1. What is the projected Compound Annual Growth Rate (CAGR) of the Fluoropolymer-lined ISO Semiconductor Chemical Storage Tank?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Fluoropolymer-lined ISO Semiconductor Chemical Storage Tank

Fluoropolymer-lined ISO Semiconductor Chemical Storage TankFluoropolymer-lined ISO Semiconductor Chemical Storage Tank by Type (Polytetrafluoroethylene (PTFE), Perfluoroalkoxyalkane (PFA), Fluorinated Ethylene Propylene (FEP)), by Application (Chemical Industry, Pharmaceutical, Food Processing, Papermaking, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

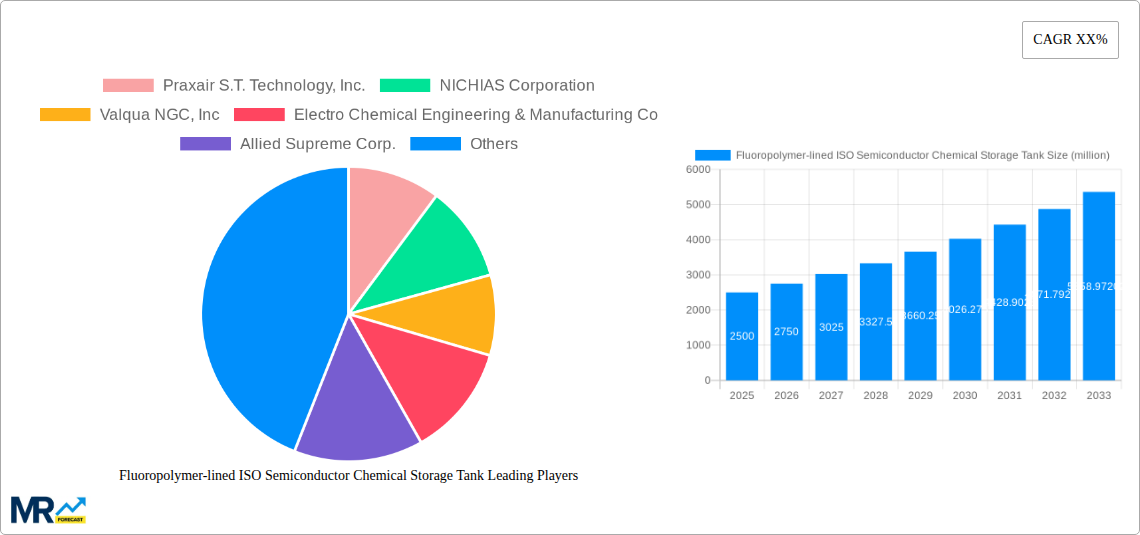

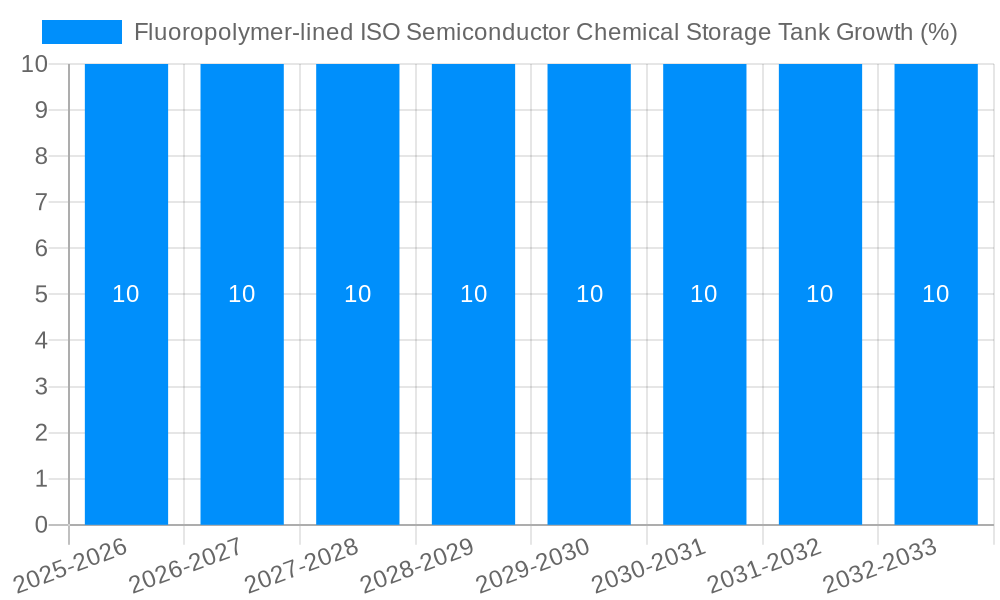

The global Fluoropolymer-lined ISO Semiconductor Chemical Storage Tank market is poised for robust expansion, driven by the increasing demand for high-purity chemical handling solutions essential for the semiconductor industry's advanced manufacturing processes. This market is projected to reach a significant size of approximately $2,500 million by 2025, with a strong Compound Annual Growth Rate (CAGR) of roughly 10% expected throughout the forecast period extending to 2033. The core value proposition of these tanks lies in their exceptional chemical resistance, inertness, and ability to maintain the integrity of highly corrosive and sensitive chemicals, crucial for preventing contamination in microelectronics fabrication. Key drivers include the relentless miniaturization of semiconductor components, the development of new and more aggressive process chemicals, and the stringent regulatory requirements for environmental safety and chemical containment. The market's growth is further fueled by substantial investments in new semiconductor fabrication plants worldwide and the upgrade of existing facilities to accommodate next-generation chip production.

The market is segmented by material type, with Polytetrafluoroethylene (PTFE) emerging as a dominant segment due to its superior chemical inertness and thermal stability. Perfluoroalkoxyalkane (PFA) and Fluorinated Ethylene Propylene (FEP) also hold significant market share, offering distinct advantages in terms of cost-effectiveness and processing flexibility for various applications. In terms of application, the chemical industry, followed closely by the pharmaceutical sector, represents the largest end-users, owing to their critical need for safe and contamination-free storage of volatile and corrosive substances. The semiconductor industry's increasing reliance on these specialized tanks for the storage of etchants, solvents, and other high-purity chemicals is a primary growth catalyst. Emerging economies in the Asia Pacific region, particularly China and South Korea, are