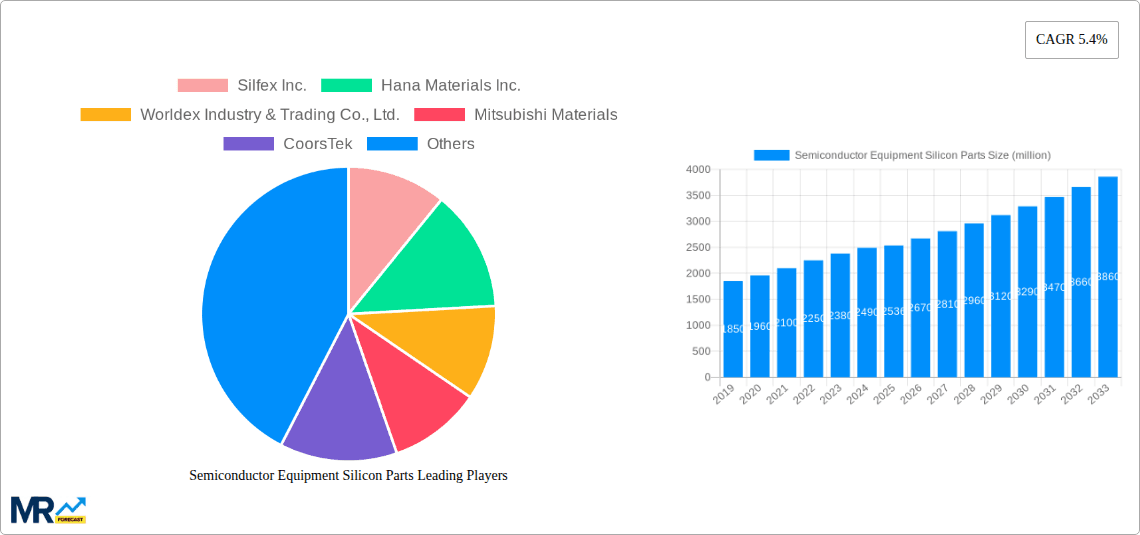

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Equipment Silicon Parts?

The projected CAGR is approximately 5.4%.

Semiconductor Equipment Silicon Parts

Semiconductor Equipment Silicon PartsSemiconductor Equipment Silicon Parts by Type (Silicon Parts for Etching, Silicon Parts for Furnaces & LPCVD), by Application (Etching Process, Semiconductor Heat Treatment Furnaces, LPCVD Process), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

