1. What is the projected Compound Annual Growth Rate (CAGR) of the LCD and OLED Panel?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

LCD and OLED Panel

LCD and OLED PanelLCD and OLED Panel by Type (/> LCD Panel, OLED Panel), by Application (/> Consumer Electronics, Commercial Screens, Transportation Equipment, Industrial Instruments, Medical Equipment), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

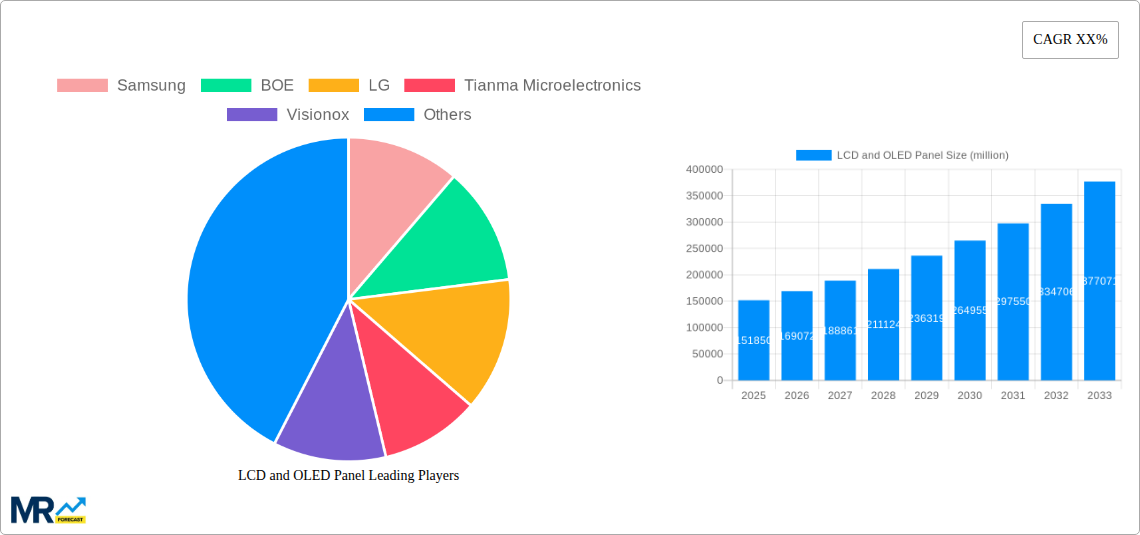

The global LCD and OLED panel market is poised for significant expansion, projected to reach a substantial market size of $151,850 million by 2025. This growth is fueled by the relentless demand for high-quality displays across a diverse range of applications, from cutting-edge consumer electronics like smartphones and televisions to critical commercial screens, advanced transportation equipment, and specialized industrial and medical instruments. The inherent advantages of both LCD and OLED technologies continue to drive their adoption. LCD panels, known for their cost-effectiveness and established manufacturing processes, remain a dominant force, particularly in larger screen applications. Meanwhile, OLED technology is carving out a substantial niche with its superior color accuracy, deep blacks, and flexible form factors, making it the preferred choice for premium devices and emerging form factors. The continuous innovation in display technology, including advancements in resolution, refresh rates, and energy efficiency, further bolsters market confidence and investment.

