1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Advanced Packaging Lithography System?

The projected CAGR is approximately 9.8%.

Semiconductor Advanced Packaging Lithography System

Semiconductor Advanced Packaging Lithography SystemSemiconductor Advanced Packaging Lithography System by Type (200mm Wafer, 300mm Wafer, Others, World Semiconductor Advanced Packaging Lithography System Production ), by Application (Wafer Level Packaging, 2.5/3D Packaging, FC Packaging, Others, World Semiconductor Advanced Packaging Lithography System Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

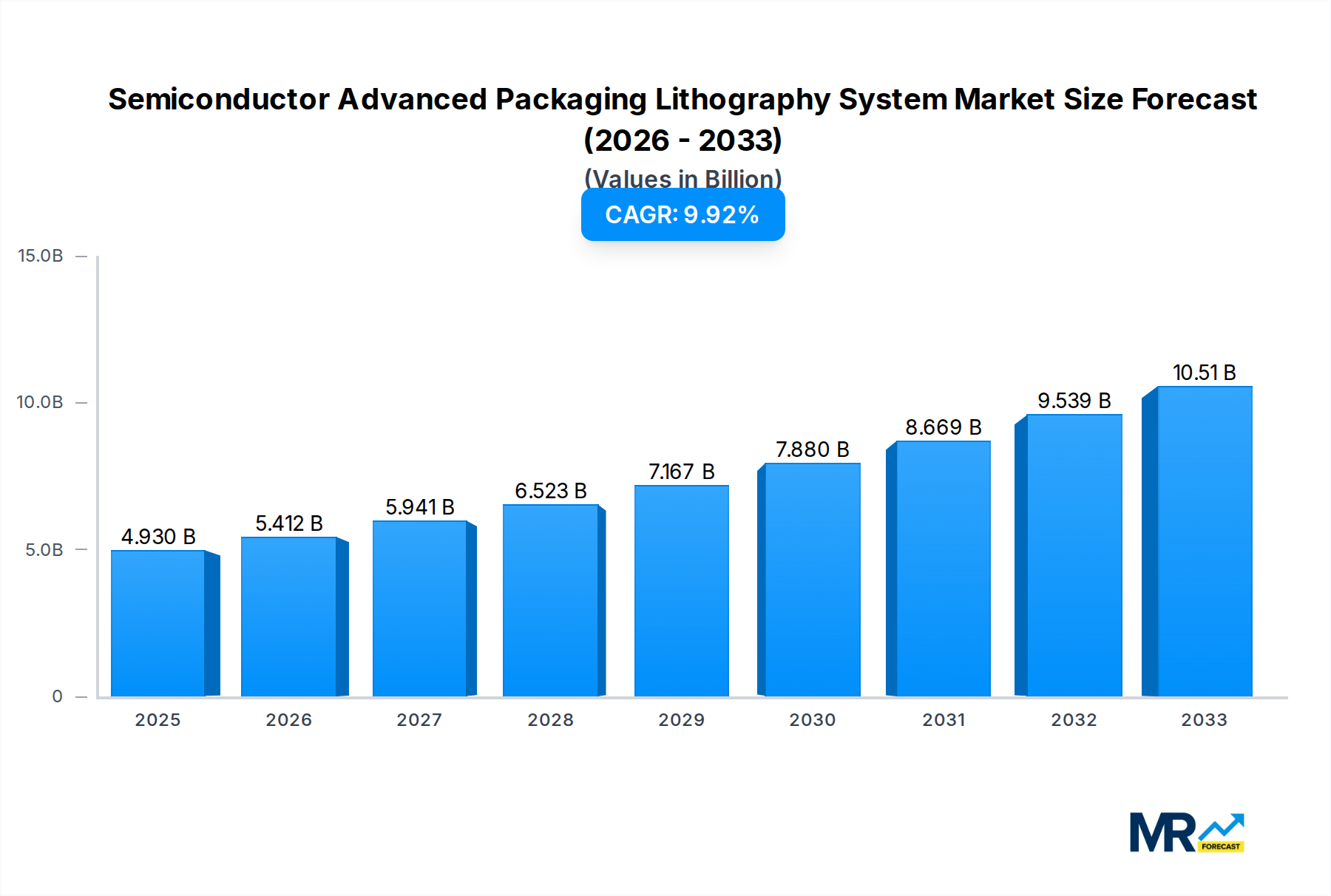

The global Semiconductor Advanced Packaging Lithography System market is poised for substantial expansion, estimated at a robust USD 4.93 billion in 2025 and projected to grow at a compelling Compound Annual Growth Rate (CAGR) of 9.8% through 2033. This significant growth is fueled by the escalating demand for more sophisticated and power-efficient semiconductors, driven by advancements in AI, 5G, high-performance computing (HPC), and the Internet of Things (IoT). As device miniaturization and performance demands intensify, advanced packaging lithography systems become indispensable for their ability to enable finer feature sizes and complex interconnects, crucial for next-generation chip designs. Key market drivers include the continuous innovation in chip architectures, the increasing complexity of semiconductor manufacturing processes, and the growing adoption of heterogeneous integration strategies. These systems are pivotal in achieving the high resolution and precision required for advanced packaging techniques like wafer-level packaging, 2.5/3D packaging, and flip-chip (FC) packaging, all of which are essential for enhancing semiconductor functionality and performance.

