1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Materials for CMP?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Semiconductor Materials for CMP

Semiconductor Materials for CMPSemiconductor Materials for CMP by Type (/> CMP Slurry, CMP Pads, CMP Pad Conditioners, CMP POU Slurry Filters, CMP PVA Brushes, CMP Retaining Rings), by Application (/> 300 Wafers, 200 Wafers, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

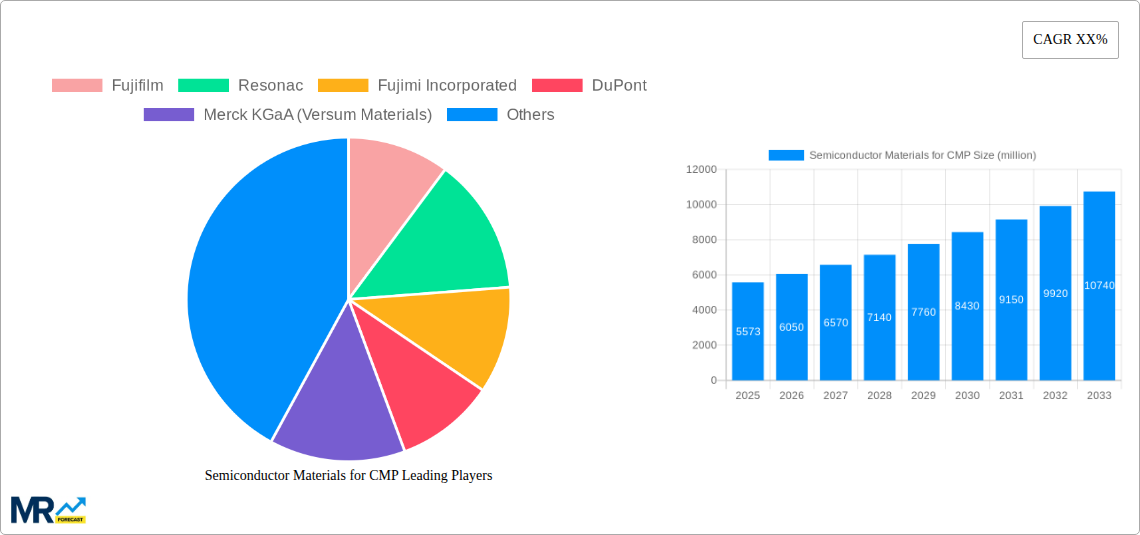

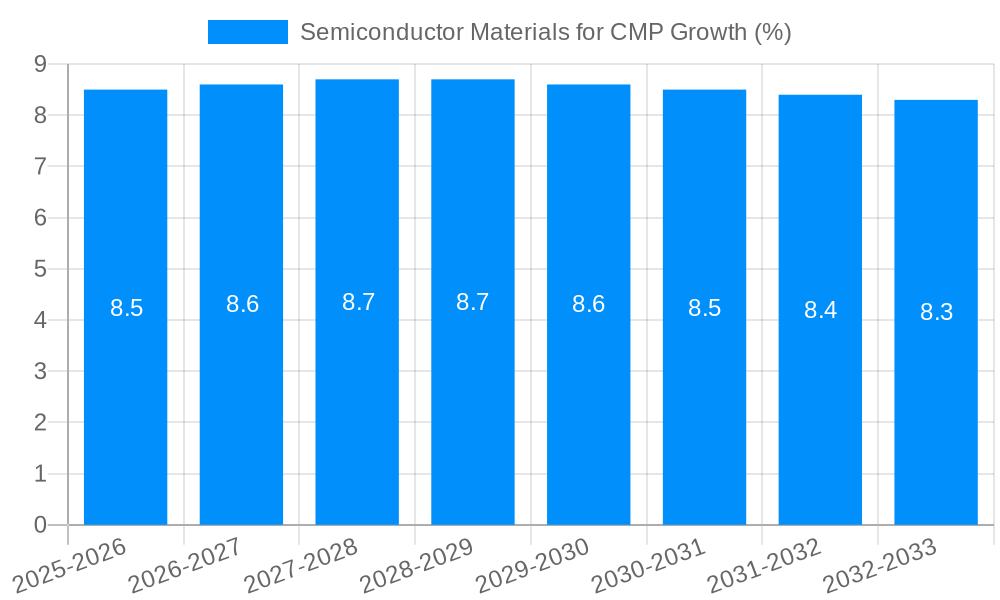

The global market for Semiconductor Materials for Chemical Mechanical Planarization (CMP) is poised for significant expansion, projected to reach an estimated $5573 million in 2025. This robust growth trajectory is fueled by the relentless demand for increasingly sophisticated semiconductor devices, driven by advancements in artificial intelligence, 5G technology, the Internet of Things, and high-performance computing. CMP, a critical process in semiconductor manufacturing, is indispensable for achieving the ultra-flat wafer surfaces required for complex microchip architectures. The market's expansion is further bolstered by the continuous innovation in CMP slurries, pads, and related consumables, designed to enhance precision, reduce defects, and improve yield. Emerging trends such as the development of novel abrasive materials, eco-friendly slurry formulations, and advanced pad conditioning techniques are shaping the competitive landscape and driving investment in research and development.

The market's upward momentum is underpinned by several key drivers, including the increasing complexity of semiconductor nodes, the miniaturization of electronic components, and the rising production of advanced packaging technologies. The shift towards smaller wafer sizes (like 300mm) for enhanced performance and cost-efficiency necessitates higher precision CMP processes, thereby increasing the demand for specialized CMP materials. Conversely, challenges such as stringent environmental regulations and the high cost of advanced CMP materials can pose significant restraints. However, the sheer volume of semiconductor production globally, particularly in the Asia Pacific region, coupled with substantial investments in wafer fabrication facilities, ensures a sustained and growing demand for CMP solutions. The competitive environment is characterized by the presence of major global players and emerging regional manufacturers, all striving to capture market share through product innovation, strategic partnerships, and geographical expansion.

