1. What is the projected Compound Annual Growth Rate (CAGR) of the Smartphone Image Sensors?

The projected CAGR is approximately 7.67%.

Smartphone Image Sensors

Smartphone Image SensorsSmartphone Image Sensors by Type (CMOS, CCD, World Smartphone Image Sensors Production ), by Application (Android, iPhone, World Smartphone Image Sensors Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

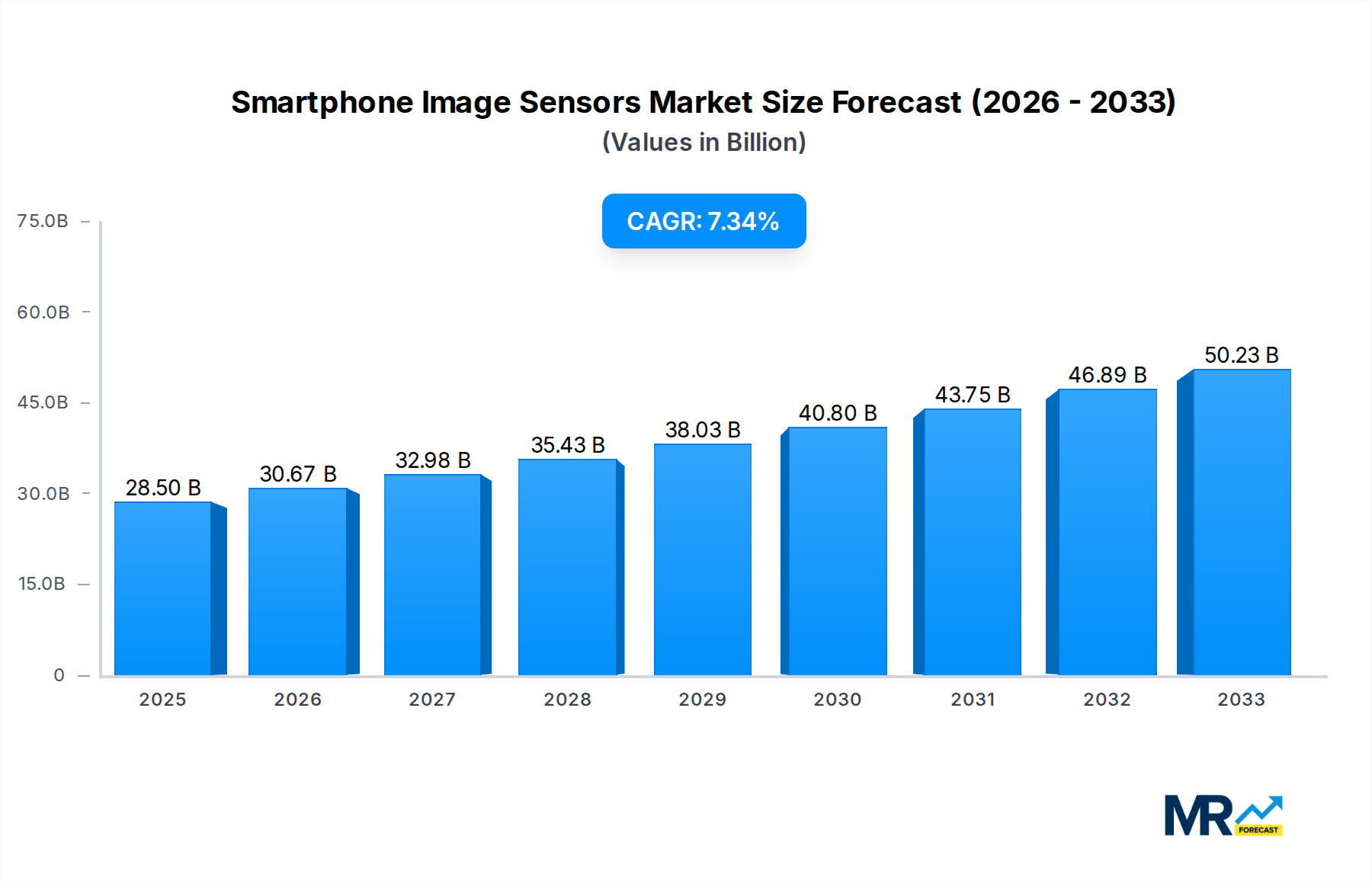

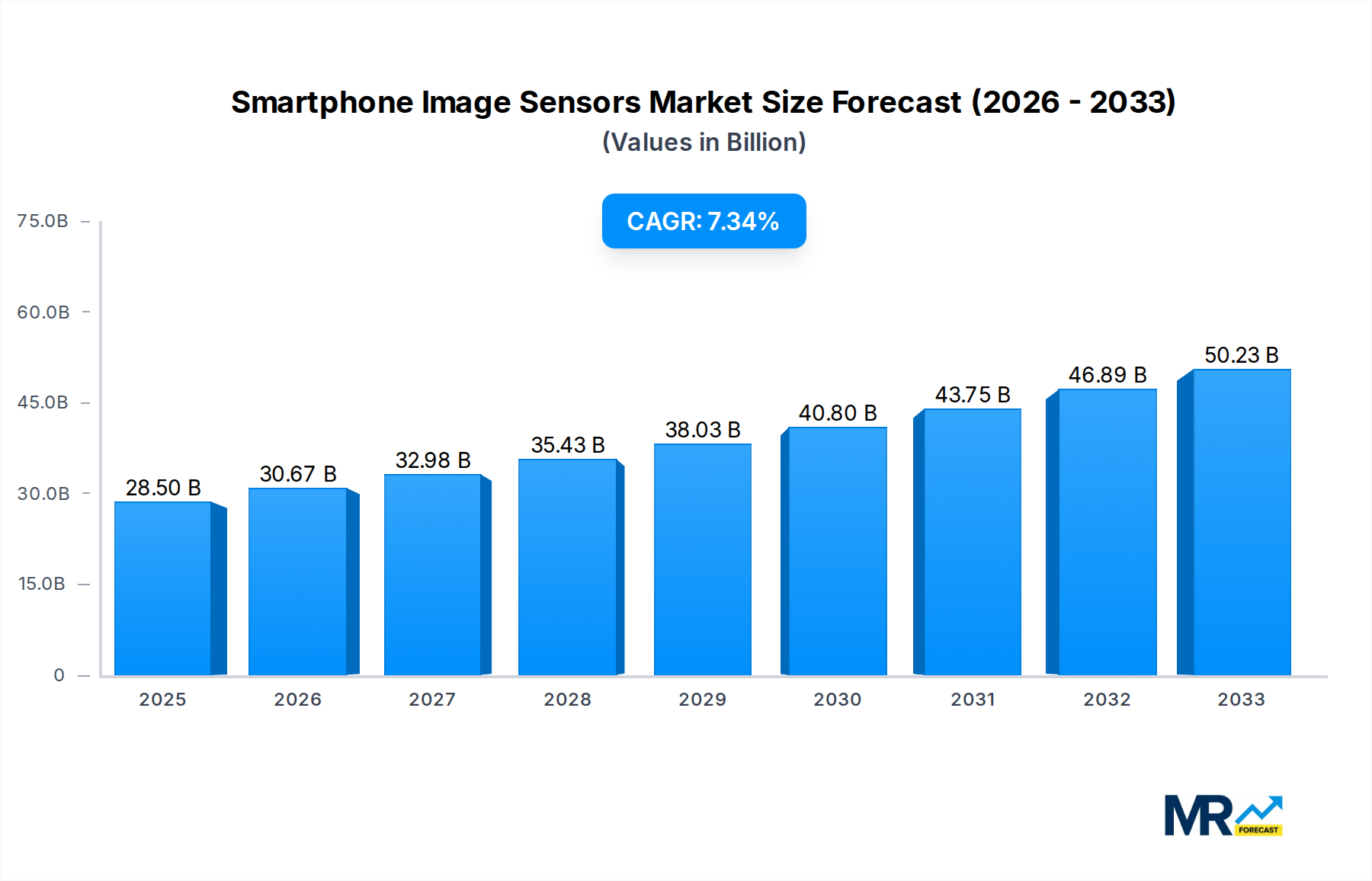

The global smartphone image sensor market is poised for substantial growth, projected to reach an estimated $28.5 billion in 2025. This robust expansion is driven by an anticipated Compound Annual Growth Rate (CAGR) of 7.67% between 2025 and 2033. The escalating demand for high-resolution cameras in smartphones, fueled by advancements in artificial intelligence for image processing, augmented reality applications, and the ever-increasing desire for professional-grade photography on mobile devices, are key catalysts. Furthermore, the proliferation of dual-camera, triple-camera, and even quad-camera systems across all smartphone price segments, from premium flagships to mid-range offerings, significantly bolsters the market. Emerging economies with growing smartphone penetration and a rising middle class are also contributing to this upward trajectory, creating new avenues for market players. The continuous innovation in sensor technology, including the development of larger pixels, improved low-light performance, and enhanced autofocus capabilities, further stimulates consumer interest and replacement cycles.

The market is segmented by sensor type, with CMOS sensors dominating due to their superior performance, lower power consumption, and cost-effectiveness, making them the standard for modern smartphones. On the application front, both Android and iPhone ecosystems represent significant demand centers, with manufacturers consistently pushing the boundaries of mobile imaging. Key players such as Sony, Samsung, and OmniVision Technologies are at the forefront of this innovation, investing heavily in research and development to maintain their competitive edge. While the market is