1. What is the projected Compound Annual Growth Rate (CAGR) of the Datacom Silicon Photonics Chip?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Datacom Silicon Photonics Chip

Datacom Silicon Photonics ChipDatacom Silicon Photonics Chip by Type (100G, 400G, 800G, Others, World Datacom Silicon Photonics Chip Production ), by Application (Data Center, High Performance Computing, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

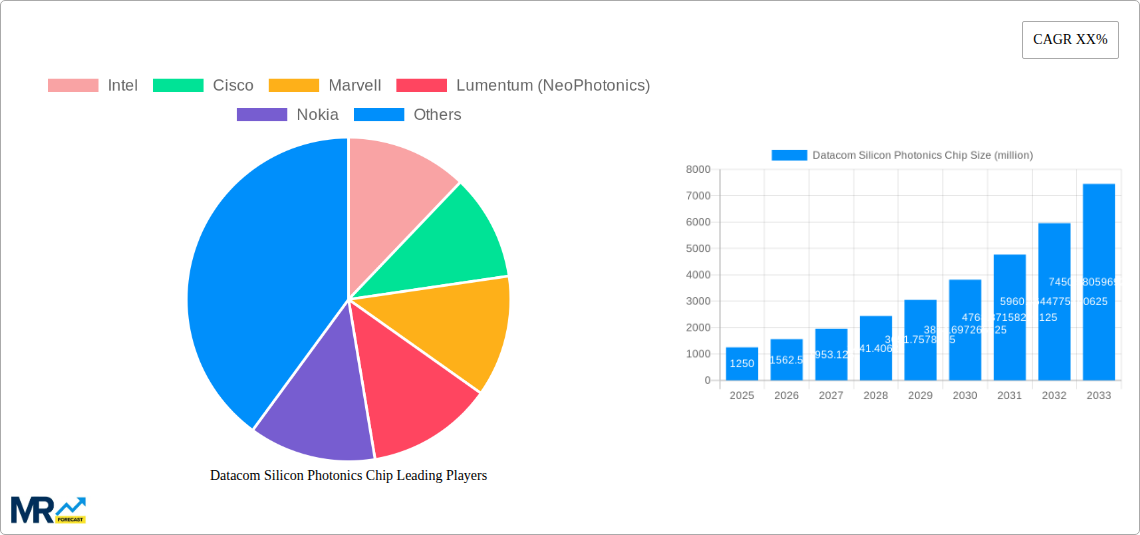

The global market for Datacom Silicon Photonics Chips is experiencing robust expansion, projected to reach a substantial market size of USD 1250 million. This growth is fueled by the relentless demand for higher bandwidth and faster data transmission speeds across data centers, high-performance computing (HPC) environments, and other burgeoning digital infrastructure. Key drivers include the increasing adoption of 100G, 400G, and the emerging 800G technologies, all of which rely heavily on the performance and efficiency offered by silicon photonics. The continuous evolution of cloud computing, AI/ML workloads, and the proliferation of connected devices are creating an unprecedented surge in data traffic, necessitating advanced optical interconnect solutions that silicon photonics is uniquely positioned to provide. Furthermore, the inherent advantages of silicon photonics, such as cost-effectiveness, miniaturization, and seamless integration with existing semiconductor manufacturing processes, are accelerating its adoption over traditional solutions.

