1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Packaging Materials?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Semiconductor Packaging Materials

Semiconductor Packaging MaterialsSemiconductor Packaging Materials by Type (/> Packaging Substrate, Lead Frame, Bonding Wire, Encapsulating Resin, Ceramic Packaging Material, Chip Bonding Material, Others), by Application (/> Consume Electrons, Automobiles, Communications, Medical, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

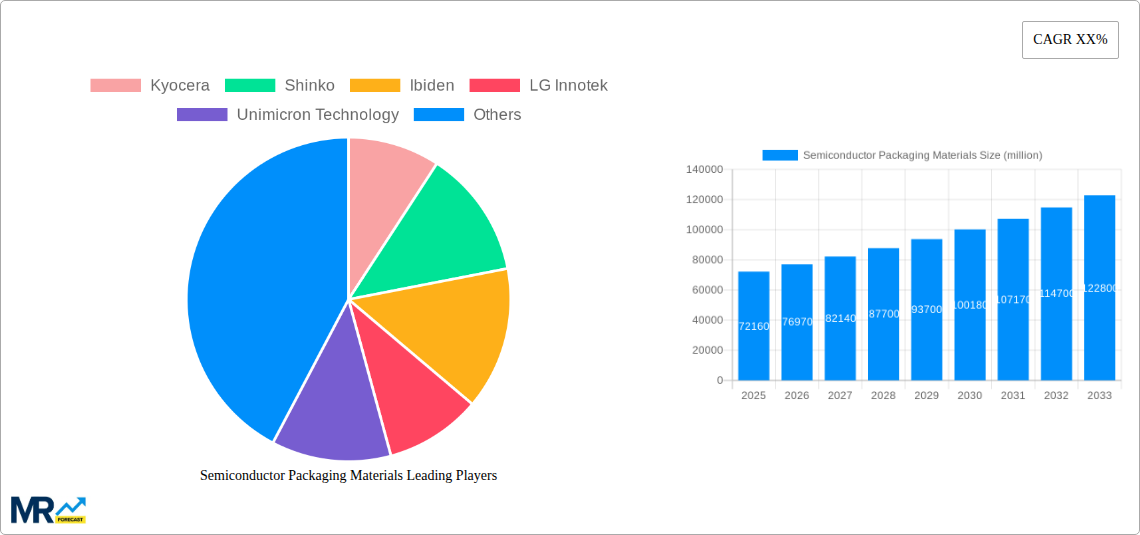

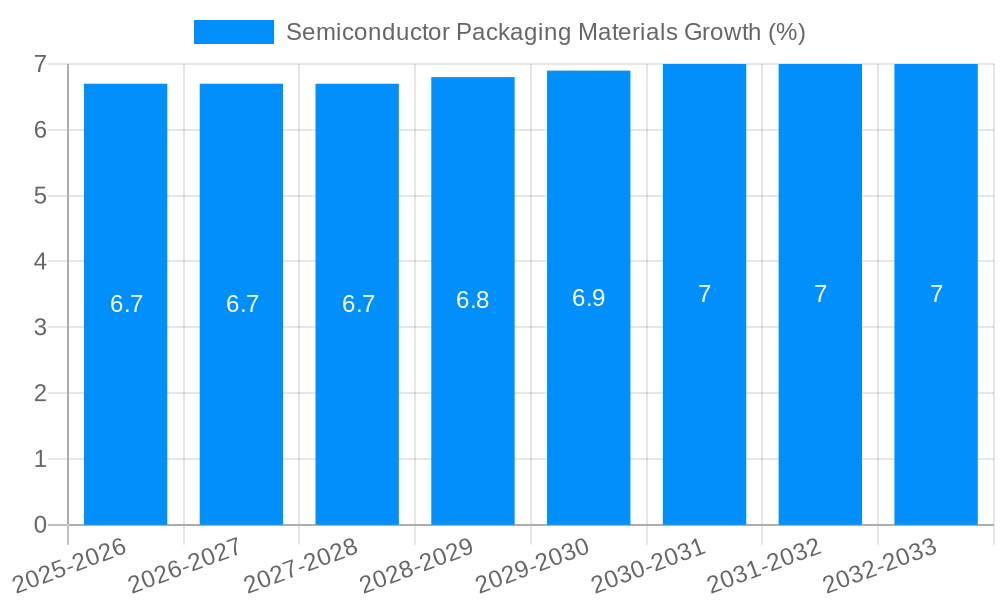

The global Semiconductor Packaging Materials market is poised for significant expansion, with a robust market size of approximately USD 72,160 million in 2025. This growth is propelled by an estimated Compound Annual Growth Rate (CAGR) of around 6.5% to 7.5% throughout the forecast period of 2025-2033. Key market drivers include the escalating demand for advanced electronic devices across consumer electronics, automotive, and telecommunications sectors. The increasing sophistication of integrated circuits (ICs) necessitates higher-performance packaging solutions, including advanced substrates, lead frames, and encapsulating resins, to ensure reliability, miniaturization, and enhanced thermal management. Furthermore, the burgeoning adoption of 5G technology, the proliferation of AI and machine learning applications, and the continuous innovation in the Internet of Things (IoT) ecosystem are creating a sustained demand for specialized semiconductor packaging materials. The medical sector's growing reliance on sophisticated medical devices also contributes to this upward trajectory.

Several critical trends are shaping the semiconductor packaging materials landscape. The shift towards miniaturization and higher component density is driving the development of advanced substrates like Fan-Out Wafer Level Packaging (FOWLP) and 2.5D/3D IC packaging. The increasing importance of thermal management is fostering innovation in encapsulating resins and ceramic packaging materials designed for superior heat dissipation. Supply chain resilience and regionalization efforts, influenced by geopolitical factors and a desire for localized production, are also becoming prominent. Restraints in the market, though, may include volatile raw material prices for certain specialized components and the significant capital investment required for advanced manufacturing capabilities. Despite these challenges, the market is expected to witness sustained growth, supported by ongoing research and development efforts and a strong pipeline of emerging applications that rely heavily on high-performance semiconductor packaging.