characterized by strong growth, potential restraints include the increasing commoditization of certain sensor technologies and the lengthy smartphone development cycles. Nevertheless, the ongoing integration of advanced features like computational photography and enhanced video recording capabilities will continue to sustain a healthy market momentum. The Asia Pacific region, led by China and India, is expected to remain the largest and fastest-growing market due to its massive consumer base and aggressive smartphone adoption rates.

This report provides an in-depth analysis of the global smartphone image sensor market, projecting a robust growth trajectory driven by relentless innovation and evolving consumer demands. The market, estimated to reach USD 15.75 billion in 2025, is poised for substantial expansion throughout the Forecast Period of 2025-2033. Our comprehensive study, spanning the Study Period of 2019-2033, with 2025 as the Base Year and Estimated Year, delves into the intricate dynamics shaping this vital segment of the mobile technology ecosystem. We meticulously examine key trends, driving forces, challenges, and growth catalysts, offering unparalleled insights for stakeholders. The report covers the Historical Period of 2019-2024, providing a solid foundation for understanding the market's evolution. With a focus on key players, technological advancements, and regional dominance, this report equips businesses with the strategic intelligence needed to navigate and capitalize on the burgeoning opportunities within the smartphone image sensor industry, anticipating it to grow at a CAGR of over 7.5% from 2025 to 2033.

XXX The smartphone image sensor market is currently experiencing a profound transformation, driven by an insatiable consumer appetite for ever-more sophisticated mobile photography and videography capabilities. As smartphones increasingly become the primary capture devices for memories, content creation, and even professional documentation, the demand for higher resolution, superior low-light performance, advanced computational photography features, and compact yet powerful sensors continues to surge. The market is witnessing a