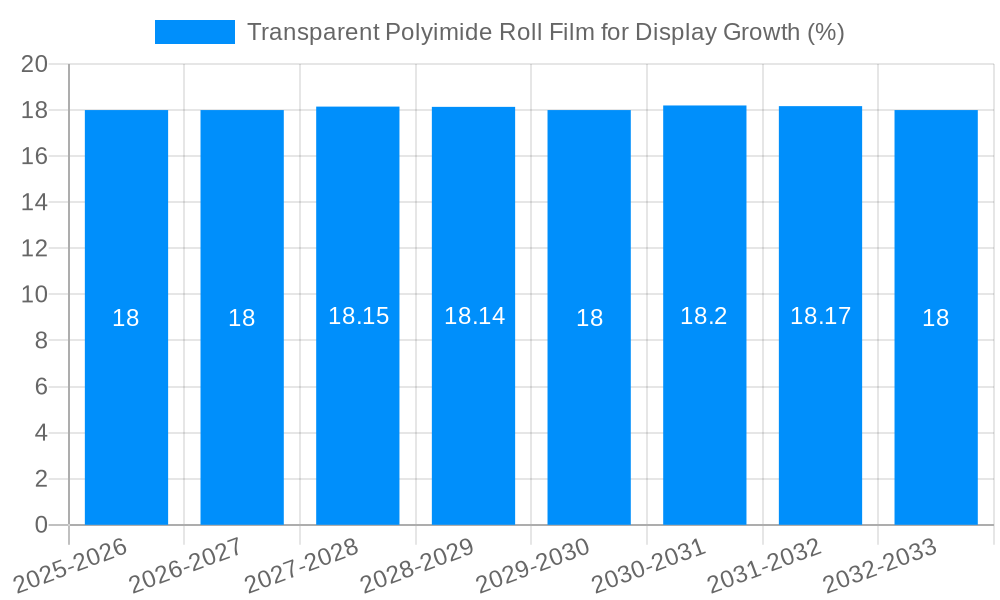

1. What is the projected Compound Annual Growth Rate (CAGR) of the Transparent Polyimide Roll Film for Display?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Transparent Polyimide Roll Film for Display

Transparent Polyimide Roll Film for DisplayTransparent Polyimide Roll Film for Display by Type (Thickness: 15μm-25μm, Thickness: below 15μm, Others, World Transparent Polyimide Roll Film for Display Production ), by Application (Cell Phone, Computer, Others, World Transparent Polyimide Roll Film for Display Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