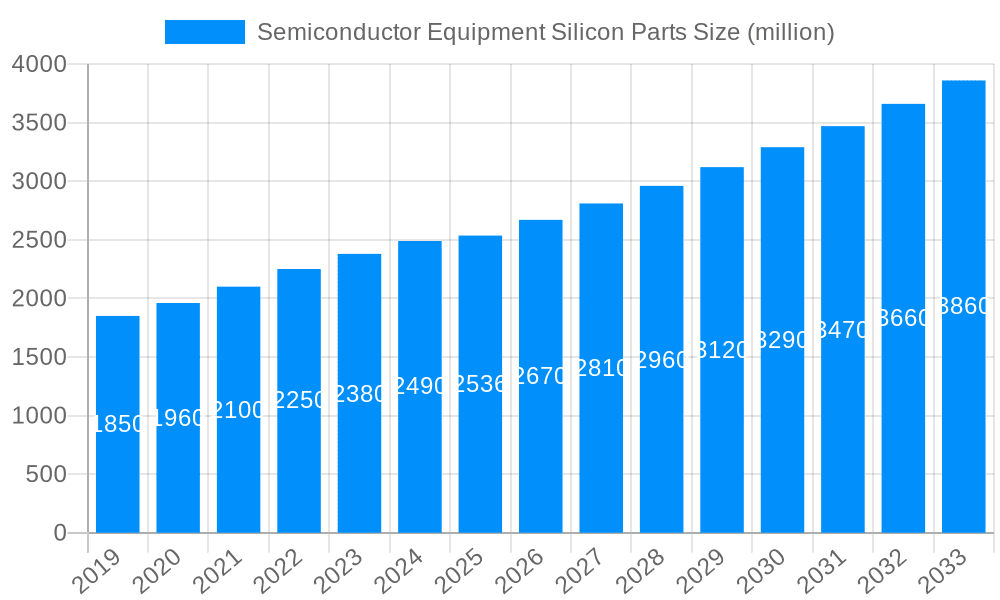

The global Semiconductor Equipment Silicon Parts market is poised for robust growth, projected to reach an estimated value of approximately $2,536 million by 2025 and expand at a Compound Annual Growth Rate (CAGR) of 5.4% through 2033. This dynamic sector is primarily driven by the escalating demand for advanced semiconductors across a multitude of industries, including consumer electronics, automotive, telecommunications, and artificial intelligence. The increasing complexity and miniaturization of semiconductor manufacturing processes necessitate highly pure and precisely engineered silicon components for critical operations like etching and high-temperature furnace applications. The burgeoning adoption of 5G technology, the proliferation of Internet of Things (IoT) devices, and the continuous innovation in advanced computing are significant tailwinds for this market. Furthermore, the growing investments in expanding semiconductor fabrication capacity globally are directly translating into increased demand for these specialized silicon parts.

Key trends shaping the Semiconductor Equipment Silicon Parts market include a heightened focus on material purity and dimensional accuracy to meet stringent semiconductor manufacturing standards. Manufacturers are investing in advanced processing techniques and quality control measures to deliver components that minimize contamination and ensure optimal performance in wafer processing. The market is also witnessing a gradual shift towards more sophisticated silicon materials and coatings to withstand the increasingly aggressive chemical and thermal environments encountered in cutting-edge semiconductor fabrication. While the market is characterized by strong growth prospects, potential restraints include the high cost of raw materials and the complex manufacturing processes involved, which can impact profitability and lead times. Supply chain disruptions, geopolitical factors influencing trade, and the need for continuous technological adaptation to align with evolving semiconductor designs also present challenges that market players must navigate.

This report offers an in-depth analysis of the global Semiconductor Equipment Silicon Parts market, meticulously examining trends, drivers, challenges, and growth opportunities from 2019 to 2033. Utilizing a robust methodology, the report leverages a base year of 2025 for precise estimations, with historical data spanning 2019-2024 and a detailed forecast from 2025-2033. The analysis delves into critical market segments, including Silicon Parts for Etching and Silicon Parts for Furnaces & LPCVD, and their applications within Etching Processes, Semiconductor Heat Treatment Furnaces, and LPCVD Processes. With an anticipated market size in the millions of units, this report provides actionable insights for stakeholders navigating this dynamic and increasingly vital sector of the semiconductor supply chain.

The Semiconductor Equipment Silicon Parts market is witnessing a significant upward trajectory, driven by the insatiable global demand for advanced electronic devices and the relentless innovation within the semiconductor industry. As chip manufacturers push the boundaries of miniaturization, performance, and energy efficiency, the requirement for ultra-pure, precisely engineered silicon components in their manufacturing equipment escalates. These parts, crucial for processes like etching, diffusion, and epitaxy, must withstand extreme temperatures, corrosive chemicals, and vacuum environments with exceptional durability and minimal contamination. The historical period from 2019-2024 has seen consistent growth, fueled by the expansion of wafer fabrication facilities worldwide and the increasing complexity of semiconductor manufacturing processes. The base year of 2025 is projected to be a pivotal point, with further acceleration anticipated in the forecast period of 2025-2033. Key trends include the growing demand for specialized silicon materials with enhanced purity levels and specific thermal and chemical resistance properties. Furthermore, advancements in manufacturing techniques for silicon parts, such as single-crystal silicon growth and precision machining, are enabling the production of more complex geometries and tighter tolerances, essential for next-generation semiconductor devices. The market is also observing a trend towards custom-engineered silicon solutions tailored to specific equipment and process requirements, moving away from a one-size-fits-all approach. The increasing focus on yield improvement and process stability by semiconductor manufacturers directly translates into a higher demand for high-performance and reliable silicon parts. This market is intrinsically linked to the growth of the overall semiconductor industry, and as the latter continues its expansion, the demand for these critical components will undoubtedly follow suit. The sheer volume of chip production, measured in millions of units annually, necessitates a commensurate production of these essential silicon parts.

