominance of Asia Pacific is further reinforced by the presence of key global manufacturers and a strong ecosystem of supporting industries. Companies like Zhejiang Jiemei Electronic And Technology, SEWATE, Oji F-Tex, Sierra Electronics, YAC Garter, Lasertek, Daio Paper, Hansol Korea, and Mavat have a significant presence in the region, either through manufacturing facilities or strong distribution networks. This localized production and supply chain efficiency contribute to the region's market leadership. The ongoing technological advancements in manufacturing processes within Asia Pacific also ensure that the region remains at the forefront of innovation in paper carrier tape production, further solidifying its dominant position. The competitive pricing strategies adopted by manufacturers in the region also make it an attractive market for global electronics producers.

Several key factors are acting as growth catalysts for the electronic components paper carrier tape industry. The escalating demand for miniaturized and portable electronic devices, ranging from smartphones to IoT sensors, necessitates the precise and secure packaging offered by carrier tapes. The continuous advancement and adoption of automation in electronics manufacturing globally are paramount, as high-speed pick-and-place machines rely heavily on the dimensional stability and reliability of paper carrier tapes for efficient component feeding. Furthermore, the burgeoning growth of the automotive electronics sector, particularly in the realm of electric vehicles and advanced driver-assistance systems, is driving the need for specialized carrier tapes capable of handling an increasing array of sophisticated components.

This comprehensive report provides an exhaustive analysis of the Electronic Components Paper Carrier Tape market, offering deep insights into trends, drivers, challenges, and regional dynamics. It meticulously details the market segmentation by type (Slitting, Punched, Embossed) and application (Capacitor, Resistor, Inductors, Other), providing quantitative data and qualitative analysis. The study leverages a robust methodology, incorporating historical data from 2019-2024, a base year of 2025, and an extensive forecast period up to 2033. This report is designed to equip stakeholders with the necessary intelligence to navigate the complexities of the market, identify growth opportunities, and formulate effective business strategies within the evolving landscape of electronic component packaging.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.2%.

Key companies in the market include Zhejiang Jiemei Electronic And Technology, SEWATE, Oji F-Tex, Sierra Electronics, YAC Garter, Lasertek, Daio Paper, Hansol Korea, Mavat.

The market segments include Type, Application.

The market size is estimated to be USD 762 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Electronic Components Paper Carrier Tape," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Electronic Components Paper Carrier Tape, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.