1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Modeling?

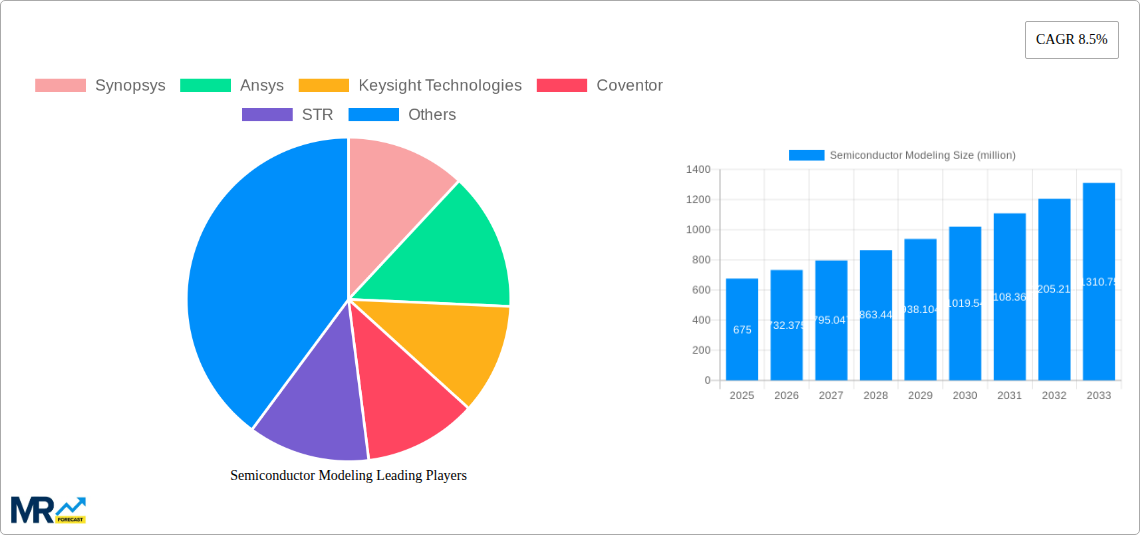

The projected CAGR is approximately 8.5%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Semiconductor Modeling

Semiconductor ModelingSemiconductor Modeling by Type (Cloud-Based, On-Premise), by Application (Automotive, Industrial, Consumer Electronics, Communication, Medical, Aerospace and Defense, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global Semiconductor Modeling market is poised for substantial growth, projected to reach an estimated USD 675 million by 2025 with a robust Compound Annual Growth Rate (CAGR) of 8.5% throughout the forecast period of 2025-2033. This significant expansion is fueled by an increasing demand for sophisticated chip designs, the relentless advancement of semiconductor technology, and the growing complexity of integrated circuits (ICs) across various industries. Key drivers include the proliferation of artificial intelligence (AI) and machine learning (ML) applications, the burgeoning Internet of Things (IoT) ecosystem, and the continuous innovation in consumer electronics, automotive, and telecommunications sectors. These trends necessitate highly accurate and efficient modeling solutions to predict device behavior, optimize performance, and reduce design cycles, thereby accelerating time-to-market for next-generation semiconductor products.

The market is experiencing a dynamic evolution with a strong shift towards cloud-based modeling solutions, offering greater scalability, accessibility, and collaborative capabilities. While on-premise solutions continue to hold relevance, particularly for organizations with stringent data security requirements, the agility and cost-effectiveness of cloud platforms are increasingly attracting adoption. The application landscape is diverse, with Automotive and Industrial segments leading the charge due to the integration of advanced electronics in autonomous vehicles and smart manufacturing. Consumer Electronics, Communication, Medical, and Aerospace & Defense also represent significant growth areas, driven by miniaturization, increased functionality, and stringent performance demands. The competitive landscape is characterized by the presence of established players and innovative startups, all contributing to advancements in simulation accuracy, speed, and feature sets. Strategic collaborations, mergers, and acquisitions are anticipated to further shape the market dynamics as companies strive to enhance their technological offerings and expand their global reach.

Here's a unique report description for Semiconductor Modeling, incorporating the requested elements:

The semiconductor modeling market is experiencing a dynamic evolution, driven by an escalating demand for sophisticated and accurate simulations that underpin the design and optimization of next-generation integrated circuits. Our comprehensive report, spanning the Study Period of 2019-2033 with a Base Year of 2025, forecasts significant growth. In the Estimated Year of 2025, the global semiconductor modeling market is projected to be valued at approximately $7,500 million units. This robust expansion is fueled by the increasing complexity of semiconductor architectures, the relentless miniaturization of transistors, and the growing need for advanced functionalities across a diverse range of applications. The Historical Period of 2019-2024 laid the groundwork for this surge, with consistent year-on-year growth observed as companies increasingly adopted simulation tools to reduce design cycles and mitigate costly manufacturing defects.

The adoption of Cloud-Based semiconductor modeling solutions is rapidly gaining traction, offering unparalleled scalability and accessibility. This shift is particularly evident in the Forecast Period of 2025-2033, where cloud solutions are expected to capture a substantial market share, allowing smaller players and academic institutions to leverage powerful simulation capabilities without significant upfront infrastructure investments. Conversely, On-Premise solutions continue to hold a strong position, especially within large enterprises that prioritize data security and have established robust IT infrastructures. The intricate interplay between these deployment models is shaping the market landscape, with vendors strategically offering hybrid solutions to cater to a broader customer base. Furthermore, the integration of artificial intelligence and machine learning within modeling workflows is a paramount trend, enabling faster and more accurate predictions, as well as the discovery of novel design optimizations. This integration is projected to revolutionize the speed and efficacy of semiconductor development, making the market a highly competitive and innovation-driven space. The increasing demand for power-efficient designs and advanced packaging technologies further amplifies the need for highly precise simulation tools that can accurately predict device behavior under extreme conditions.

