1. What is the projected Compound Annual Growth Rate (CAGR) of the Conductive Silicon Carbide Wafer?

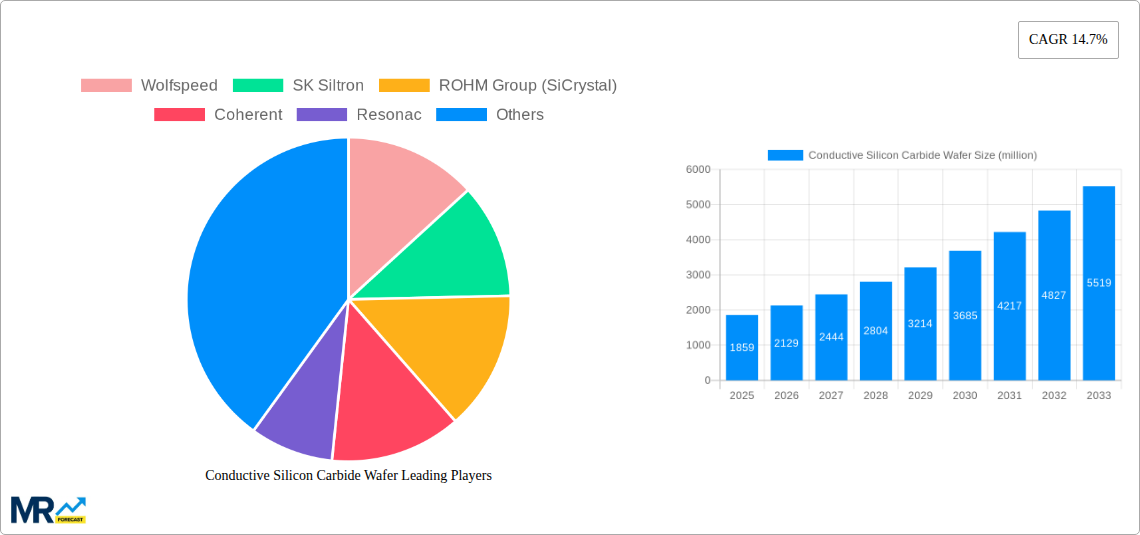

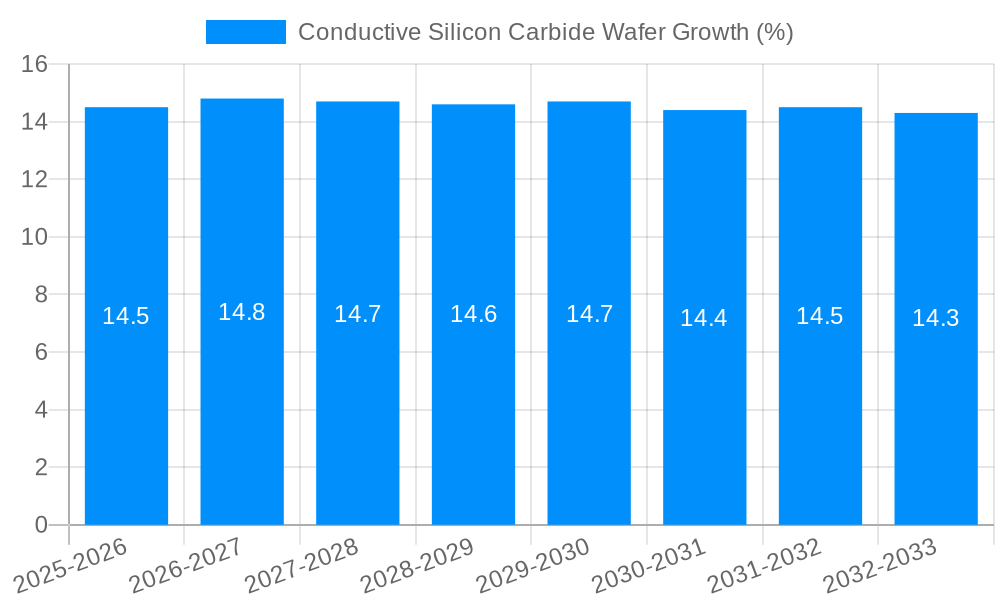

The projected CAGR is approximately 14.7%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Conductive Silicon Carbide Wafer

