1. What is the projected Compound Annual Growth Rate (CAGR) of the Thin-Film Piezo MEMS Foundry?

The projected CAGR is approximately XX%.

Thin-Film Piezo MEMS Foundry

Thin-Film Piezo MEMS FoundryThin-Film Piezo MEMS Foundry by Type (/> MEMS Sensor Foundry, MEMS Actuator Foundry), by Application (/> Consumer Electronics, Industrial, Automotive, Medical, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

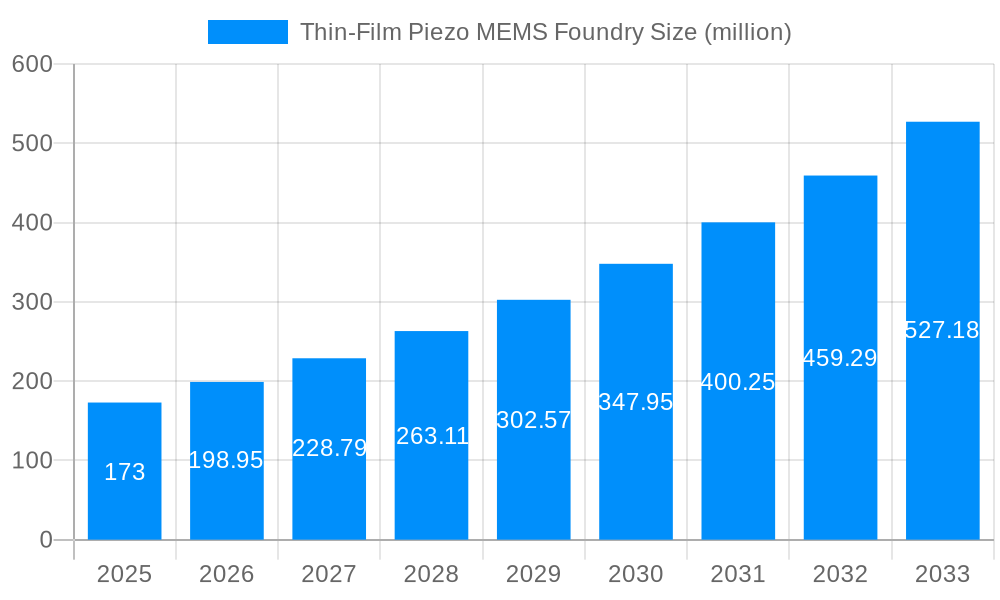

The global Thin-Film Piezo MEMS Foundry market is poised for significant expansion, projected to reach a substantial value of $173 million by 2025, with an estimated Compound Annual Growth Rate (CAGR) of approximately 15%. This robust growth is primarily fueled by the escalating demand for advanced sensors and actuators across a multitude of industries. The proliferation of consumer electronics, including smartphones, wearables, and smart home devices, is a major driver, as these products increasingly integrate sophisticated MEMS components for enhanced functionality. Similarly, the industrial sector is witnessing a surge in adoption of Piezo MEMS for automation, precision manufacturing, and condition monitoring. Automotive applications, particularly in areas like advanced driver-assistance systems (ADAS), autonomous driving, and in-cabin sensing, are also contributing significantly to market expansion. Furthermore, the medical industry's growing reliance on miniaturized and highly sensitive devices for diagnostics, drug delivery, and imaging further bolsters the market's trajectory.

The market is characterized by a dynamic landscape of technological innovation and strategic collaborations among key players like Bosch, STMicroelectronics, and Silex Microsystems. Emerging trends include the development of novel thin-film piezoelectric materials with improved performance characteristics and greater manufacturing efficiency. Miniaturization and integration of MEMS devices into complex systems are also critical trends, enabling more compact and powerful electronic solutions. While the market exhibits strong growth potential, certain restraints exist. High initial investment costs for foundry setup and advanced manufacturing processes can be a barrier for new entrants. Additionally, the complexity of wafer-level fabrication and the stringent quality control required for high-yield production present ongoing challenges. Nevertheless, the inherent advantages of thin-film piezo MEMS, such as their compact size, low power consumption, and high sensitivity, are expected to outweigh these challenges, driving sustained growth and innovation in the coming years.

This comprehensive report delves into the dynamic and rapidly evolving landscape of the Thin-Film Piezo MEMS Foundry market, projecting significant growth and innovation over the study period of 2019-2033. The market, valued in the millions of units, is characterized by increasing demand for high-performance, miniaturized, and energy-efficient sensing and actuation solutions across a multitude of applications.

