1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Facility Hook Up Services?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Semiconductor Facility Hook Up Services

Semiconductor Facility Hook Up ServicesSemiconductor Facility Hook Up Services by Type (/> Gas & Pumping Hook-up Services, Chemical Hook-up Services, Water & UPW Line Hook Up, Exhaust Line Hook-up Services, Drain Line Hook-up Services, Vacuum Line Hook-up Services, Waste Line Hook-up Services), by Application (/> 300mm Wafer Fabs, 200mm Wafer Fabs, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

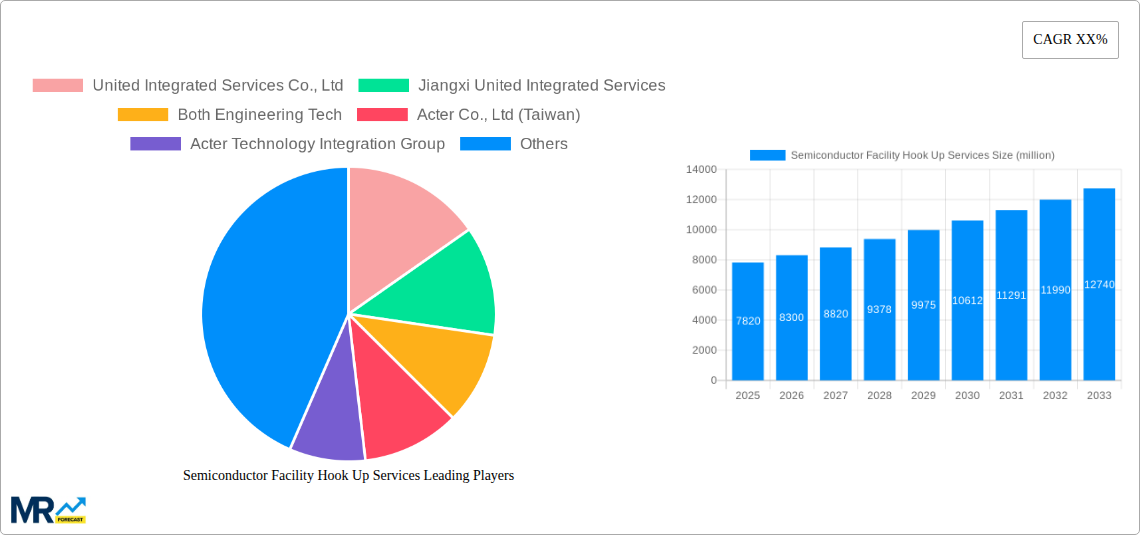

The global semiconductor facility hook-up services market, valued at approximately $7.82 billion in 2025, is poised for significant growth. Driven by the escalating demand for advanced semiconductors across various industries like automotive, consumer electronics, and 5G infrastructure, this market is expected to experience substantial expansion over the forecast period (2025-2033). Key growth drivers include the increasing complexity of semiconductor fabrication plants, requiring specialized expertise in installation and commissioning, and the rising adoption of advanced packaging technologies, which necessitate intricate hook-up processes. Furthermore, the ongoing trend towards automation and the need for higher precision in semiconductor manufacturing are contributing factors. While potential restraints like supply chain disruptions and skilled labor shortages exist, the overall market outlook remains positive. The market is segmented by service type (installation, testing, commissioning, maintenance), geography, and end-user industry. Leading players such as United Integrated Services, Acter Co., Ltd, L&K Engineering, and Jacobs Engineering are strategically investing in advanced technologies and expanding their service portfolios to capture a larger market share. The competitive landscape is characterized by both established players and emerging specialized service providers, resulting in a dynamic market environment.

The competitive landscape within the semiconductor facility hook-up services market is intensely competitive, characterized by a mix of large multinational corporations and specialized regional providers. The success of these companies hinges on factors such as their technical expertise, project management capabilities, and ability to meet stringent quality and safety standards within tight deadlines. The ongoing need for sophisticated technological integration, coupled with the expanding semiconductor manufacturing capacity globally, fosters opportunities for industry consolidation and strategic partnerships. Geographic expansion, particularly into emerging semiconductor manufacturing hubs, and investments in research and development to adapt to evolving industry needs are crucial for sustaining competitive advantage. Future growth will depend on players successfully navigating supply chain challenges, fostering skilled labor pools, and providing innovative solutions to meet the increasingly demanding requirements of advanced semiconductor fabrication processes.

