1. What is the projected Compound Annual Growth Rate (CAGR) of the Phase Change Thermal Pads?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Phase Change Thermal Pads

Phase Change Thermal PadsPhase Change Thermal Pads by Type (Thermal Conductivity: <3 W/mK, Thermal Conductivity: 3-6 W/mK, Thermal Conductivity: 6-8 W/mK, Thermal Conductivity: >8 W/mK, World Phase Change Thermal Pads Production ), by Application (Electronics, Industrials, Communications, Others, World Phase Change Thermal Pads Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

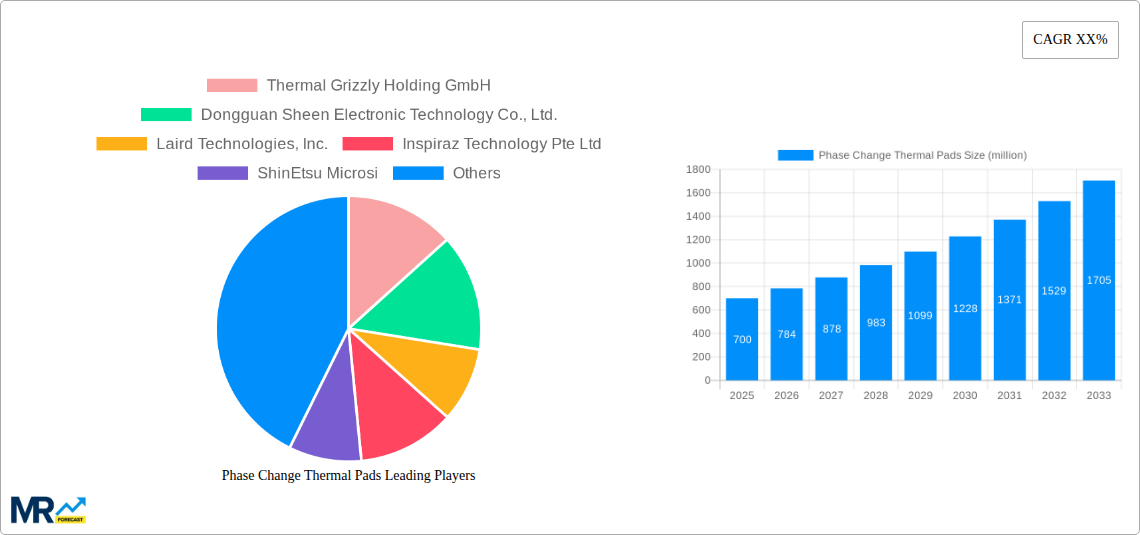

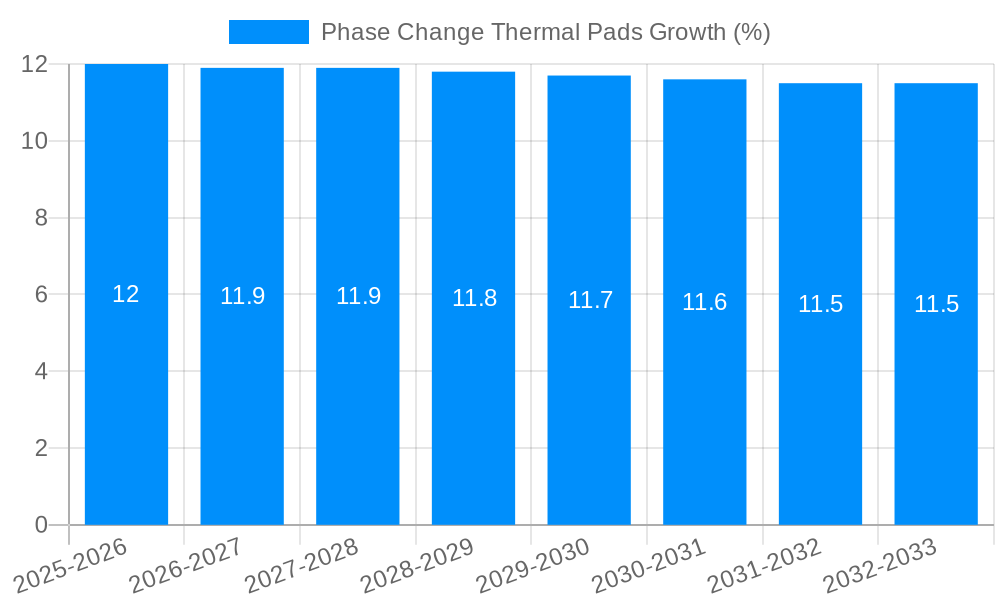

The global Phase Change Thermal Pads market is experiencing robust growth, projected to reach approximately $700 million by 2025, with an impressive Compound Annual Growth Rate (CAGR) of around 12% anticipated throughout the forecast period (2025-2033). This expansion is primarily fueled by the escalating demand for high-performance thermal management solutions across a diverse range of industries. The electronics sector, encompassing consumer electronics, high-performance computing, and gaming devices, stands as a principal driver, necessitating efficient heat dissipation to ensure optimal performance and longevity. The burgeoning communications infrastructure, driven by 5G deployment and data center expansion, further bolsters this demand. Industrial applications, from power electronics and automotive components to medical devices, also represent a significant growth avenue, as these sectors increasingly adopt sophisticated technologies that generate substantial heat. The market is characterized by a steady increase in the adoption of pads with higher thermal conductivity ratings (e.g., >8 W/mK), reflecting the trend towards more compact and powerful electronic devices.