Several powerful forces are propelling the growth of the Semiconductor Equipment Silicon Parts market. Foremost among these is the exponential growth of the global semiconductor industry itself, fueled by the widespread adoption of technologies such as artificial intelligence, 5G, the Internet of Things (IoT), and electric vehicles. Each of these advancements relies on increasingly sophisticated and densely packed semiconductor chips, requiring more advanced and reliable manufacturing processes. This, in turn, directly translates to a higher demand for the specialized silicon components that form the backbone of the wafer fabrication equipment. Secondly, the ongoing technological race to develop smaller, faster, and more power-efficient chips necessitates continuous innovation in semiconductor manufacturing equipment. This innovation often involves the introduction of new etching chemistries, higher temperature processes, and more precise deposition techniques, all of which demand silicon parts with superior material properties, such as higher purity, improved thermal stability, and enhanced resistance to chemical etching. The increasing complexity of wafer designs and the adoption of advanced packaging technologies also contribute to the demand for specialized silicon parts that can accommodate intricate process flows. Furthermore, government initiatives and incentives aimed at boosting domestic semiconductor manufacturing capabilities in various regions are leading to the construction of new fabrication plants and expansion of existing ones, creating a sustained demand for equipment and its constituent parts.

Despite the robust growth prospects, the Semiconductor Equipment Silicon Parts market is not without its challenges and restraints. One of the primary hurdles is the stringent quality control and high purity requirements associated with silicon parts used in semiconductor manufacturing. Even minute impurities can severely impact wafer yield and device performance, necessitating complex and costly purification and manufacturing processes. This can lead to higher production costs and longer lead times, potentially impacting the pace of adoption for new equipment. Another significant challenge is the volatility in the price and availability of raw materials, particularly high-purity silicon precursors. Fluctuations in the supply chain for these essential raw materials can affect production costs and market stability. Moreover, the semiconductor equipment industry is characterized by long product development cycles and significant capital investment. Companies investing in silicon part manufacturing must contend with these long lead times and the risk of technological obsolescence, as advancements in semiconductor technology can quickly render existing equipment and its components outdated. The highly specialized nature of these silicon parts also means that manufacturers need to possess advanced technical expertise and significant R&D investment to stay competitive. Navigating international trade policies, tariffs, and geopolitical factors can also introduce uncertainties and complexities for global suppliers.