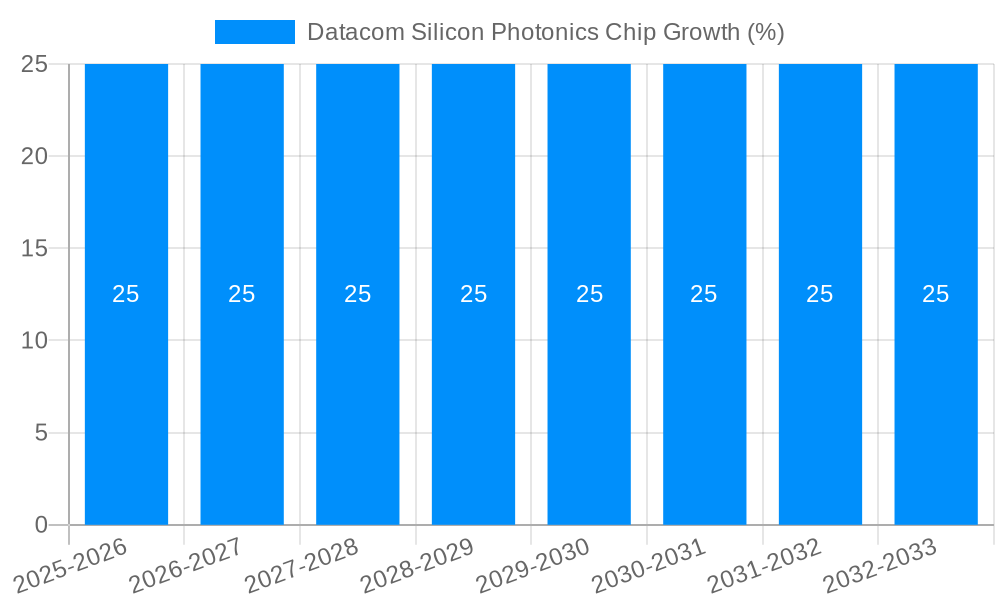

The market is characterized by significant innovation and a dynamic competitive landscape, with major players like Intel, Cisco, Marvell, Lumentum, and Nokia investing heavily in research and development. Emerging trends include the push towards co-packaged optics (CPO) and integrated photonic systems on a chip (SoCs), which promise even greater integration density and power efficiency. While the market demonstrates a promising Compound Annual Growth Rate (CAGR) of approximately 20-25% (estimated based on market size and potential growth drivers), it faces certain restraints. These include the initial high capital expenditure for R&D and manufacturing, the need for standardization in certain emerging applications, and the ongoing development of alternative high-speed interconnect technologies. Despite these challenges, the forward momentum driven by the insatiable appetite for data and the inherent scalability of silicon photonics indicates a sustained period of strong growth and significant opportunities for market participants.

Here's a unique report description for Datacom Silicon Photonics Chips, incorporating your specified elements:

The global Datacom Silicon Photonics Chip market is experiencing an unprecedented surge, projected to eclipse $150 million in production by the base year 2025, and further escalate to $800 million by the conclusion of the forecast period in 2033. This remarkable expansion is underpinned by the relentless demand for higher bandwidth and lower latency solutions within critical computing infrastructures. The study period, spanning from 2019 to 2033, encompasses a historical trajectory of rapid innovation and adoption, with the base year of 2025 serving as a pivotal point for current market valuation and future projections. The historical period (2019-2024) laid the groundwork for this explosive growth, witnessing significant advancements in integration density and performance metrics of silicon photonics components. As we move through the forecast period, the market will be characterized by the increasing dominance of higher-speed interfaces, particularly 800G and beyond, as data centers and high-performance computing environments grapple with ever-increasing data traffic volumes. The "Others" category within Types is also expected to witness substantial growth, indicative of emerging applications and specialized solutions within the datacom ecosystem. The primary application segment, Data Centers, will continue to be the dominant force, consuming the lion's share of silicon photonics chip production, driven by hyperscale cloud providers and enterprise digital transformation initiatives. However, High Performance Computing (HPC) is emerging as a significant secondary driver, with its insatiable appetite for rapid data transfer and low-latency communication. This dynamic interplay between evolving technological capabilities and burgeoning application demands will shape the market landscape for the foreseeable future.