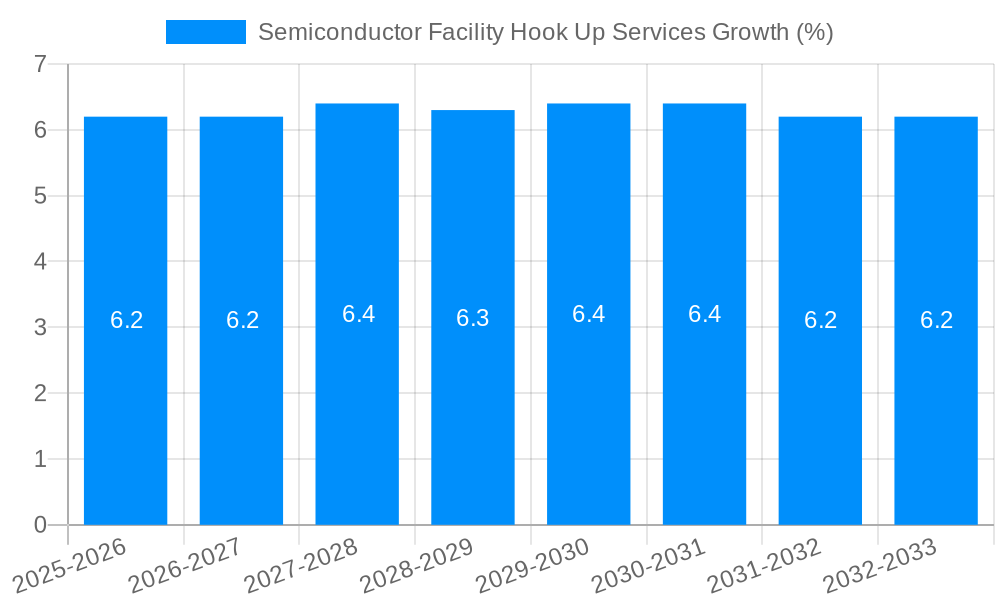

The global semiconductor facility hook-up services market is experiencing robust growth, projected to reach USD XXX million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033). The historical period (2019-2024) witnessed a significant upswing driven by the escalating demand for advanced semiconductor devices across various applications, including smartphones, automotive electronics, and high-performance computing. The estimated market value in 2025 stands at USD XXX million. This surge is primarily fueled by the expanding capacity of semiconductor fabrication plants (fabs) globally, necessitating extensive and specialized hook-up services. Furthermore, the increasing complexity of semiconductor manufacturing processes and the rising adoption of advanced technologies, such as 5G and AI, are further propelling market growth. The shift towards advanced packaging technologies and the increasing need for cleanroom construction and maintenance also significantly contribute to the market's expansion. Geographically, Asia-Pacific, particularly Taiwan, South Korea, and China, remains the dominant region due to the high concentration of semiconductor manufacturing facilities. However, increasing investments in semiconductor manufacturing in North America and Europe are expected to drive regional market growth in the coming years. The market is characterized by a diverse range of service providers, including specialized engineering firms, general contractors, and equipment suppliers, each catering to specific aspects of facility hook-up. The competitive landscape is dynamic, with companies constantly innovating to offer efficient, cost-effective, and technologically advanced solutions to meet the evolving needs of the semiconductor industry. This report provides a comprehensive analysis of market trends, key drivers, challenges, and growth opportunities, offering valuable insights for stakeholders involved in this rapidly growing sector.

The semiconductor industry's relentless pursuit of miniaturization and increased performance drives the demand for advanced facility hook-up services. The construction of new fabs, expansions of existing ones, and technology upgrades necessitate specialized expertise in installing and integrating intricate equipment, handling ultra-pure gases, and ensuring stringent environmental control. The increasing complexity of semiconductor manufacturing processes, incorporating advanced lithography techniques and 3D packaging, requires highly skilled technicians and specialized tools, driving the market for these services. Furthermore, the growing demand for high-performance computing (HPC), artificial intelligence (AI), and 5G technology fuels the need for more advanced semiconductor chips, thereby driving the expansion of fabs and increasing the demand for facility hook-up services. The rising focus on automation and robotics within semiconductor fabrication plants further fuels this demand as these require specific integration and maintenance services. Stringent regulatory compliance and safety standards within the semiconductor industry create a substantial need for specialized hook-up services that can guarantee compliance and minimize operational risks. Finally, the ongoing geopolitical shifts and the desire for regional diversification in semiconductor manufacturing are prompting significant investments in new facilities and expansion in various geographic locations, directly translating to increased demand for these specialized services.

The semiconductor facility hook-up services market faces several challenges. The high precision and cleanliness required in semiconductor manufacturing demand meticulous execution, increasing operational complexities and potentially leading to delays and cost overruns. Acquiring and retaining highly skilled personnel with specialized knowledge of cleanroom environments and semiconductor equipment is a significant hurdle, especially considering the fierce competition for talent in the technology sector. The inherent complexity of semiconductor manufacturing processes and the constant technological advancements necessitate continuous training and upskilling of workforce, representing substantial investments for service providers. Moreover, fluctuations in global semiconductor demand can impact project timelines and budgets, creating uncertainty for service providers. Geopolitical factors, such as trade disputes and sanctions, can disrupt supply chains and create delays in equipment procurement and project completion. Stringent regulatory compliance requirements and safety standards impose strict protocols and necessitate adherence to strict quality control measures, adding to the operational cost. Finally, intense competition among service providers necessitates continuous innovation, efficient resource management and the need to offer competitive pricing, which can negatively impact profit margins.