The global semiconductor packaging materials market is undergoing a profound transformation, driven by the relentless miniaturization of electronic devices and the escalating demand for enhanced performance, reliability, and thermal management. Over the Study Period: 2019-2033, the market has witnessed consistent growth, with the Base Year: 2025 serving as a critical pivot point for understanding the trajectory of this dynamic industry. The Estimated Year: 2025 further solidifies the current landscape, showcasing a robust demand across various applications. The Forecast Period: 2025-2033 is poised for significant expansion, fueled by breakthroughs in material science and the burgeoning adoption of advanced packaging technologies. During the Historical Period: 2019-2024, foundational growth was established, laying the groundwork for the accelerated progress anticipated in the coming years.

The evolution of semiconductor packaging materials is intricately linked to the broader semiconductor industry's push towards higher integration, greater power efficiency, and reduced form factors. Key market insights reveal a substantial shift from traditional materials to high-performance alternatives that can withstand increasingly demanding operating conditions. For instance, the demand for advanced packaging substrates, such as High-Density Interconnect (HDI) substrates and Fan-Out Wafer-Level Packaging (FOWLP) substrates, has surged. These substrates are crucial for enabling the dense routing of signals and accommodating multiple die in a single package, thereby reducing overall board space and improving electrical performance. The market for encapsulating resins is also seeing significant innovation, with a focus on materials offering superior thermal conductivity, lower dielectric loss, and enhanced protection against environmental factors. This is particularly critical for applications in high-power devices and automotive electronics, where robust thermal management is paramount. Bonding wires are witnessing a transition towards finer diameters and higher conductivity materials, such as copper and palladium, to meet the requirements of high-speed interconnects and reduced signal latency. Furthermore, the increasing complexity of semiconductor devices is driving the demand for sophisticated chip bonding materials, including conductive adhesives and solder pastes that offer excellent adhesion, mechanical strength, and electrical performance. The "Others" category, encompassing a range of specialized materials like thermal interface materials (TIMs) and underfill encapsulants, is also expected to grow as package designs become more intricate and performance demands intensify. The overarching trend is towards materials that enable smaller, faster, and more reliable semiconductor devices, directly impacting the performance and longevity of the end products in consumer electronics, automotive, communications, and medical sectors.

