1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Solid-state LiDAR Silicon Photonic Chip?

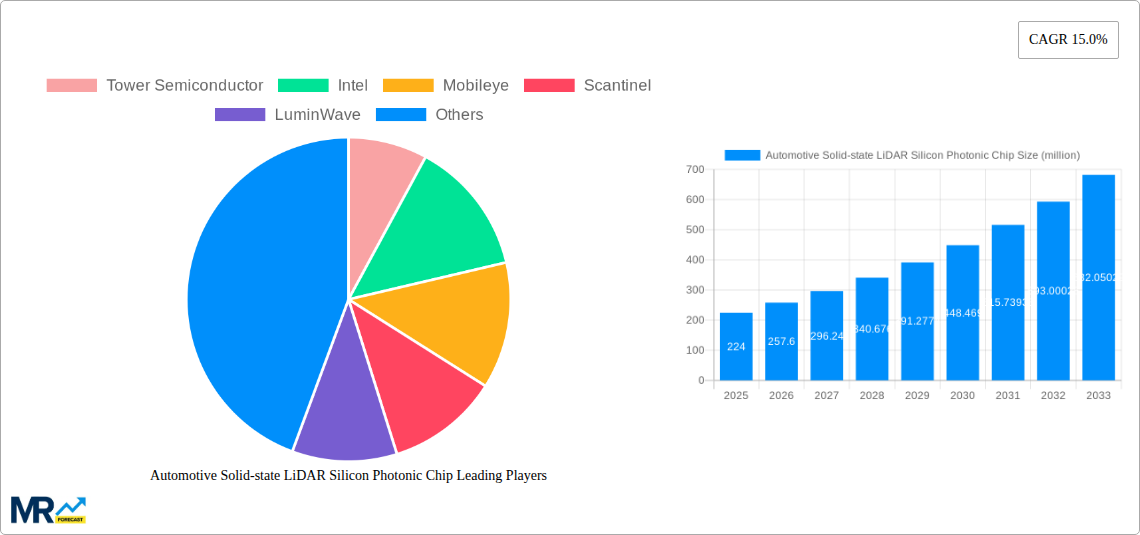

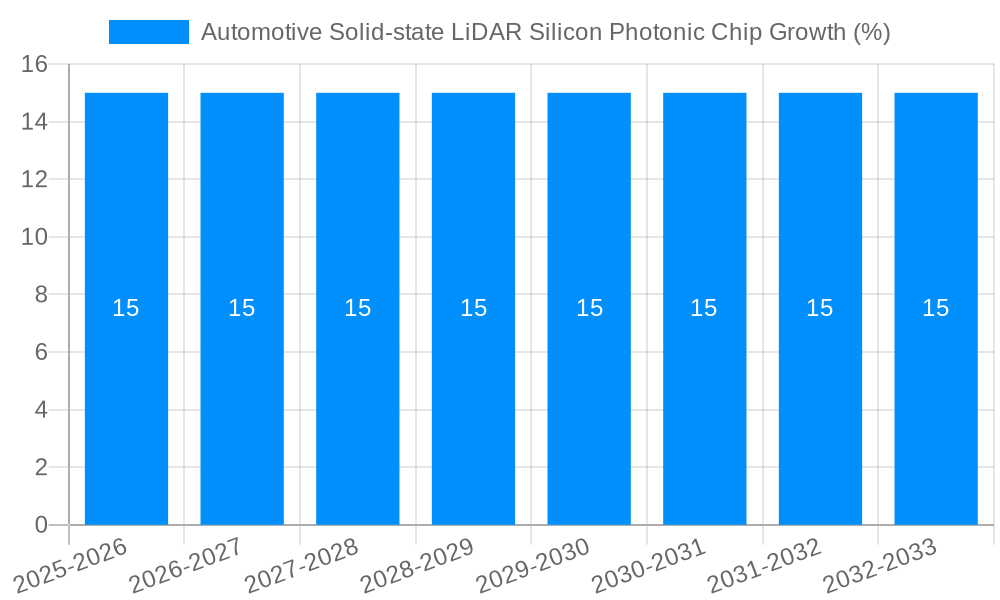

The projected CAGR is approximately 15.0%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Automotive Solid-state LiDAR Silicon Photonic Chip

Automotive Solid-state LiDAR Silicon Photonic ChipAutomotive Solid-state LiDAR Silicon Photonic Chip by Application (Sedan, SUV), by Type (FMCW LiDAR Chip, OPA LiDAR Chip, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The Automotive Solid-state LiDAR Silicon Photonic Chip market is experiencing robust expansion, projected to reach a significant valuation by 2033. The current market size in 2025 stands at an estimated \$224 million, driven by the escalating adoption of advanced driver-assistance systems (ADAS) and the relentless pursuit of autonomous driving technologies. The market's growth trajectory is further bolstered by a compelling Compound Annual Growth Rate (CAGR) of 15.0%, indicating substantial future potential. Key drivers include the increasing demand for enhanced safety features in vehicles, such as object detection and collision avoidance, alongside the development of sophisticated sensing capabilities essential for Level 3 and above autonomous driving. The miniaturization and cost-effectiveness offered by silicon photonic chips are making LiDAR technology more accessible and practical for mass-market vehicle integration.