Conductive Silicon Carbide WaferConductive Silicon Carbide Wafer by Type (4 Inch SiC Wafer, 6 Inch SiC Wafer, 8 Inch SiC Wafer), by Application (New Energy Vehicles, Charging Piles, Photovoltaic and Wind Power, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global conductive silicon carbide (SiC) wafer market is poised for substantial expansion, projected to reach approximately \$1859 million by 2025, driven by a remarkable Compound Annual Growth Rate (CAGR) of 14.7%. This robust growth is fueled by the accelerating adoption of SiC technology across several high-impact sectors. The burgeoning electric vehicle (EV) market stands out as a primary demand driver, with SiC wafers enabling more efficient power conversion, leading to extended battery range and faster charging capabilities for new energy vehicles. Similarly, the expansion of renewable energy infrastructure, particularly in photovoltaic (PV) and wind power generation, is creating significant demand for SiC wafers due to their superior performance in power inverters and converters, facilitating greater energy efficiency and reliability. The development of advanced charging piles also directly benefits from the high-power handling capabilities of SiC devices.

The market is further segmented by wafer size, with 6-inch and 8-inch SiC wafers gaining prominence as manufacturers scale up production and integrate them into next-generation power electronics. While the transition to larger wafer diameters presents opportunities, the established 4-inch SiC wafer segment continues to hold relevance for specific applications. Key industry players, including Wolfspeed, SK Siltron, and ROHM Group (SiCrystal), are investing heavily in research and development and expanding manufacturing capacities to meet this escalating demand. Geographically, Asia Pacific, particularly China, is anticipated to be a dominant region due to its strong manufacturing base and rapid adoption of EVs and renewable energy. However, North America and Europe are also demonstrating significant growth potential, driven by supportive government policies and increasing investments in sustainable technologies. Despite the optimistic outlook, challenges such as high manufacturing costs and the need for further technological advancements in wafer production could pose minor restraints, but the overall trajectory remains strongly upward.

This comprehensive report delves into the dynamic Conductive Silicon Carbide (SiC) Wafer market, analyzing its trajectory from the historical period of 2019-2024 through a projected landscape up to 2033, with a base and estimated year of 2025. The market's evolution is marked by significant technological advancements and an insatiable demand from critical sectors, promising substantial growth in the coming years. We anticipate the global market size, in terms of revenue, to potentially reach several hundred million USD by 2025, with projections indicating a rapid ascent in the subsequent forecast period. The report meticulously examines the various wafer types, from the established 4-inch and 6-inch SiC wafers to the emerging and increasingly dominant 8-inch SiC wafers, understanding their market penetration and application-specific advantages. Furthermore, it dissects the application landscape, focusing on the burgeoning demand from New Energy Vehicles (NEVs), Charging Piles, Photovoltaic and Wind Power generation, alongside other niche but growing applications. The study also incorporates an in-depth analysis of industry developments and strategic initiatives undertaken by key players that are shaping the future of this high-growth segment. Our research methodology employed a combination of primary and secondary research, including expert interviews and extensive data analysis, to provide a holistic view of the market's current state and its future potential.

The Conductive Silicon Carbide wafer market is experiencing a transformative shift, driven by the unparalleled material properties of SiC and its critical role in enabling next-generation power electronics. The historical period of 2019-2024 witnessed a steady rise in demand, primarily fueled by the automotive industry's pivot towards electrification and the renewable energy sector's expansion. By the base year of 2025, we foresee the market size potentially reaching hundreds of millions of dollars, a testament to its rapid adoption. A pivotal trend is the escalating adoption of larger diameter wafers, specifically the 8-inch SiC wafer. While 4-inch and 6-inch wafers remain significant, the industry is actively migrating towards 8-inch technology due to its inherent cost efficiencies, higher throughput, and improved performance characteristics for high-power applications. This transition is not merely incremental; it represents a fundamental step in scaling up production and reducing the overall cost of SiC-based devices, making them more competitive with traditional silicon counterparts. Consequently, the market share of 8-inch wafers is expected to witness exponential growth in the forecast period (2025-2033).

Another pronounced trend is the increasing integration of SiC devices in various segments. In the New Energy Vehicle (NEV) sector, SiC power modules are becoming standard for inverters, on-board chargers, and DC-DC converters, significantly improving energy efficiency and extending driving range. Similarly, Charging Piles are increasingly incorporating SiC technology to enable faster and more efficient charging. The Photovoltaic and Wind Power industries are also leveraging SiC for their inverters, boosting power conversion efficiency and reducing system size and weight. The "Others" category, encompassing industrial applications, consumer electronics, and aerospace, is also showing robust growth as designers recognize the advantages of SiC in demanding environments. The market is also observing a trend towards greater vertical integration among key players, with some companies investing in both wafer manufacturing and device fabrication to ensure supply chain stability and optimize performance. Furthermore, advancements in wafer epitaxy and processing techniques are leading to higher quality wafers with reduced defect densities, which is crucial for achieving higher device yields and reliability. The overall market sentiment is optimistic, with continuous innovation and expanding application horizons setting a strong foundation for sustained expansion throughout the study period.