The global market for Semiconductor Materials for Chemical Mechanical Planarization (CMP) is poised for robust expansion, driven by the relentless demand for advanced semiconductor devices. During the historical period of 2019-2024, the market witnessed steady growth, fueled by the increasing complexity of integrated circuits and the need for pristine wafer surfaces. As we enter the base year of 2025, the market is estimated to reach significant figures, projected to exceed $5,000 million in revenue. The study period, spanning from 2019 to 2033, anticipates a Compound Annual Growth Rate (CAGR) that will propel the market beyond $10,000 million by the end of the forecast period. This upward trajectory is intrinsically linked to the continuous advancements in semiconductor manufacturing processes, particularly the miniaturization of transistors and the development of novel chip architectures. The adoption of 300mm wafer technology, a key driver of economies of scale and enhanced production efficiency, has further solidified the importance of high-performance CMP materials.

The market is characterized by a dynamic interplay of innovation and optimization. Manufacturers are constantly striving to develop CMP slurries with enhanced selectivity and reduced defectivity, while CMP pads are engineered for superior durability and material removal uniformity. The introduction of specialized CMP materials for niche applications, such as advanced packaging and heterogeneous integration, is also contributing to market diversification. Furthermore, the growing emphasis on sustainability and environmental regulations is influencing the development of eco-friendly CMP solutions, including low-VOC slurries and recyclable pad materials. The strategic investments in research and development by leading players are crucial in addressing the evolving needs of the semiconductor industry, ensuring that CMP materials remain at the forefront of enabling next-generation semiconductor technologies. The intricate demands of fabricating cutting-edge logic and memory devices, from advanced FinFETs to emerging 3D NAND structures, necessitate highly precise and controlled material removal processes, making CMP an indispensable pillar of modern semiconductor fabrication. The ongoing transition to smaller process nodes, such as 5nm, 3nm, and beyond, amplifies the requirement for CMP solutions that can precisely manage critical dimensions and minimize surface roughness, directly impacting device performance and yield.

