1. What is the projected Compound Annual Growth Rate (CAGR) of the Si Photonics Transceivers?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Si Photonics Transceivers

Si Photonics TransceiversSi Photonics Transceivers by Type (100G Silicon Photonic Transceiver, 200G/400G Silicon Photonic Transceiver, Others, World Si Photonics Transceivers Production ), by Application (Datacenter Transceivers, Long Haul Transceivers, Optical Interconnects, Automotive LiDAR, Immunoassay Tests, Fiber-optic Gyroscope, Others, World Si Photonics Transceivers Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

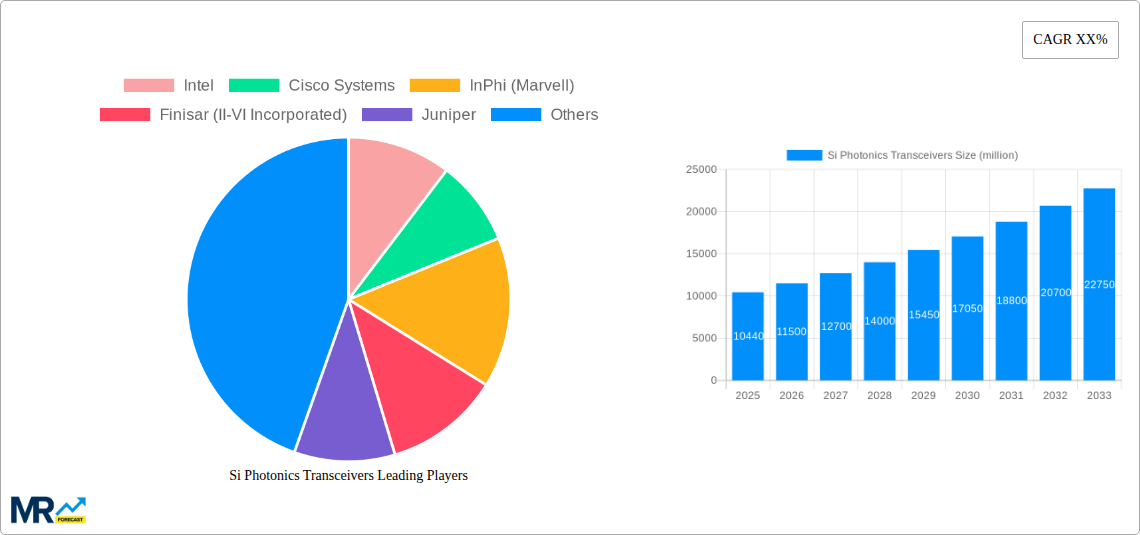

The global Silicon Photonics (Si-Ph) transceivers market is experiencing robust growth, projected to reach an estimated market size of $10,440 million by 2025. This expansion is driven by the insatiable demand for higher bandwidth and faster data transfer rates across various applications, particularly in data centers and telecommunications. The increasing adoption of 5G networks, cloud computing, and AI workloads necessitates more efficient and cost-effective optical interconnect solutions, positioning Si-Ph transceivers as a leading technology. The inherent advantages of silicon photonics, including its integration capabilities with CMOS manufacturing, miniaturization potential, and cost-effectiveness at scale, are key enablers of this market surge. As research and development efforts continue to enhance performance and reduce power consumption, Si-Ph transceivers are poised to displace traditional solutions in an increasing number of segments.