The exponential growth of the datacom silicon photonics chip market is primarily propelled by the insatiable global demand for faster, more efficient, and more scalable data transmission capabilities. The relentless expansion of cloud computing, driven by the increasing adoption of Artificial Intelligence, Machine Learning, and big data analytics, necessitates unprecedented bandwidth within data centers. Traditional copper interconnects are reaching their physical limitations, making silicon photonics the clear technological successor for high-speed data communications. Furthermore, the evolution of networking infrastructure, particularly the move towards 400G, 800G, and even future terabit interfaces, is a direct catalyst. These next-generation speeds are simply not achievable or cost-effective with existing electronic solutions, making the integration of photonic components onto silicon platforms a strategic imperative. The inherent advantages of silicon photonics, including its ability to integrate complex optical functions onto a single chip, its CMOS compatibility for mass production, and its lower power consumption compared to discrete optical components, are powerful drivers for adoption. The significant investments made by key industry players in research and development, coupled with strategic partnerships aimed at accelerating product development and market penetration, are also crucial in fueling this upward trajectory.

Despite the robust growth, the datacom silicon photonics chip market faces several significant challenges and restraints that could temper its trajectory. One of the primary hurdles remains the high cost of manufacturing and wafer processing. While silicon photonics benefits from CMOS-compatible manufacturing processes, the specialized equipment and intricate fabrication steps still contribute to a higher unit cost compared to established electronic components, particularly for lower-speed applications. This cost differential can be a significant barrier for widespread adoption in price-sensitive segments of the market. Another critical challenge lies in yield and reliability, especially for highly complex integrated photonic circuits. Achieving consistent high yields during wafer fabrication and ensuring long-term reliability under demanding operational conditions are paramount for widespread market acceptance. Furthermore, integration complexity and ecosystem development present ongoing challenges. Seamless integration of silicon photonics chips with existing electronic systems and the development of a mature supply chain, including specialized testing and packaging solutions, are still evolving. The need for specialized expertise in both photonics and electronics design also creates a talent gap that can hinder rapid innovation. Finally, standardization and interoperability remain crucial. While progress is being made, establishing universally accepted standards for silicon photonics interfaces and components will be essential to foster broader adoption and prevent vendor lock-in.

The Data Center segment is unequivocally positioned to dominate the datacom silicon photonics chip market in terms of production volume and revenue generation. By the base year of 2025, data centers are estimated to consume over 60% of the total silicon photonics chip production, a figure projected to grow substantially through the forecast period. This dominance stems from the ever-increasing demand for bandwidth driven by hyperscale cloud providers, enterprise IT infrastructure upgrades, and the explosive growth of data-intensive applications such as AI, ML, and big data analytics. As data traffic within these facilities continues to surge, the need for high-speed, low-latency interconnects becomes paramount. Silicon photonics chips, with their ability to support 400G and 800G interfaces and beyond, are crucial for meeting these bandwidth demands efficiently and cost-effectively.

Within the Type segments, 800G is poised for significant growth, transitioning from an emerging technology to a mainstream solution during the forecast period. While 100G and 400G will continue to be significant contributors, the rapid pace of technological evolution in data centers will propel the adoption of higher speeds to alleviate network congestion and enhance overall performance. The World Datacom Silicon Photonics Chip Production itself is a segment that will see substantial expansion, indicating the global scale of this technological shift.