The conductive silicon carbide wafer market is being propelled by a confluence of powerful factors, chief among them being the burgeoning demand for electrification across multiple critical sectors. The most significant driver remains the New Energy Vehicle (NEV) revolution. As governments worldwide set ambitious targets for reducing carbon emissions and consumers embrace electric mobility, the demand for highly efficient and compact power electronics is skyrocketing. SiC's superior performance characteristics, including higher voltage handling, faster switching speeds, and lower conduction losses compared to traditional silicon, make it the material of choice for NEV powertrains, charging systems, and battery management. This translates directly into a massive and sustained demand for SiC wafers.

Secondly, the global push towards renewable energy is another monumental driver. The expansion of solar farms and wind turbine installations necessitates highly efficient power inverters to convert generated electricity into usable grid power. SiC-based inverters offer substantial improvements in energy conversion efficiency, reducing energy loss and thereby increasing the overall output of renewable energy systems. This translates to a direct and growing need for conductive SiC wafers to manufacture these critical components. The "Charging Piles" segment is intrinsically linked to the NEV market, experiencing a parallel surge in demand as charging infrastructure development races to keep pace with the growing electric vehicle fleet. Furthermore, advancements in manufacturing technologies and the scaling up of production capacities by leading players are contributing to a reduction in SiC wafer costs, making them more accessible and economically viable for a wider range of applications. The intrinsic material advantages of SiC – its high thermal conductivity, robustness against high temperatures and voltages, and excellent chemical resistance – are increasingly being recognized and leveraged by industries operating in demanding environments, further broadening its market appeal.

Despite the incredibly promising growth trajectory of the conductive silicon carbide wafer market, several challenges and restraints warrant careful consideration. The primary impediment remains the high manufacturing cost of SiC wafers compared to traditional silicon wafers. The complex crystallization process, the difficulty in growing large diameter defect-free crystals, and the stringent quality control required contribute to significantly higher production expenses. This cost differential can be a barrier to entry for cost-sensitive applications and can slow down the widespread adoption of SiC technology, especially in segments where price sensitivity is high.

Another significant challenge is the complexity and maturity of the manufacturing process. Producing high-quality, large-diameter (8-inch) SiC wafers with minimal defects is technically demanding and requires specialized equipment and expertise. Yields can be lower than with silicon, further impacting costs and supply. This technical complexity also leads to a limited number of established manufacturers capable of producing high-quality wafers at scale, creating potential supply chain vulnerabilities and bottlenecks. The industry is still in a phase of scaling up, and ensuring a consistent and reliable supply of wafers that meet the stringent quality standards for high-performance power electronics is an ongoing challenge. Furthermore, while SiC offers superior performance, the design and integration of SiC devices can require specialized knowledge and tooling, potentially increasing the development cycle and initial investment for device manufacturers. Lastly, the recycling and disposal of SiC materials present an emerging environmental challenge that the industry will need to address as production volumes increase. While not an immediate restraint, it is a factor that could influence long-term sustainability and regulatory considerations.

The conductive silicon carbide wafer market is poised for significant growth across several key regions and segments, with certain areas and applications showing exceptional dominance.

Dominant Segments:

Type: 8 Inch SiC Wafer: This segment is set to be a major growth engine and likely to dominate the market in the coming years. While 4-inch and 6-inch SiC wafers have been the workhorses for a considerable period, the industry's strategic focus has decisively shifted towards 8-inch technology.

Application: New Energy Vehicles (NEVs): The electrification of the automotive sector is arguably the single most significant application driving the demand for conductive SiC wafers.

