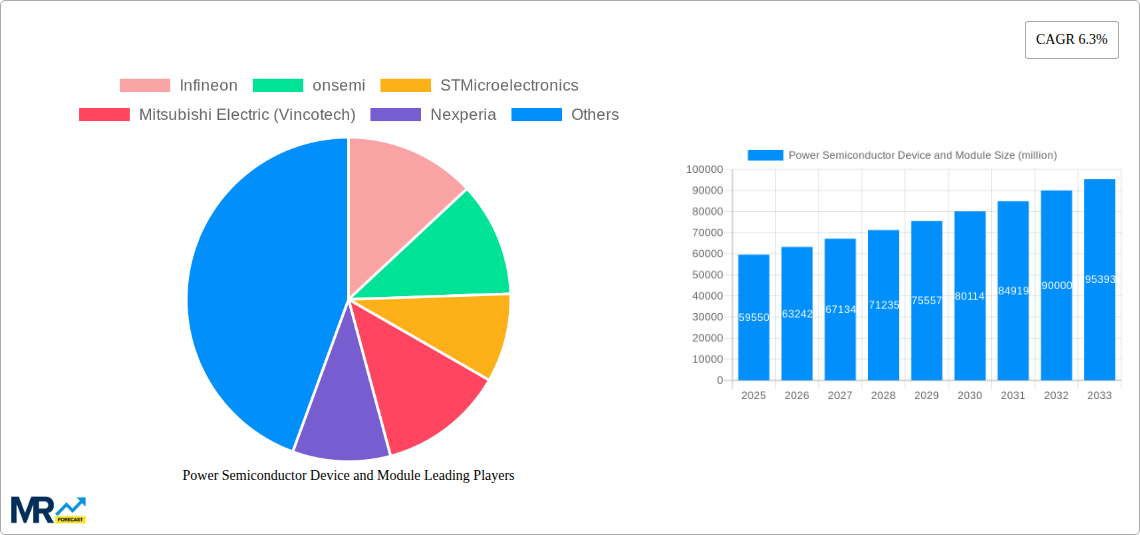

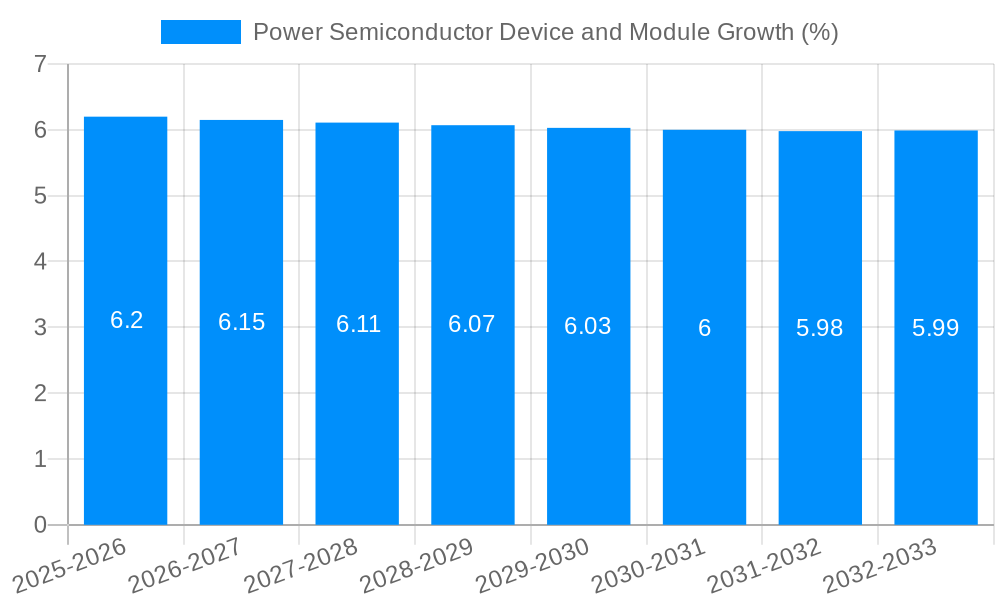

1. What is the projected Compound Annual Growth Rate (CAGR) of the Power Semiconductor Device and Module?

The projected CAGR is approximately 6.3%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Power Semiconductor Device and Module

