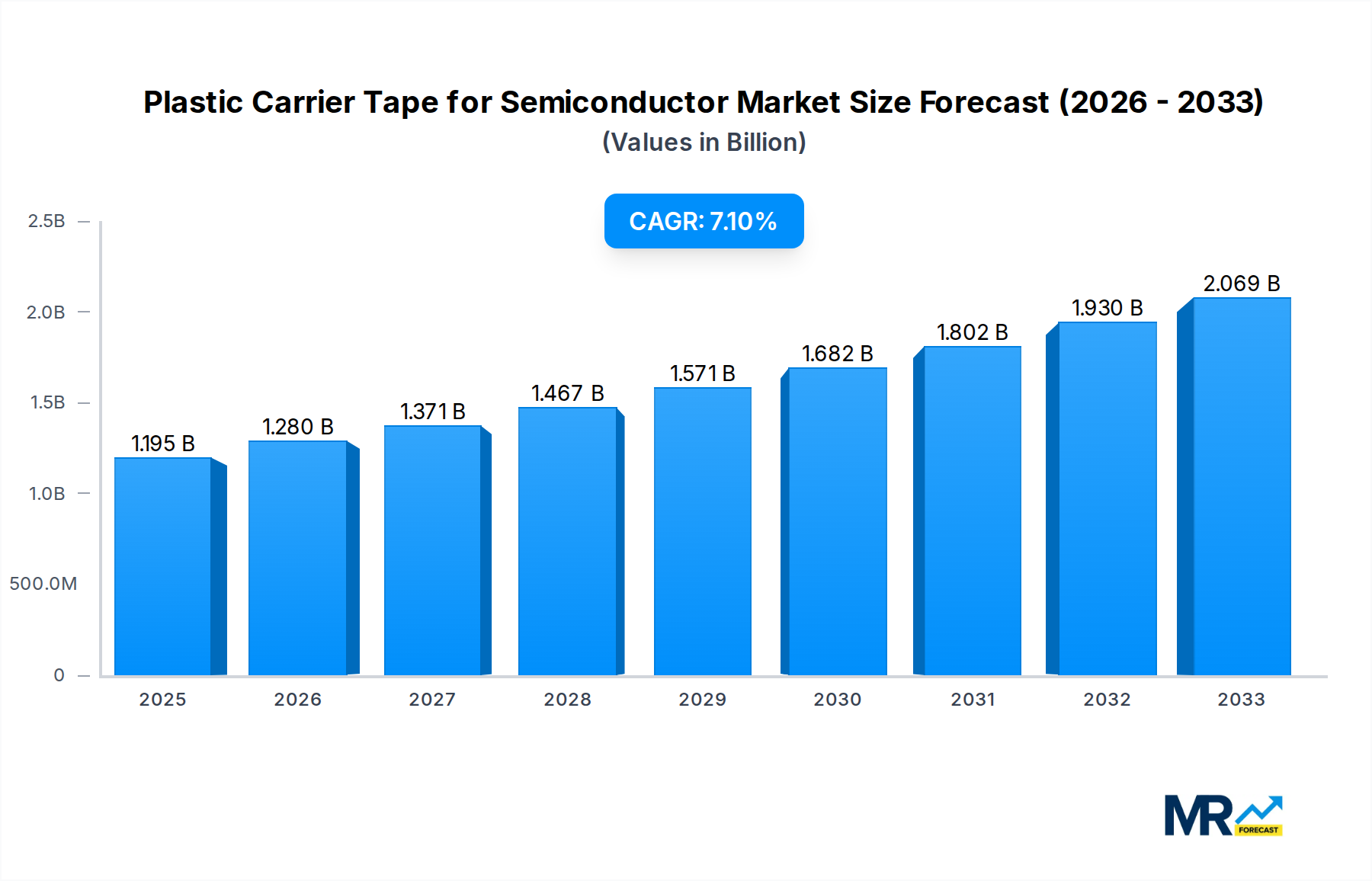

1. What is the projected Compound Annual Growth Rate (CAGR) of the Plastic Carrier Tape for Semiconductor?

The projected CAGR is approximately 7.1%.