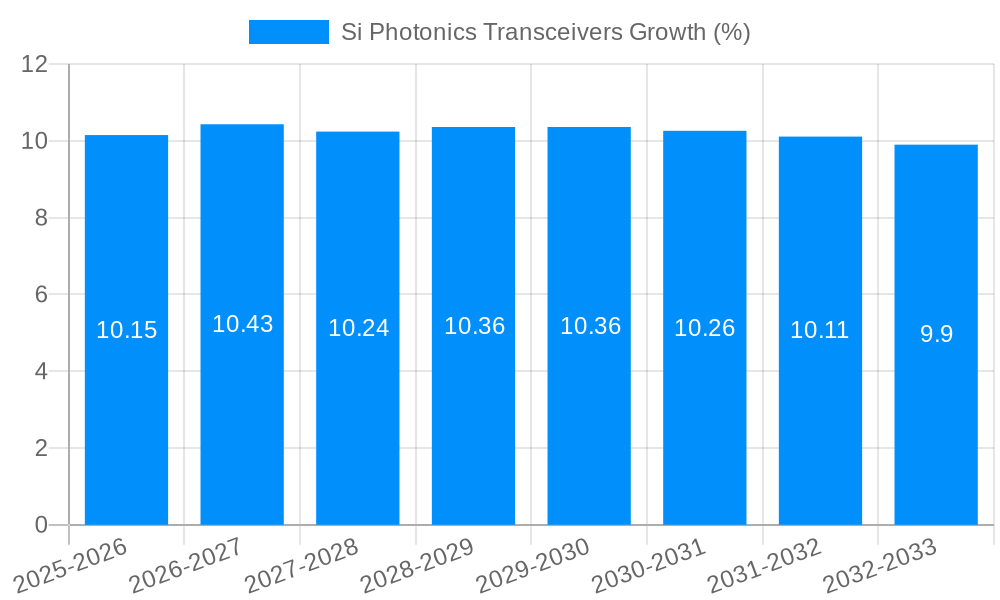

The market is segmented by type, with 200G/400G Silicon Photonic transceivers witnessing particularly rapid adoption due to the immediate need for increased capacity. While data centers represent the largest application segment, growth is also anticipated in areas like long-haul telecommunications, optical interconnects for high-performance computing, and emerging applications such as automotive LiDAR and advanced sensing technologies. Key players like Intel, Cisco, and InPhi (Marvell) are at the forefront of innovation, investing heavily in R&D and manufacturing capabilities. The market's trajectory is characterized by a sustained Compound Annual Growth Rate (CAGR), underscoring its significant potential. However, challenges related to manufacturing complexity and the need for specialized fabrication processes could present some restraints, though these are steadily being addressed by technological advancements and industry collaboration.

Here's a report description for Si Photonics Transceivers, incorporating the provided information and adhering to your formatting requests:

The global Si Photonics Transceivers market is experiencing a transformative surge, driven by an insatiable demand for higher bandwidth and greater energy efficiency across diverse applications. This report delves into the intricate dynamics shaping this burgeoning sector, projecting a market valued in the tens of millions of units by the base year of 2025. The historical period of 2019-2024 has witnessed the foundational growth, with World Si Photonics Transceivers Production steadily climbing as key players like Intel, Cisco Systems, and InPhi (Marvell) invested heavily in R&D and manufacturing capabilities. The study period from 2019 to 2033 encompasses a deep dive into the market's trajectory, highlighting the critical Estimated Year of 2025 as a pivotal point for widespread adoption of next-generation technologies. The forecast period of 2025-2033 anticipates exponential growth, largely fueled by the escalating requirements of hyperscale datacenters and the burgeoning adoption of AI and machine learning, which necessitate incredibly fast and efficient data transfer.

The market's evolution is intrinsically linked to the rapid advancement in Datacenter Transceivers, which currently represent a dominant application segment. As data centers grapple with exponential data growth, the inherent advantages of silicon photonics – including miniaturization, cost-effectiveness through wafer-scale manufacturing, and superior performance characteristics over traditional solutions – are making it the technology of choice. Furthermore, the increasing sophistication of 200G/400G Silicon Photonic Transceiver technologies is not only meeting but exceeding the performance demands of modern network infrastructure. While datacenter applications are currently leading, the report also scrutinizes emerging applications such as Automotive LiDAR and Immunoassay Tests, which are poised to unlock significant new market avenues. The intricate interplay between technological innovation, market demand, and strategic investments by major industry players, including Finisar (II-VI Incorporated), Juniper, Rockley Photonics, FUJITSU, Broadex Technologies, Hengtong Rockley Technologies, and Accelink Technologies, is meticulously analyzed. The report provides a granular understanding of the unit production trends, moving from the initial millions in the historical period to projections of substantial growth in the forecast period, underscoring the pivotal role silicon photonics plays in defining the future of optical communication.