Dominant Regions:

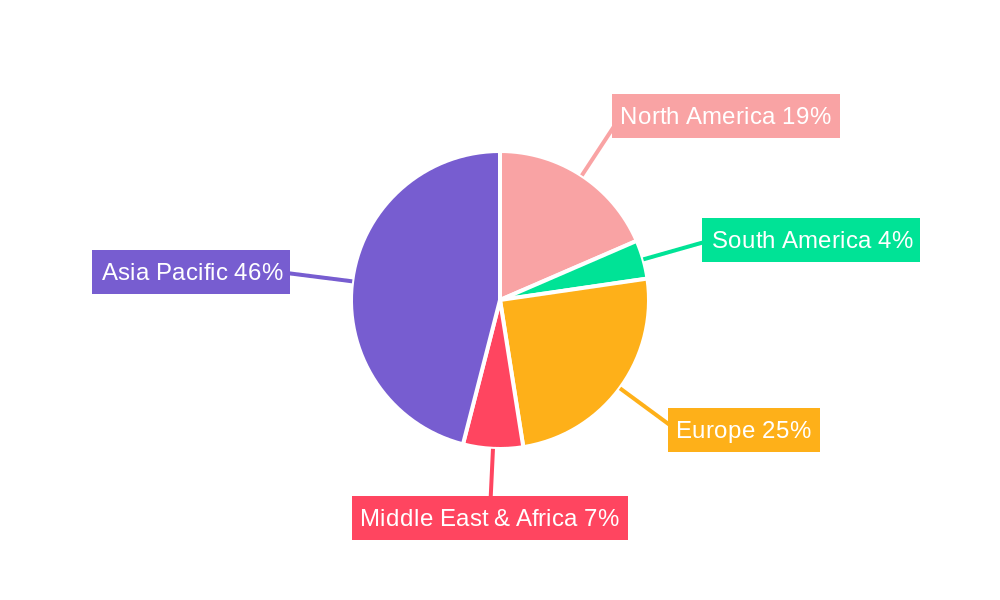

Asia-Pacific: This region is emerging as the undisputed leader in the conductive silicon carbide wafer market, driven by a combination of strong manufacturing capabilities, substantial government support for emerging technologies, and a burgeoning end-user market.

North America: Driven by the strong presence of automotive giants investing heavily in electric vehicle technology and the significant growth in renewable energy infrastructure, North America is a crucial market.

Europe: Europe is a significant market for conductive silicon carbide wafers, largely due to its aggressive push towards automotive electrification and ambitious renewable energy targets.

The synergy between advanced manufacturing capabilities, supportive government policies, and the relentless demand from high-growth application sectors like NEVs and renewable energy will continue to shape the dominance of these regions and segments in the conductive silicon carbide wafer market. The transition to 8-inch wafers will be a key enabler, democratizing access to SiC technology and further solidifying the market's expansion.

The conductive silicon carbide wafer industry is experiencing robust growth fueled by several key catalysts. The undeniable acceleration of electrification across various sectors, most notably New Energy Vehicles (NEVs) and renewable energy infrastructure like solar and wind power, creates a fundamental and ever-increasing demand for SiC's superior power handling capabilities. Furthermore, continuous technological advancements in wafer manufacturing, particularly the successful scaling of 8-inch SiC wafer production, are crucial. This scaling reduces costs and improves yields, making SiC more economically viable for a broader range of applications. Supportive government policies worldwide, including incentives for electric mobility and clean energy, also play a significant role in driving adoption and investment within the industry.

This report provides an exhaustive analysis of the conductive silicon carbide wafer market, meticulously examining its present landscape and future trajectory from 2019 to 2033. It offers deep insights into the market dynamics, covering key aspects such as market size, segmentation by wafer type (4-inch, 6-inch, 8-inch) and application (NEVs, Charging Piles, Photovoltaic & Wind Power, Others). The study delves into the critical driving forces propelling this market forward, including the relentless demand for electrification and renewable energy solutions. It also critically evaluates the challenges and restraints that could impact market growth, such as manufacturing costs and process complexities. Furthermore, the report identifies the dominant regions and segments poised for significant expansion, while also highlighting the key players and their strategic contributions. By offering a comprehensive understanding of the industry's evolution, technological advancements, and future outlook, this report serves as an indispensable resource for stakeholders seeking to navigate and capitalize on the opportunities within the rapidly evolving conductive silicon carbide wafer sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 14.7% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 14.7%.

Key companies in the market include Wolfspeed, SK Siltron, ROHM Group (SiCrystal), Coherent, Resonac, STMicroelectronics, TankeBlue, SICC, Hebei Synlight Crystal, CETC, San'an Optoelectronics.

The market segments include Type, Application.

The market size is estimated to be USD 1859 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Conductive Silicon Carbide Wafer," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Conductive Silicon Carbide Wafer, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.