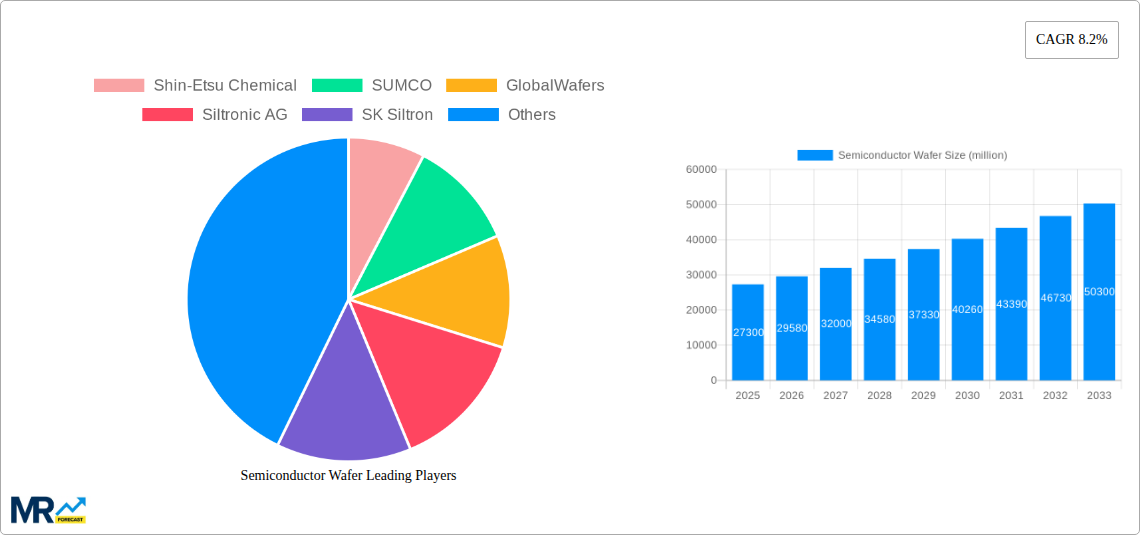

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Wafer?

The projected CAGR is approximately 8.2%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Semiconductor Wafer

Semiconductor WaferSemiconductor Wafer by Type (Semiconductor Silicon Wafers, Silicon Carbide (SiC) Wafers, GaAs Wafers), by Application (Memory, Logic/MPU, Analog, Power Module & Discretes, Sensors, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global semiconductor wafer market is poised for substantial expansion, projected to reach approximately $27,300 million in 2025 and grow at a robust Compound Annual Growth Rate (CAGR) of 8.2% through 2033. This dynamic growth is primarily fueled by the insatiable demand for advanced electronics across various sectors. Key drivers include the proliferation of 5G technology, the burgeoning Internet of Things (IoT) ecosystem, the exponential rise of artificial intelligence (AI) and machine learning (ML) applications, and the continuous evolution of automotive electronics, particularly in the electric vehicle (EV) segment. The increasing complexity and miniaturization of semiconductors necessitate higher quality and advanced wafer materials, further propelling market value. Furthermore, government initiatives and investments aimed at bolstering domestic semiconductor manufacturing capabilities worldwide are creating significant tailwinds for market expansion. Emerging trends such as the adoption of silicon carbide (SiC) and gallium arsenide (GaAs) wafers for high-power and high-frequency applications are diversifying the market landscape and opening new avenues for growth.

Despite the optimistic outlook, the market faces certain restraints. Fluctuations in raw material prices, particularly for high-purity silicon, can impact production costs. Geopolitical tensions and trade disputes can disrupt supply chains and create market uncertainty. Moreover, the high capital expenditure required for advanced wafer fabrication facilities presents a barrier to entry for new players. Nevertheless, the overwhelming demand driven by digital transformation initiatives across industries, coupled with ongoing technological advancements in wafer manufacturing processes, is expected to outweigh these challenges. The market is segmented by wafer type, with semiconductor silicon wafers dominating the current landscape, but SiC and GaAs wafers are experiencing rapid growth. Applications such as memory, logic/MPU, and power modules are key revenue generators, while the increasing use of wafers in sensors and other specialized areas are contributing to market diversification. Asia Pacific, led by China and other key manufacturing hubs, is expected to remain the dominant region, driven by robust domestic demand and extensive manufacturing infrastructure.

This report offers an in-depth analysis of the global semiconductor wafer market, providing critical insights into its historical performance, current standing, and projected trajectory through 2033. The study encompasses a rigorous examination of key market drivers, emerging trends, significant challenges, and regional dynamics, with a specific focus on the period from 2019 to 2033. The base year for estimation is 2025, with projections extending through 2033.

