1. What is the projected Compound Annual Growth Rate (CAGR) of the PoC Inductors for Vehicle Camera?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

PoC Inductors for Vehicle Camera

PoC Inductors for Vehicle CameraPoC Inductors for Vehicle Camera by Type (High Frequency Inductors, Low Frequency Inductors), by Application (Commercial Vehicles, Passenger Vehicles), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

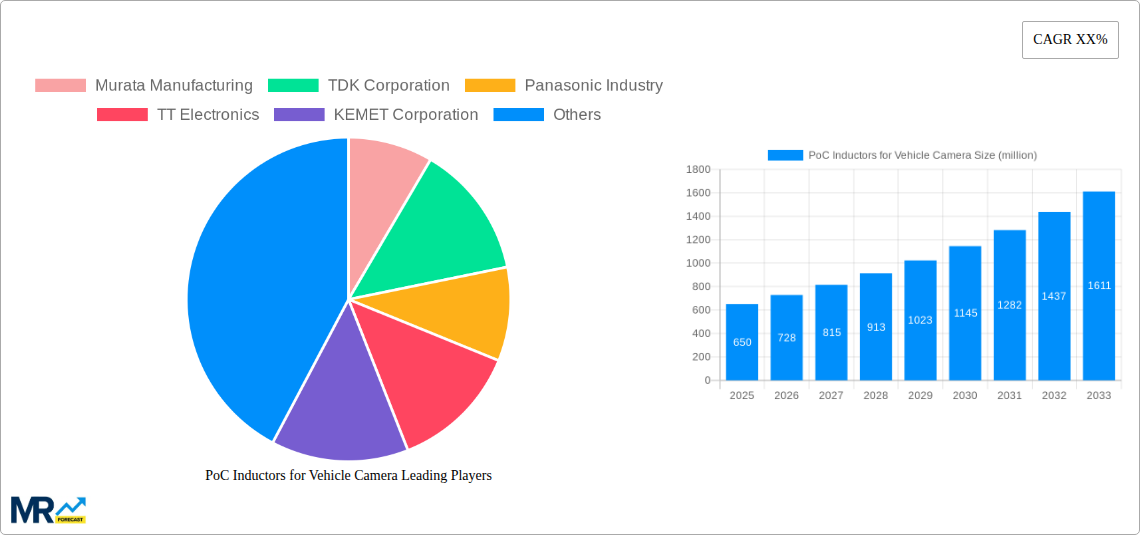

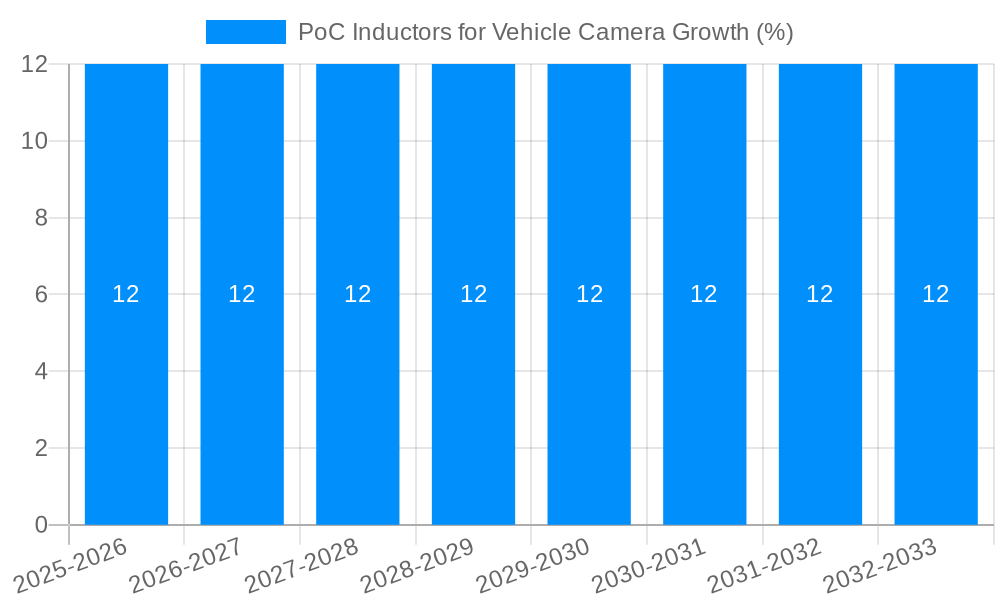

The global market for PoC (Power over Coaxial) Inductors for Vehicle Cameras is experiencing robust growth, driven by the escalating demand for advanced driver-assistance systems (ADAS) and autonomous driving technologies. With an estimated market size of USD 650 million in 2025 and projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 12% through 2033, this sector is poised for significant expansion. The increasing integration of multiple cameras in vehicles for functions like surround-view systems, rear-view cameras, and traffic sign recognition is a primary catalyst. Furthermore, the trend towards higher resolution imaging and more sophisticated sensor fusion demands highly efficient and reliable inductive components. The value unit is expected to reach over USD 1.6 billion by 2033.

The market is segmented by inductor type into High Frequency Inductors and Low Frequency Inductors, with High Frequency Inductors holding a dominant share due to their critical role in high-speed data transmission and noise suppression for camera modules. In terms of applications, Commercial Vehicles and Passenger Vehicles are the key segments, with Passenger Vehicles currently leading due to higher production volumes and a quicker adoption rate of ADAS features. Emerging economies, particularly in Asia Pacific, are showing substantial growth potential, fueled by government initiatives promoting automotive safety and the increasing disposable income of consumers. Key market players are focusing on miniaturization, improved performance, and cost-effectiveness to maintain a competitive edge. However, challenges such as the complexity of supply chains and the need for stringent quality control in automotive applications present moderate restraints.

This report provides an in-depth analysis of the Power over Coax (PoC) Inductors market for vehicle camera applications. The study spans the Study Period of 2019-2033, with a Base Year of 2025 and an Estimated Year also of 2025. The Forecast Period is from 2025-2033, building upon the Historical Period of 2019-2024. The report examines market trends, driving forces, challenges, regional dynamics, growth catalysts, and key players, offering valuable insights for stakeholders in the automotive electronics supply chain. The market size is projected to reach hundreds of millions of units in the coming years, reflecting the escalating adoption of advanced camera systems in vehicles.