The semiconductor packaging materials market is experiencing robust growth propelled by a confluence of powerful driving forces. Foremost among these is the insatiable demand for advanced electronic devices across various sectors. The relentless evolution of Consume Electrons devices, from smartphones and wearables to high-performance computing and artificial intelligence (AI) hardware, necessitates smaller, more powerful, and energy-efficient chips. This directly translates into a need for sophisticated packaging solutions that can accommodate increasing transistor densities and advanced functionalities. The automotive industry's rapid electrification and the increasing integration of autonomous driving technologies are further fueling demand. Vehicles are becoming mobile data centers, requiring advanced semiconductor components for sensors, processing units, and communication systems, all of which rely heavily on specialized packaging materials for reliability and performance in harsh environments. The Communications sector, particularly the rollout of 5G and the development of future wireless technologies, demands high-frequency and high-speed interconnect solutions, driving innovation in packaging substrates and bonding materials. Furthermore, the growing adoption of advanced semiconductor technologies in the Medical field, for applications ranging from implantable devices to advanced diagnostic equipment, underscores the critical role of biocompatible and highly reliable packaging materials. The continuous push for miniaturization, improved thermal management, and enhanced electrical performance across all these segments creates a virtuous cycle, stimulating ongoing research and development in semiconductor packaging materials.

Despite the optimistic growth trajectory, the semiconductor packaging materials market faces several significant challenges and restraints that could temper its expansion. One of the primary hurdles is the escalating cost of advanced materials and manufacturing processes. The development and implementation of cutting-edge materials, such as specialized polymers, ceramics, and metal alloys, often come with a premium price tag. This can be a significant barrier, especially for cost-sensitive applications or smaller manufacturers. The complexity of the supply chain for these specialized materials also presents challenges. Sourcing raw materials from diverse global suppliers can lead to potential disruptions, geopolitical risks, and fluctuations in pricing. Maintaining consistent quality and ensuring the availability of critical components across a geographically dispersed network requires robust supply chain management. Moreover, the rapid pace of technological advancement in semiconductor devices often outpaces the development and qualification of new packaging materials. Introducing and validating novel materials to meet stringent industry standards and reliability requirements can be a time-consuming and expensive process, creating a lag between innovation in chip design and the availability of suitable packaging solutions. Environmental regulations and sustainability concerns are also emerging as significant restraints. The industry is under increasing pressure to develop eco-friendly materials and manufacturing processes, reducing waste and minimizing the use of hazardous substances. Adapting to these evolving regulations requires substantial investment in research and development and a potential overhaul of existing production methodologies. Finally, the skilled workforce gap in specialized areas of materials science and semiconductor packaging can hinder the adoption of new technologies and the scaling of production, posing a constraint on overall market growth.