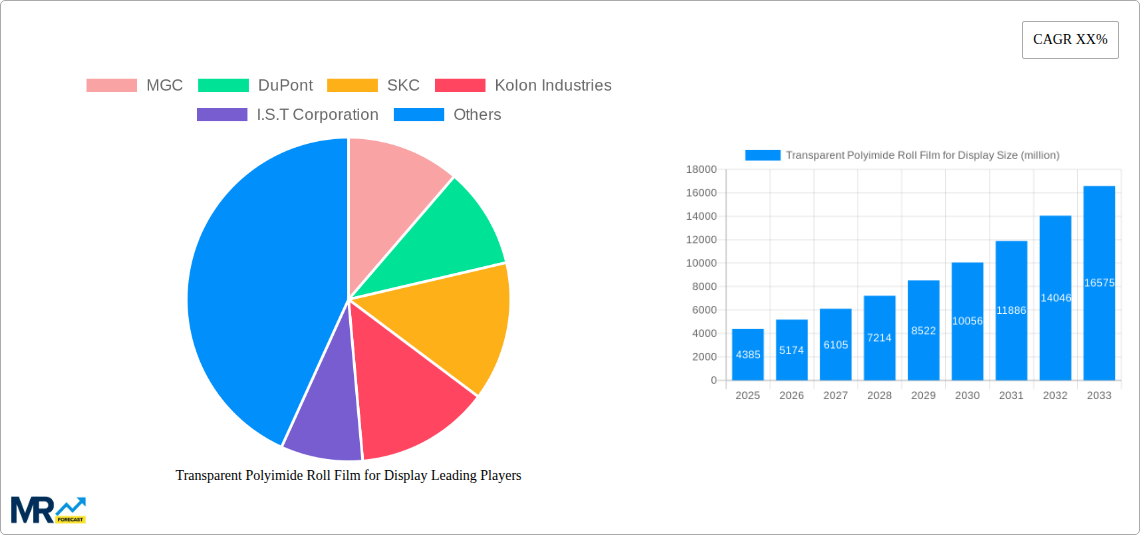

The global Transparent Polyimide (TPI) roll film market for display production is poised for significant expansion, driven by the burgeoning demand for advanced electronic displays. With a current market size of approximately $4,385 million in 2025, the industry is projected to experience a robust Compound Annual Growth Rate (CAGR) of roughly 18-20% over the forecast period from 2025 to 2033. This growth is primarily fueled by the increasing adoption of TPI films in high-end smartphones, flexible and foldable displays, and other wearable electronics, where its unique properties like superior optical clarity, high thermal stability, and mechanical flexibility are indispensable. The rising consumer preference for larger, more immersive, and durable displays across various electronic devices directly translates into a higher demand for TPI roll films. Furthermore, advancements in display technologies, such as OLED and micro-LED, which benefit greatly from the characteristics of TPI, are acting as significant market accelerators. The development of thinner and more resilient TPI films, particularly those below 15μm thickness, is also a key trend, catering to the miniaturization and portability demands of modern gadgets.

Despite the optimistic outlook, certain restraints could temper the growth trajectory. The high cost of raw materials and complex manufacturing processes associated with TPI films can pose a challenge, potentially impacting affordability and wider market penetration, especially in cost-sensitive segments. However, ongoing research and development efforts are focused on optimizing production methods and exploring alternative material sourcing to mitigate these cost pressures. Geographically, the Asia Pacific region, led by China, South Korea, and Japan, is expected to dominate the market, owing to its strong presence in electronics manufacturing and a high concentration of key TPI film producers and display manufacturers. North America and Europe are also significant markets, driven by innovation in consumer electronics and the growing demand for premium display solutions. The market segmentation indicates a strong focus on thinner TPI films (below 15μm and 15μm-25μm) for advanced display applications, with cell phones and computers being the primary application areas.

This report offers an in-depth examination of the global Transparent Polyimide Roll Film for Display market, charting its trajectory from the historical period of 2019-2024 through the base year of 2025 and extending into a detailed forecast period of 2025-2033. The analysis will leverage a robust dataset, including an estimated production volume of 350 million square meters in 2025, projected to reach 780 million square meters by 2033. Our study meticulously dissects market dynamics, identifying key trends, driving forces, challenges, and regional dominance, while highlighting the crucial role of leading players and significant industry developments.

The global Transparent Polyimide (TPI) roll film market for display applications is poised for robust expansion, driven by an insatiable demand for advanced display technologies across a myriad of consumer electronics. The core trend revolves around the increasing adoption of flexible and foldable displays, where TPI's inherent properties – exceptional transparency, high thermal stability, superior mechanical strength, and excellent dielectric performance – make it an indispensable substrate material. As manufacturers push the boundaries of device form factors, from bendable smartphones and rollable televisions to augmented and virtual reality headsets, the need for thin, lightweight, and durable transparent films intensifies. The market is witnessing a significant shift towards thinner films, with a growing emphasis on segments below 15μm, catering to the ever-decreasing thickness requirements of next-generation devices. Furthermore, advancements in manufacturing processes, including improved coating and curing techniques, are leading to enhanced optical clarity and reduced surface imperfections, further solidifying TPI's position. The market is also characterized by an evolving landscape of applications, moving beyond traditional cell phones to include a wider array of consumer electronics such as tablets, laptops, smartwatches, and automotive displays. This diversification of end-use applications fuels consistent demand. The market's growth is further amplified by a concerted effort from leading players to develop innovative TPI formulations that offer improved scratch resistance, enhanced flexibility, and better adhesion properties, thereby addressing specific performance requirements of diverse display technologies like OLED, MicroLED, and Quantum Dot. The projected market size in 2025 is estimated at US$ 1.2 billion, with a projected CAGR of 12.5% during the forecast period, underscoring its significant growth potential. The production volume is also expected to surge, with an estimated 350 million square meters in 2025, growing to approximately 780 million square meters by 2033.

