1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Abatement Systems?

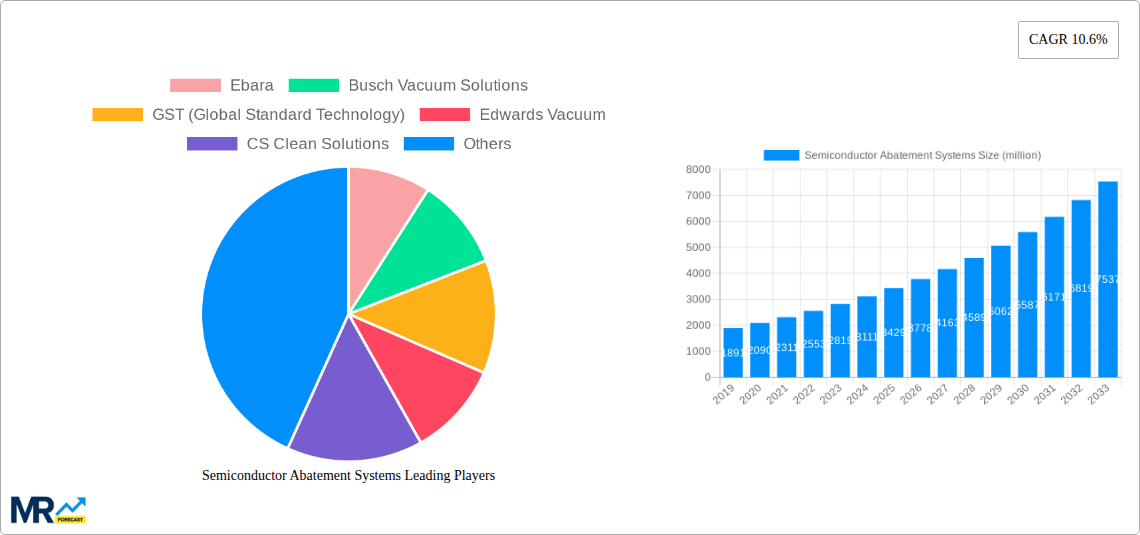

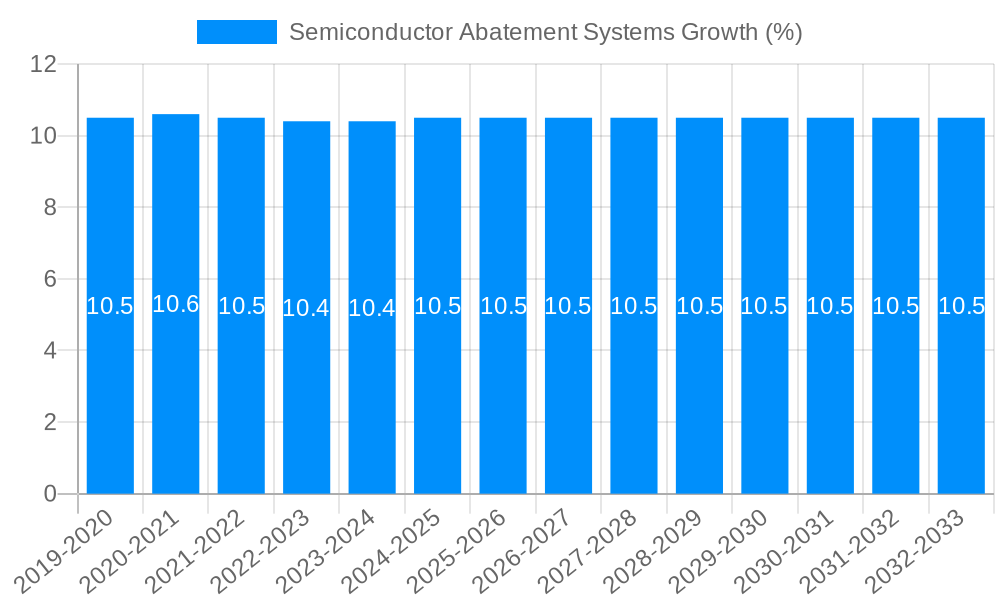

The projected CAGR is approximately 10.6%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Semiconductor Abatement Systems