The automotive industry is experiencing a transformative shift, driven by the relentless pursuit of enhanced safety, advanced driver-assistance systems (ADAS), and autonomous driving capabilities. Central to these advancements is the proliferation of vehicle cameras, which are becoming indispensable for functionalities ranging from parking assistance and surround-view systems to sophisticated object detection and road sign recognition. This surge in camera integration directly fuels the demand for Power over Coax (PoC) inductors, critical components that enable the simultaneous transmission of both power and data over a single coaxial cable. The trend towards higher resolution cameras and increased data bandwidth requirements is pushing the development of PoC inductors with superior performance characteristics. Manufacturers are focusing on miniaturization to accommodate increasingly constrained automotive spaces, alongside the development of inductors capable of handling higher power densities and wider operating temperature ranges. The evolving regulatory landscape, with a growing emphasis on automotive safety standards, further solidifies the importance of reliable and efficient PoC inductor solutions. We anticipate a steady increase in the adoption of advanced PoC inductor technologies, including integrated solutions and components designed for high-frequency applications, to meet the ever-growing demands of sophisticated automotive camera systems. The market is witnessing a gradual move towards more intelligent and integrated PoC solutions, aligning with the broader trend of electrification and digitalization within the automotive sector. The need for robust electromagnetic interference (EMI) suppression is also a significant trend, as the increasing density of electronic components within a vehicle necessitates highly effective filtering capabilities, which PoC inductors play a crucial role in providing. Furthermore, the pursuit of cost optimization within the automotive supply chain will drive innovation in manufacturing processes for PoC inductors, aiming to achieve higher production yields and reduce per-unit costs without compromising on quality or performance. The increasing complexity of automotive electronic architectures also necessitates PoC inductors that offer improved thermal management properties, ensuring operational stability under demanding conditions.