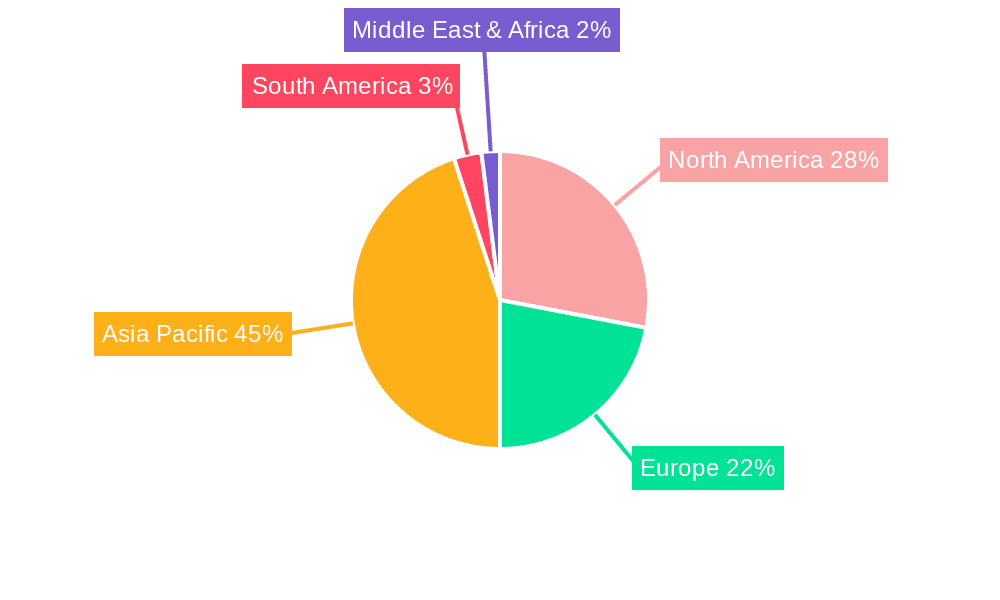

The global Semiconductor Equipment Silicon Parts market is poised for significant growth, with dominance expected to be exerted by specific regions and segments. Asia-Pacific, particularly countries like South Korea, Taiwan, China, and Japan, is projected to be a leading force in this market. This dominance is primarily attributed to the sheer concentration of leading semiconductor manufacturers and wafer fabrication plants within this region. These nations are at the forefront of semiconductor innovation and production, driving substantial demand for advanced manufacturing equipment and, consequently, for high-quality silicon parts. The continuous expansion of existing foundries and the establishment of new ones, often supported by government initiatives, further solidify Asia-Pacific's leading position. For instance, China's ambitious plans to increase its domestic semiconductor production capacity will undoubtedly fuel significant demand for silicon components.

Within this dominant region, Silicon Parts for Furnaces & LPCVD (Low-Pressure Chemical Vapor Deposition) are expected to exhibit particularly strong growth and hold a substantial market share. This segment is critical for key semiconductor manufacturing processes such as diffusion, oxidation, and epitaxy, which are fundamental to chip fabrication. Semiconductor Heat Treatment Furnaces operate at extremely high temperatures and require components that can withstand these harsh conditions without degrading or contaminating the wafer. Similarly, LPCVD processes involve the deposition of thin films of various materials onto silicon wafers under specific temperature and pressure conditions. The silicon parts used in these furnaces and LPCVD chambers, including susceptors, liners, rings, and bell jars, must possess exceptional purity, thermal stability, and chemical inertness to ensure process integrity and maximize wafer yield. As wafer sizes continue to increase (e.g., from 300mm to larger formats) and process complexity escalates, the demand for more advanced and precisely engineered silicon parts for these applications will grow exponentially. The ability to maintain ultra-high purity environments within these furnaces and LPCVD systems is paramount, making the quality and material integrity of the silicon parts indispensable. The forecast period of 2025-2033 will witness a heightened emphasis on these segments as leading chip manufacturers strive for greater efficiency and yield in their high-volume production lines.

The Semiconductor Equipment Silicon Parts industry is experiencing several key growth catalysts. The escalating demand for advanced semiconductor devices across various sectors, including AI, 5G, IoT, and automotive, is a primary driver. This surge in demand necessitates increased wafer fabrication capacity and, consequently, a greater need for the specialized silicon components integral to manufacturing equipment. Furthermore, the ongoing miniaturization of transistors and the push for higher chip densities require more complex and precise manufacturing processes, which in turn, demand higher purity and more advanced silicon parts. Technological advancements in wafer processing, such as the adoption of new materials and intricate multi-layer structures, also contribute to this demand.

This comprehensive report provides an exhaustive analysis of the global Semiconductor Equipment Silicon Parts market, offering critical insights for industry stakeholders. It meticulously examines market trends, delves into the driving forces and challenges shaping the landscape, and identifies key regions and segments poised for dominance. The report leverages a detailed study period from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033, all supported by historical data from 2019-2024. With market size estimations in the millions of units, the report offers actionable intelligence on various silicon part types and applications, enabling strategic decision-making in this vital sector of the semiconductor supply chain.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.4%.

Key companies in the market include Silfex Inc., Hana Materials Inc., Worldex Industry & Trading Co., Ltd., Mitsubishi Materials, CoorsTek, SiFusion, KC Parts Tech., Ltd., RS Technologies Co., Ltd., ThinkonSemi (Fujian Dynafine), Techno Quartz Inc., Chongqing Genori Technology Co., Ltd, Ruijiexinsheng Electronic Technology (WuXi) Co., Ltd, One Semicon Co.,Ltd, Coma Technology Co., Ltd., BC&C, K-max, DS Techno, Ronda Semiconductor, SICREAT(Suzhou) Semitech Co.,Ltd., SICO Technology GmbH, Siliciumbearbeitung Andrea Holm GmbH.

The market segments include Type, Application.

The market size is estimated to be USD 2536 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Semiconductor Equipment Silicon Parts," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Equipment Silicon Parts, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.