Semiconductor Abatement SystemsSemiconductor Abatement Systems by Type (Combustion-wash Type, Dry Type, Catalytic Type, Wet Type, Plasma Wet Type, Others), by Application (IDM, Foundry), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global Semiconductor Abatement Systems market is poised for significant expansion, projected to reach a substantial size by 2033, driven by a robust Compound Annual Growth Rate (CAGR) of 10.6% from its 2019 valuation. This growth is primarily fueled by the escalating demand for advanced semiconductor devices across various sectors, including the Internet of Things (IoT), artificial intelligence (AI), and high-performance computing. The increasing complexity of semiconductor manufacturing processes necessitates sophisticated abatement solutions to manage and neutralize the toxic and hazardous byproducts generated during wafer fabrication. Strict environmental regulations globally are also a major catalyst, compelling semiconductor manufacturers to invest in state-of-the-art abatement technologies to comply with emission standards and ensure sustainable operations. The market is witnessing a surge in adoption of advanced abatement techniques, such as plasma wet type and catalytic type systems, which offer higher efficiency and better environmental performance.

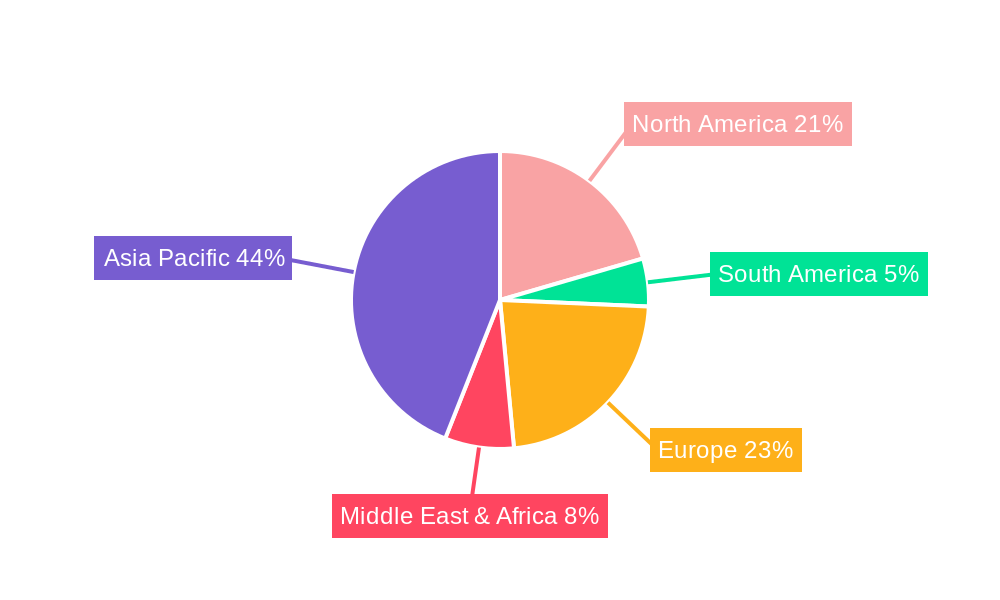

The competitive landscape of the Semiconductor Abatement Systems market is characterized by the presence of established global players and emerging innovators, all vying for market share through technological advancements, strategic partnerships, and product diversification. Key companies like Ebara, Busch Vacuum Solutions, and Edwards Vacuum are at the forefront, offering a comprehensive range of abatement solutions tailored to the specific needs of integrated device manufacturers (IDMs) and foundries. The market is segmented by abatement type, with combustion-wash and dry types holding significant shares, while catalytic and plasma wet types are experiencing rapid growth due to their superior effectiveness in handling complex process gases. Geographically, the Asia Pacific region, particularly China and South Korea, is anticipated to be the largest and fastest-growing market, owing to its dominant position in semiconductor manufacturing and increasing investments in cutting-edge fabrication facilities. North America and Europe also represent substantial markets, driven by technological advancements and stringent environmental policies.