The market is segmented by application into Sedan and SUV categories, with LiDAR chips for both these vehicle types seeing significant investment. In terms of technology, FMCW (Frequency Modulated Continuous Wave) LiDAR Chip and OPA (Optical Phased Array) LiDAR Chip segments are at the forefront of innovation, promising higher performance and novel functionalities. Emerging trends include the integration of AI and machine learning with LiDAR data for more intelligent perception, as well as advancements in chip design for improved range, resolution, and immunity to interference. While the market is poised for remarkable growth, potential restraints such as high initial R&D costs and the need for standardization across the automotive industry present challenges that stakeholders are actively addressing. The competitive landscape is dynamic, with key players like Tower Semiconductor, Intel, and Mobileye spearheading innovation and market development.

Here is a unique report description on Automotive Solid-state LiDAR Silicon Photonic Chip, incorporating your specified elements:

The automotive solid-state LiDAR silicon photonic chip market is on a trajectory of explosive growth, poised to revolutionize vehicle perception systems. With the global market projected to reach an estimated 125 million units in 2025, its impact is undeniable. This surge is driven by the escalating demand for advanced driver-assistance systems (ADAS) and the imperative for autonomous driving capabilities across the automotive spectrum. Silicon photonics, with its inherent advantages of miniaturization, cost-effectiveness through mass production on existing semiconductor fabs, and superior performance, is emerging as the dominant technology for LiDAR integration. The historical period from 2019 to 2024 witnessed foundational advancements and early adoption, laying the groundwork for the substantial market expansion anticipated from 2025 through 2033. Key market insights reveal a significant shift towards FMCW LiDAR chips, which offer unparalleled advantages in velocity measurement and interference rejection, crucial for complex driving environments. Furthermore, the report highlights the increasing sophistication of OPA (Optical Phased Array) LiDAR chips, promising even greater scanning flexibility and performance enhancements. The integration of these advanced photonic chips into a wide array of vehicle segments, from mass-market Sedans to premium SUVs, signifies a broadening application base. As the technology matures and economies of scale are realized, the cost per unit is expected to decline, making solid-state LiDAR silicon photonic chips an indispensable component for future vehicle safety and autonomy. The estimated market size for 2025, at 125 million units, is a testament to the rapid adoption and technological maturation occurring within this dynamic sector.

The relentless pursuit of enhanced vehicle safety and the burgeoning transition towards autonomous driving are the primary architects of the automotive solid-state LiDAR silicon photonic chip market's impressive growth. As regulatory bodies worldwide mandate stricter safety standards and automakers strive to differentiate their offerings with cutting-edge ADAS features, the demand for reliable and high-performance perception sensors like LiDAR intensifies. Silicon photonics offers a compelling solution, leveraging established semiconductor manufacturing processes to enable the mass production of compact, power-efficient, and cost-effective LiDAR chips. This intrinsic scalability is a critical enabler for widespread adoption across all vehicle tiers. The ability of silicon photonic LiDAR to accurately perceive the environment in varying lighting and weather conditions, coupled with its potential for deep integration into vehicle architectures, makes it an attractive proposition for automotive manufacturers. The forecast period from 2025 to 2033 will likely see a substantial increase in the integration of these chips, moving beyond niche luxury applications to become a standard feature in mainstream vehicles, driven by both consumer demand for safety and the strategic imperatives of automotive OEMs.

Despite the promising outlook, the automotive solid-state LiDAR silicon photonic chip market faces several hurdles that could temper its growth trajectory. One significant challenge revolves around cost reduction, particularly for high-performance solutions, to achieve mass-market affordability. While silicon photonics promises economies of scale, the initial investment in specialized manufacturing and packaging can still be substantial. Furthermore, the reliability and durability of these chips in the harsh automotive environment, exposed to extreme temperatures, vibrations, and moisture, remain critical areas of focus. Ensuring long-term performance and meeting automotive-grade standards requires rigorous testing and validation. The standardization of LiDAR interfaces and data protocols is another area that needs further development to facilitate seamless integration and interoperability between different sensor manufacturers and vehicle platforms. Finally, public perception and acceptance of LiDAR technology, particularly concerning potential privacy concerns and visual impact, could also present a restraint, necessitating clear communication and education campaigns from the industry.

