1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive-grade SiC Power Device?

The projected CAGR is approximately 22.5%.

Automotive-grade SiC Power Device

Automotive-grade SiC Power DeviceAutomotive-grade SiC Power Device by Type (Automotive Grade SiC MOSFET Module, Automotive Grade SiC MOSFET Discrete, Automotive Grade SiC SBD, World Automotive-grade SiC Power Device Production ), by Application (Main Inverter, EV On-Board Chargers, DC/DC Converter, EV Charging, World Automotive-grade SiC Power Device Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

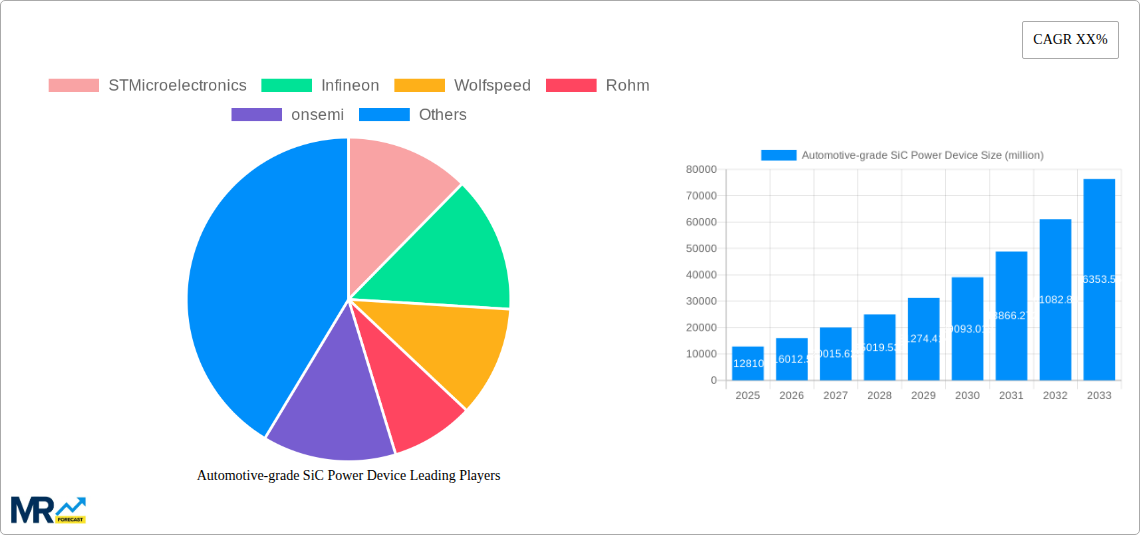

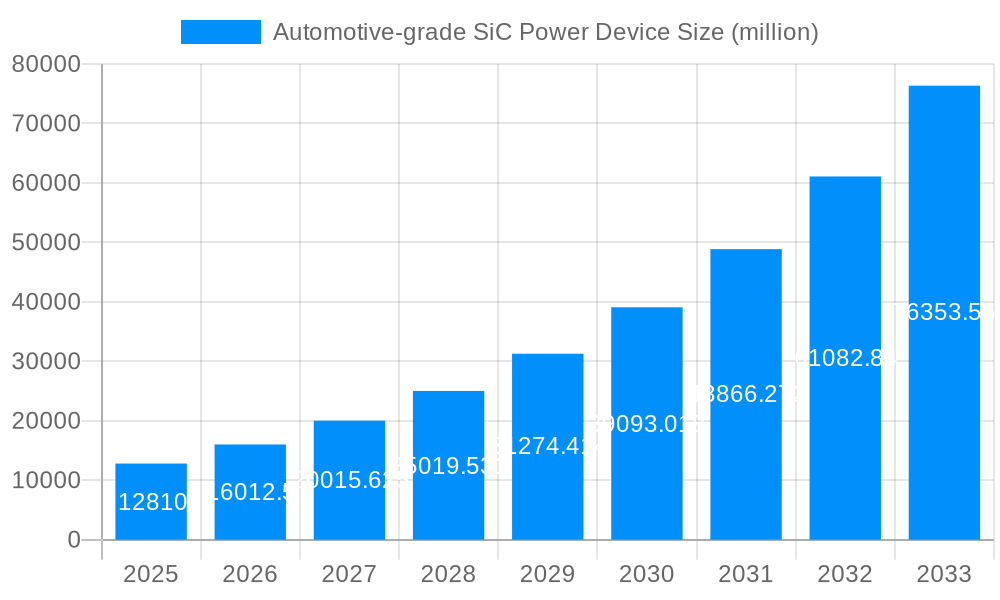

The global automotive-grade Silicon Carbide (SiC) power device market is set for significant expansion, driven by the rapid adoption of electric vehicles (EVs) and the growing need for advanced automotive electronics. The market is projected to reach a size of $12,810 million by 2025, with a Compound Annual Growth Rate (CAGR) of approximately 25% for the forecast period 2025-2033. SiC MOSFET modules and discrete components are crucial for enhancing EV powertrain efficiency, offering superior