This comprehensive report delves into the dynamic global market for Semiconductor Abatement Systems, offering an in-depth analysis of its trajectory from 2019 to 2033. The study, with a base and estimated year of 2025, and a forecast period spanning 2025-2033, meticulously examines the historical period of 2019-2024 to provide robust market insights. With a projected market size in the hundreds of million units, this report is an essential resource for stakeholders seeking to understand the intricate landscape of semiconductor manufacturing's environmental control solutions. The analysis encompasses key market trends, driving forces, critical challenges, dominant regional and segment performances, significant growth catalysts, and the leading players shaping this crucial industry.

The Semiconductor Abatement Systems market is experiencing a transformative period, driven by an escalating awareness of environmental regulations and the increasing complexity of semiconductor manufacturing processes. As the industry pushes the boundaries of chip miniaturization and advanced materials, the generation of hazardous gases and byproducts has become a critical concern. This has consequently fueled a robust demand for sophisticated abatement technologies designed to neutralize or capture these emissions. The market is witnessing a notable shift towards more energy-efficient and sustainable abatement solutions. While traditional Combustion-wash Type systems remain prevalent, there is a discernible surge in the adoption of Dry Type and Catalytic Type abatement systems, owing to their higher efficiency in handling specific hazardous gases and reduced water consumption. The market size, evaluated in the hundreds of million units, is projected for significant expansion. The increasing prevalence of advanced node manufacturing, particularly in Foundry and IDM applications, necessitates highly specialized abatement solutions capable of handling novel process chemistries. Furthermore, the growing emphasis on circular economy principles is prompting research and development into systems that can not only abate but also recover valuable byproducts, thereby minimizing waste and enhancing resource utilization. The regulatory landscape, which is continuously evolving towards stricter emission standards globally, acts as a significant catalyst for innovation and market growth. Companies are investing heavily in R&D to develop next-generation abatement technologies that offer superior performance, lower operational costs, and a smaller environmental footprint. The integration of smart technologies, such as IoT sensors and AI-driven monitoring, is also becoming a prominent trend, enabling real-time performance tracking, predictive maintenance, and optimized operational efficiency for abatement systems. This holistic approach to environmental management is crucial for the long-term sustainability of the semiconductor industry. The demand for abatement systems is intricately linked to the growth of the semiconductor industry itself, which is currently experiencing unprecedented demand for advanced chips across various sectors like automotive, AI, and consumer electronics, further bolstering the market for these essential environmental control solutions.

The semiconductor abatement systems market is being propelled by a confluence of powerful factors that underscore the industry's commitment to environmental responsibility and operational excellence. Foremost among these drivers is the increasing stringency of global environmental regulations. Governments worldwide are implementing stricter emission standards for hazardous gases and volatile organic compounds (VOCs) generated during semiconductor manufacturing. This necessitates substantial investment in advanced abatement technologies to ensure compliance and avoid significant penalties. Coupled with this is the inherent growth of the semiconductor industry itself. The insatiable demand for advanced chips across sectors like artificial intelligence, 5G, automotive, and data centers fuels increased wafer fabrication, directly translating into a higher volume of process gases requiring abatement. Furthermore, the ongoing transition to more complex and advanced semiconductor manufacturing processes, which often utilize novel and more potent chemistries, inherently generates a wider range of hazardous byproducts, thus demanding more sophisticated and tailored abatement solutions. The pursuit of corporate social responsibility (CSR) and sustainability goals by semiconductor manufacturers also plays a crucial role. Companies are increasingly recognizing the importance of minimizing their environmental footprint not only for regulatory compliance but also for brand reputation and attracting environmentally conscious investors and customers. This has led to a proactive adoption of cutting-edge abatement technologies that offer superior performance and reduced environmental impact. Finally, the economic benefits associated with efficient abatement, such as reduced waste disposal costs and potential for byproduct recovery, further incentivize the adoption of these critical systems.