The market's trajectory is further shaped by prevailing trends such as the integration of artificial intelligence and machine learning into lithography processes for improved yield and throughput, alongside the development of novel materials and manufacturing techniques that demand enhanced lithographic capabilities. Emerging technologies like EUV (Extreme Ultraviolet) lithography, though primarily used in front-end manufacturing, are influencing the development and requirements for advanced packaging lithography, pushing for greater precision and resolution. Despite this optimistic outlook, potential restraints include the high capital expenditure associated with acquiring and maintaining these sophisticated systems, coupled with the ongoing global supply chain complexities that can impact production and delivery timelines. Nonetheless, the sustained investment in R&D by leading players like Onto Innovation, Ushio, Canon, Kulicke and Soffa Industries, Veeco, Shanghai Micro Electronics Equipment, and Circuit Fabology Microelectronics Equipment, alongside the diversified regional presence across North America, Europe, and particularly the Asia Pacific, underscores the industry's commitment to innovation and market penetration. The dominance of 300mm wafers in advanced packaging further indicates a significant market segment for systems supporting this wafer size.

This comprehensive report offers an in-depth analysis of the global Semiconductor Advanced Packaging Lithography System market, meticulously examining its trajectory from 2019 to 2033. With a base year of 2025, the study delves into historical trends from 2019-2024 and provides robust forecasts for the period 2025-2033. The market, projected to reach billions of dollars, is driven by the escalating demand for sophisticated semiconductor solutions across a multitude of high-growth applications. We will dissect the market by segment, including Type (200mm Wafer, 300mm Wafer, Others) and Application (Wafer Level Packaging, 2.5/3D Packaging, FC Packaging, Others), providing granular insights into their respective market shares and growth dynamics. Furthermore, the report scrutinizes the intricate landscape of World Semiconductor Advanced Packaging Lithography System Production, highlighting key industry developments and the innovations shaping the future of this critical sector.

The global Semiconductor Advanced Packaging Lithography System market is experiencing a period of intense innovation and substantial growth, projected to exceed tens of billions of US dollars by the end of the study period. This upward trajectory is fundamentally driven by the insatiable demand for increasingly powerful and compact electronic devices. As Moore's Law approaches its physical limitations in traditional front-end semiconductor manufacturing, advanced packaging lithography systems have emerged as a crucial enabler for continued performance gains and functional integration. The industry is witnessing a significant shift towards higher density interconnects, smaller feature sizes, and the ability to integrate diverse chip functionalities within a single package. This necessitates lithography solutions capable of achieving unprecedented resolution and precision. The growing complexity of mobile devices, high-performance computing (HPC), artificial intelligence (AI) accelerators, and advanced automotive electronics are all directly fueling the need for these sophisticated systems. Furthermore, the trend towards heterogeneous integration, where different types of chips are combined in advanced packages, is creating new avenues for lithography equipment manufacturers. The ability to precisely pattern intricate interconnects for wafer-level packaging, 2.5D/3D integration, and flip-chip (FC) packaging is paramount. The market is also characterized by an increasing focus on cost-effectiveness and throughput, pushing for lithography solutions that can deliver high yields at competitive price points. The ongoing evolution of maskless lithography technologies and advanced inspection techniques are also key trends that will shape the market's future. The sheer volume of semiconductors required for emerging applications like the Internet of Things (IoT) and 5G infrastructure further underscores the vital role of advanced packaging lithography in ensuring the continued miniaturization and enhanced performance of electronic components.

The semiconductor advanced packaging lithography system market is being propelled by a confluence of powerful driving forces, primarily stemming from the relentless demand for enhanced electronic performance and miniaturization across various industries. The exponential growth in data consumption and processing power required for applications like artificial intelligence, machine learning, and high-performance computing necessitates more sophisticated packaging solutions. Advanced packaging lithography systems are critical for achieving the fine pitch interconnects and high-density wiring required to support these demanding workloads. Moreover, the burgeoning Internet of Things (IoT) ecosystem, with its vast array of connected devices, requires smaller, more power-efficient, and cost-effective semiconductors. Advanced packaging, enabled by precise lithography, allows for the integration of multiple functionalities onto a single chip or package, leading to reduced form factors and lower power consumption. The automotive industry's increasing reliance on advanced driver-assistance systems (ADAS) and autonomous driving technology also contributes significantly to this market's growth, as these applications demand highly reliable and high-performance semiconductor components. Furthermore, the ongoing miniaturization trend in consumer electronics, from smartphones to wearables, continues to push the boundaries of what is possible in semiconductor packaging, directly impacting the demand for cutting-edge lithography solutions. The shift towards heterogeneous integration, where different types of semiconductor dies are combined into a single package, further amplifies the need for highly versatile and precise lithography systems capable of patterning complex interconnect structures.