Plastic Carrier Tape for Semiconductor

Plastic Carrier Tape for SemiconductorPlastic Carrier Tape for Semiconductor by Type (Polycarbonate, Polystyrene, Polyethylene Terephthalate, Polypropylene, Others), by Application (Power Discrete Devices, Integrated Circuit, Optoelectronics, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global Plastic Carrier Tape for Semiconductor market is projected for robust growth, estimated at $1195 million in 2025 and anticipated to expand at a Compound Annual Growth Rate (CAGR) of 7.1% through 2033. This strong trajectory is propelled by the ever-increasing demand for advanced electronic components across a multitude of industries, including consumer electronics, automotive, telecommunications, and industrial automation. The burgeoning use of semiconductors in these sectors, driven by innovations in areas like artificial intelligence, 5G technology, and the Internet of Things (IoT), directly fuels the need for efficient and reliable packaging solutions like carrier tapes. Manufacturers are increasingly focusing on developing high-performance tapes that offer superior protection against electrostatic discharge (ESD) and physical damage during handling and automated assembly processes. Furthermore, the miniaturization trend in electronics necessitates carrier tapes capable of accommodating smaller and more complex semiconductor devices, pushing innovation in material science and tape design.

The market is segmented by type, with Polycarbonate, Polystyrene, Polyethylene Terephthalate, and Polypropylene holding significant shares, each offering distinct advantages in terms of cost, performance, and application suitability. Polyethylene Terephthalate (PET) is a dominant player due to its excellent clarity, good mechanical strength, and cost-effectiveness, making it suitable for a wide range of semiconductor applications. The application segment is led by Power Discrete Devices and Integrated Circuits, reflecting their widespread adoption in modern electronics. The Asia Pacific region, particularly China and South Korea, is expected to remain the largest and fastest-growing market, owing to its status as a global hub for semiconductor manufacturing and assembly. Key players are actively investing in research and development to enhance product features, expand production capacities, and strengthen their global presence to cater to the evolving needs of the semiconductor industry.

Here's a report description for Plastic Carrier Tape for Semiconductor, incorporating your specific requirements:

The global Plastic Carrier Tape for Semiconductor market is experiencing a robust upward trajectory, with projections indicating a significant surge in demand over the study period of 2019-2033. Driven by the ever-increasing miniaturization and complexity of semiconductor devices, the need for reliable and efficient packaging solutions remains paramount. The base year, 2025, serves as a critical benchmark, with estimates for the same year highlighting the current market standing. The forecast period from 2025-2033 anticipates sustained growth, building upon the momentum observed in the historical period of 2019-2024. Key market insights reveal a strong correlation between advancements in consumer electronics, the automotive sector's embrace of sophisticated electronic components, and the expansion of 5G infrastructure, all of which are directly fueling the demand for plastic carrier tapes. The market's evolution is also characterized by a growing emphasis on material innovation, with manufacturers actively researching and developing tapes with enhanced properties such as improved ESD (Electrostatic Discharge) protection, higher temperature resistance, and superior dimensional stability to accommodate increasingly sensitive and advanced semiconductor packages. The shift towards automation in semiconductor manufacturing further amplifies the need for standardized and high-precision carrier tapes, making them indispensable in high-volume production environments. Emerging trends also point towards a greater adoption of specialized carrier tapes for niche applications, such as those in the medical device and industrial automation sectors, which require tailored solutions to meet unique performance and regulatory demands. The market is also witnessing a consolidation phase, with strategic collaborations and acquisitions aimed at expanding product portfolios and geographical reach. Looking ahead, the market is poised for continued expansion, propelled by the ongoing digital transformation across industries and the relentless pursuit of next-generation semiconductor technologies. The increasing adoption of wafer-level packaging technologies is also creating new opportunities for specialized carrier tape designs. Furthermore, the growing focus on sustainable manufacturing practices is prompting a shift towards eco-friendly materials and production processes within the carrier tape industry, albeit this remains an evolving aspect. The market's resilience and adaptability are key to its sustained growth in the face of evolving technological landscapes and global economic dynamics.