significant shift towards larger sensor sizes, enabling better light gathering and shallower depth of field effects, akin to dedicated cameras. This is coupled with the integration of pixel-binning technologies, which allow lower-resolution sensors to capture more light and produce brighter, less noisy images in challenging conditions. Furthermore, the proliferation of multi-camera systems, including ultrawide, telephoto, and macro lenses, has fundamentally altered smartphone photography, demanding diverse and specialized image sensors. The incorporation of Artificial Intelligence (AI) and Machine Learning (ML) algorithms directly into image signal processors (ISPs) is another pivotal trend, powering features like scene recognition, subject tracking, intelligent HDR, and advanced image stabilization. The pursuit of cinematic video recording, including higher frame rates, 8K resolution, and enhanced dynamic range, is also pushing the boundaries of image sensor technology. Looking ahead, advancements in sensor architectures, such as stacked CMOS sensors and novel pixel designs, are expected to further enhance performance and efficiency. The integration of Time-of-Flight (ToF) sensors for improved depth sensing and augmented reality (AR) applications is also gaining traction. The increasing commoditization of high-quality imaging within smartphones is democratizing advanced photography, making professional-grade results accessible to the masses. This trend is underpinned by relentless innovation from leading manufacturers, who are continuously pushing the envelope in terms of pixel pitch, quantum efficiency, and readout speeds. The market is also seeing a growing emphasis on power efficiency, as advanced imaging features place a greater demand on battery life. Ultimately, the smartphone image sensor market is characterized by a dynamic interplay of technological innovation, evolving consumer expectations, and intense competition, all aimed at delivering unparalleled visual experiences directly from our pockets. The projected World Smartphone Image Sensors Production is expected to witness significant volume growth, with billions of units produced annually.