Despite the robust growth prospects, the Semiconductor Advanced Packaging Lithography System market faces several significant challenges and restraints that could temper its expansion. A primary concern is the immense capital investment required for the research, development, and manufacturing of these sophisticated lithography systems. The technological complexity and precision demanded necessitate substantial financial outlays, potentially limiting the number of market players and creating high barriers to entry. Furthermore, the rapid pace of technological evolution in the semiconductor industry presents a continuous challenge. Lithography systems must constantly adapt to meet ever-decreasing feature sizes and increasing integration densities. This necessitates ongoing R&D efforts and frequent product upgrades, which can be costly and time-consuming for both manufacturers and end-users. The availability and cost of skilled labor – engineers and technicians with specialized expertise in lithography and semiconductor manufacturing – is another critical restraint. A shortage of qualified personnel can hinder production, slow down innovation, and impact the adoption of new technologies. Supply chain disruptions, as witnessed in recent global events, can also significantly impact the availability of essential components and raw materials, leading to production delays and increased costs. Finally, stringent quality control and yield requirements in semiconductor manufacturing place immense pressure on lithography systems to deliver consistent, high-precision results. Any deviation can lead to significant financial losses due to rejected wafers, thus demanding highly reliable and validated equipment.

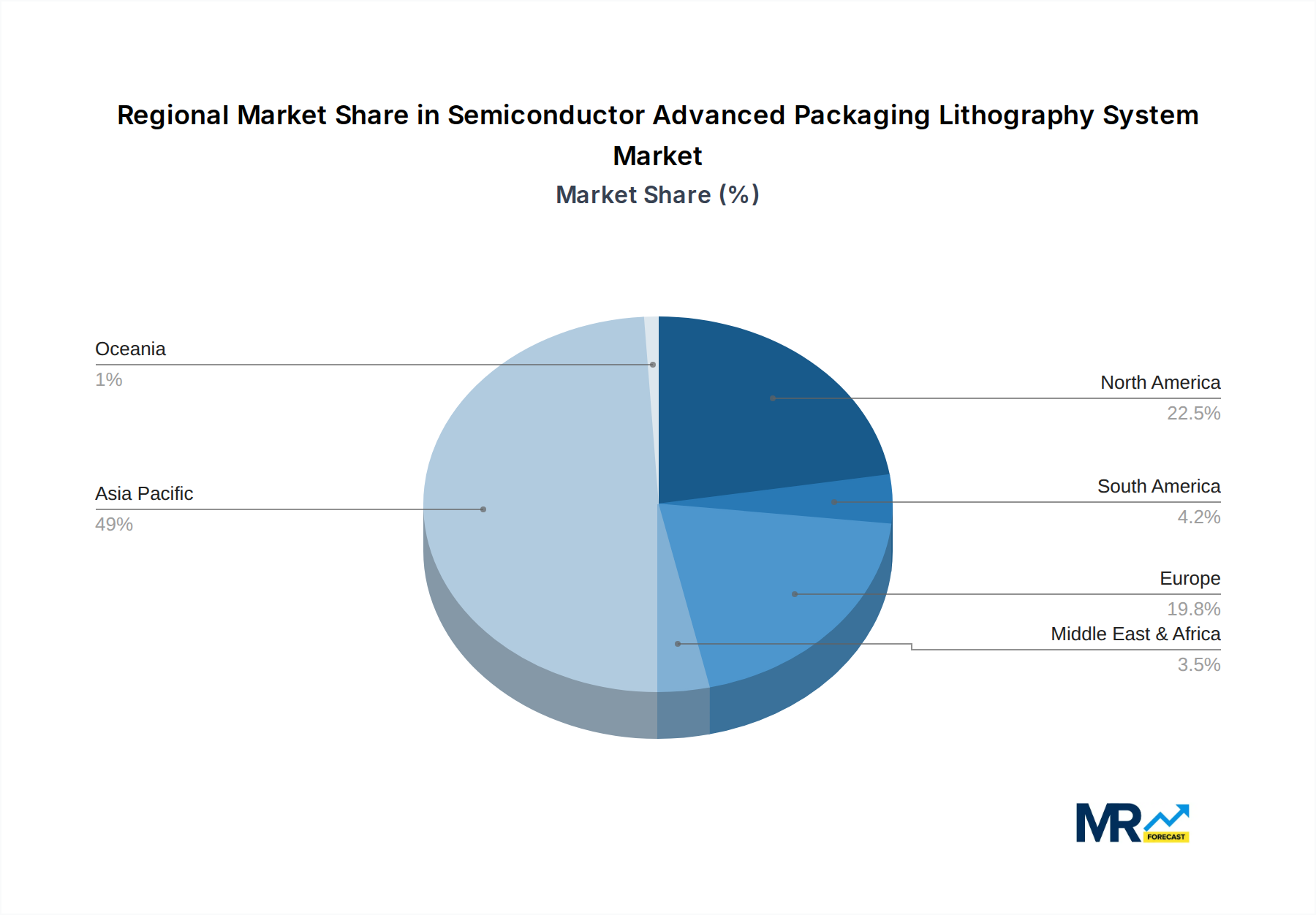

The global Semiconductor Advanced Packaging Lithography System market is poised for significant growth, with specific regions and segments expected to lead the charge.

Key Dominating Regions/Countries:

Key Dominating Segments:

300mm Wafer Segment (Type): As the industry standard for high-volume manufacturing of leading-edge semiconductors, the 300mm Wafer segment will undoubtedly dominate the market for advanced packaging lithography systems. The vast majority of advanced packaging processes, including wafer-level packaging, 2.5/3D packaging, and FC packaging, are increasingly being implemented on 300mm wafers to leverage economies of scale and optimize manufacturing efficiency. The continuous demand for higher performance and greater integration in consumer electronics, data centers, and high-performance computing applications directly fuels the need for advanced lithography solutions that can effectively pattern these larger wafers with sub-micron precision. The cost-effectiveness and throughput advantages offered by 300mm wafer processing make it the preferred choice for next-generation semiconductor devices. The development of new packaging technologies that require even finer features and denser interconnects will further solidify the dominance of the 300mm wafer segment. The sheer volume of production on these wafers makes it the most impactful area for lithography equipment manufacturers.