power density and thermal management over traditional silicon devices. Innovations in EV charging infrastructure, including DC/DC converters and on-board chargers, further boost demand by enabling faster charging and extended vehicle range. Increasing regulatory pressure for reduced emissions and growing consumer preference for sustainable transportation are key factors fueling this growth.

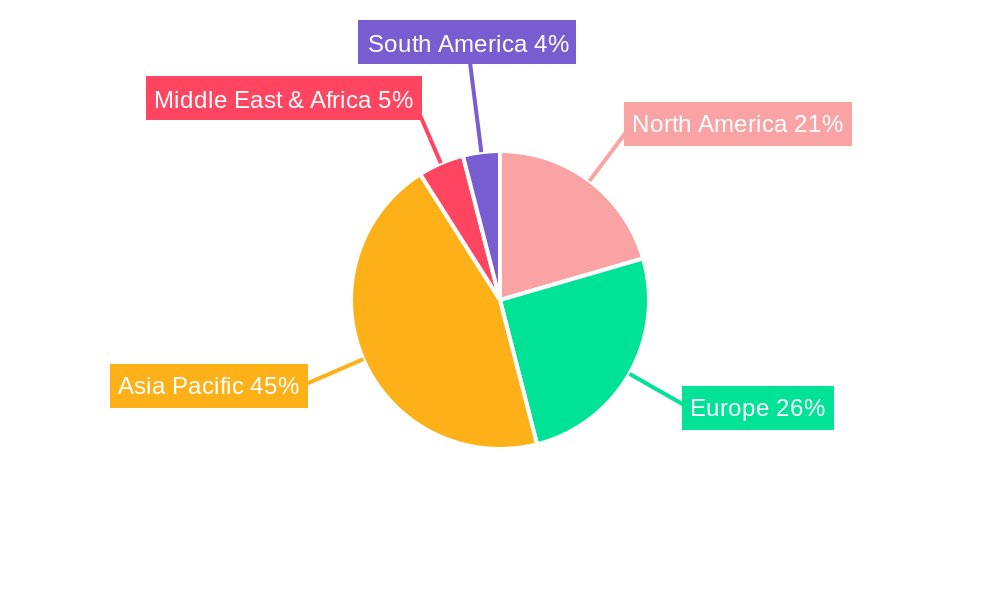

The inherent advantages of SiC in high-voltage applications, its ability to operate at higher temperatures, and its contribution to reducing the weight and size of power electronics systems are vital for EV design. Leading manufacturers are investing heavily in research, development, and manufacturing capacity, indicating strong market confidence. While initial cost premiums for SiC devices and supply chain development present potential challenges, ongoing technological advancements and economies of scale are expected to overcome these hurdles. The Asia Pacific region, especially China, is anticipated to lead in both production and consumption due to its prominent position in the global EV market.