Power Semiconductor Device and ModulePower Semiconductor Device and Module by Type (MOSFET, Diodes, IGBT, BJT, Thyristor, SiC Power Device, GaN Power Device), by Application (Automotive & EV/HEV, EV Charging, Industrial Motor/Drive, PV, Energy Storage, Wind Power, UPS, Data Center & Server, Rail Transport, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global Power Semiconductor Device and Module market is poised for robust growth, projected to reach approximately USD 59,550 million by 2025, with a Compound Annual Growth Rate (CAGR) of 6.3% expected to persist through 2033. This expansion is primarily fueled by the escalating demand across several critical sectors. The automotive industry, particularly the burgeoning electric vehicle (EV) and hybrid electric vehicle (HEV) segment, is a significant driver, requiring advanced power modules for efficient power management, battery control, and motor drives. Similarly, the renewable energy sector, encompassing photovoltaic (PV) power generation, wind power, and energy storage solutions, relies heavily on high-performance power semiconductors to convert and manage electrical energy effectively. The industrial motor and drive sector also continues to be a substantial contributor, with advancements in automation and energy efficiency mandating the use of sophisticated power devices. Furthermore, the rapid growth of data centers and servers, driven by cloud computing and artificial intelligence, necessitates efficient power supply solutions, bolstering the demand for these components.

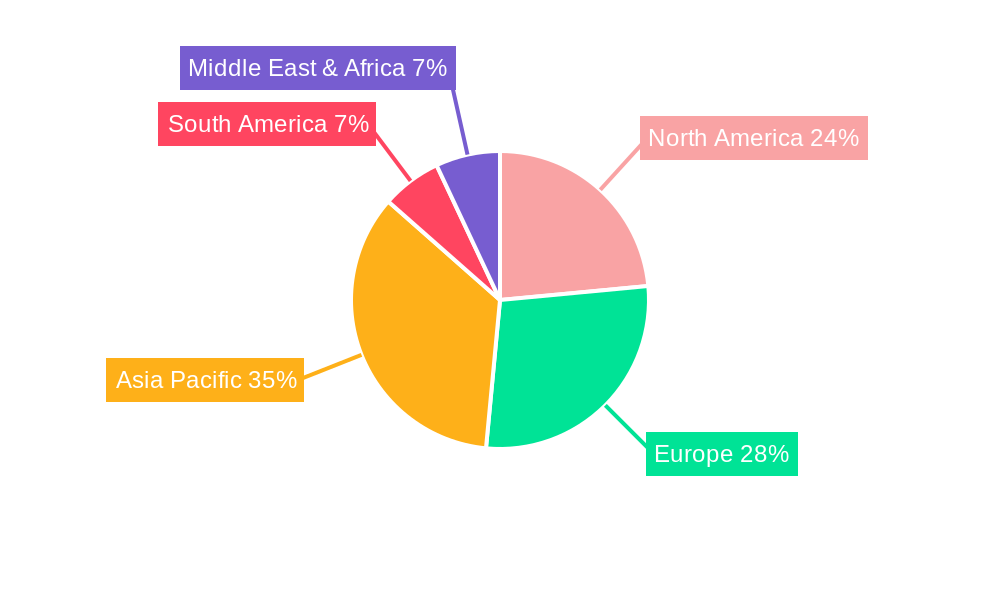

Key trends shaping the power semiconductor landscape include the increasing adoption of wide-bandgap (WBG) materials like Silicon Carbide (SiC) and Gallium Nitride (GaN) power devices, which offer superior efficiency, higher operating temperatures, and smaller form factors compared to traditional silicon-based devices. These advancements are crucial for meeting the stringent performance requirements of modern applications in EVs, renewable energy, and high-power industrial systems. The market is also witnessing a continuous drive towards miniaturization and increased power density. Geographically, the Asia Pacific region, led by China, is expected to dominate the market share due to its extensive manufacturing capabilities and substantial domestic demand across all key application segments. The North America and Europe regions are also significant markets, driven by technological innovation, EV adoption, and investments in smart grids and renewable energy infrastructure. While robust growth is evident, challenges such as intense competition and the need for continuous innovation to keep pace with evolving technological demands present ongoing considerations for market participants.