The relentless evolution of smartphone image sensors is propelled by a confluence of powerful driving forces, primarily centered around consumer expectations and technological advancements. The most significant driver is the ever-increasing demand for superior mobile photography and videography. Consumers no longer settle for basic snapshots; they expect their smartphones to deliver professional-grade images and videos, capable of capturing stunning detail in any lighting condition, achieving beautiful background blur, and offering a wide array of creative effects. This demand is fueled by the pervasive use of social media platforms, where visual content reigns supreme, and the growing trend of smartphone-based content creation for vlogging, professional photography, and e-commerce. Furthermore, the rapid advancement of computational photography, powered by sophisticated algorithms and AI, has unlocked new possibilities for image enhancement, noise reduction, and feature integration, making advanced imaging accessible even with smaller sensor sizes. The integration of multiple camera modules on smartphones, each with a specialized purpose (e.g., ultrawide, telephoto, macro), creates a need for a diverse range of high-performance image sensors that can work in concert. The emergence of Augmented Reality (AR) and Virtual Reality (VR) applications also necessitates advanced depth sensing and high-quality imaging capabilities, further spurring innovation in image sensor technology. Moreover, the competitive landscape among smartphone manufacturers is intense, pushing them to differentiate their devices through cutting-edge camera technology, with image sensors being a core component of this differentiation. The continuous pursuit of thinner, more power-efficient devices also demands smaller, yet more capable, image sensors that can be seamlessly integrated into sleek smartphone designs.

Despite the robust growth and innovation within the smartphone image sensor market, several challenges and restraints can impede its unhindered progression. One of the primary hurdles is the inherent physical limitation of sensor miniaturization. As smartphone designs become increasingly compact, there's a finite limit to how large and sophisticated image sensors can become without compromising on other essential components or device aesthetics. This necessitates intricate engineering to achieve higher pixel densities and better performance within constrained physical dimensions. Another significant challenge lies in the escalating cost of research and development (R&D) for advanced sensor technologies. The pursuit of next-generation features, such as enhanced low-light performance, improved dynamic range, and faster readout speeds, requires substantial investment in new materials, fabrication processes, and specialized chip designs. This can create a barrier to entry for smaller players and consolidate market power among established giants. The complex supply chain involved in manufacturing these highly specialized components also presents potential vulnerabilities. Disruptions due to geopolitical factors, natural disasters, or unforeseen production issues can impact the availability and cost of essential raw materials and fabricated sensor chips. Furthermore, the ever-increasing processing demands of advanced imaging algorithms place a significant strain on smartphone chipsets and battery life. Balancing high-performance imaging with energy efficiency remains a perpetual challenge, requiring optimized sensor designs and efficient image signal processing. Finally, the rapid pace of technological obsolescence in the smartphone industry means that image sensor innovations can quickly become outdated, necessitating continuous investment in upgrades and new product development to stay competitive. The market also faces the challenge of consumer perception, where perceived differences in image quality might not always align with the underlying technological advancements, requiring effective marketing and user education.