The silicon photonics transceiver market is propelled by a confluence of powerful forces, primarily centered around the escalating demand for bandwidth and the relentless pursuit of energy efficiency in modern computing and communication infrastructure. The exponential growth of data generated by cloud computing, artificial intelligence, and the Internet of Things (IoT) necessitates transceiver technologies capable of handling unprecedented data rates. Silicon photonics, with its inherent scalability and potential for high integration, offers a compelling solution to meet these bandwidth demands. Furthermore, the cost-effectiveness of manufacturing silicon photonics devices through established semiconductor fabrication processes, like those employed by industry giants such as Intel and InPhi (Marvell), is a significant driver. This wafer-scale manufacturing approach allows for mass production, driving down per-unit costs and making silicon photonic transceivers more accessible for widespread deployment, particularly in high-volume applications like datacenters. The increasing density of servers and the need for high-speed interconnects within these facilities are creating a fertile ground for the adoption of these advanced transceivers.

Beyond the datacenter, the intrinsic advantages of silicon photonics, such as its smaller form factor and reduced power consumption compared to traditional optical components, are opening doors in new and emerging markets. For instance, the development of specialized silicon photonic transceivers for applications like Automotive LiDAR promises to enhance the sensing capabilities of autonomous vehicles. Similarly, the precision and miniaturization offered by silicon photonics are finding utility in advanced medical diagnostics and scientific instrumentation, such as Immunoassay Tests. The continuous innovation by companies like Cisco Systems, Finisar (II-VI Incorporated), and Juniper in refining their silicon photonics technologies, alongside the emergence of specialized players like Rockley Photonics, further fuels this growth by expanding the product portfolio and addressing a wider range of market needs. The drive towards greener IT infrastructure, with a focus on reducing energy consumption, also strongly favors silicon photonics due to its inherent power efficiency advantages.

Despite the promising outlook, the silicon photonics transceiver market faces several significant challenges and restraints that could temper its growth trajectory. One of the primary hurdles remains the Complexity of Integration and Manufacturing Yield. While silicon photonics leverages established semiconductor fabrication processes, the integration of optical components – such as lasers, modulators, and detectors – onto a silicon chip is still a complex endeavor. Achieving high manufacturing yields at the wafer scale, critical for cost-effectiveness, can be challenging, leading to higher initial production costs compared to more mature optical technologies. The specialized nature of the manufacturing process also requires significant capital investment in foundries and advanced equipment, which can be a barrier for new entrants.

Another restraint lies in the Interoperability and Standardization of silicon photonic transceivers, particularly as new product generations emerge. Ensuring seamless integration with existing network infrastructure and establishing industry-wide standards for performance and interfaces is crucial for widespread adoption. While efforts are underway, the pace of standardization can sometimes lag behind the rapid pace of technological innovation. Furthermore, the Perceived High Cost of Entry for certain niche applications, despite the long-term cost-saving potential, can still be a deterrent. For industries with tighter budget constraints or less immediate demand for extreme bandwidth, the upfront investment in silicon photonic solutions might be less appealing than continuing with established, albeit less performant, technologies. The market also needs to contend with Talent Acquisition and Development in the specialized field of silicon photonics, requiring a skilled workforce proficient in both photonics and semiconductor engineering. Finally, Supply Chain Volatility and the geopolitical landscape can impact the availability of raw materials and the stability of global manufacturing and distribution, posing a risk to consistent production and delivery schedules.