anticipated to witness the fastest growth due to the rapid expansion of their semiconductor manufacturing capabilities. Restraints, such as the high initial cost of specialized fluoropolymer lining and the complexity of installation and maintenance, are being gradually overcome by advancements in manufacturing technologies and increasing awareness of the long-term cost benefits derived from enhanced product longevity and reduced risk of contamination.

The global market for Fluoropolymer-lined ISO Semiconductor Chemical Storage Tanks is experiencing robust growth, driven by the stringent purity requirements and corrosive chemical handling needs prevalent in advanced industries. The study period, from 2019 to 2033, with a base year of 2025, highlights a significant upward trajectory. In the estimated year of 2025, the market value is projected to reach USD 1,500 million, a testament to the increasing demand for these specialized containment solutions. The forecast period (2025-2033) anticipates a Compound Annual Growth Rate (CAGR) of approximately 7.5%, further solidifying its importance. This growth is fundamentally linked to the semiconductor industry's continuous expansion, its reliance on ultra-pure chemicals, and the parallel rise of advanced chemical manufacturing processes across various sectors. The historical period (2019-2024) has already laid a strong foundation, characterized by increasing awareness and adoption of these high-performance tanks.

The market is segmented by material type, with Polytetrafluoroethylene (PTFE) emerging as the dominant material due to its exceptional chemical inertness and thermal stability, valued at an estimated USD 700 million in 2025. Perfluoroalkoxyalkane (PFA) and Fluorinated Ethylene Propylene (FEP) also hold significant market shares, with PFA garnering an estimated USD 500 million and FEP an estimated USD 300 million in the same year, owing to their distinct advantages in specific applications. On the application front, the Chemical Industry remains the largest segment, accounting for an estimated USD 800 million in 2025, driven by its need to safely store and transport highly reactive and corrosive substances. The Pharmaceutical sector follows closely, with an estimated market value of USD 400 million in 2025, emphasizing the critical need for contamination-free storage of sensitive compounds. The Food Processing and Papermaking industries, while smaller, also contribute to the market's diversity, with estimated values of USD 200 million and USD 100 million respectively in 2025, showcasing the broad applicability of these advanced storage solutions. The 'Others' segment, encompassing emerging applications, is also projected for steady growth.