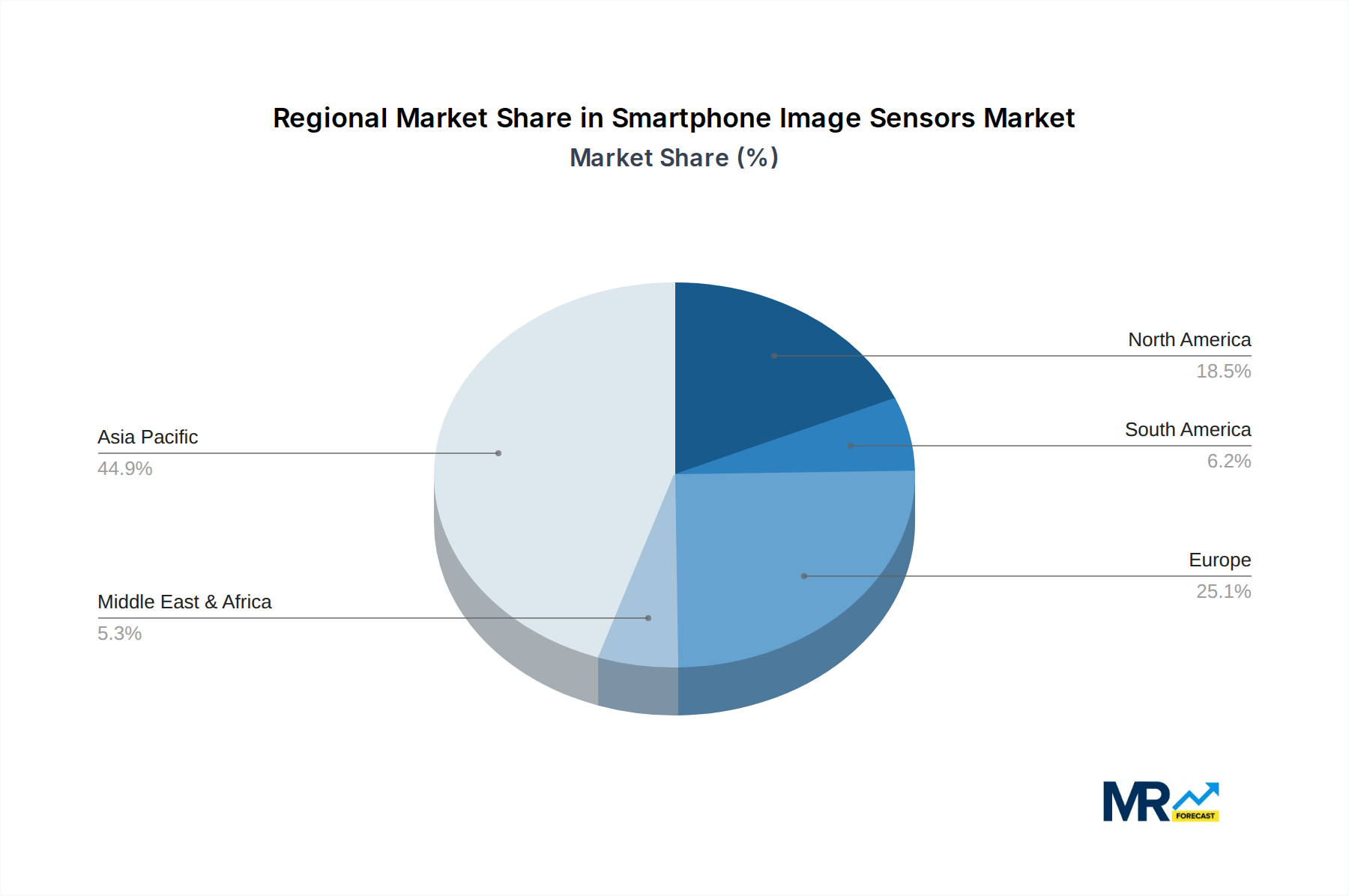

The global smartphone image sensor market is characterized by a dynamic interplay of regional dominance and segment-specific leadership, with Asia Pacific emerging as the undisputed powerhouse, both in terms of production and consumption. Within this region, China stands out as a monumental force, not only as the world's largest smartphone manufacturing hub but also as a significant consumer of these advanced imaging components. The sheer volume of smartphone production in China, catering to both domestic and global markets, directly translates into an immense demand for image sensors. Furthermore, the presence of numerous domestic smartphone brands, alongside global giants with significant manufacturing operations, fuels continuous procurement of these vital components. The rapid adoption of advanced smartphone features, including sophisticated camera systems, by Chinese consumers further solidifies the region's dominance.