Despite the robust growth trajectory, the semiconductor abatement systems market encounters several significant challenges and restraints that can temper its expansion. A primary hurdle is the substantial capital investment required for the procurement and installation of advanced abatement systems. These sophisticated technologies, especially those designed for niche applications or handling extremely hazardous substances, can carry a hefty price tag, making them a significant expenditure for semiconductor manufacturers, particularly smaller ones or those in emerging markets. Furthermore, the operational costs associated with these systems, including energy consumption, consumables (such as catalysts or scrubbing media), and regular maintenance, can also be considerable. This can lead to a higher total cost of ownership, which requires careful consideration during investment decisions. Another challenge lies in the dynamic nature of semiconductor manufacturing processes. As new materials and fabrication techniques are introduced, abatement system manufacturers face the continuous need to adapt and innovate. Developing systems that can effectively handle novel, complex, and often highly corrosive or toxic gas mixtures requires significant R&D investment and can lead to obsolescence of existing technologies. The availability of skilled personnel to operate and maintain these complex systems also poses a challenge in certain regions. Proper training and expertise are essential for ensuring optimal performance and safety. Finally, the lack of universally standardized emission regulations across all geographical regions can create complexity for global semiconductor manufacturers, requiring them to implement different abatement strategies for different fabrication sites, thereby increasing operational overhead and potentially hindering economies of scale in abatement technology deployment.

The global Semiconductor Abatement Systems market is characterized by strong regional and segmental dominance, intricately linked to the concentration of semiconductor manufacturing activities and regulatory landscapes.

Dominant Segments:

Type: Dry Type Abatement Systems

Application: Foundry

Dominant Regions:

The combination of a vast manufacturing footprint, a relentless pursuit of technological innovation, and evolving environmental mandates positions APAC, with a particular emphasis on the Foundry segment and Dry Type abatement technologies, as the leading force in the semiconductor abatement systems market for the foreseeable future. The sheer scale of operations and the continuous drive for efficiency and compliance in this region ensure sustained and significant demand for these critical environmental control solutions.

The semiconductor abatement systems industry is propelled by several key growth catalysts. The relentless global demand for advanced semiconductors, driven by AI, 5G, and IoT, fuels increased wafer fabrication, directly boosting the need for abatement solutions. Furthermore, increasingly stringent environmental regulations worldwide are compelling manufacturers to invest in state-of-the-art systems to ensure compliance. The continuous evolution of semiconductor manufacturing processes, involving more complex chemistries and materials, necessitates the development and adoption of sophisticated abatement technologies. The growing emphasis on corporate sustainability and ESG (Environmental, Social, and Governance) initiatives by semiconductor companies also acts as a significant catalyst, promoting proactive investment in emission control.

This report offers a holistic and granular view of the semiconductor abatement systems market. It provides detailed insights into market size estimations and projections in hundreds of million units, coupled with an in-depth analysis of historical trends and future forecasts. The study dissects the market by critical segments, including abatement Type (Combustion-wash, Dry, Catalytic, Wet, Plasma Wet, Others) and Application (IDM, Foundry, Industry), identifying key areas of growth and demand. Furthermore, the report scrutinizes the driving forces, challenges, and significant developments that shape the industry landscape. With a focus on leading players and key regional dynamics, this analysis empowers stakeholders with the knowledge needed to navigate this complex and vital sector of the semiconductor ecosystem.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.6% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 10.6%.

Key companies in the market include Ebara, Busch Vacuum Solutions, GST (Global Standard Technology), Edwards Vacuum, CS Clean Solutions, DAS Environmental Expert, CSK (Atlas Copco), Ecosys Abatement, Highvac, Nippon Sanso, Showa Denko.

The market segments include Type, Application.

The market size is estimated to be USD 1891 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Semiconductor Abatement Systems," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Abatement Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.