The global automotive-grade Silicon Carbide (SiC) power device market is poised for a monumental surge, projected to witness a staggering growth from approximately 15 million units in 2019 to an estimated 120 million units by 2025, and further escalating to an impressive 500 million units by 2033. This exponential trajectory underscores the transformative impact of SiC technology on electric vehicles (EVs) and the broader automotive landscape. The study period of 2019-2033, with a base year of 2025, highlights the rapid evolution and adoption of these advanced power semiconductors. The historical period of 2019-2024 has laid the groundwork, characterized by initial investments and growing awareness of SiC’s superior performance over traditional silicon-based devices. As the market matures and economies of scale are realized, we anticipate a sustained and aggressive expansion. The primary driver for this growth is the relentless pursuit of higher efficiency, increased power density, and enhanced thermal performance in electric powertrains. SiC devices, with their inherent advantages in handling higher voltages and temperatures, are crucial for optimizing EV performance, extending driving range, and enabling faster charging capabilities. The estimated production for 2025 alone is projected to reach 120 million units, signifying a critical inflection point in market penetration. This expansion is not uniform, with certain segments and applications experiencing more rapid adoption than others. For instance, the demand for SiC MOSFET modules in main inverters is already outstripping supply, as automotive manufacturers strive to reduce the size, weight, and energy losses of their powertrains. Similarly, SiC Schottky Barrier Diodes (SBDs) are becoming indispensable for their fast switching speeds and low forward voltage drop, contributing to overall system efficiency. The forecast period of 2025-2033 will be defined by further technological advancements, including the development of higher voltage and higher current SiC devices, as well as the exploration of novel packaging solutions to maximize performance and reliability in demanding automotive environments. The global automotive-grade SiC power device production is not just a quantitative expansion but a qualitative shift towards a more sustainable and high-performance future for mobility.

The meteoric rise of automotive-grade SiC power devices is fueled by a confluence of powerful driving forces, spearheaded by the global imperative for electrification and decarbonization in the automotive sector. Governments worldwide are implementing stringent emission regulations and offering incentives for EV adoption, creating a robust demand for efficient and high-performance electric powertrains. SiC technology, with its ability to significantly improve power conversion efficiency, is a cornerstone in meeting these demands. The inherent advantages of SiC over conventional silicon (Si) are undeniable; it offers higher bandgap, superior thermal conductivity, and greater breakdown electric field strength. These properties translate directly into lighter, smaller, and more efficient power electronics for EVs, leading to extended driving ranges and reduced charging times. Furthermore, the increasing consumer expectation for faster charging infrastructure and longer battery life directly correlates with the adoption of SiC in on-board chargers and main inverters. As the cost of SiC wafer production continues to decrease due to advancements in manufacturing techniques and economies of scale, its economic viability for mass-market automotive applications becomes increasingly compelling. The competitive landscape among automotive OEMs to launch more advanced and competitive EV models also acts as a significant catalyst, pushing them to integrate cutting-edge technologies like SiC to differentiate their offerings.

Despite the overwhelmingly positive outlook, the automotive-grade SiC power device market faces several significant challenges and restraints that could temper its growth trajectory. One of the primary hurdles remains the cost of SiC materials and manufacturing. While prices are declining, SiC wafers and devices are still considerably more expensive than their silicon counterparts. This cost premium can be a significant barrier for mass-market adoption, especially in lower-cost vehicle segments. Supply chain constraints and capacity limitations also present a challenge. The rapid growth in demand has put a strain on the existing manufacturing infrastructure for SiC, leading to potential bottlenecks and extended lead times for critical components. Ensuring a stable and scalable supply chain that can meet the projected demand of hundreds of millions of units by 2033 is crucial. Reliability and long-term performance validation in the harsh automotive environment are ongoing concerns. While SiC offers superior thermal and electrical characteristics, comprehensive testing and validation are required to ensure its longevity and robustness under extreme temperature fluctuations, vibration, and electrical stress. Developing standardized testing protocols and proving long-term reliability comparable to or exceeding that of silicon devices is paramount for widespread acceptance. Finally, the availability of skilled engineers and technicians with expertise in SiC technology and its integration into automotive systems can be a limiting factor. The specialized nature of SiC requires a new skill set, and developing this talent pool will be essential for continued innovation and successful implementation.