The market for Plastic Carrier Tape for Semiconductor is propelled by a confluence of powerful driving forces, predominantly stemming from the relentless innovation and expansion within the semiconductor industry itself. The exponential growth in the production of Integrated Circuits (ICs) and microprocessors, essential for powering everything from smartphones and laptops to advanced automotive systems and artificial intelligence hardware, directly translates into an escalating requirement for carrier tapes. As semiconductor devices become smaller, more complex, and increasingly sensitive, the need for protective and precisely dimensioned packaging solutions becomes critically important. Furthermore, the burgeoning Internet of Things (IoT) ecosystem, with its vast array of connected devices, necessitates a significant increase in the manufacturing of specialized semiconductors, each requiring dedicated carrier tape solutions for efficient handling and assembly. The automotive industry's deep dive into electrification and autonomous driving technologies is another significant contributor, as these applications demand a substantially higher number of sophisticated electronic components, thereby boosting the demand for carrier tapes. Advancements in optoelectronics, including the widespread adoption of LEDs and advanced display technologies, also contribute to this market's expansion. The increasing demand for higher bandwidth and faster data transfer speeds, epitomized by the rollout of 5G networks, is spurring the development and production of advanced semiconductors that, in turn, require advanced carrier tape solutions for their packaging.

Despite the optimistic growth outlook, the Plastic Carrier Tape for Semiconductor market faces several significant challenges and restraints that could temper its expansion. One of the primary hurdles is the inherent volatility of the semiconductor industry itself, which is subject to cyclical fluctuations in demand and rapid technological obsolescence. This unpredictability can make long-term capacity planning and investment decisions for carrier tape manufacturers more complex. The increasing pressure for cost reduction throughout the semiconductor supply chain also poses a challenge, forcing carrier tape producers to optimize their manufacturing processes and material sourcing to maintain competitive pricing. Furthermore, the development and adoption of alternative packaging technologies, such as wafer-level packaging or advanced substrate integration, could potentially reduce the reliance on traditional carrier tapes in certain applications, although carrier tapes often remain integral to these processes. Stringent regulatory requirements and environmental concerns, particularly regarding the use of certain plastics and their disposal, can also impose additional compliance costs and necessitate the exploration of more sustainable material alternatives, which may not always be cost-effective. Supply chain disruptions, whether due to geopolitical events, natural disasters, or raw material shortages, can also impact the availability and pricing of essential materials for carrier tape production. The high precision required for carrier tape manufacturing, coupled with the need for continuous research and development to keep pace with semiconductor advancements, demands significant capital investment, which can be a barrier for smaller players. Finally, the intricate nature of ESD protection and the need for consistent performance across diverse environmental conditions present ongoing technical challenges for manufacturers.