The increasing complexity and sensitivity of chemical processes, especially within the semiconductor manufacturing realm, necessitate storage solutions that offer unparalleled purity and chemical resistance. Traditional storage materials often fail to meet these exacting standards, leading to contamination risks, equipment degradation, and potential safety hazards. Fluoropolymer linings, such as PTFE, PFA, and FEP, provide an inert barrier that effectively prevents leaching of impurities into stored chemicals and resists attack from a wide spectrum of aggressive substances. This is crucial for maintaining the integrity of high-purity chemicals essential for microchip fabrication, where even trace contaminants can render entire batches of semiconductors unusable. As the semiconductor industry continues its relentless drive towards smaller feature sizes and more complex architectures, the demand for ultra-pure materials and, consequently, for superior storage solutions will only intensify. Furthermore, the growing emphasis on environmental regulations and process safety across all chemical-intensive industries further bolsters the appeal of these advanced tanks, ensuring compliance and minimizing the risk of leaks or spills.

The burgeoning demand for fluoropolymer-lined ISO semiconductor chemical storage tanks is propelled by a confluence of critical industrial needs and technological advancements. Foremost among these is the relentless pursuit of ultra-high purity in the semiconductor manufacturing sector. The intricate processes involved in creating microchips demand chemicals of unparalleled purity, where even minute contamination can lead to catastrophic failures in wafer production. Fluoropolymer linings, renowned for their exceptional inertness and non-leaching properties, are indispensable in preserving the integrity of these sensitive chemicals throughout their storage and transport. This inherent characteristic directly translates into reduced production costs and improved yields for semiconductor manufacturers, making these tanks a vital component of their supply chain.

Furthermore, the increasing sophistication and diversification of chemical applications across various industries are creating a significant pull for these advanced storage solutions. Industries such as pharmaceuticals, advanced materials, and specialty chemicals frequently handle highly corrosive, reactive, or toxic substances. Traditional storage materials often prove inadequate against the aggressive nature of these chemicals, leading to material degradation, frequent replacements, and potential environmental hazards. Fluoropolymer-lined tanks offer a robust and long-term solution, ensuring safe containment, extended equipment lifespan, and enhanced process reliability. The growing global emphasis on stringent environmental regulations and workplace safety standards further amplifies the adoption of these tanks, as they significantly minimize the risk of leaks, spills, and chemical exposure, thereby contributing to a safer and more sustainable industrial landscape.

Despite the robust growth trajectory, the fluoropolymer-lined ISO semiconductor chemical storage tank market is not without its hurdles. One of the primary challenges is the high initial cost of production and installation. The specialized nature of fluoropolymer materials, coupled with the complex manufacturing processes required for lining ISO tanks to meet stringent industry standards, contributes to a significant upfront investment. This can be a deterrent for smaller enterprises or those operating in price-sensitive markets, limiting wider adoption, especially in sectors where the direct impact of purity is less critical than in semiconductors.

Another significant restraint is the limited availability of skilled labor and specialized manufacturing expertise. The precise application of fluoropolymer linings requires highly trained personnel and sophisticated equipment to ensure consistent quality, integrity, and adherence to performance specifications. A scarcity of such expertise can lead to production bottlenecks, increased lead times, and potential quality concerns, impacting market expansion. Furthermore, technical limitations in specific applications can pose challenges. While fluoropolymers offer broad chemical resistance, certain extreme temperature conditions or highly abrasive media might necessitate more specialized material combinations or advanced design considerations, thus limiting the universal applicability of standard fluoropolymer-lined tanks. Finally, fluctuations in raw material prices, particularly for virgin fluoropolymers, can introduce price volatility and impact the overall cost-effectiveness of these storage solutions, creating uncertainty for both manufacturers and end-users.

The market for Fluoropolymer-lined ISO Semiconductor Chemical Storage Tanks is poised for significant dominance by specific regions and segments, driven by their inherent industrial strengths and future growth potential.

Dominant Segment: Polytetrafluoroethylene (PTFE) - Estimated Value: USD 700 million in 2025