The global semiconductor wafer market is experiencing a period of unprecedented transformation, driven by a confluence of technological advancements, escalating demand across diverse end-use industries, and evolving geopolitical landscapes. In the Historical Period (2019-2024), the market witnessed steady growth, albeit with some volatility influenced by supply chain disruptions and the initial impact of global events. The Base Year (2025) serves as a pivotal point, reflecting a market that has largely stabilized and is poised for accelerated expansion. Projections for the Forecast Period (2025-2033) indicate a robust CAGR, potentially reaching several hundred million USD in market value, fueled by the insatiable appetite for more powerful and efficient electronic devices. Key market insights reveal a pronounced shift towards advanced wafer materials and larger wafer diameters, such as the increasing adoption of 300mm wafers, which offer higher yields and reduced manufacturing costs per chip. The burgeoning demand for Silicon Carbide (SiC) wafers and Gallium Arsenide (GaAs) wafers is a testament to the growing importance of these materials in high-performance applications, particularly in the automotive and telecommunications sectors. Furthermore, the increasing sophistication of semiconductor devices, from advanced processors for artificial intelligence to energy-efficient power modules, is constantly pushing the boundaries of wafer technology, necessitating innovations in material purity, crystal growth, and wafer processing techniques. The market is also being shaped by significant investments in research and development, aimed at overcoming inherent material limitations and exploring novel wafer architectures to support next-generation semiconductor technologies. Strategic collaborations and mergers & acquisitions among key players are becoming increasingly prevalent as companies seek to secure supply chains, expand their product portfolios, and gain a competitive edge in this dynamic and capital-intensive industry. The emphasis on miniaturization, increased processing power, and enhanced energy efficiency in electronic devices continues to drive the demand for smaller feature sizes on wafers, pushing the limits of photolithography and etching technologies. Consequently, the semiconductor wafer market is characterized by continuous innovation and a relentless pursuit of technological excellence.

The semiconductor wafer market's upward trajectory is being propelled by a powerful synergy of interconnected forces. Foremost among these is the relentless advancement of digitalization across virtually every facet of modern life. The proliferation of 5G technology and the subsequent explosion of data traffic are creating an insatiable demand for high-performance processors and communication chips, all reliant on sophisticated semiconductor wafers. This is further amplified by the rapid expansion of the Internet of Things (IoT), where billions of connected devices, from smart home appliances to industrial sensors, require increasingly powerful and energy-efficient semiconductor components. Artificial intelligence (AI) and machine learning (ML) are also major catalysts, demanding specialized and high-density computing power that can only be delivered by cutting-edge wafer technology. The automotive industry's transition towards electric vehicles (EVs) and autonomous driving systems is another significant driver, as these vehicles incorporate a vast number of power semiconductors, sensors, and advanced computing units, all manufactured on specialized wafers. Furthermore, the ongoing digital transformation in sectors like healthcare, manufacturing, and finance continues to fuel the demand for advanced semiconductors, thereby underpinning the growth of the wafer market. Investments in advanced computing infrastructure, including data centers and high-performance computing (HPC) clusters, also contribute significantly to this demand. The push towards greater energy efficiency in electronic devices, driven by both environmental concerns and the need to reduce operational costs, is also a key propellant, encouraging the adoption of newer wafer materials like SiC and GaN.

Despite its robust growth prospects, the semiconductor wafer market is not without its significant challenges and restraints. Foremost among these is the inherent complexity and capital intensity of wafer manufacturing. Establishing and maintaining state-of-the-art fabrication facilities requires astronomical investments, often running into billions of dollars, creating high barriers to entry for new players. The extreme precision required in wafer production, with tolerances measured in nanometers, necessitates highly specialized equipment and a meticulously controlled manufacturing environment, making any deviation costly and time-consuming. Supply chain volatility, as demonstrated during recent global events, poses another substantial risk. Disruptions in the availability of critical raw materials, such as high-purity silicon or specialty gases, can lead to production delays and price fluctuations, impacting the entire semiconductor ecosystem. Furthermore, the semiconductor industry is highly susceptible to cyclical demand. Fluctuations in consumer spending, economic downturns, or shifts in technology adoption can lead to periods of oversupply or undersupply, creating market instability. Geopolitical tensions and trade disputes can also create significant headwinds, impacting global trade flows and potentially leading to market fragmentation. The escalating cost of research and development, coupled with the shortening lifecycles of semiconductor technologies, adds to the pressure on manufacturers to continuously innovate while managing costs. Stringent environmental regulations and the increasing focus on sustainability in manufacturing processes also present challenges, requiring companies to invest in greener technologies and responsible waste management. The ongoing global semiconductor shortage, though easing in some segments, highlights the delicate balance between supply and demand.