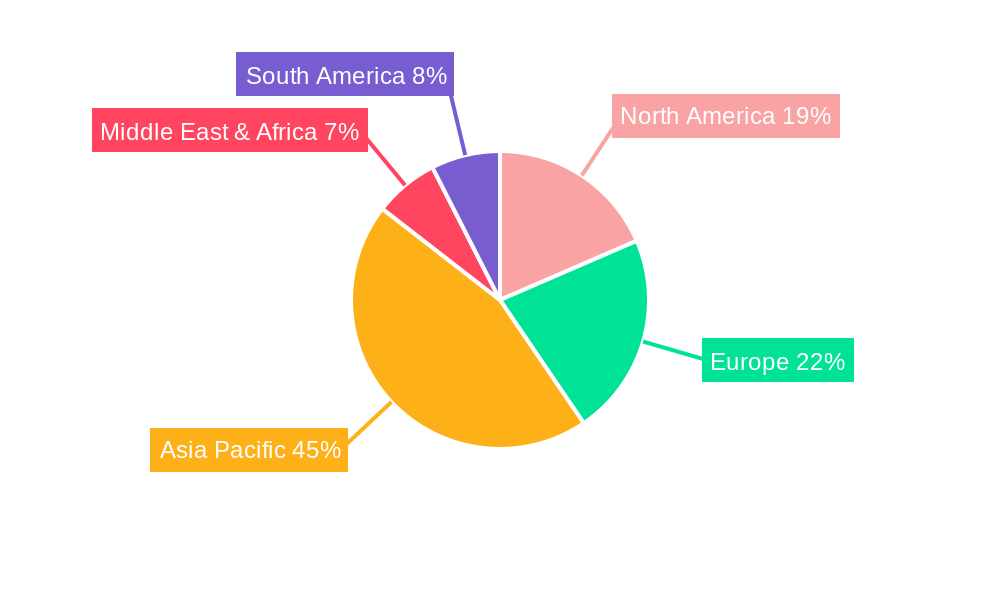

The global semiconductor packaging materials market is characterized by regional dominance and segment leadership, with specific geographies and product categories playing pivotal roles in market expansion.

Dominant Regions/Countries:

Asia-Pacific: This region stands as the undisputed leader in both the production and consumption of semiconductor packaging materials. Countries like Taiwan, South Korea, and China are home to a significant concentration of leading semiconductor fabrication plants (fabs), outsourced semiconductor assembly and test (OSAT) facilities, and material manufacturers. Taiwan, in particular, with giants like Unimicron Technology and Kinsus Interconnect Technology, is a powerhouse in packaging substrate manufacturing. South Korea, boasting companies like LG Innotek and Semco, excels in advanced packaging solutions and material innovation. China's rapid growth in its domestic semiconductor industry, supported by companies like Shennan Circuits and Kangqiang Electronics, is making it an increasingly influential player, particularly in packaging substrates and encapsulating resins. The sheer volume of semiconductor manufacturing activities in this region, driven by the massive consumer electronics market, makes it the primary hub for packaging material demand and supply.

North America: While not the largest manufacturing hub for packaging materials themselves, North America, particularly the United States, is a significant consumer and innovator in advanced semiconductor packaging technologies. Its dominance lies in the R&D and application of high-end packaging materials for sectors like artificial intelligence, high-performance computing, and defense. Companies like Henkel (with significant operations) are key material suppliers in this region, focusing on advanced bonding materials and encapsulants. The presence of major chip designers and system integrators drives the demand for cutting-edge packaging solutions.

Europe: Europe is a growing player, particularly in specialized applications like automotive and industrial electronics. Germany, with its strong automotive industry, is a key market for semiconductor packaging materials that require high reliability and thermal performance. Companies like Heraeus are prominent in this region, specializing in materials for lead frames and precious metal-based components. The increasing focus on domestic semiconductor manufacturing capabilities in Europe is also expected to drive future growth in this sector.

Dominant Segments:

Packaging Substrate: This segment consistently holds the largest market share and is projected to continue its dominance throughout the forecast period. Packaging substrates are the foundational component of most advanced semiconductor packages, providing electrical interconnection, mechanical support, and thermal management. The increasing complexity of integrated circuits (ICs), the rise of System-in-Package (SiP) and Multi-Chip Module (MCM) architectures, and the growing demand for high-density interconnects (HDIs) are the primary drivers for this segment's growth. Companies such as Kyocera, Shinko, Ibiden, Unimicron Technology, and ZhenDing Tech are key players, investing heavily in R&D to develop thinner, more flexible, and higher-performance substrates that can accommodate next-generation chip designs. The increasing adoption of advanced materials like organic substrates with refined copper and advanced dielectric layers is a significant trend.