The burgeoning demand for PoC inductors in vehicle camera applications is propelled by several powerful forces, chief among them being the escalating adoption of advanced driver-assistance systems (ADAS). As vehicle manufacturers strive to enhance safety and convenience, features like adaptive cruise control, lane departure warning, and automatic emergency braking, all heavily reliant on camera data, are becoming mainstream. This widespread integration of ADAS directly translates into a higher number of cameras per vehicle, consequently boosting the need for efficient power and data transmission solutions like PoC inductors. Furthermore, the growing consumer preference for enhanced visibility and convenience, evident in the increasing popularity of 360-degree camera systems and advanced parking aids, further underpins this market growth. The continuous advancements in camera technology, leading to higher resolutions and increased data throughput, necessitate robust and reliable power delivery and signal integrity, areas where PoC inductors excel. The automotive industry's push towards electrification and the development of more complex in-vehicle networks also create a favorable environment for PoC inductor adoption, as they contribute to simplified wiring harnesses and reduced overall system weight. Moreover, stringent automotive safety regulations worldwide are increasingly mandating the inclusion of advanced safety features, indirectly driving the demand for the camera systems and their associated components, including PoC inductors. The trend towards connected vehicles and the need for seamless data exchange for infotainment and telematics also indirectly benefit the PoC inductor market by encouraging the adoption of more sophisticated camera-based systems. The pursuit of fuel efficiency and weight reduction in vehicles also favors solutions that simplify wiring, making PoC technology an attractive proposition.

Despite the robust growth prospects, the PoC inductors for vehicle camera market faces several challenges and restraints that could impede its full potential. One of the primary hurdles is the increasing complexity of automotive electronic systems and the stringent reliability requirements associated with vehicle safety. Ensuring that PoC inductors can consistently perform under extreme temperature variations, vibration, and harsh environmental conditions encountered in vehicles is a significant engineering challenge. The miniaturization trend, while desirable for space-saving, can lead to increased thermal management concerns, requiring careful design and material selection to prevent overheating and performance degradation. Furthermore, the cost sensitivity of the automotive industry poses a restraint. Manufacturers are constantly seeking cost-effective solutions, and the integration of advanced PoC inductor technologies may face resistance if the perceived value does not outweigh the additional cost. The standardization of PoC technology across different automotive manufacturers and camera suppliers is another area that requires attention. A lack of unified standards can lead to fragmentation and increased development efforts for component suppliers. Moreover, the emergence of alternative technologies for power and data transmission, while not yet a major threat, could present a future restraint if they offer comparable or superior performance at a lower cost. The supply chain for specialized inductor components can also be complex, and ensuring a consistent and reliable supply of high-quality PoC inductors to meet the massive volume demands of the automotive industry can be a challenge. Finally, the development of highly integrated System-on-Chips (SoCs) that incorporate power management and data processing capabilities could potentially reduce the need for discrete PoC inductor components in some future designs, although the need for filtering and impedance matching will likely persist.

The Passenger Vehicles segment, particularly those equipped with advanced driver-assistance systems (ADAS) and infotainment cameras, is poised to dominate the PoC inductors for vehicle camera market. This dominance is fueled by the sheer volume of passenger vehicles manufactured globally and the increasing penetration of camera-based safety and convenience features in this segment. From basic rearview cameras to sophisticated surround-view systems and forward-facing cameras for ADAS, the demand for reliable PoC inductors is exceptionally high.