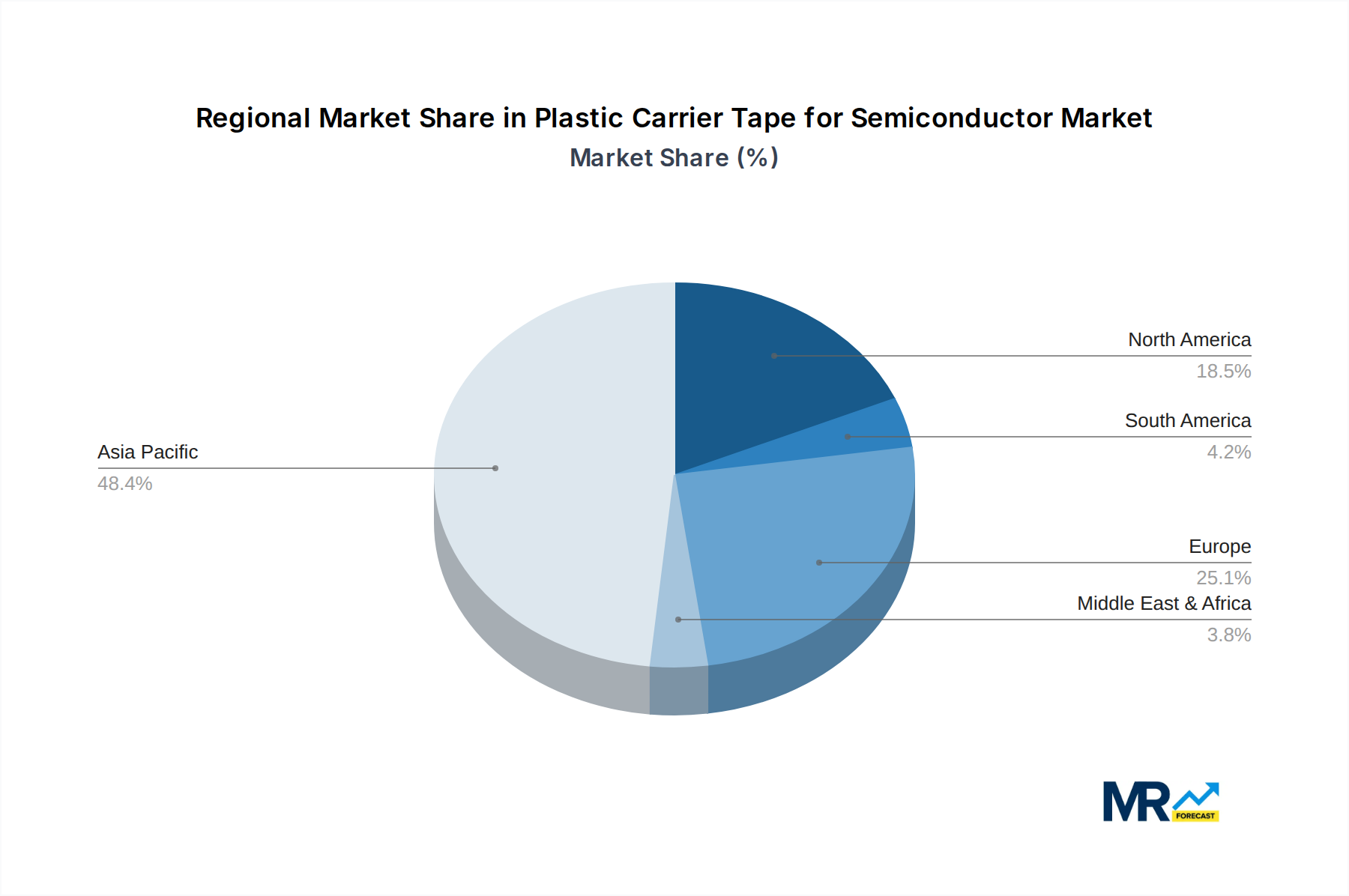

The Plastic Carrier Tape for Semiconductor market exhibits distinct regional dominance and segment leadership, with Asia Pacific emerging as the powerhouse due to its concentration of semiconductor manufacturing facilities. This region's supremacy is underpinned by countries like China, Taiwan, South Korea, and Japan, which house a vast ecosystem of semiconductor foundries, assembly, and testing houses.

Key Regions/Countries Dominating the Market:

Asia Pacific:

North America: A significant market driven by its strong presence in semiconductor design, research and development, and the increasing adoption of advanced electronics in automotive and industrial applications. The US is a key consumer of carrier tapes for its advanced chip manufacturers and high-tech industries.

Europe: Demonstrates steady growth driven by the automotive sector's demand for advanced semiconductors and the region's focus on industrial automation and emerging technologies.

Dominant Segments:

Within the Plastic Carrier Tape for Semiconductor market, the Integrated Circuit (IC) segment stands out as the most dominant. This dominance is directly attributable to the sheer volume and diversity of ICs manufactured globally, encompassing microprocessors, memory chips, application-specific integrated circuits (ASICs), and various other logic and analog devices. The continuous drive for smaller form factors, higher performance, and increased functionality in ICs necessitates the use of precision-engineered carrier tapes to ensure their safe and efficient handling throughout the manufacturing process.