The automotive solid-state LiDAR silicon photonic chip market is poised for significant dominance in certain regions and segments, driven by a confluence of factors including technological innovation, automotive manufacturing prowess, and regulatory landscapes.

Dominating Segments:

FMCW LiDAR Chip: This segment is anticipated to experience the most substantial growth and dominance.

Sedan Application: While SUVs are significant, the sheer volume of sedan production worldwide positions it as a dominant application segment for silicon photonic LiDAR.

Key Dominating Region/Country:

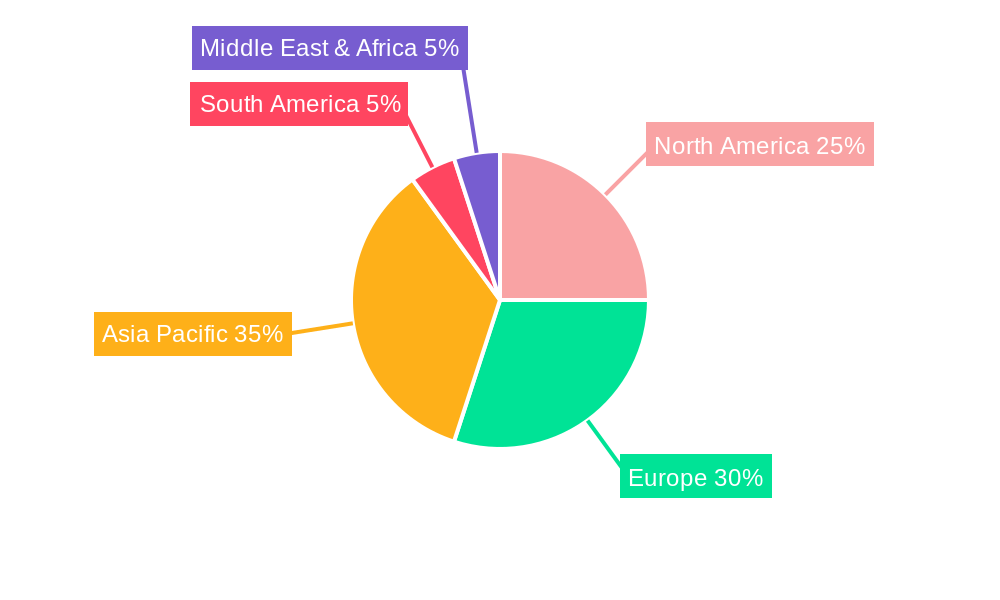

North America: This region is expected to lead in the adoption and market penetration of automotive solid-state LiDAR silicon photonic chips.

China: China's vast automotive market and its strategic focus on developing advanced automotive technologies, including intelligent connected vehicles (ICVs), position it as another dominant force.

Several factors are acting as potent growth catalysts for the automotive solid-state LiDAR silicon photonic chip industry. The escalating demand for enhanced vehicle safety features, driven by regulatory pressures and consumer preferences, is a primary driver. Furthermore, the accelerating pace of autonomous driving development across various levels of autonomy necessitates robust and reliable perception systems, with LiDAR being a cornerstone technology. The significant advancements in silicon photonics technology, enabling miniaturization, cost reduction through leveraging existing semiconductor infrastructure, and improved performance, are also critical enablers. The increasing number of strategic collaborations between LiDAR developers, chip manufacturers, and automotive OEMs is fostering innovation and accelerating market penetration, ensuring a sustained upward trajectory in adoption.

This comprehensive report delves deep into the intricacies of the automotive solid-state LiDAR silicon photonic chip market, offering an unparalleled analytical perspective. It provides detailed market sizing and forecasting from 2019 to 2033, with a specific focus on the base year of 2025 and the forecast period of 2025-2033, including an estimate of 125 million units for 2025. The analysis dissects key trends, including the ascendance of FMCW and OPA LiDAR chip types and their integration into various vehicle applications like Sedans and SUVs. The report meticulously examines the driving forces, challenges, and restraints shaping the market, alongside in-depth regional and segment-specific dominance analysis. Furthermore, it identifies critical growth catalysts, profiles leading industry players, and highlights significant historical and ongoing developments. The report’s detailed methodology and extensive data analysis ensure a robust understanding of the current landscape and future potential of this transformative technology.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 15.0% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 15.0%.

Key companies in the market include Tower Semiconductor, Intel, Mobileye, Scantinel, LuminWave, Guo Ke Guang Xin (Haining) Technology, Yangzhou Qunfa, Shanghai Xihe.

The market segments include Application, Type.

The market size is estimated to be USD 224 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Solid-state LiDAR Silicon Photonic Chip," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Solid-state LiDAR Silicon Photonic Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.