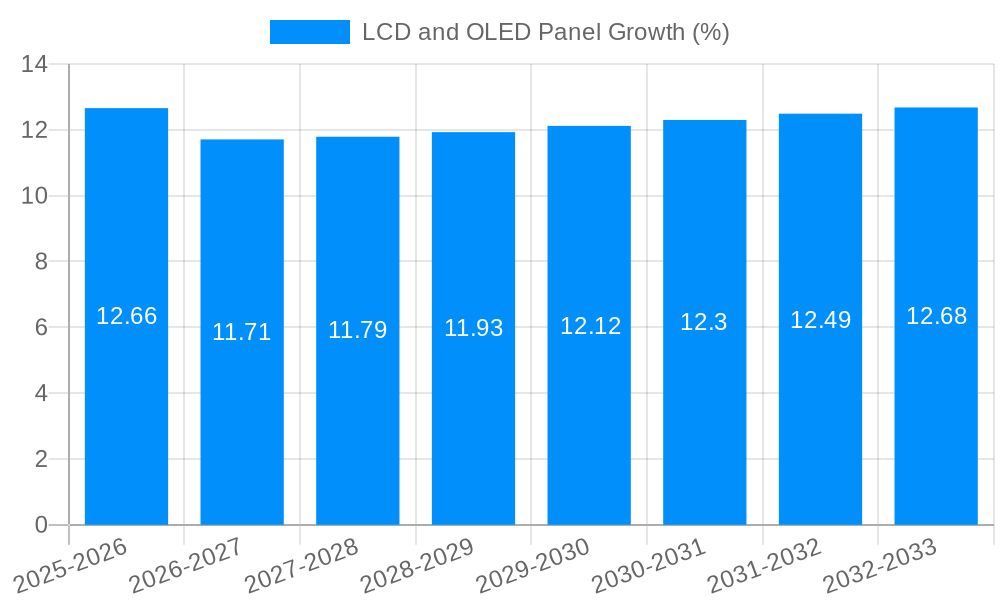

The projected Compound Annual Growth Rate (CAGR) of approximately 12-15% over the forecast period (2025-2033) underscores the robust health and dynamism of this market. Key growth drivers include the increasing disposable income in emerging economies, leading to higher consumer spending on advanced electronics, and the ongoing digital transformation across industries, necessitating sophisticated display solutions for everything from digital signage to in-vehicle infotainment systems and medical imaging. Despite this strong upward trajectory, the market faces certain restraints. The significant capital investment required for advanced manufacturing facilities and the ongoing research and development for next-generation display technologies can present barriers to entry. Furthermore, fluctuations in raw material costs and supply chain disruptions can impact profitability. Nevertheless, the persistent drive for thinner, brighter, more efficient, and more versatile displays, coupled with an expanding application landscape, ensures a positive outlook for both LCD and OLED panel manufacturers.

Here's a unique report description for LCD and OLED Panels, incorporating your specified elements:

The global LCD and OLED panel market is poised for dynamic evolution, driven by relentless technological advancements and the insatiable demand from a multitude of consumer and industrial applications. Over the study period from 2019 to 2033, with a base year of 2025, the market is expected to witness substantial shifts in technology adoption and market share. The historical period of 2019-2024 laid the groundwork, characterized by the dominance of LCD technology in a wide array of devices, from smartphones and televisions to automotive displays. However, the ascendant OLED technology has steadily carved out its niche, particularly in premium segments, owing to its superior contrast ratios, deeper blacks, and faster response times.

The estimated year of 2025 marks a critical juncture, with significant investments being channeled into next-generation panel manufacturing capabilities. We anticipate a continued bifurcation of the market, where LCD technology will remain a cost-effective and high-volume solution for many applications, especially in large-format displays and budget-conscious consumer electronics. Conversely, OLED is projected to experience exponential growth, fueled by its increasing adoption in flagship smartphones, high-end televisions, and emerging applications such as flexible and foldable displays. The forecast period of 2025-2033 will likely see an acceleration of this trend, with OLED gaining further traction across more mainstream consumer devices. The market's overall trajectory, measured in millions of units, indicates a robust and expanding landscape. Strategic shifts in manufacturing capacities and R&D focus will be pivotal in shaping the competitive dynamics within this multi-billion dollar industry. The intricate interplay between innovation, manufacturing scale, and application diversification will define the future of both LCD and OLED panels.

The LCD and OLED panel industry is propelled by a confluence of powerful drivers that are reshaping consumer expectations and industrial requirements. A primary catalyst is the ever-increasing consumer appetite for more immersive and visually engaging experiences. This translates into a demand for larger screen sizes, higher resolutions (such as 4K and 8K), and enhanced color accuracy across all forms of electronic devices. The proliferation of high-definition content, from streaming services to gaming, directly fuels this demand. Furthermore, the rapid growth of the Internet of Things (IoT) ecosystem is opening new avenues for display integration in a diverse range of devices, from smart home appliances to wearables. The automotive sector, in particular, is undergoing a revolution with the integration of sophisticated digital dashboards, infotainment systems, and advanced driver-assistance systems (ADAS) that rely heavily on high-quality, robust display technologies. This burgeoning automotive segment represents a significant growth opportunity for both LCD and OLED panels. The constant pursuit of thinner, lighter, and more energy-efficient devices by manufacturers also plays a crucial role in driving innovation and the adoption of advanced panel technologies.

Despite the robust growth, the LCD and OLED panel industry faces several significant challenges and restraints that could temper its expansion. One of the most persistent challenges is the intense price competition, particularly within the LCD segment, which can lead to shrinking profit margins for manufacturers. The high capital expenditure required for setting up and maintaining state-of-the-art panel manufacturing facilities also presents a substantial barrier to entry and a significant risk for existing players. Furthermore, the rapid pace of technological innovation means that older technologies can quickly become obsolete, necessitating continuous and substantial investment in research and development to remain competitive. Supply chain disruptions, as witnessed in recent years due to geopolitical events and global pandemics, can impact the availability of raw materials and components, leading to production delays and increased costs. For OLED technology, while its performance is superior, the manufacturing complexity and associated higher costs still present a barrier to widespread adoption in price-sensitive markets. Concerns regarding the lifespan and potential for burn-in, especially in certain OLED applications, also remain a point of consideration for some consumers and manufacturers.