Type Segment: Polyethylene Terephthalate (PET) is expected to be a leading type of plastic carrier tape. PET offers a favorable balance of properties including good dimensional stability, excellent transparency (allowing for visual inspection), adequate ESD protection when properly treated, and cost-effectiveness for high-volume applications. While Polycarbonate (PC) offers superior temperature resistance and mechanical strength for demanding applications, and Polystyrene (PS) provides a more economical option, PET's versatility and widespread adoption in standard IC packaging make it a dominant force. Polypropylene (PP) finds its niche in specific applications where its chemical resistance or flexibility is prioritized. The "Others" category will likely encompass specialized polymer blends or advanced composite materials catering to niche requirements.

Application Segment: The Integrated Circuit (IC) application segment is by far the largest and most influential. This broad category encompasses a vast array of semiconductor devices, from basic microcontrollers and memory chips to complex CPUs and GPUs. The relentless demand for computing power in consumer electronics, servers, data centers, and emerging AI applications ensures a constant and growing need for carrier tapes to package these ICs. The miniaturization and increasing complexity of ICs further amplify this demand, requiring tapes with tighter tolerances and enhanced protective features.

In terms of market share, the Asia Pacific region will continue to hold the lion's share of the global Plastic Carrier Tape for Semiconductor market, driven by its unparalleled manufacturing infrastructure for ICs. Countries like Taiwan and China will remain at the forefront, with South Korea and Japan contributing significantly to the regional dominance. The integrated circuit application segment, owing to its sheer volume and diverse product range, will therefore also be the primary driver of market value and volume.

Several key factors are acting as significant growth catalysts for the Plastic Carrier Tape for Semiconductor industry. The relentless advancement of semiconductor technology, leading to smaller, more powerful, and increasingly complex chips, necessitates specialized carrier tapes for their protection and handling. The burgeoning Internet of Things (IoT) ecosystem, with its expanding network of interconnected devices, is creating a massive demand for a wide array of semiconductors, thereby boosting carrier tape consumption. Furthermore, the rapid growth of the automotive sector, driven by electrification, advanced driver-assistance systems (ADAS), and infotainment technologies, requires a significant increase in the number of embedded semiconductors, further fueling market growth.

This comprehensive report offers an in-depth analysis of the Plastic Carrier Tape for Semiconductor market, providing granular insights into its dynamics and future trajectory. The study meticulously examines market size and forecasts for the period 2019-2033, with a specific focus on the base year 2025 and the extended forecast period of 2025-2033, building upon a detailed historical analysis from 2019-2024. The report delves into the key market drivers and restraints, dissecting the forces that propel and impede market growth. It also provides a thorough regional analysis, highlighting the dominant markets and emerging opportunities. Furthermore, the report segments the market by Type (Polycarbonate, Polystyrene, Polyethylene Terephthalate, Polypropylene, Others) and Application (Power Discrete Devices, Integrated Circuit, Optoelectronics, Others), offering detailed insights into the performance of each segment. Leading industry players are profiled, alongside significant recent and projected developments, providing a holistic view of the competitive landscape and future innovations. This report is an indispensable resource for stakeholders seeking to understand and capitalize on the evolving Plastic Carrier Tape for Semiconductor market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.1%.

Key companies in the market include 3M, Advantek, Shin-Etsu Polymer, Nissho Corporation, Zhejiang Jiemei Electronic Technology, NIPPO CO.,LTD, YAC GARTER, U-PAK, C-Pak, ePAK International, ROTHE, Sumitomo Bakelite, Tek Pak, Jiangyin Winpack, SEKISUI SEIKEI, Asahi Kasei, Kanazu Giken, Taiwan Carrier Tape Enterprise Co., Ltd, LaserTek, JSK Co.,Ltd, Miyata System, Hwa Shu Enterpris, Xiamen Hatro Electronics.

The market segments include Type, Application.

The market size is estimated to be USD 1195 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Plastic Carrier Tape for Semiconductor," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Plastic Carrier Tape for Semiconductor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.