The global automotive-grade SiC power device market is characterized by dominant regions and segments that are shaping its future.

Key Regions/Countries to Dominate:

Key Segments to Dominate:

The World Automotive-grade SiC Power Device Production volume is a direct reflection of the success in these key segments and regions. The projected output of 500 million units by 2033 is heavily influenced by the demand for SiC MOSFET modules in main inverters, driven by the booming EV market, particularly in China. The increasing integration of SiC across the entire EV power train, from charging to propulsion, underpins the sustained growth in these dominant segments and regions.

Several growth catalysts are propelling the automotive-grade SiC power device industry forward. The most significant is the escalating adoption of electric vehicles (EVs), driven by environmental concerns and supportive government policies. SiC's inherent advantages in efficiency, power density, and thermal performance are critical for meeting the performance demands of modern EVs, including extended range and faster charging. Furthermore, the continuous innovation in SiC material and device fabrication is leading to improved performance and reduced manufacturing costs, making SiC more accessible for mass-market applications. The development of robust and reliable SiC components, validated for the harsh automotive environment, is also a key catalyst, building trust and accelerating adoption among automotive manufacturers.

This report provides an in-depth and comprehensive analysis of the automotive-grade SiC power device market, offering critical insights for stakeholders. It delves into the intricate dynamics shaping the industry, from market size and growth projections to technological advancements and competitive landscapes. The report meticulously examines the historical performance and forecasts future trends, with a particular focus on the estimated production of 120 million units by 2025 and the projected 500 million units by 2033. It highlights the key drivers, such as the accelerating shift towards electrification in the automotive sector and the superior performance characteristics of SiC technology. Simultaneously, it addresses the challenges and restraints, including cost implications and supply chain considerations, offering a balanced perspective. The detailed segmentation by device type (MOSFET Modules, MOSFET Discrete, SBDs) and application (Main Inverter, On-Board Chargers, DC/DC Converters, EV Charging) provides granular understanding of market dynamics. Furthermore, the report identifies the leading players and their contributions, alongside significant developments that are revolutionizing the sector. This comprehensive coverage empowers businesses to make informed strategic decisions and capitalize on the immense opportunities within the burgeoning automotive-grade SiC power device market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 22.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 22.5%.

Key companies in the market include STMicroelectronics, Infineon, Wolfspeed, Rohm, onsemi, BYD Semiconductor, Microchip (Microsemi), Mitsubishi Electric (Vincotech), Semikron Danfoss, Fuji Electric, Navitas (GeneSiC), Toshiba, Qorvo (UnitedSiC), San'an Optoelectronics, Littelfuse (IXYS), CETC 55, WeEn Semiconductors, BASiC Semiconductor, SemiQ, Diodes Incorporated, SanRex, Alpha & Omega Semiconductor, Bosch, KEC Corporation, PANJIT Group, Nexperia, Vishay Intertechnology, Zhuzhou CRRC Times Electric, China Resources Microelectronics Limited, StarPower, Yangzhou Yangjie Electronic Technology, Guangdong AccoPower Semiconductor, Changzhou Galaxy Century Microelectronics, Hangzhou Silan Microelectronics, Cissoid, SK powertech, InventChip Technology, Hebei Sinopack Electronic Technology, Oriental Semiconductor, Jilin Sino-Microelectronics, PN Junction Semiconductor (Hangzhou), United Nova Technology.

The market segments include Type, Application.

The market size is estimated to be USD 2225.95 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive-grade SiC Power Device," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive-grade SiC Power Device, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.