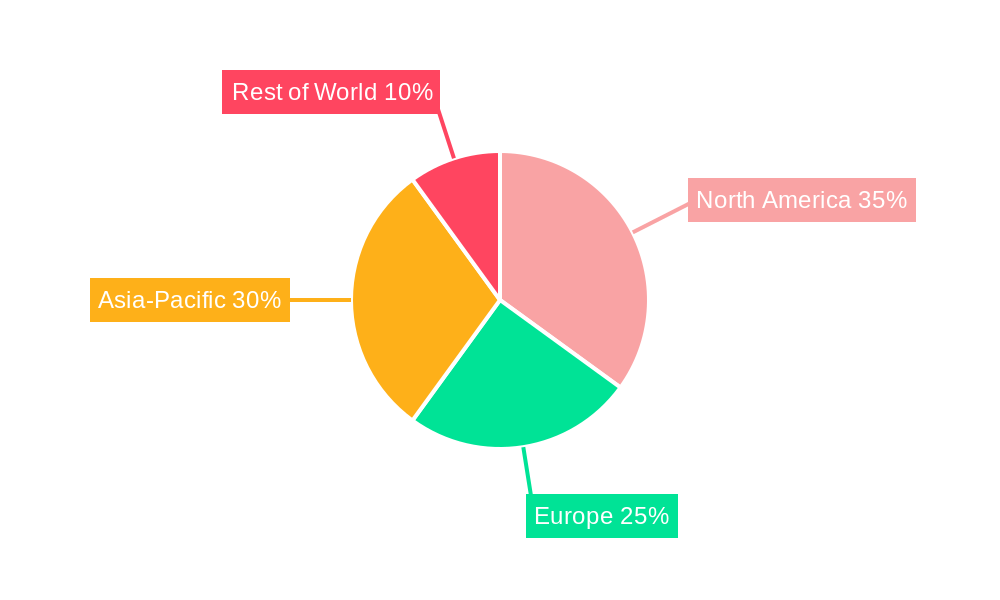

Asia-Pacific (specifically Taiwan, South Korea, and China): This region houses a significant concentration of leading semiconductor manufacturers, driving the demand for facility hook-up services. The ongoing investments in advanced fabs and capacity expansions in these countries solidify their dominance in the market. Taiwan, in particular, holds a strong position due to the presence of Taiwan Semiconductor Manufacturing Company (TSMC) and other major players. South Korea's substantial investments in memory chip manufacturing also contribute to the region's market leadership. China's ambitious plans to become a global semiconductor powerhouse are further fueling the growth of the hook-up services market within the country.

North America & Europe: While currently holding a smaller market share compared to Asia-Pacific, North America and Europe are witnessing a resurgence in semiconductor manufacturing due to geopolitical factors and government incentives. This renewed focus translates into significant growth potential for facility hook-up services providers in these regions. Increased investments in advanced technology and research and development within these regions are also driving the demand.

Segments: The segment focused on cleanroom construction and maintenance is a particularly dominant one, given the critical need for ultra-clean environments in semiconductor fabrication. This segment requires specialized skills and equipment, resulting in higher margins. Similarly, the segment offering specialized equipment installation and integration is crucial for efficient and compliant semiconductor manufacturing, driving high demand.

The combined factors of geographical concentration of manufacturing and specialized high-demand segments contribute to the market dominance of specific players in these areas.

The burgeoning demand for advanced semiconductors across various sectors, coupled with substantial investments in expanding existing fabrication plants and building new ones, acts as a primary growth catalyst. Government incentives and policies aiming to bolster domestic semiconductor manufacturing further stimulate market growth. Technological advancements in semiconductor manufacturing processes, necessitating more complex and specialized hook-up services, also fuels expansion.

This report offers a comprehensive overview of the semiconductor facility hook-up services market, providing detailed insights into market trends, drivers, challenges, and growth opportunities. It includes a detailed analysis of key players, regional dynamics, and segment-specific trends, providing invaluable information for stakeholders in the semiconductor industry. The report's data-driven approach and in-depth analysis make it an essential resource for strategic decision-making and market forecasting.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include United Integrated Services Co., Ltd, Jiangxi United Integrated Services, Both Engineering Tech, Acter Co., Ltd (Taiwan), Acter Technology Integration Group, L&K Engineering, L&K Engineering (Suzhou), Wholetech System Hitech, Yankee Engineering, China Electronics Engineering Design Institute (CEEDI), EDRI (Taiji Industry), CESE2, CEFOC, Exyte, Jacobs Engineering, Samsung C&T Corporation, Hyundai E&C, Kelington Group Berhad (KGB), International Facility Engineering (IFE), ChenFull International, Toyoko Kagaku, Total Facility Engineering (TFE), ACFM E&C, Chuan Engineering, Cleantech Services (CTS).

The market segments include Type, Application.

The market size is estimated to be USD 7820 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Semiconductor Facility Hook Up Services," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Facility Hook Up Services, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.