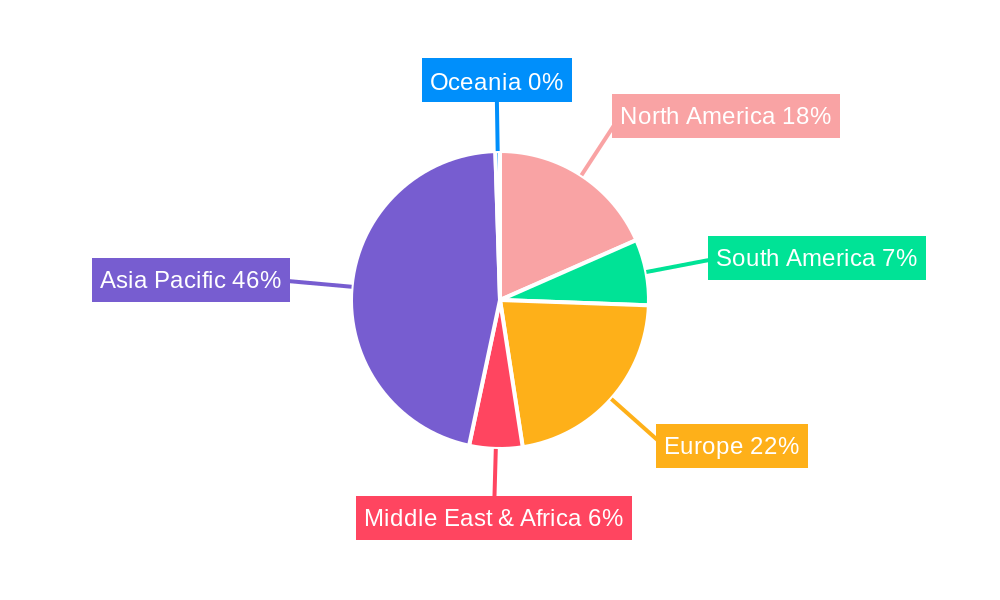

The global LCD and OLED panel market's dominance is multifaceted, with specific regions and application segments exhibiting pronounced leadership. Asia Pacific, particularly China, stands out as the epicenter of panel manufacturing, housing a majority of the world's leading panel producers and a significant portion of the manufacturing capacity. This region's dominance is driven by substantial government support, a vast domestic market, and a highly developed supply chain infrastructure for display technologies. Countries like South Korea, Taiwan, and Japan also play crucial roles, particularly in the research and development of advanced display technologies and the production of high-value components.

Within this broad regional context, the Consumer Electronics segment remains the most dominant application for both LCD and OLED panels. This encompasses a vast array of products, including smartphones, televisions, laptops, tablets, and gaming consoles. The sheer volume of units produced and consumed within this segment makes it the primary revenue driver. However, the Transportation Equipment segment is emerging as a significant growth frontier, driven by the automotive industry's increasing reliance on sophisticated in-car displays. As vehicles become more connected and autonomous, the demand for advanced digital cockpits, heads-up displays, and infotainment systems is soaring. Both LCD and OLED technologies are finding extensive application here, with OLED offering premium visual experiences and LCD providing cost-effective solutions for various display needs.

The Commercial Screens segment, including digital signage, interactive displays, and large-format advertising boards, is another area of substantial market penetration. The increasing adoption of digital communication and advertising strategies across various industries fuels the demand for these displays.

The interplay between these dominant regions and segments, characterized by massive production volumes in Asia and burgeoning application demands in consumer electronics and automotive, defines the current and future landscape of the LCD and OLED panel market.

The LCD and OLED panel industry's growth is significantly propelled by innovation in display technologies, leading to enhanced visual experiences and new application possibilities. The relentless pursuit of higher resolutions, improved color reproduction, and increased brightness by manufacturers directly fuels consumer upgrades. Furthermore, the expanding adoption of flexible and foldable display technologies is opening up novel product categories, particularly in smartphones and wearables, creating new market opportunities. The increasing integration of displays in the automotive sector, for advanced infotainment systems and digital cockpits, is a major growth catalyst. The burgeoning Internet of Things (IoT) ecosystem also necessitates integrated displays across a wider range of devices, from smart home appliances to industrial equipment.

This comprehensive report delves into the intricate dynamics of the LCD and OLED panel market, providing an in-depth analysis of market size, segmentation, and growth projections. It meticulously examines the technological evolution of both LCD and OLED technologies, highlighting key innovations and their impact on performance and cost. The report offers a granular breakdown of the market by type (LCD Panel, OLED Panel), application (Consumer Electronics, Commercial Screens, Transportation Equipment, Industrial Instruments, Medical Equipment), and region. With a study period spanning from 2019 to 2033, a base year of 2025, and a detailed forecast period (2025-2033), it provides invaluable insights into future market trends and opportunities. The report also identifies key market drivers, challenges, and the competitive landscape, featuring leading players and their strategic initiatives. This detailed coverage ensures stakeholders have a complete understanding of the forces shaping this rapidly evolving industry.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Samsung, BOE, LG, Tianma Microelectronics, Visionox, Shenzhen China Star Optoelectronics Technology, HKC, Innolux.

The market segments include Type, Application.

The market size is estimated to be USD 151850 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "LCD and OLED Panel," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the LCD and OLED Panel, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.