The burgeoning demand for sophisticated electronic devices across various sectors, including consumer electronics, automotive, telecommunications, and artificial intelligence, serves as a primary catalyst for the semiconductor materials for CMP market. The relentless pursuit of smaller, faster, and more power-efficient semiconductors necessitates increasingly intricate fabrication processes, where CMP plays a pivotal role in achieving the planar surfaces required for multi-layer interconnects and advanced lithography. The exponential growth in data generation and consumption, driven by cloud computing, the Internet of Things (IoT), and the proliferation of 5G networks, is spurring the development of high-capacity memory chips and high-performance processors, both of which rely heavily on effective CMP techniques. The automotive industry's transition towards electric vehicles and autonomous driving systems further intensifies the need for advanced semiconductor components, thereby boosting the demand for CMP materials. Moreover, government initiatives aimed at promoting domestic semiconductor manufacturing capabilities and bolstering supply chain resilience are leading to increased investments in fabrication facilities, consequently driving the demand for essential consumables like CMP materials. The ongoing miniaturization trend, pushing the boundaries of Moore's Law, continues to increase the complexity of chip designs and fabrication steps, making CMP an even more critical enabling technology.

Despite the promising growth outlook, the semiconductor materials for CMP market faces several challenges and restraints that could impede its progress. One significant hurdle is the escalating cost of raw materials and manufacturing, which can impact the profitability of CMP material suppliers and, consequently, the overall cost of semiconductor production. The stringent quality control and purity requirements for semiconductor-grade materials necessitate substantial investments in advanced manufacturing infrastructure and rigorous testing protocols. Furthermore, the rapid pace of technological evolution in the semiconductor industry demands continuous innovation and adaptation from CMP material providers. Companies must constantly invest in research and development to keep pace with the introduction of new materials, process technologies, and device architectures, which can be a resource-intensive endeavor. The supply chain for specialized chemicals and abrasive particles used in CMP slurries can be complex and prone to disruptions, as highlighted by recent global events, leading to potential shortages and price volatility. The environmental impact of certain CMP chemicals and waste disposal also presents a growing concern, necessitating the development of more sustainable and eco-friendly alternatives, which can require significant R&D investment and may initially face adoption barriers. The need for highly specialized expertise and skilled labor to develop, manufacture, and effectively utilize these advanced CMP materials further adds to the operational complexities.

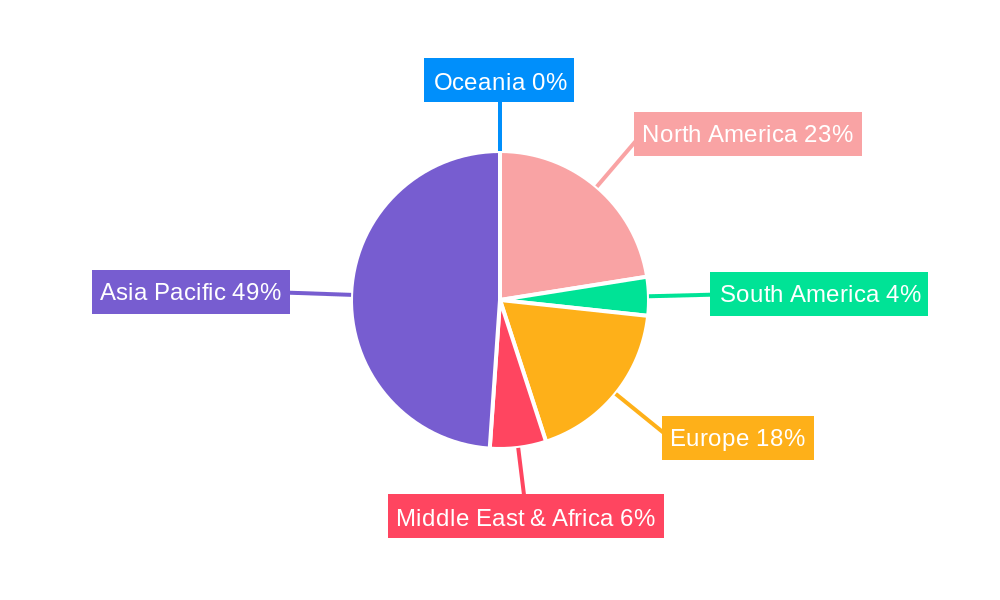

The Asia Pacific region is projected to dominate the global Semiconductor Materials for CMP market, largely driven by the presence of major semiconductor manufacturing hubs and substantial investments in wafer fabrication facilities across countries like China, South Korea, Taiwan, and Japan. The robust growth of the electronics manufacturing industry in this region, coupled with government initiatives to bolster domestic semiconductor production, creates a fertile ground for CMP material suppliers. Within this dominant region, Taiwan stands out as a significant player, owing to its established semiconductor ecosystem and the presence of leading foundries.