2.5/3D Packaging (Application): This application segment is experiencing explosive growth, driven by the need for increased performance and functionality without relying solely on traditional scaling. 2.5/3D Packaging allows for the vertical stacking of multiple dies (2.5D) or the integration of dies in both horizontal and vertical dimensions (3D), leading to significant improvements in processing power, memory bandwidth, and form factor reduction. Lithography systems are critical for creating the intricate interconnects, through-silicon vias (TSVs), and redistribution layers (RDLs) that enable these advanced packaging architectures. The demand for AI accelerators, advanced networking chips, and high-end graphics processing units (GPUs) is a primary driver for the adoption of 2.5/3D packaging solutions. As the complexity of integrated circuits continues to rise, the precision and resolution offered by advanced packaging lithography become indispensable. The ability to interconnect diverse chip types within a single package further amplifies the importance of this segment. This segment is expected to outpace others due to its direct contribution to overcoming the limitations of traditional chip scaling and enabling next-generation electronic devices.

The semiconductor advanced packaging lithography system industry is poised for accelerated growth, driven by several key catalysts. The relentless demand for higher performance and increased functionality in consumer electronics, automotive systems, and data centers is a primary growth driver. This is closely followed by the surging adoption of artificial intelligence and machine learning, which require specialized and powerful processors that heavily rely on advanced packaging. The expanding Internet of Things (IoT) ecosystem, with its proliferation of connected devices, also fuels the need for miniaturized, power-efficient, and cost-effective semiconductor solutions enabled by advanced packaging. Furthermore, government initiatives aimed at strengthening domestic semiconductor supply chains and promoting technological innovation are providing significant impetus to the market. The ongoing push for heterogeneous integration, where different types of chips are combined in sophisticated packages, presents a substantial opportunity for advanced lithography solutions to enable intricate interconnections.

This report provides an exhaustive analysis of the global Semiconductor Advanced Packaging Lithography System market, offering unparalleled depth and breadth of coverage. It meticulously dissects market dynamics, key trends, and future projections, presenting a holistic view of this critical sector. The report delves into the intricate details of market segmentation, including detailed breakdowns by Type (200mm Wafer, 300mm Wafer, Others) and Application (Wafer Level Packaging, 2.5/3D Packaging, FC Packaging, Others). It also examines the global production landscape of World Semiconductor Advanced Packaging Lithography System Production, highlighting significant industry developments and technological advancements. With a robust study period spanning from 2019 to 2033, anchored by a base year of 2025, the report offers actionable insights for stakeholders seeking to navigate this dynamic and rapidly evolving market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 9.8%.

Key companies in the market include Onto Innovation, Ushio, Canon, Kulicke and Soffa Industries, Veeco, Shanghai Micro Electronics Equipment, Circuit Fabology Microelectronics Equipment.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Semiconductor Advanced Packaging Lithography System," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Advanced Packaging Lithography System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.