The thin-film piezo MEMS foundry sector is witnessing a transformative period, driven by relentless advancements in material science, fabrication processes, and an insatiable appetite for sophisticated micro-scale devices. Over the historical period of 2019-2024, the market has steadily expanded, laying the groundwork for accelerated growth in the coming years. The base year of 2025 marks a significant inflection point, with the estimated market poised for a substantial upward trajectory throughout the forecast period of 2025-2033. A key trend is the increasing adoption of thin-film piezoelectric materials, such as Aluminum Nitride (AlN) and Lead Zirconate Titanate (PZT), due to their superior electromechanical coupling coefficients and compatibility with wafer-level manufacturing processes. This allows for the fabrication of smaller, more sensitive, and power-efficient MEMS devices compared to bulk piezoelectric counterparts.

Furthermore, the industry is observing a pronounced shift towards specialized foundries capable of offering advanced fabrication techniques, including precise thin-film deposition, etching, and packaging solutions tailored for piezoelectric MEMS. This specialization is critical for achieving the stringent performance requirements demanded by emerging applications. The integration of artificial intelligence and machine learning in the design and optimization of piezoelectric MEMS is also gaining momentum, promising to shorten development cycles and enhance device performance. The foundry model itself is evolving, with a greater emphasis on co-design, prototyping, and end-to-end manufacturing services, enabling fabless companies to bring innovative piezoelectric MEMS solutions to market more efficiently. The miniaturization trend continues unabated, with foundries investing in process nodes that enable the creation of exceptionally small yet highly functional piezoelectric MEMS devices. This miniaturization is directly fueling the growth in mobile, wearable, and implantable medical devices.

The market is also experiencing a diversification in piezoelectric materials, with research and development focusing on lead-free alternatives that offer comparable or superior performance while addressing environmental concerns. This pursuit of sustainable and high-performance materials will undoubtedly shape the foundry offerings in the coming years. Moreover, the growing complexity of piezoelectric MEMS devices, incorporating multiple layers and intricate designs, necessitates advanced lithography and deposition techniques, which are becoming core competencies for leading foundries. The demand for higher frequency operation and increased power handling capabilities in piezoelectric MEMS further pushes the boundaries of thin-film deposition and material quality. As the IoT ecosystem expands and autonomous systems become more prevalent, the need for highly reliable and compact piezoelectric MEMS sensors and actuators will continue to be a primary driver of foundry innovation and investment. The increasing focus on high-volume manufacturing and cost optimization will also compel foundries to refine their processes and achieve economies of scale.

The thin-film piezo MEMS foundry market is experiencing robust growth, propelled by a confluence of powerful driving forces that are reshaping industries and creating new technological frontiers. Foremost among these is the insatiable demand for enhanced sensing and actuation capabilities across a vast array of consumer electronics. As devices become more sophisticated, from smartphones and wearables to smart home appliances, the need for precise environmental sensing, haptic feedback, and micro-scale actuation becomes paramount. Thin-film piezoelectric MEMS offer a compelling solution due to their high sensitivity, low power consumption, and compact form factor, enabling the integration of advanced functionalities into increasingly smaller devices.

The burgeoning Internet of Things (IoT) ecosystem is another significant catalyst. The sheer volume of connected devices, each requiring sensing and actuation for data acquisition and interaction, creates an enormous market for MEMS components. Piezoelectric MEMS, with their ability to operate wirelessly and with minimal power, are perfectly suited for many IoT applications, including smart sensors, energy harvesting modules, and micro-actuators for smart grids and industrial automation. Furthermore, the automotive industry's transition towards autonomous driving and electric vehicles is a major growth engine. Piezoelectric MEMS are crucial for various automotive systems, including advanced driver-assistance systems (ADAS) for sensor fusion, active noise cancellation, and high-precision fuel injection systems, all demanding reliability and miniaturization. The medical sector's relentless pursuit of minimally invasive procedures, sophisticated diagnostics, and personalized healthcare solutions is also a strong driver. Piezoelectric MEMS are finding applications in microfluidic pumps, ultrasound imaging transducers, drug delivery systems, and implantable sensors, where biocompatibility, precision, and miniaturization are critical. The continuous miniaturization of electronic components across all sectors further amplifies the demand for advanced MEMS fabrication capabilities, pushing foundries to refine their thin-film deposition and patterning techniques.

Despite the promising growth trajectory, the thin-film piezo MEMS foundry market is not without its inherent challenges and restraints that could potentially temper its expansion. A primary hurdle lies in the complexity and cost associated with advanced thin-film piezoelectric material deposition and processing. Achieving high-quality, uniform thin films with precise piezoelectric properties, such as low leakage current and high electromechanical coupling, requires sophisticated equipment and rigorous process control, leading to higher manufacturing costs compared to more established MEMS technologies. This cost factor can be a significant barrier for widespread adoption in cost-sensitive applications.