Encapsulating Resin: This segment is the second-largest and is experiencing robust growth. Encapsulating resins protect semiconductor devices from environmental damage, mechanical stress, and contamination. The demand for high-performance encapsulants with superior thermal conductivity, excellent adhesion, and improved dielectric properties is driven by the need for enhanced reliability in harsh operating conditions, such as in automotive and industrial applications. The development of halogen-free and low-stress encapsulating resins is also a key trend, aligning with environmental regulations and the need for gentler processing of sensitive semiconductor devices. LG Chem, Henkel, and Sumitomo are notable companies in this segment, continually innovating to meet evolving performance requirements.

Chip Bonding Material: This segment is witnessing significant growth due to the increasing adoption of advanced packaging techniques like flip-chip and die-attach processes. Chip bonding materials, including conductive adhesives, solder pastes, and die attach films, are critical for establishing reliable electrical and mechanical connections between the semiconductor die and the packaging substrate. The need for higher interconnect density, finer pitch bonding, and improved thermal performance in advanced packages is driving innovation in this segment. Companies like Heraeus, Henkel, and Element Solutions are at the forefront of developing advanced chip bonding solutions that offer superior performance and reliability.

The interplay between these dominant regions and segments creates a dynamic market landscape. The concentration of manufacturing in Asia-Pacific, coupled with the technological advancements in packaging substrates and encapsulating resins, positions the region for continued leadership. Simultaneously, innovation in chip bonding materials and specialized applications in North America and Europe will contribute to the overall growth and diversification of the global semiconductor packaging materials market.

Several key growth catalysts are propelling the semiconductor packaging materials industry forward. The relentless pursuit of miniaturization and performance enhancement in consumer electronics, exemplified by the demand for thinner smartphones and more powerful computing devices, is a primary driver. The explosive growth of the automotive sector, driven by electrification and autonomous driving, necessitates highly reliable and thermally efficient semiconductor packaging. The expansion of 5G infrastructure and the increasing adoption of IoT devices create a surge in demand for high-speed and compact packaging solutions. Furthermore, advancements in AI and machine learning require sophisticated packaging that can handle high-power density and complex interconnects. Finally, government initiatives and increased investments in domestic semiconductor manufacturing in various regions are fostering innovation and creating new market opportunities for packaging material suppliers.

The semiconductor packaging materials market is populated by a diverse range of global players, each contributing unique expertise and product portfolios. The leading companies shaping this industry include:

The semiconductor packaging materials sector has witnessed numerous impactful developments over the Study Period: 2019-2033:

This comprehensive report offers an in-depth analysis of the global semiconductor packaging materials market, meticulously detailing trends, growth drivers, and challenges throughout the Study Period: 2019-2033. It provides crucial insights into the market dynamics from the Base Year: 2025 and projects future expansion during the Forecast Period: 2025-2033, building upon the foundational understanding established in the Historical Period: 2019-2024. The report examines key market segments, including Packaging Substrate, Lead Frame, Bonding Wire, Encapsulating Resin, Ceramic Packaging Material, Chip Bonding Material, and Others, along with their application in Consume Electrons, Automobiles, Communications, Medical, and Other industries. Strategic regional analysis highlights the dominant markets and countries, while a thorough examination of leading players and significant industry developments provides a holistic view of the competitive landscape and technological advancements. This report serves as an indispensable resource for stakeholders seeking to understand and capitalize on the evolving opportunities within the semiconductor packaging materials sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Kyocera, Shinko, Ibiden, LG Innotek, Unimicron Technology, ZhenDing Tech, Semco, KINSUS INTERCONNECT TECHNOLOGY, Nan Ya PCB, Nippon Micrometal Corporation, Simmtech, Mitsui High-tec, Inc., HAESUNG, Shin-Etsu, Heraeus, AAMI, Henkel, Shennan Circuits, Kangqiang Electronics, LG Chem, NGK/NTK, MK Electron, Toppan Printing Co., Ltd., Tanaka, MARUWA, Momentive, SCHOTT, Element Solutions, Hitachi Chemical, Fastprint, Hongchang Electronic, Sumitomo.

The market segments include Type, Application.

The market size is estimated to be USD 72160 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Semiconductor Packaging Materials," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Packaging Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.