Several key trends are shaping the Phase Change Thermal Pads landscape. Innovations in material science are leading to the development of thinner, more flexible, and higher-performing pads, enhancing ease of application and thermal efficiency. The increasing miniaturization of electronic components, coupled with rising power densities, creates a persistent need for advanced thermal interface materials (TIMs). Furthermore, the growing emphasis on energy efficiency and the extended lifespan of electronic equipment are pushing manufacturers to integrate superior thermal management solutions like phase change materials. While the market exhibits strong growth, certain restraints exist, including the relatively high cost of certain advanced phase change materials and the ongoing competition from other TIMs like thermal pastes and graphite sheets. However, the unique benefits of phase change pads – their reworkability, ease of automation in assembly, and consistent performance – are expected to mitigate these challenges and sustain market momentum.

Here is a report description on Phase Change Thermal Pads, incorporating the provided information and adhering to the specified format:

The global phase change thermal pads market is poised for significant expansion, driven by an escalating demand for efficient thermal management solutions across a multitude of high-growth sectors. During the study period of 2019-2033, with a base year of 2025, the market is projected to witness robust compound annual growth rates. This surge is fundamentally linked to the relentless miniaturization and increasing power density of electronic devices. As processors become more potent and compact, the need to dissipate heat effectively becomes paramount to prevent performance degradation and ensure longevity. The forecast period of 2025-2033, building upon the estimated year of 2025, anticipates a market valuation in the hundreds of millions of dollars, underscoring its critical importance. Innovations in material science are continuously yielding phase change materials with enhanced thermal conductivity, pushing the boundaries of what is achievable. The segment of thermal conductivity exceeding 8 W/mK is likely to experience the most dynamic growth, as industries push for ever-higher performance metrics. Similarly, the applications within the electronics sector, particularly in high-performance computing, artificial intelligence, and 5G infrastructure, will continue to be the primary demand drivers. The historical period of 2019-2024 has laid a strong foundation, characterized by a steady increase in adoption as engineers recognized the inherent advantages of phase change materials over traditional thermal pastes and greases, such as their ease of application, reusability, and excellent gap-filling capabilities. The transition from liquid to solid states at operating temperatures provides a reliable and consistent thermal interface, a feature increasingly valued in demanding environments. The world phase change thermal pads production is expected to see a substantial increase to meet this burgeoning demand, with advancements in manufacturing processes contributing to improved product quality and cost-effectiveness. The industry is moving towards a future where thermal management is not an afterthought but an integral part of product design.

Several pivotal factors are orchestrating the upward trajectory of the phase change thermal pads market. Foremost among these is the insatiable appetite for enhanced performance in electronic devices. Modern processors, graphics cards, and other semiconductor components are generating unprecedented levels of heat as they push the boundaries of computational power. Phase change thermal pads offer a superior solution for dissipating this heat compared to conventional methods, ensuring optimal operating temperatures and preventing thermal throttling. Furthermore, the exponential growth of the Internet of Things (IoT) ecosystem, coupled with the rollout of 5G networks, is generating a massive influx of connected devices, each requiring reliable thermal management. From smart home appliances to industrial sensors and telecommunications equipment, the need for efficient heat dissipation is universal. The increasing complexity and miniaturization of electronic circuitry further exacerbate thermal challenges, making the precise and consistent thermal interface provided by phase change pads indispensable. The drive towards higher power efficiency in electronics also indirectly fuels the demand for advanced thermal solutions, as more efficient components still require effective heat removal to maintain their performance and lifespan. As a result, the global phase change thermal pads production is steadily increasing to meet this escalating global requirement.