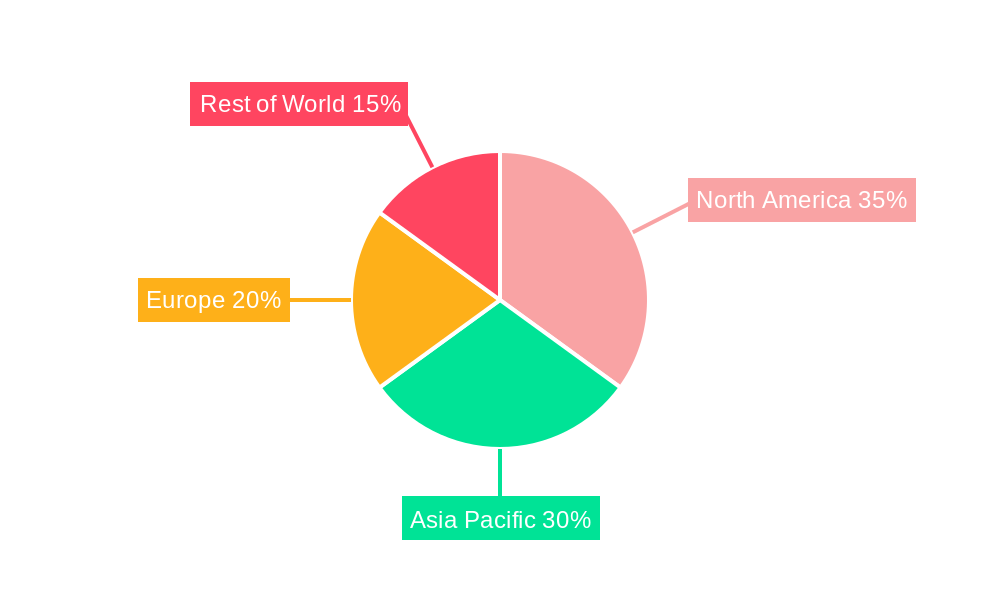

Geographically, North America, particularly the United States, is expected to lead the market. This leadership is attributed to the presence of major hyperscale cloud providers, leading semiconductor manufacturers with significant silicon photonics R&D capabilities (like Intel and Marvell), and a strong ecosystem of research institutions driving innovation. The concentration of data center infrastructure and the early adoption of advanced networking technologies in this region provide a fertile ground for silicon photonics market growth.

Other key regions and countries that will play a crucial role include:

The interplay between the dominant Data Center application and the rapidly advancing 800G Type segment, supported by strong regional hubs like North America, will define the future landscape of the datacom silicon photonics chip market.

Several key factors are acting as powerful growth catalysts for the datacom silicon photonics chip industry. The continuous evolution of Artificial Intelligence (AI) and Machine Learning (ML) workloads is generating an exponential increase in data traffic, demanding higher bandwidth and lower latency interconnects that silicon photonics can uniquely provide. The ongoing expansion of 5G networks and the proliferation of edge computing further amplify this demand by requiring efficient data aggregation and processing closer to the source. Furthermore, significant and sustained investments in R&D and infrastructure by leading technology companies are accelerating product development, improving manufacturing processes, and driving down costs, making silicon photonics more accessible and competitive. The increasing number of strategic partnerships and collaborations between chip manufacturers, equipment vendors, and end-users are also fostering a more cohesive ecosystem and accelerating market adoption.

This comprehensive report offers an in-depth analysis of the global datacom silicon photonics chip market, providing a detailed understanding of its present state and future trajectory. Spanning a study period from 2019 to 2033, with a keen focus on the base year of 2025 and a robust forecast period from 2025 to 2033, the report meticulously examines key market trends, driving forces, and the inherent challenges. It delves into the dominant application segments, particularly the critical role of Data Centers and the burgeoning significance of High Performance Computing. Furthermore, the report dissects the evolution of chip types, highlighting the anticipated dominance of 800G and the continued relevance of 100G and 400G technologies. Our analysis also sheds light on significant industry developments and identifies the leading players shaping this dynamic landscape. This report is an essential resource for stakeholders seeking to navigate and capitalize on the evolving opportunities within the rapidly expanding datacom silicon photonics chip sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Intel, Cisco, Marvell, Lumentum (NeoPhotonics), Nokia, SiFotonics, MACOM, ACCELINK, Coherent(II-VI), HTGD, BROADEX TECHNOLOGIES, HGTECH, Yuanjie Semiconductor Technology.

The market segments include Type, Application.

The market size is estimated to be USD 1250 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Datacom Silicon Photonics Chip," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Datacom Silicon Photonics Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.