The global semiconductor wafer market is characterized by a dynamic interplay of regional dominance and segment-specific growth. However, the Asia-Pacific (APAC) region, particularly China, Taiwan, South Korea, and Japan, is poised to exert significant influence and dominate market share throughout the forecast period. This dominance stems from a confluence of factors, including robust government support for the semiconductor industry, substantial investments in advanced manufacturing capabilities, and the presence of leading integrated device manufacturers (IDMs) and foundries. Taiwan, for instance, remains the epicenter of advanced semiconductor manufacturing, with its foundries producing a significant portion of the world's most sophisticated chips. South Korea's strength lies in its leadership in memory chip production, a critical segment of the wafer market. China's aggressive expansion and strategic focus on achieving semiconductor self-sufficiency are rapidly increasing its market share, with substantial investments in wafer fabrication facilities and material research.

Within the Type segment, Semiconductor Silicon Wafers will continue to be the dominant category, accounting for the largest market share. This is due to their foundational role in the vast majority of electronic devices manufactured globally. However, the growth of Silicon Carbide (SiC) Wafers is expected to be the most significant in percentage terms. This surge is driven by their superior performance characteristics, including higher breakdown voltage, better thermal conductivity, and increased efficiency, making them indispensable for applications in electric vehicles, renewable energy systems (such as solar inverters and wind turbines), and high-power industrial equipment. The demand for SiC wafers is projected to witness a CAGR exceeding 25% during the forecast period, reaching a market value of tens of millions of USD.

Considering the Application segment, Logic/MPU (Microprocessing Unit) and Memory applications will continue to represent substantial market segments due to the ever-increasing demand for powerful processors and vast data storage capabilities in consumer electronics, servers, and computing devices. However, the Power Module & Discretes segment is expected to experience exceptionally strong growth, closely mirroring the rise of SiC wafer adoption. This segment encompasses components crucial for power management in electric vehicles, energy-efficient power supplies, and industrial automation. The increasing electrification of transportation and the global push for energy efficiency are directly translating into a massive demand for power semiconductor devices manufactured on advanced wafers. The market value for the Power Module & Discretes segment is anticipated to grow at a robust pace, reaching hundreds of millions of USD by 2033, with SiC and Gallium Nitride (GaN) wafers playing an increasingly crucial role. Sensors, another vital application, will also see steady growth driven by the proliferation of IoT devices and advanced automotive safety systems.

Several key growth catalysts are propelling the semiconductor wafer industry forward. The accelerating adoption of electric vehicles (EVs) is a primary driver, as EVs require significantly more power semiconductors than traditional internal combustion engine vehicles, demanding specialized SiC and GaN wafers for efficient power management. The ongoing rollout of 5G infrastructure globally is fueling demand for high-frequency communication chips, driving the need for GaAs and other advanced compound semiconductor wafers. The insatiable growth of data centers, powered by cloud computing and AI, necessitates advanced processors and memory chips, leading to increased demand for high-volume silicon wafers with tighter specifications. Finally, government initiatives and investments aimed at boosting domestic semiconductor manufacturing capabilities in various regions are providing substantial impetus for market expansion and innovation.

This comprehensive report delves into the intricate landscape of the semiconductor wafer market, offering a detailed examination of its historical evolution, current market dynamics, and future projections. The study meticulously analyzes the key segments, including Semiconductor Silicon Wafers, Silicon Carbide (SiC) Wafers, and GaAs Wafers, and their respective applications in Memory, Logic/MPU, Analog, Power Module & Discretes, and Sensors. The report highlights the significant growth catalysts such as the burgeoning electric vehicle market and the expansion of 5G networks, as well as the challenges posed by supply chain volatility and the high capital intensity of manufacturing. With an extensive review of industry developments and an in-depth profiling of leading players, this report provides a strategic roadmap for stakeholders navigating this critical and rapidly evolving sector. The market is projected to experience substantial growth, driven by technological advancements and increasing global demand for advanced electronic components.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.2% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.2%.

Key companies in the market include Shin-Etsu Chemical, SUMCO, GlobalWafers, Siltronic AG, SK Siltron, FST Corporation, Wafer Works Corporation, Soitec, National Silicon Industry Group (NSIG), Zhonghuan Advanced Semiconductor Materials, Hangzhou Lion Microelectronics, Hangzhou Semiconductor Wafer +AK12+G1+G12:AD12, GRINM Semiconductor Materials, MCL Electronic Materials, Shanghai Advanced Silicon Technology (AST), Beijing ESWIN Technology Group, Zhejiang MTCN Technology, Hebei Puxing Electronic Technology, Nanjing Guosheng Electronics, Wolfspeed, SK Siltron, ROHM Group (SiCrystal), Coherent, Resonac, STMicroelectronics, TankeBlue, SICC, Hebei Synlight Crystal, CETC, San'an Optoelectronics, Freiberger Compound Materials, AXT, Inc., Sumitomo Electric Industries, Ltd., Vital Materials, China Crystal Technologies Co., Ltd., H3C SecPath Series, DOWA Electronics Materials Co., Ltd..

The market segments include Type, Application.

The market size is estimated to be USD 27300 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Semiconductor Wafer," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Wafer, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.