Another challenge is the long development cycles and the high initial investment required for foundries to establish specialized fabrication lines for thin-film piezoelectric MEMS. The stringent performance requirements for reliability and long-term stability in critical applications, particularly in automotive and medical sectors, necessitate extensive testing and qualification procedures, further extending development timelines and R&D expenses. The limited availability of skilled personnel with expertise in piezoelectric materials science, MEMS fabrication, and device integration also poses a constraint on the industry's growth. Finding and retaining engineers and technicians with the specialized knowledge required to design, fabricate, and test these intricate devices can be difficult. Furthermore, the market is subject to intense competition, both from established MEMS players and emerging specialized foundries, leading to price pressures and the need for continuous innovation to maintain a competitive edge. Ensuring consistency and uniformity in piezoelectric properties across large wafer batches can also be a technical challenge, impacting yield and overall production efficiency. The development and adoption of lead-free piezoelectric materials, while environmentally beneficial, present ongoing research challenges to match the performance characteristics of traditional lead-based materials, potentially slowing down their integration into high-performance applications.

The thin-film piezo MEMS foundry market is poised for significant regional and segment-driven dominance, with a clear indication of where the most substantial growth and technological advancements are likely to originate and concentrate.

Dominant Regions/Countries:

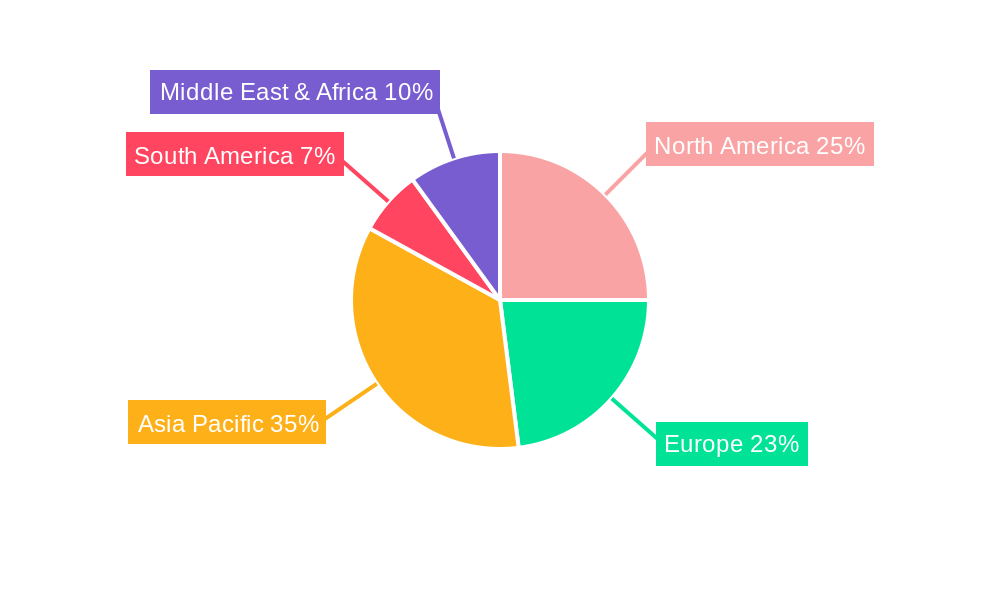

Asia-Pacific: This region is emerging as a powerhouse in the thin-film piezo MEMS foundry landscape, driven by a strong manufacturing base, significant government investment in advanced technologies, and a rapidly growing consumer electronics and automotive industries. Countries like China and South Korea are at the forefront, boasting a large number of semiconductor manufacturing facilities that are increasingly pivoting towards MEMS production. China, in particular, with its aggressive push for technological self-sufficiency, is investing heavily in domestic MEMS foundries, including those specializing in piezoelectric technologies. South Korea, with its established strengths in display and semiconductor manufacturing, is also a key player, leveraging its expertise in thin-film deposition and microfabrication. Japan, while having a more established history in precision manufacturing, continues to contribute significantly through its leading players in consumer electronics and automotive, driving demand for advanced MEMS. The sheer volume of end-user demand from these economies for smartphones, wearables, automotive components, and industrial automation equipment directly fuels the need for robust MEMS foundry services. The presence of a vast pool of engineers and a proactive policy environment supporting high-tech manufacturing further solidifies Asia-Pacific's leading position.

North America: This region, particularly the United States, remains a critical hub for innovation and high-end MEMS development. While not boasting the same sheer manufacturing volume as Asia-Pacific, North America excels in specialized foundries, research and development, and the development of cutting-edge applications in areas like medical devices, defense, and advanced industrial systems. The concentration of leading research institutions and venture capital funding for deep tech startups fosters an environment ripe for pioneering MEMS technologies, including advanced piezoelectric solutions.

Europe: Europe, with countries like Germany and France, represents a significant market for industrial automation, automotive, and medical devices. Its strong engineering heritage and focus on quality and reliability make it a key region for high-performance piezoelectric MEMS. The emphasis on industrial IoT (IIoT) and the growing demand for smart manufacturing solutions are driving the adoption of advanced MEMS in this region.