Among the various segments, CMP Slurry is expected to hold the largest market share. This dominance is attributed to the indispensable role of CMP slurries in precisely removing material and achieving the desired surface finish during wafer fabrication. The continuous advancements in slurry formulations, aimed at improving selectivity, reducing defects, and enabling the planarization of novel materials like advanced dielectrics and interlayers, further solidify its leading position.

Dominant Region: Asia Pacific

Dominant Segment: CMP Slurry

The 300mm Wafer application segment is also a significant contributor to the market's growth. The transition to 300mm wafers has become the industry standard for high-volume manufacturing due to its cost efficiencies and increased throughput. Consequently, the demand for CMP materials optimized for these larger wafers is substantial. As the industry continues to refine 300mm processes and push towards even more advanced nodes on these wafers, the requirement for high-performance CMP slurries and pads tailored for this application will only intensify. The ability of CMP materials to precisely control material removal and maintain wafer uniformity across the entire 300mm surface is paramount for the successful fabrication of complex integrated circuits.

The accelerating adoption of advanced packaging techniques, such as 2.5D and 3D integration, is a significant growth catalyst for the semiconductor materials for CMP industry. These technologies require multiple layers of interconnects and complex wafer bonding processes, all of which demand highly precise CMP steps to ensure optimal performance and reliability. The increasing integration of AI, machine learning, and high-performance computing (HPC) is driving the demand for more powerful and specialized chips, necessitating further advancements in semiconductor fabrication and, by extension, CMP materials. The ongoing global push towards digitalization across all sectors fuels the demand for semiconductors, indirectly benefiting the CMP materials market.

This comprehensive report offers an in-depth analysis of the global Semiconductor Materials for Chemical Mechanical Planarization (CMP) market, encompassing the historical period of 2019-2024 and extending through a robust forecast period up to 2033. The report delves into the intricate dynamics of market segmentation by product type, including CMP Slurry, CMP Pads, CMP Pad Conditioners, CMP POU Slurry Filters, CMP PVA Brushes, and CMP Retaining Rings. Furthermore, it examines the market's application landscape, with a specific focus on 300mm Wafer and 200mm Wafer technologies, along with other niche applications. The research meticulously identifies and analyzes the key industry developments, driving forces, and challenges that are shaping the market's trajectory. It provides critical insights into regional market dominance, particularly highlighting the pivotal role of the Asia Pacific region, and forecasts future growth patterns. The report also presents a detailed overview of leading market players and their strategic initiatives, offering a holistic understanding of this vital segment of the semiconductor manufacturing ecosystem.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Fujifilm, Resonac, Fujimi Incorporated, DuPont, Merck KGaA (Versum Materials), Fujifilm, AGC, KC Tech, JSR Corporation, Anjimirco Shanghai, Soulbrain, Saint-Gobain, Ace Nanochem, Dongjin Semichem, Vibrantz (Ferro), WEC Group, SKC (SK Enpulse), Shanghai Xinanna Electronic Technology, Hubei Dinglong, Beijing Hangtian Saide, Fujibo Group, 3M, FNS TECH, IVT Technologies Co, Ltd., TWI Incorporated, KPX Chemical, Engis Corporation, TOPPAN INFOMEDIA, Samsung SDI, Entegris, Pall, Cobetter, Kinik Company, Saesol Diamond, EHWA DIAMOND, Nippon Steel & Sumikin Materials, Shinhan Diamond, BEST Engineered Surface Technologies, Willbe S&T, CALITECH, Cnus Co., Ltd., UIS Technologies, Euroshore, PTC, Inc., AKT Components Sdn Bhd, Ensinger, CHUANYAN, Zhuhai Cornerstone Technologies, Konfoong Materials International, Tianjin Helen, Shenzhen Angshite Technology, Advanced Nano Products Co.,Ltd, Zhejiang Bolai Narun Electronic Materials, Xiamen Chia Ping Diamond Industrial.

The market segments include Type, Application.

The market size is estimated to be USD 5573 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Semiconductor Materials for CMP," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Materials for CMP, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.