Here is a unique report description on Power Semiconductor Devices and Modules, incorporating the provided information, values, and structure:

XXX The global power semiconductor device and module market is poised for robust expansion, driven by an insatiable demand for efficient energy conversion and management solutions across a multitude of industries. The market, projected to reach an estimated $XX million in 2025 and expand to $YY million by 2033, will witness a compound annual growth rate (CAGR) of Z.Z% during the forecast period of 2025-2033. This significant surge is intrinsically linked to the escalating adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs), the burgeoning renewable energy sector, and the continuous evolution of industrial automation. The historical period of 2019-2024 has laid the groundwork for this accelerated growth, characterized by increasing investments in R&D and a strategic focus on next-generation materials like Silicon Carbide (SiC) and Gallium Nitride (GaN). These wide-bandgap semiconductors are revolutionizing power electronics by offering superior performance metrics, including higher power density, improved efficiency, and enhanced thermal management capabilities, directly translating to more compact, lighter, and cost-effective power solutions. The base year of 2025 will mark a pivotal point where the market's trajectory becomes clearly defined by these transformative technologies. The integration of advanced power modules, crucial for handling higher voltages and currents, will become increasingly prevalent, particularly in high-power applications such as wind turbines and industrial motor drives. Furthermore, the push towards grid modernization and smart energy infrastructure will continue to fuel demand for reliable and efficient power semiconductors. The evolving landscape also sees a growing emphasis on miniaturization and integration, leading to the development of highly sophisticated power management integrated circuits (PMICs) and compact power modules that cater to the space-constrained requirements of consumer electronics and portable devices. The interplay between technological innovation, policy support for sustainable energy, and industrial digitalization will collectively shape the power semiconductor market's dynamics for years to come, exceeding $AA million in shipments in the coming years.

The power semiconductor device and module market is experiencing an unprecedented surge, fundamentally propelled by the global imperative for energy efficiency and the electrification of various sectors. The automotive industry, particularly the burgeoning electric vehicle (EV) and hybrid electric vehicle (HEV) segment, stands as a paramount driver. With an estimated BB million units of EVs anticipated to be on roads by 2025, each requires a sophisticated power management system, heavily reliant on advanced power semiconductors like MOSFETs, IGBTs, and increasingly, SiC and GaN devices for optimal performance and range. Complementing this is the rapid expansion of the renewable energy sector. The installation of CC million new solar photovoltaic (PV) systems and the continued development of wind farms globally necessitate robust power conversion solutions to efficiently harness and integrate these energy sources into the grid. The demand for electric vehicle charging infrastructure, projected to reach DD million charging points by 2025, further amplifies the need for high-power diodes and modules capable of handling significant energy transfer. Industrial automation and motor drives are also experiencing a significant uplift, driven by Industry 4.0 initiatives that emphasize energy-saving processes and enhanced productivity, requiring millions of power semiconductor devices for efficient motor control.

Despite the overwhelmingly positive growth trajectory, the power semiconductor device and module market faces several significant hurdles that could potentially temper its ascent. A primary concern is the persistent global semiconductor supply chain volatility. Disruptions stemming from geopolitical tensions, trade disputes, and unforeseen events can lead to extended lead times and increased manufacturing costs, impacting the availability of essential components. The intricate nature of advanced power semiconductor manufacturing, especially for SiC and GaN technologies, requires specialized fabrication facilities and a highly skilled workforce. Scaling up production to meet the rapidly escalating demand, estimated to require EE million advanced power devices annually, presents a considerable challenge. Furthermore, the initial higher cost of SiC and GaN devices compared to traditional silicon-based counterparts, although decreasing, can be a restraint for price-sensitive applications. The development of specialized packaging technologies capable of handling the high temperatures and power densities of these advanced materials also presents an ongoing engineering challenge, with an estimated FF million advanced packages required for next-generation modules. Finally, stringent environmental regulations and the increasing complexity of product certifications add layers of compliance challenges for manufacturers, potentially slowing down product development and market entry.