Despite the promising outlook, the phase change thermal pads market is not without its impediments. One significant challenge revolves around the cost of high-performance phase change materials, particularly those exhibiting thermal conductivities exceeding 8 W/mK. While the performance benefits are undeniable, the premium pricing can be a barrier for some cost-sensitive applications, especially in the lower-tier consumer electronics market. Another challenge lies in the manufacturing complexity and quality control required for consistent product performance. Variations in material composition or application techniques can lead to inconsistent thermal transfer, potentially impacting device reliability. Furthermore, the emergence of alternative advanced thermal interface materials, such as liquid metal thermal interfaces and advanced thermal pastes, presents a competitive landscape. While phase change pads offer distinct advantages in terms of ease of use and reusability, these alternatives can sometimes offer even higher thermal conductivity or a more established market presence in specific niches. The development of robust and standardized testing methodologies to accurately assess and compare the long-term performance and reliability of different phase change thermal pads across diverse operating conditions also remains an ongoing area of focus for the industry. The world phase change thermal pads production needs to continually innovate to overcome these hurdles.

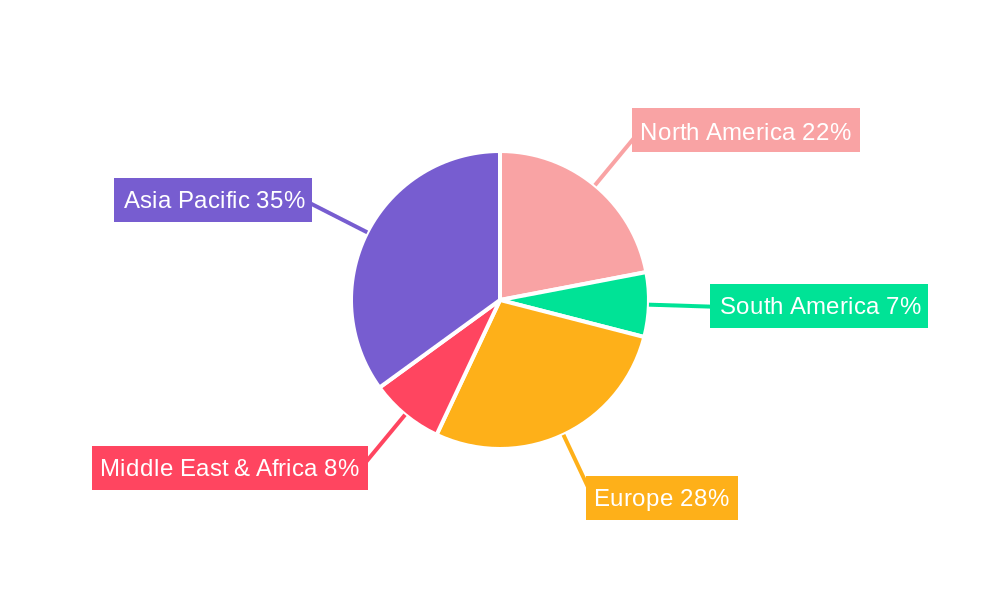

The dominance of specific regions and segments within the global phase change thermal pads market is a multifaceted phenomenon, driven by industrial concentration, technological advancement, and consumer demand.

Dominant Regions/Countries:

Asia Pacific: This region is unequivocally the powerhouse of the global phase change thermal pads market. Its dominance stems from:

North America: While not a manufacturing behemoth on the same scale as Asia Pacific, North America exerts significant influence through:

Dominant Segments:

Thermal Conductivity: >8 W/mK: This segment is poised for exceptional growth and is expected to dominate the market in the coming years.

Application: Electronics: The electronics sector will continue to be the bedrock of the phase change thermal pads market, encompassing a vast array of sub-segments:

The growth of the phase change thermal pads industry is propelled by several key catalysts. The relentless pursuit of higher performance and power efficiency in electronics necessitates advanced thermal management. The proliferation of 5G technology and the Internet of Things (IoT) are creating a massive ecosystem of interconnected devices, each requiring effective heat dissipation. Furthermore, the automotive industry's rapid shift towards electric vehicles, with their complex power electronics, presents a significant growth opportunity. Miniaturization trends in electronics further amplify the need for compact and efficient thermal solutions.

This report offers a holistic view of the phase change thermal pads market, delving into intricate details of its growth trajectory. It meticulously analyzes market trends, identifies key driving forces such as the increasing power density of electronics and the expansion of 5G and IoT networks, and scrutinizes challenges including cost constraints and competitive alternatives. The report further pinpoints dominant regions and segments, such as the Asia Pacific market and the high-conductivity (>8 W/mK) category, providing in-depth insights into their market share and future potential. It also outlines critical growth catalysts and provides a comprehensive list of leading industry players and their significant recent developments.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Thermal Grizzly Holding GmbH, Dongguan Sheen Electronic Technology Co., Ltd., Laird Technologies, Inc., Inspiraz Technology Pte Ltd, ShinEtsu Microsi, AI Technology, Inc., T-Global Technology, Shielding Solutions Ltd, Honeywell International Inc., Henkel Singapore Pte. Ltd., Dobon, Dongguan Ziitek Electronical Material and Technology, Ltd., Zesion, Hemi Electronics.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Phase Change Thermal Pads," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Phase Change Thermal Pads, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.