1. What is the projected Compound Annual Growth Rate (CAGR) of the EUV Light Sources?

The projected CAGR is approximately 11.4%.

EUV Light Sources

EUV Light SourcesEUV Light Sources by Type (Low Power, High Power), by Application (Equipment Factory, Fab), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

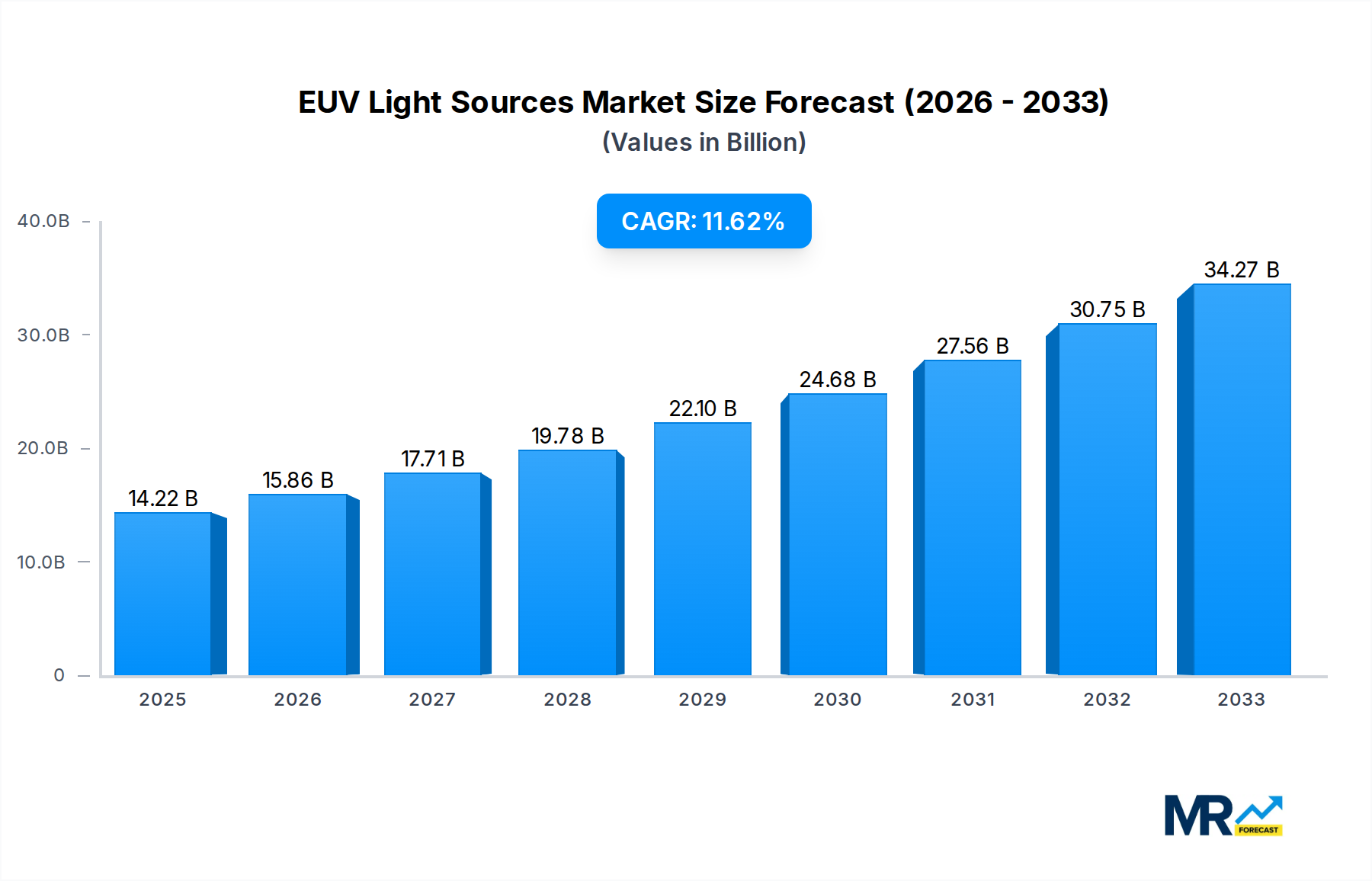

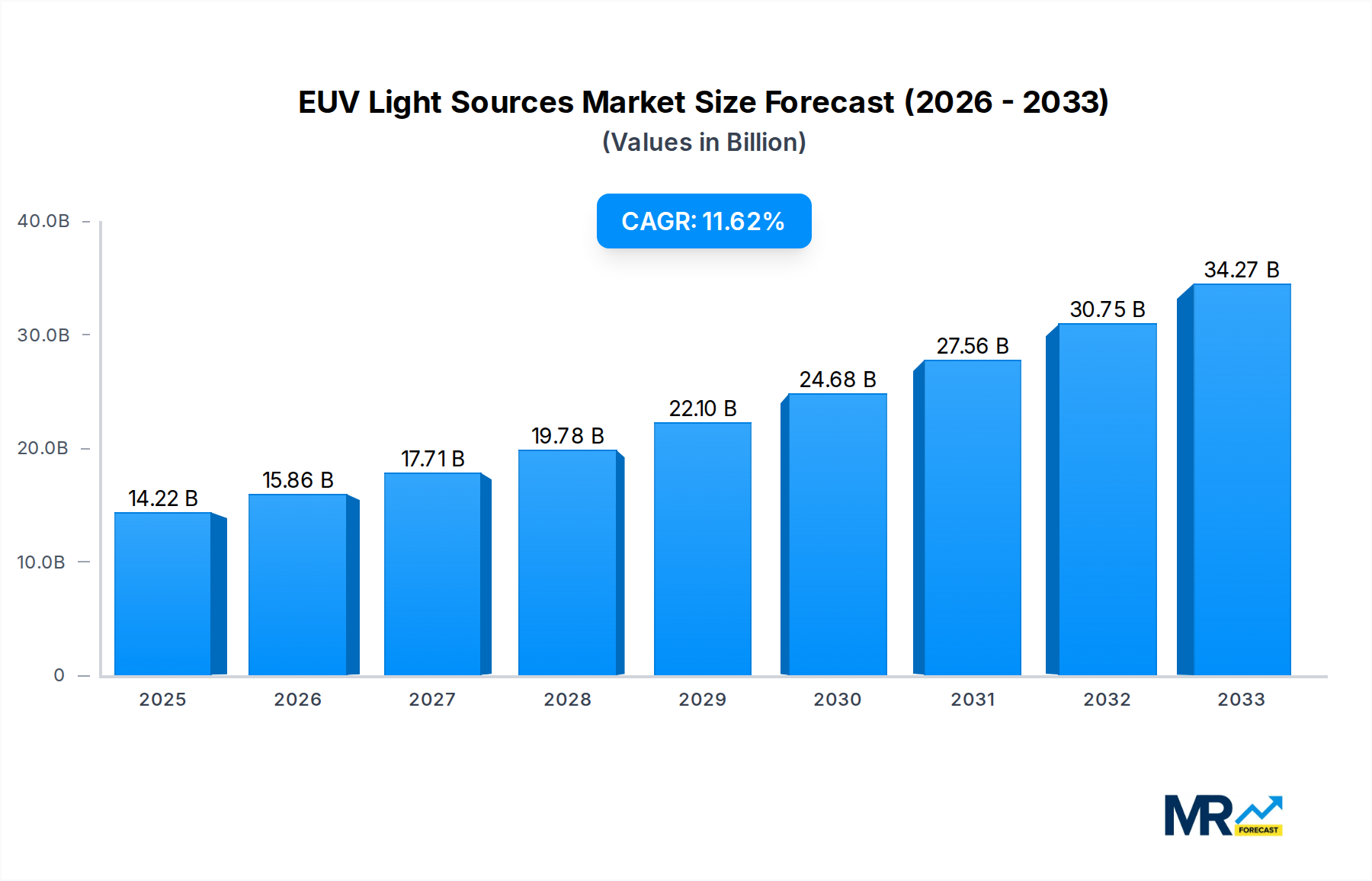

The global EUV (Extreme Ultraviolet) Light Sources market is poised for substantial expansion, projected to reach a valuation of $14.22 billion by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 11.4% throughout the forecast period of 2025-2033. This remarkable growth is primarily fueled by the escalating demand for advanced semiconductor manufacturing, particularly for high-performance computing, artificial intelligence, and next-generation mobile devices. EUV lithography is the cornerstone technology enabling the production of increasingly smaller and more powerful integrated circuits, making these light sources indispensable for semiconductor foundries. The market's trajectory is further bolstered by ongoing technological advancements and significant investments in research and development by leading players aiming to enhance the efficiency, reliability, and cost-effectiveness of EUV light sources. Key applications within equipment factories and fabrication plants are expected to drive this demand, as manufacturers strive to achieve higher yields and smaller feature sizes in their chip production.