The power semiconductor device and module market is characterized by a dynamic interplay of regional dominance and segment-specific growth, with specific areas poised to lead the charge.

Dominant Segments by Application:

Dominant Regions/Countries:

The synergistic growth of these segments and regions, fueled by technological advancements and policy support, ensures a robust and expanding market landscape for power semiconductor devices and modules, with the potential to surpass OO million units in shipments by the end of the forecast period.

The power semiconductor device and module industry is experiencing accelerated growth, propelled by several key catalysts. The undeniable shift towards electrification, particularly in the automotive sector with the widespread adoption of EVs and HEVs, creates a monumental demand for efficient power management solutions. Secondly, the global push for renewable energy sources like solar and wind power necessitates advanced power electronics for grid integration and energy conversion. Furthermore, the ongoing digitalization of industries, leading to increased automation and smart manufacturing, requires more sophisticated and energy-efficient motor drives and control systems. The continuous innovation in wide-bandgap semiconductor materials like Silicon Carbide (SiC) and Gallium Nitride (GaN) is another critical growth catalyst, offering superior performance characteristics that unlock new levels of efficiency and power density.

Here is a list of leading players in the power semiconductor device and module market:

This report offers a comprehensive analysis of the global power semiconductor device and module market, providing in-depth insights into its current landscape and future trajectory. The study meticulously examines market segmentation by device type (MOSFET, Diodes, IGBT, BJT, Thyristor, SiC Power Device, GaN Power Device) and application (Automotive & EV/HEV, EV Charging, Industrial Motor/Drive, PV, Energy Storage, Wind Power, UPS, Data Center & Server, Rail Transport, Others). The report delves into key market drivers, restraints, opportunities, and challenges, underpinned by robust historical data from 2019-2024 and future projections for the period 2025-2033, with a base year of 2025. Leading players, significant industry developments, and regional market dynamics are thoroughly explored, offering stakeholders valuable intelligence to navigate this rapidly evolving and critical sector of the electronics industry. The report's scope extends to analyzing the impact of emerging technologies and evolving market trends, ensuring a holistic understanding for strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.3% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.3%.

Key companies in the market include Infineon, onsemi, STMicroelectronics, Mitsubishi Electric (Vincotech), Nexperia, Vishay Intertechnology, Toshiba, Fuji Electric, Rohm, Renesas Electronics, Diodes Incorporated, Littelfuse (IXYS), Alpha & Omega Semiconductor, Semikron Danfoss, Hitachi Power Semiconductor Device, Microchip, Sanken Electric, Semtech, MagnaChip, Bosch, Texas Instruments, KEC Corporation, Wolfspeed, PANJIT Group, Unisonic Technologies (UTC), Niko Semiconductor, Hangzhou Silan Microelectronics, Yangzhou Yangjie Electronic Technology, China Resources Microelectronics Limited, Jilin Sino-Microelectronics, StarPower, NCEPOWER, Prisemi, Jiangsu Jiejie Microelectronics, OmniVision Technologies, Suzhou Good-Ark Electronics, Zhuzhou CRRC Times Electric, WeEn Semiconductors, Changzhou Galaxy Century Microelectronics, MacMic Science & Technolog, BYD, Hubei TECH Semiconductors, BASiC Semiconductor, Shandong Jingdao Microelectronics, CETC 55, Guangdong AccoPower Semiconductor, InventChip Technology, United Nova Technology, ANHI Semiconductor, Grecon Semiconductor (Shanghai), Denso.

The market segments include Type, Application.

The market size is estimated to be USD 59550 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Power Semiconductor Device and Module," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Power Semiconductor Device and Module, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.