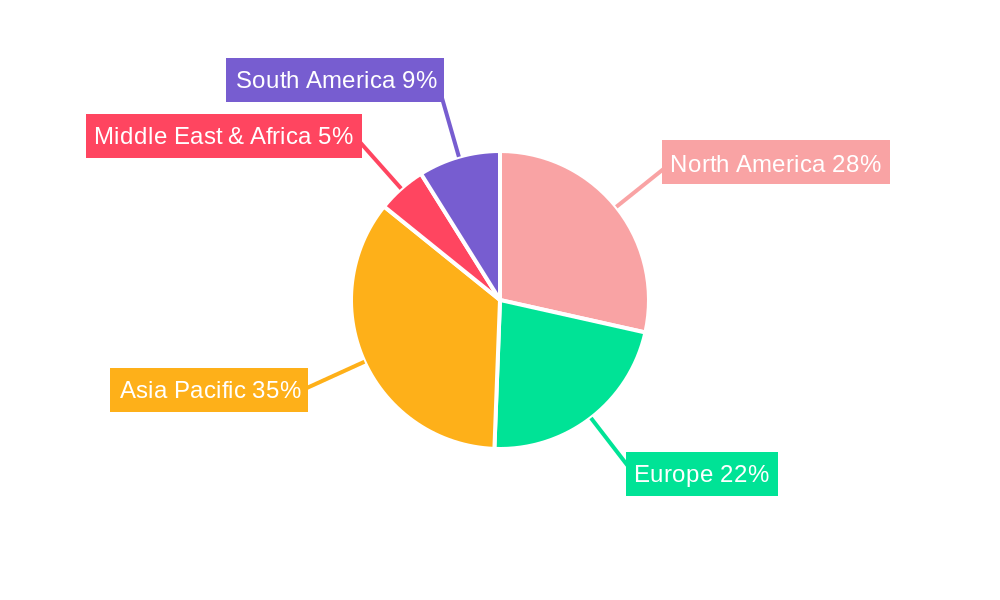

The silicon photonics transceiver market is characterized by a dynamic interplay of dominant regions and segments, with a clear concentration of activity and projected dominance.

Dominant Segment:

Dominant Region/Country:

While other regions like Asia-Pacific are rapidly emerging, particularly with the presence of companies like FUJITSU, Broadex Technologies, Hengtong Rockley Technologies, and Accelink Technologies, and are expected to play a crucial role in manufacturing and future growth, North America's established ecosystem, strong R&D, and substantial datacenter footprint currently position it as the dominant region driving the silicon photonics transceiver market. The focus on Datacenter Transceivers within this region, specifically the higher-speed 200G/400G Silicon Photonic Transceiver variants, will continue to shape market trends and production volumes in the foreseeable future.

The silicon photonics transceiver industry is experiencing a significant growth spurt fueled by several key catalysts. The exponential increase in data traffic generated by cloud computing, artificial intelligence, and the Internet of Things is creating an unyielding demand for higher bandwidth and more efficient data transfer solutions. Silicon photonics, with its ability to integrate multiple optical functions onto a single chip and leverage established semiconductor manufacturing processes, offers a cost-effective and scalable path to meet these escalating bandwidth requirements. Furthermore, the ongoing advancements in laser technology, modulator efficiency, and detector sensitivity within silicon photonics are continually pushing performance boundaries, enabling higher data rates and longer reach capabilities. The drive towards energy efficiency in datacenters, driven by both economic and environmental concerns, also favors silicon photonics due to its inherent lower power consumption compared to traditional optical transceiver technologies.

This comprehensive report provides an in-depth analysis of the global Si Photonics Transceivers market, covering the historical period from 2019 to 2024 and projecting trends up to 2033, with a key focus on the estimated year of 2025. It meticulously examines market drivers, challenges, and opportunities, offering a granular view of production volumes in the tens of millions of units. The report delves into specific segments such as 100G, 200G/400G Silicon Photonic Transceivers, and key applications including Datacenter Transceivers, Long Haul Transceivers, Optical Interconnects, Automotive LiDAR, and others. Leading companies like Intel, Cisco Systems, and InPhi (Marvell) are profiled, alongside significant industry developments. This report is an essential resource for stakeholders seeking to understand the evolving landscape, identify growth catalysts, and make informed strategic decisions in this rapidly advancing sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Intel, Cisco Systems, InPhi (Marvell), Finisar (II-VI Incorporated), Juniper, Rockley Photonics, FUJITSU, Broadex Technologies, Hengtong Rockley Technologies, Accelink Technologies.

The market segments include Type, Application.

The market size is estimated to be USD 10440 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Si Photonics Transceivers," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Si Photonics Transceivers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.