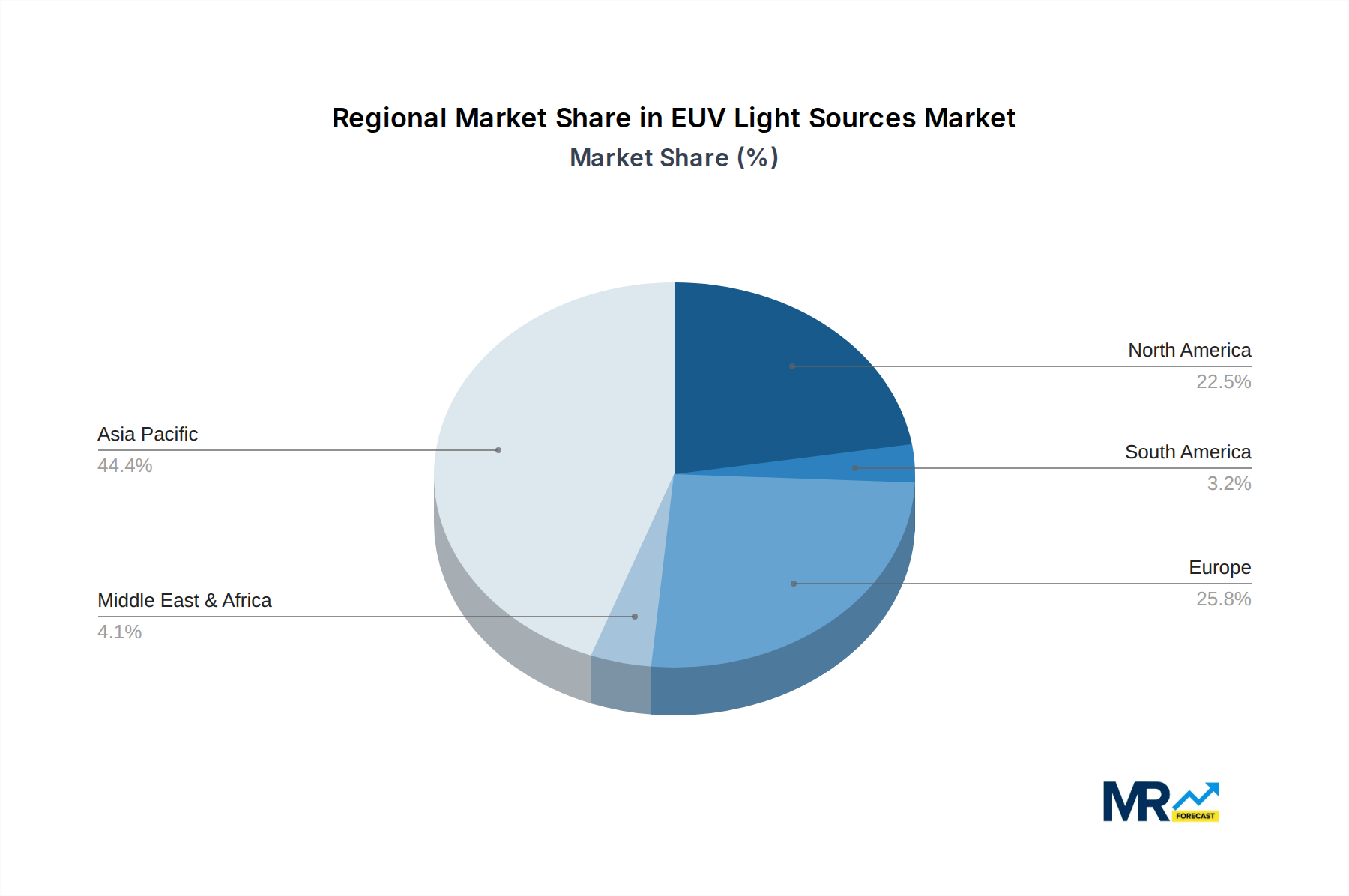

The market is segmented into Low Power and High Power EUV light sources, with High Power sources likely to dominate due to the increasing power requirements of advanced lithography nodes. Geographically, Asia Pacific, led by China, Japan, and South Korea, is anticipated to be the largest and fastest-growing region, owing to its dominant position in global semiconductor manufacturing. North America and Europe also represent significant markets, driven by the presence of major semiconductor equipment manufacturers and R&D centers. However, the market is not without its challenges. The high cost of EUV lithography systems and the complexity of the technology present substantial barriers to entry and widespread adoption. Furthermore, stringent environmental regulations and the need for specialized infrastructure add to the operational complexities. Despite these restraints, the relentless pursuit of miniaturization and performance enhancement in the semiconductor industry ensures a bright future for the EUV Light Sources market.

This report provides an in-depth analysis of the global EUV (Extreme Ultraviolet) light sources market, a critical technology underpinning the next generation of semiconductor manufacturing. The study, spanning from 2019 to 2033, with a Base Year of 2025 and a detailed Forecast Period of 2025-2033, offers invaluable insights for stakeholders navigating this rapidly evolving landscape. Examining the Historical Period of 2019-2024, we’ve pinpointed key market dynamics and technological advancements. Our analysis meticulously dissects market segmentation, competitive landscapes, and future growth trajectories, offering a strategic roadmap for businesses.

The EUV light sources market is on an exponential growth trajectory, projected to exceed several hundred billion dollars by the end of the Forecast Period (2025-2033). This surge is primarily driven by the relentless demand for more powerful and energy-efficient semiconductors, which are essential for advancements in artificial intelligence, 5G, the Internet of Things (IoT), and high-performance computing. The adoption of EUV lithography by leading foundries has transitioned from a niche, bleeding-edge technology to a mainstream manufacturing necessity for advanced nodes, particularly at the sub-7nm and sub-5nm technology nodes. The Estimated Year of 2025 sees the market firmly entrenched, with significant investments flowing into R&D and production capacity expansion. The report highlights a discernible trend towards higher power EUV sources, enabling faster throughput and lower cost-per-wafer, a crucial factor in driving widespread adoption. Furthermore, the development of more compact and cost-effective EUV source technologies is anticipated to broaden its application spectrum beyond leading-edge logic chips to include advanced memory devices and even potentially for specialized applications outside of traditional semiconductor manufacturing. The competitive landscape is characterized by intense innovation, with companies vying to offer superior source performance, reliability, and total cost of ownership. The market is also witnessing increased collaboration between light source manufacturers and scanner vendors, ensuring seamless integration and optimized performance for the entire lithography ecosystem.