Dominant Segments:

The thin-film piezo MEMS foundry market will witness a pronounced dominance in several key segments, reflecting the most significant areas of application and technological advancement:

MEMS Sensor Foundry: This segment is expected to be the primary driver of the thin-film piezo MEMS foundry market. The increasing demand for miniaturized, high-sensitivity, and low-power sensors across all application areas is creating an unprecedented need for specialized foundry services.

MEMS Actuator Foundry: While currently a smaller segment compared to sensors, the MEMS actuator foundry segment is projected for rapid growth, driven by emerging applications that require precise micro-scale movement and force generation.

The synergy between these segments, particularly the increasing integration of both sensing and actuation capabilities within single MEMS devices, will further drive the demand for foundries that can offer comprehensive solutions. The overarching trend is the need for foundries that can provide high-volume, cost-effective manufacturing of thin-film piezoelectric MEMS with a high degree of customization and advanced performance characteristics.

The thin-film piezo MEMS foundry industry is experiencing robust growth fueled by several key catalysts. The ever-increasing demand for miniaturized, power-efficient, and high-performance sensors and actuators across consumer electronics, automotive, industrial, and medical sectors is a primary driver. The expansion of the Internet of Things (IoT) ecosystem necessitates a vast number of connected devices, each requiring sophisticated MEMS for sensing and interaction. Furthermore, advancements in material science, leading to improved piezoelectric thin-film properties and more cost-effective fabrication processes, are making these technologies more accessible. The growing trend towards autonomous systems, smart manufacturing, and minimally invasive medical procedures further amplifies the need for reliable and precise piezoelectric MEMS solutions.

This report offers a comprehensive and in-depth analysis of the thin-film piezo MEMS foundry market, providing critical insights for stakeholders. It meticulously examines market trends, drivers, challenges, and opportunities across the study period from 2019 to 2033, with a detailed focus on the forecast period of 2025-2033. The report leverages proprietary data and expert analysis to deliver accurate market estimations and projections in millions of units. It covers a wide spectrum of segments, including MEMS Sensor Foundry and MEMS Actuator Foundry, and analyzes their penetration across key applications such as Consumer Electronics, Industrial, Automotive, and Medical. Furthermore, the report identifies leading players and analyzes their strategic initiatives and technological advancements. This comprehensive coverage equips businesses with the essential intelligence needed to navigate this rapidly evolving market, identify growth opportunities, and formulate effective business strategies.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

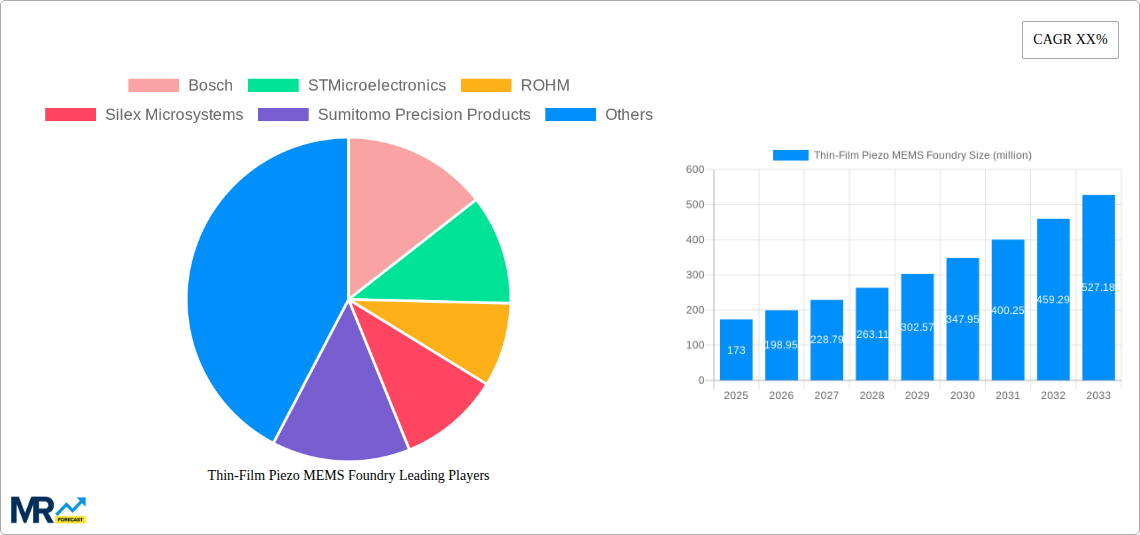

Key companies in the market include Bosch, STMicroelectronics, ROHM, Silex Microsystems, Sumitomo Precision Products.

The market segments include Type, Application.

The market size is estimated to be USD 173 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Thin-Film Piezo MEMS Foundry," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Thin-Film Piezo MEMS Foundry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.