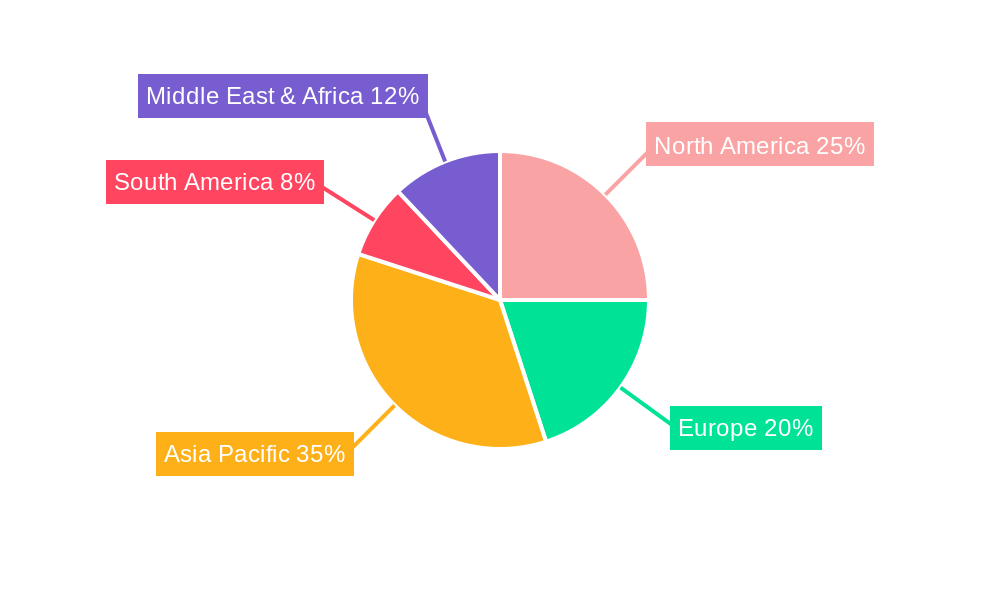

Dominant Region: Asia Pacific - Estimated Market Value Contribution in 2025: Over USD 600 million

Emerging Dominant Application: Chemical Industry (Beyond Semiconductors)

While the semiconductor application is critically important, the broader Chemical Industry is also a significant and growing force in this market.

The growth of the fluoropolymer-lined ISO semiconductor chemical storage tank industry is significantly catalyzed by the ever-increasing demand for high-purity chemicals in advanced manufacturing. The semiconductor industry's continuous push for smaller, more powerful microchips necessitates stringent contamination control, making these tanks indispensable. Furthermore, evolving environmental regulations across various sectors are mandating safer and more reliable chemical containment solutions, pushing industries to adopt superior materials and technologies. The expanding applications in the pharmaceutical sector, requiring sterile and inert storage for sensitive compounds, also contribute to market expansion. Finally, ongoing advancements in fluoropolymer technology are leading to improved performance characteristics, making these tanks more versatile and cost-effective for a wider range of demanding industrial applications, thereby fostering consistent market growth.

This comprehensive report delves deeply into the global Fluoropolymer-lined ISO Semiconductor Chemical Storage Tank market, offering an exhaustive analysis from the historical period of 2019-2024 through to an extended forecast period of 2025-2033, with 2025 serving as the base and estimated year. The report meticulously examines key market insights, projecting a significant market value of USD 1,500 million by 2025 and a robust CAGR of approximately 7.5% during the forecast period. It dissects the market by crucial segments, detailing the estimated market values for Polytetrafluoroethylene (PTFE) at USD 700 million, Perfluoroalkoxyalkane (PFA) at USD 500 million, and Fluorinated Ethylene Propylene (FEP) at USD 300 million in 2025. Application segments are also thoroughly covered, with the Chemical Industry valued at USD 800 million, Pharmaceutical at USD 400 million, Food Processing at USD 200 million, Papermaking at USD 100 million, and 'Others' at USD 100 million in the estimated year. The report further elucidates the driving forces, challenges, and restraints shaping the market landscape, identifies key dominating regions and segments, highlights significant growth catalysts, and provides an updated list of leading players. It also tracks crucial industry developments, offering a holistic understanding of the market's present state and future trajectory for stakeholders and industry participants.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Praxair S.T. Technology, Inc., NICHIAS Corporation, Valqua NGC, Inc, Electro Chemical Engineering & Manufacturing Co, Allied Supreme Corp., Sigma Roto Lining LLP, FISHER COMPANY, Edlon, Pennwalt Ltd., Jiangsu Ruineng Anticorrosion Equipment Co.,Ltd, Gartner Coatings, Inc., Plasticon Composites, SUN FLUORO SYSTEM CO.,LTD, EVERSUPP TECHNOLOGY CORP, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Fluoropolymer-lined ISO Semiconductor Chemical Storage Tank," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Fluoropolymer-lined ISO Semiconductor Chemical Storage Tank, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.