The escalating demand for enhanced computational power and energy efficiency across a multitude of consumer electronics, enterprise solutions, and emerging technologies is the primary engine propelling the EUV light sources market. As the semiconductor industry pushes the boundaries of Moore's Law, enabling smaller, faster, and more power-efficient transistors becomes paramount. EUV lithography, with its shorter wavelengths, is the only viable technology capable of patterning these intricate features at advanced process nodes. The proliferation of AI, requiring massive processing capabilities, and the rollout of 5G networks, necessitating low-latency and high-bandwidth communication, are directly fueling the need for next-generation semiconductors manufactured using EUV. Furthermore, the increasing complexity of semiconductor designs and the miniaturization of components make traditional lithography techniques insufficient. This technological imperative, coupled with the economic benefits of higher yields and reduced manufacturing steps offered by EUV, creates a compelling case for its widespread adoption. The continuous innovation in EUV source technology, leading to improved power output and reliability, further strengthens this driving force, making it an indispensable tool for the future of microelectronics.

Despite its immense promise, the EUV light sources market faces significant challenges that temper its growth. The extremely high cost of EUV lithography equipment, particularly the light sources themselves, represents a substantial barrier to entry, especially for smaller foundries. These sources, often costing hundreds of millions of dollars, require substantial capital investment, limiting their accessibility. Furthermore, the operational complexity and the requirement for highly specialized expertise to maintain and operate these systems add to the overall cost and logistical hurdles. The reliability and uptime of EUV sources have been a persistent concern, although significant progress has been made. Historically, lower uptime translated to higher manufacturing costs and potential production delays. The inherent difficulty in generating and managing such short-wavelength light also leads to unique challenges in optics, contamination control, and vacuum systems, demanding continuous innovation and rigorous engineering. The nascent nature of the EUV ecosystem, with a limited number of established players and a relatively complex supply chain, also poses certain constraints. Supply chain disruptions, material availability, and the need for specialized components can impact production schedules and costs.

The High Power segment is poised to dominate the EUV light sources market, driven by the insatiable demand for increased wafer throughput and cost-effectiveness in advanced semiconductor manufacturing. As foundries push towards higher volumes of leading-edge logic and memory chips, the necessity for light sources that can deliver more photons per second becomes critical. This higher power enables faster exposure times, leading to a significant increase in the number of wafers that can be processed within a given timeframe. This directly translates to lower manufacturing costs per chip, a crucial competitive advantage in the semiconductor industry.

The Fab segment, encompassing the end-users of EUV lithography equipment, is where the demand for these sophisticated light sources originates. The major semiconductor manufacturing hubs, particularly in Asia, are expected to lead the market's growth. Countries like South Korea and Taiwan, home to leading foundries such as Samsung and TSMC respectively, are at the forefront of adopting and expanding EUV lithography capabilities. Their continuous investment in cutting-edge manufacturing technologies to produce the most advanced semiconductors positions them as dominant regions.

Fab Segment Dominance:

Dominant Regions/Countries:

The primary growth catalysts for the EUV light sources industry are the relentless advancements in semiconductor technology, particularly the demand for smaller, faster, and more energy-efficient chips. The exponential growth of AI, 5G deployment, and the burgeoning IoT market are creating an unprecedented demand for cutting-edge semiconductors that can only be manufactured using EUV lithography. Furthermore, the increasing complexity of chip designs necessitates the shorter wavelengths offered by EUV to achieve the required resolution. Strategic investments by major semiconductor manufacturers in EUV capacity expansion, coupled with ongoing R&D efforts to improve source power, reliability, and reduce costs, are further accelerating market growth.

This comprehensive report offers a panoramic view of the EUV light sources market, detailing the intricate interplay of technological advancements, market drivers, and competitive dynamics. It meticulously dissects the historical performance, current market standing, and projected future trajectory, providing stakeholders with actionable intelligence. The report delves into the critical role of EUV in enabling next-generation semiconductor nodes, crucial for powering emerging technologies like AI and 5G. Our analysis goes beyond mere statistics, offering deep dives into the strategic imperatives of leading companies and the evolving landscape of regional dominance. This report is an indispensable resource for any entity seeking to understand and capitalize on the opportunities within this vital and rapidly expanding sector of the semiconductor industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 11.4%.

Key companies in the market include Cymer, Gigaphoton, Ushio, ISTEQ BV.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "EUV Light Sources," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the EUV Light Sources, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.