The relentless pursuit of innovation in consumer electronics serves as the primary engine driving the transparent polyimide roll film for display market. The burgeoning popularity of flexible, foldable, and even rollable display technologies is a monumental catalyst, as TPI's unique combination of optical clarity, mechanical robustness, and thermal stability makes it the ideal substrate material for these advanced form factors. Devices such as foldable smartphones, which have transitioned from a niche concept to mainstream adoption, are heavily reliant on TPI's ability to withstand repeated bending and unfolding without compromising display integrity. Similarly, the development of wearable electronics, including smartwatches and AR/VR headsets, demands ultra-thin, lightweight, and highly durable display substrates, areas where TPI excels. The expanding application spectrum beyond mobile devices, encompassing automotive displays, transparent televisions, and flexible lighting solutions, further broadens the market's growth horizons. Continuous advancements in TPI manufacturing processes, leading to improved transparency, reduced yellowing, and enhanced surface uniformity, are also crucial. The increasing emphasis on energy efficiency and miniaturization in electronic devices indirectly benefits TPI, as its thin profile and excellent dielectric properties contribute to these goals. Finally, the ongoing research and development efforts focused on creating even more advanced TPI variants with superior scratch resistance, anti-glare properties, and improved optical performance will undoubtedly sustain and accelerate market expansion in the coming years.

Despite its promising growth trajectory, the transparent polyimide roll film for display market faces several significant challenges and restraints. A primary concern revolves around the high manufacturing cost associated with producing high-purity, defect-free TPI films on a large scale. The complex synthesis and processing techniques required can lead to a higher price point compared to other flexible display substrate materials, potentially limiting its adoption in cost-sensitive applications or markets. Furthermore, achieving perfect optical clarity and uniformity across large roll films can be technically demanding. Any minor imperfections, such as surface roughness or internal defects, can significantly impact display performance and yield, necessitating stringent quality control measures that further add to production costs. Competition from alternative materials, such as ultra-thin glass (UTG) and other advanced polymers, presents another challenge. While TPI offers unique advantages, UTG, for instance, provides superior scratch resistance and a premium feel, making it a strong contender in certain premium foldable device segments. Scalability of production to meet the exponentially growing demand, especially for thinner films (below 15μm), can also be a bottleneck. Ensuring consistent quality and high throughput for these highly specialized films requires significant investment in advanced manufacturing infrastructure and expertise. Finally, recycling and environmental sustainability concerns associated with polyimide materials, although less pronounced for thin films used in high-value electronics, might become a more significant consideration in the long term, potentially influencing material choices.

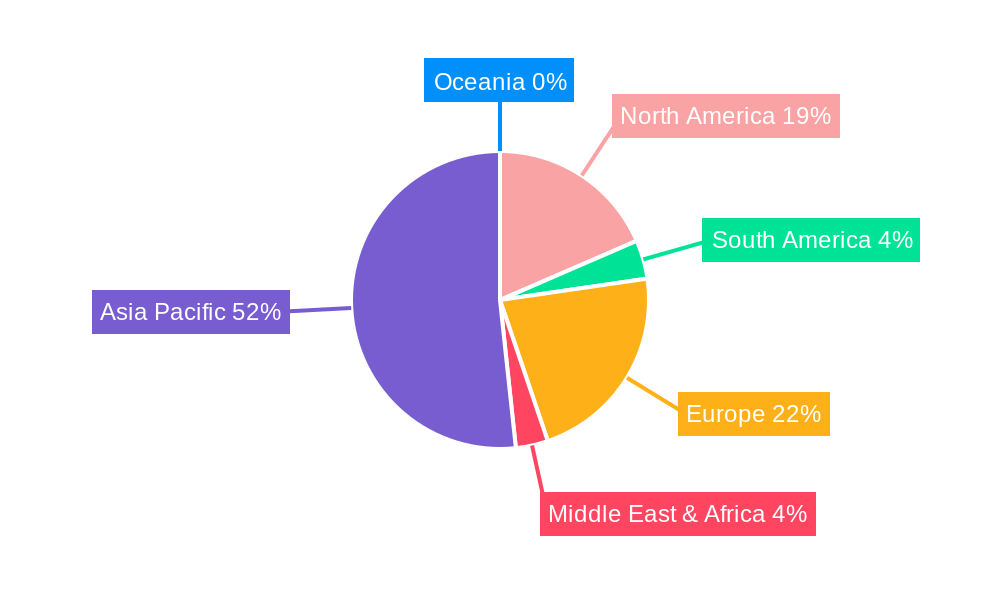

The Asia Pacific region, particularly South Korea, China, and Taiwan, is projected to dominate the global Transparent Polyimide Roll Film for Display market, both in terms of production and consumption. This dominance is intrinsically linked to the region's powerhouse status in the global consumer electronics industry, housing the world's leading display manufacturers and electronic device assemblers.