The CMOS (Complementary Metal-Oxide-Semiconductor) segment is overwhelmingly dominating the Type of image sensors used in smartphones, and this trend is expected to continue its ascendant march. CMOS technology has largely supplanted its predecessor, CCD (Charge-Coupled Device), in mobile applications due to its inherent advantages in terms of lower power consumption, higher integration capabilities, faster readout speeds, and lower manufacturing costs. This makes CMOS sensors the ideal choice for the power-constrained and cost-sensitive smartphone market. The continuous advancements in CMOS sensor architecture, such as stacked CMOS, back-illuminated CMOS (BSI), and stacked BSI CMOS, have further enhanced their performance, allowing for higher resolution, improved low-light sensitivity, and faster frame rates, all of which are critical for modern smartphone photography. The widespread adoption of CMOS sensors across virtually all smartphone price segments, from entry-level to flagship devices, underscores its market dominance.

In terms of Application, the Android operating system's vast global market share positions it as a dominant segment for smartphone image sensor consumption. While Apple's iPhone commands a significant premium segment, the sheer volume of Android devices sold worldwide, across a multitude of manufacturers and price points, creates an unparalleled demand for image sensors. The open nature of the Android ecosystem allows for a wide variety of smartphone designs and camera configurations, driving the need for a diverse range of image sensors to cater to different market segments and performance expectations. This vast user base constantly seeks improved photographic capabilities in their Android devices, pushing manufacturers to incorporate advanced image sensors. The World Smartphone Image Sensors Production figures, a crucial segment in themselves, are intrinsically linked to the demand generated by these dominant regions and applications. The billions of units produced annually are a direct reflection of the insatiable global appetite for smartphones with increasingly sophisticated imaging prowess, with Asia Pacific, particularly China, leading the manufacturing charge, and the CMOS technology powering the vast majority of these devices.

The smartphone image sensors industry is experiencing robust growth, catalyzed by several key factors. The relentless pursuit of enhanced mobile photography and videography by consumers is a primary driver, pushing manufacturers to innovate with higher resolution sensors, superior low-light performance, and advanced computational photography features. The proliferation of multi-camera systems, including ultrawide, telephoto, and macro lenses, necessitates a diverse range of sophisticated sensors. The growing importance of Augmented Reality (AR) and Virtual Reality (VR) applications also demands improved depth sensing and higher-quality imaging capabilities. Furthermore, the competitive landscape among smartphone brands, constantly striving for differentiation through camera technology, fuels continuous R&D and adoption of cutting-edge sensor solutions.

This report offers an exhaustive examination of the global smartphone image sensor market, meticulously detailing its present landscape and future trajectory. Our analysis encompasses a detailed breakdown of market trends, the fundamental drivers propelling its expansion, and the inherent challenges that stakeholders must navigate. We provide a granular view of key regional and country-specific market dynamics, alongside an in-depth segment analysis, highlighting the dominance of CMOS technology and the substantial influence of the Android application segment on global production volumes. The report further illuminates the growth catalysts that are shaping the industry's evolution, identifies the leading players driving innovation, and charts the significant technological developments shaping the sector. This comprehensive coverage is designed to equip businesses with the strategic insights and data-driven intelligence necessary to capitalize on the opportunities within this rapidly evolving and vital market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.67% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.67%.

Key companies in the market include Sony, Samsung, OmniVision Technologies, SK Hynix Inc., Panasonic, GalaxyCore, SmartSens Technology.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Smartphone Image Sensors," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Smartphone Image Sensors, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.