Key Regions:

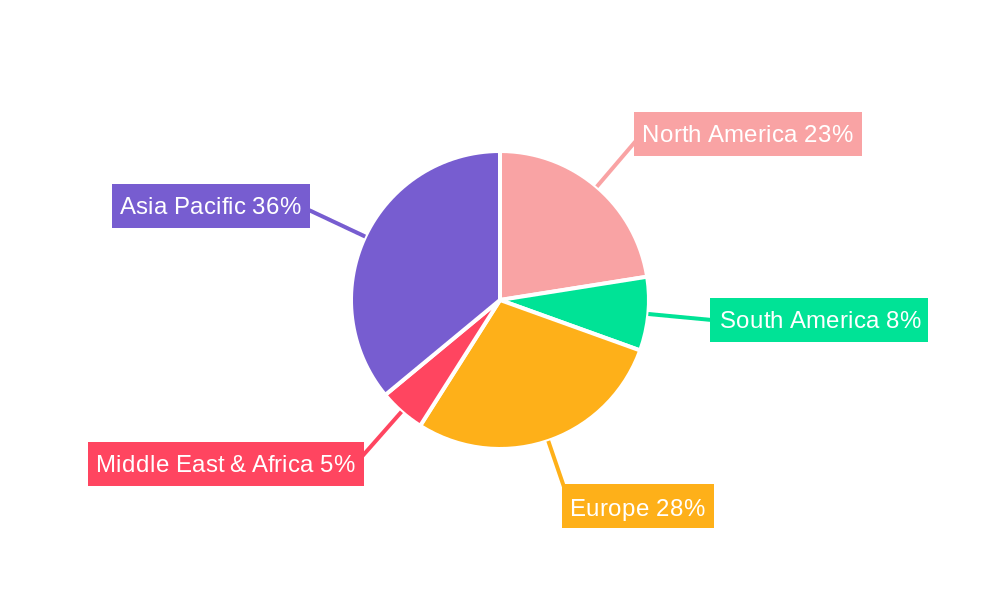

Asia Pacific: This region is expected to lead the market due to its status as the world's largest automotive manufacturing hub.

North America: This region is a major consumer of advanced automotive technologies, driven by consumer demand for safety and convenience features.

Europe: Europe's stringent safety regulations and its commitment to developing sustainable and autonomous mobility solutions make it a key market.

Dominant Segment:

The PoC inductors for vehicle camera industry is experiencing robust growth, catalyzed by several key factors. The relentless advancement and widespread adoption of Advanced Driver-Assistance Systems (ADAS) is a primary growth driver. Features like automatic emergency braking, lane keeping assist, and adaptive cruise control rely heavily on camera data, thereby increasing the number of cameras per vehicle and the demand for their supporting components. Furthermore, the increasing consumer demand for enhanced safety, convenience, and infotainment features, such as 360-degree camera systems and digital rearview mirrors, directly translates into higher volumes of PoC inductors. The ongoing trend of vehicle electrification and the associated simplification of wiring harnesses also favor PoC technology, which enables power and data transmission over a single cable, reducing complexity and weight.

This comprehensive report offers a detailed examination of the Power over Coax (PoC) Inductors market specifically for vehicle camera applications. It delves into the intricate landscape of market trends, providing actionable insights derived from extensive research. The report meticulously analyzes the driving forces behind market expansion, such as the pervasive adoption of ADAS and the escalating consumer demand for advanced in-car features. Simultaneously, it sheds light on the critical challenges and restraints that stakeholders must navigate, including technical complexities and cost sensitivities. Furthermore, the report provides a granular regional analysis, identifying key markets and countries poised for significant growth, with a particular focus on the dominant Passenger Vehicles segment and the pivotal role of High Frequency Inductors. Growth catalysts are clearly outlined, highlighting the factors poised to accelerate market expansion in the coming years. The report also includes a comprehensive list of leading manufacturers and a timeline of significant past and future developments, offering a holistic view of the market's trajectory and its potential.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Murata Manufacturing, TDK Corporation, Panasonic Industry, TT Electronics, KEMET Corporation, Vishay Intertechnology, Bourns, Eaton, Coilcraft, TAI-TECH Advanced Electronics, Shenzhen Sunlord Electronics, Shenzhen Cenker Enterprise, Shenzhen Microgate Technology, Guangdong Fenghua Advanced Technology.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "PoC Inductors for Vehicle Camera," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the PoC Inductors for Vehicle Camera, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.