Dominant Application Segment: Cell Phone: The Cell Phone segment is expected to be the leading application, driven by the explosive growth of the foldable smartphone market. South Korea, with companies like Samsung Display and LG Display at the forefront of flexible display innovation, is a key player. China’s rapidly expanding smartphone manufacturing ecosystem, with companies like BOE and Visionox investing heavily in advanced display technologies, further solidifies this segment's dominance. The demand for TPI in this application is estimated to account for over 60% of the total market by 2025, reaching an estimated 210 million square meters in volume. The continuous evolution of smartphone designs, incorporating larger, more immersive, and more durable displays, ensures a sustained demand for TPI.

Dominant Production Segment: Thickness: 15μm-25μm: While thinner films are gaining traction, the Thickness: 15μm-25μm segment is expected to remain the dominant production segment in the near to medium term, due to its current widespread adoption in many flexible display applications and a more mature production infrastructure. This thickness range offers a balance between flexibility, durability, and cost-effectiveness, making it suitable for a broad spectrum of foldable and flexible devices. By 2025, this segment is estimated to contribute approximately 55% of the total TPI production volume, equating to around 192.5 million square meters.

Emerging Dominance of Thinner Films: Thickness: below 15μm: The Thickness: below 15μm segment, while currently smaller, is poised for the most significant growth. As display technologies advance and manufacturers strive for ever-thinner and lighter devices, the demand for ultra-thin TPI films will surge. China is expected to lead in the production and adoption of these advanced thinner films, supported by government initiatives and substantial R&D investments in next-generation display materials. By 2033, this segment is projected to capture a substantial market share, challenging the dominance of thicker films. The pursuit of truly edge-to-edge displays and the integration of multiple functional layers in foldable devices will necessitate the adoption of films as thin as 10μm or even less.

Regional Production Hubs: Within Asia Pacific, South Korea is a leader in high-performance TPI production, driven by its established display industry. China is rapidly emerging as a major global production hub, characterized by significant investments in advanced manufacturing capabilities and a strong domestic demand. Taiwan also plays a crucial role, with several companies specializing in advanced polymer films. The sheer scale of manufacturing operations in these countries, coupled with their direct proximity to major display panel manufacturers, positions them as the undisputed leaders in both production volume and market penetration. The estimated production volume for the Asia Pacific region in 2025 is projected to exceed 300 million square meters, representing over 85% of the global market.

The growth of the transparent polyimide roll film for display industry is significantly catalyzed by the relentless demand for foldable and flexible displays in smartphones, tablets, and wearable devices. This trend is amplified by ongoing technological advancements in display manufacturing, leading to enhanced optical clarity, durability, and thinner film profiles. Furthermore, the expansion of applications into emerging areas such as automotive displays, augmented/virtual reality devices, and transparent electronics opens up new avenues for growth. Government initiatives supporting advanced materials research and development, coupled with substantial investments from key players in expanding production capacities and improving manufacturing processes, also serve as crucial growth catalysts, ensuring a steady supply of high-quality TPI films to meet escalating global demand.

This comprehensive report delves into the intricate landscape of the transparent polyimide roll film for display market, offering unparalleled insights from its historical evolution to future projections. We meticulously analyze key market trends, dissecting the underlying drivers such as the escalating demand for flexible and foldable displays, which are projected to consume an estimated 210 million square meters of TPI in cell phone applications alone by 2025. Our analysis also addresses the inherent challenges, including high manufacturing costs and competition from alternative materials, while pinpointing the Asia Pacific region as the dominant force in both production and consumption. Furthermore, the report highlights significant industry developments, the strategic initiatives of leading global players, and the critical role of technological advancements in shaping the market's future, ensuring a holistic understanding for stakeholders.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include MGC, DuPont, SKC, Kolon Industries, I.S.T Corporation, NeXolve, Kaneka Corporation, SK Innovation, CEN Electronic Material, Taimide Tech, Sumitomo Chemical, Zhonghui Ruineng Fengyang New Materials, PI Advanced Materials, Ningbo Solartron Technology, Shanghai Energy New Materials, Daoming Optics and Chemical, Shenzhen Rayitek Hi-Tech Film Company.

The market segments include Type, Application.

The market size is estimated to be USD 4385 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Transparent Polyimide Roll Film for Display," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Transparent Polyimide Roll Film for Display, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.