The semiconductor modeling market is being propelled by a confluence of powerful driving forces that are reshaping the industry. At the forefront is the insatiable demand for higher performance and increased functionality in electronic devices. As consumer electronics become more sophisticated, and the Internet of Things (IoT) ecosystem expands, the need for smaller, faster, and more energy-efficient chips escalates exponentially. This directly translates into a greater reliance on advanced semiconductor modeling to predict and optimize the behavior of these complex designs before physical fabrication. Furthermore, the relentless pursuit of miniaturization, often termed "Moore's Law," continues to push the boundaries of semiconductor technology. As transistors shrink to nanometer scales, the physical phenomena governing their behavior become more intricate and challenging to predict. Semiconductor modeling tools are indispensable for understanding and mitigating quantum effects, leakage currents, and other nanoscale challenges, ensuring the reliability and performance of these advanced chips. The growing adoption of AI and machine learning in chip design is also a significant propellant. These technologies require highly accurate models to train and validate algorithms, leading to a surge in demand for modeling software that can seamlessly integrate with AI workflows. The increasing complexity of new materials and fabrication processes also necessitates sophisticated modeling capabilities to predict their impact on device performance and reliability.

Despite the robust growth, the semiconductor modeling market faces several significant challenges and restraints that can impede its full potential. A primary hurdle is the escalating complexity and cost of developing and maintaining advanced modeling software. As semiconductor technologies evolve at a breakneck pace, vendors must continuously invest heavily in research and development to keep their tools relevant and accurate. This can create a barrier to entry for smaller companies and potentially lead to market consolidation. Another considerable challenge is the demand for highly skilled personnel. Operating sophisticated modeling software and interpreting complex simulation results requires specialized expertise, and a shortage of qualified engineers and researchers can limit the widespread adoption and effective utilization of these tools. The integration of diverse modeling tools and workflows also presents a challenge. Semiconductor design often involves a multi-stage process, and ensuring seamless data flow and interoperability between different simulation environments can be a complex undertaking. Furthermore, the accuracy and predictive power of models are heavily reliant on the quality and availability of experimental data for calibration and validation. In some emerging areas of semiconductor technology, such as novel materials or advanced quantum computing architectures, obtaining sufficient and reliable experimental data can be difficult, impacting the trustworthiness of the models. Finally, intellectual property concerns and the proprietary nature of certain modeling techniques can sometimes limit collaboration and knowledge sharing within the industry.

The Consumer Electronics segment, particularly within the Asia-Pacific region, is poised to dominate the semiconductor modeling market. This dominance is driven by a powerful synergy of factors, including immense market size, rapid technological adoption, and a highly competitive manufacturing ecosystem.

Asia-Pacific Region:

Consumer Electronics Segment:

Several key factors are acting as potent growth catalysts for the semiconductor modeling industry. The relentless push for miniaturization and increased transistor density in advanced nodes necessitates more sophisticated and accurate modeling to account for complex physical phenomena. The burgeoning demand for AI and machine learning hardware, requiring specialized chips, fuels the need for tailored modeling solutions. Furthermore, the increasing complexity of heterogeneous integration and advanced packaging techniques demands comprehensive simulation capabilities that extend beyond single-die analysis. The growing adoption of cloud-based modeling platforms is democratizing access to advanced simulation tools, broadening the user base and accelerating innovation. Finally, the industry's focus on power efficiency and sustainability is driving demand for modeling solutions that can optimize energy consumption in semiconductor designs.

This report provides an in-depth and holistic view of the semiconductor modeling market, offering granular insights across various facets. We delve into the intricate trends and future trajectories, meticulously analyzing the factors propelling this dynamic industry forward, from the relentless pursuit of miniaturization to the transformative impact of artificial intelligence. Simultaneously, we offer a candid assessment of the challenges and restraints that the market navigates, ensuring a balanced and realistic market perspective. The report highlights the key regions and segments that are set to dominate, with a particular focus on the Asia-Pacific's pivotal role in consumer electronics, detailing the reasons behind their ascendancy. Furthermore, we illuminate the critical growth catalysts that are poised to accelerate market expansion and provide a comprehensive overview of the leading players and their contributions. The report also chronicles the significant historical and anticipated developments within the sector, offering a valuable roadmap for stakeholders. Our extensive coverage aims to equip industry participants with the knowledge necessary to make informed strategic decisions, capitalize on emerging opportunities, and effectively navigate the complex landscape of semiconductor modeling.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.5% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.5%.

Key companies in the market include Synopsys, Ansys, Keysight Technologies, Coventor, STR, Siborg Systems, Esgee Technologies, Applied Materials, Silvaco, Nextnano, ASML, DEVSIM, COMSOL, Microport Computer Electronics, Primarius Technologies.

The market segments include Type, Application.

The market size is estimated to be USD 675 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Semiconductor Modeling," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Modeling, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.