1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Copper Wire Bonding Equipment?

The projected CAGR is approximately 9.6%.

Semiconductor Copper Wire Bonding Equipment

Semiconductor Copper Wire Bonding EquipmentSemiconductor Copper Wire Bonding Equipment by Type (Hot Press Bonding Equipment, Ultrasonic Bonding Equipment, Hot Ultrasonic Bonding Equipment, World Semiconductor Copper Wire Bonding Equipment Production ), by Application (Power Electronics, Automotive Electronics, Industrial Automation, Consumer Electronics, Others, World Semiconductor Copper Wire Bonding Equipment Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

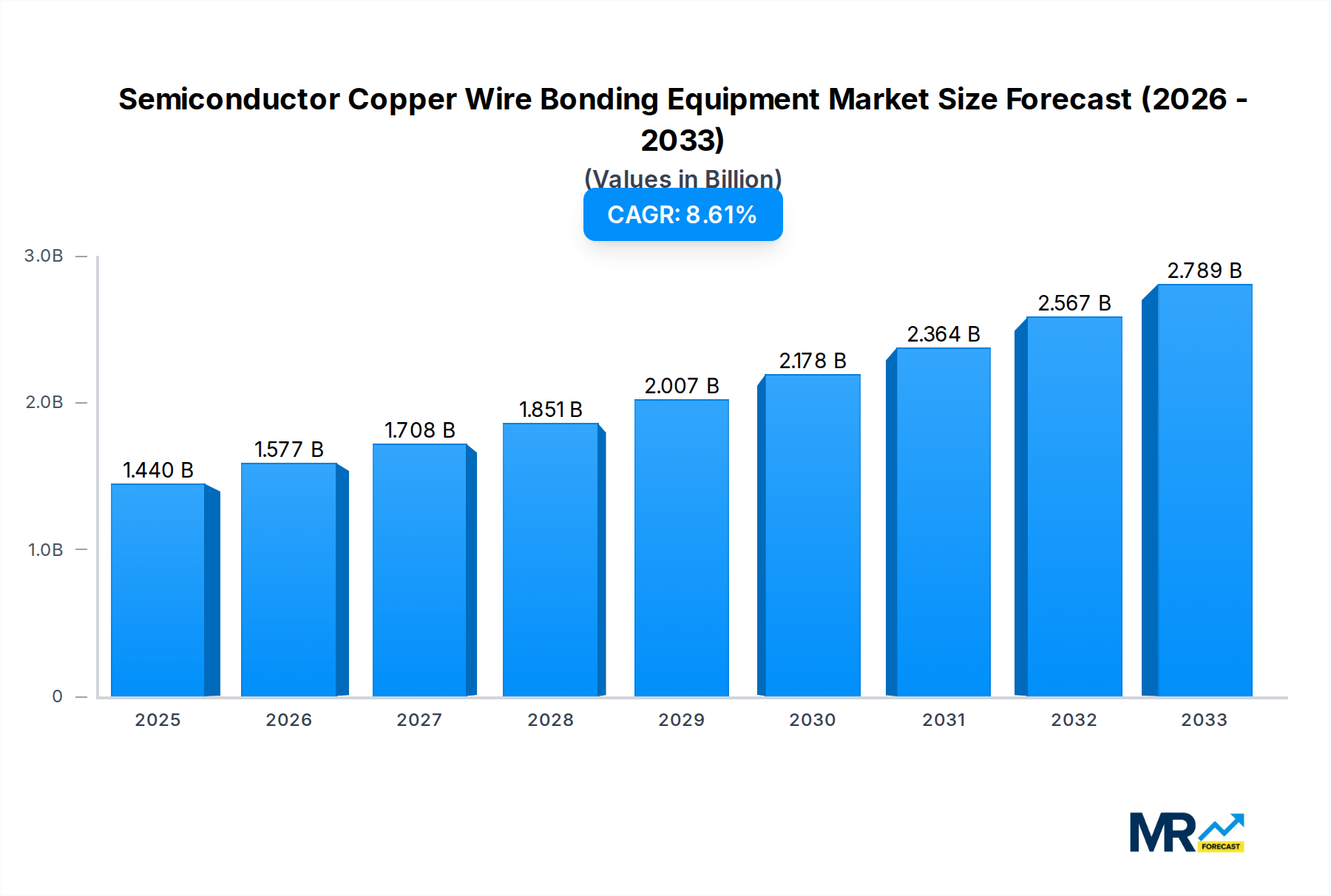

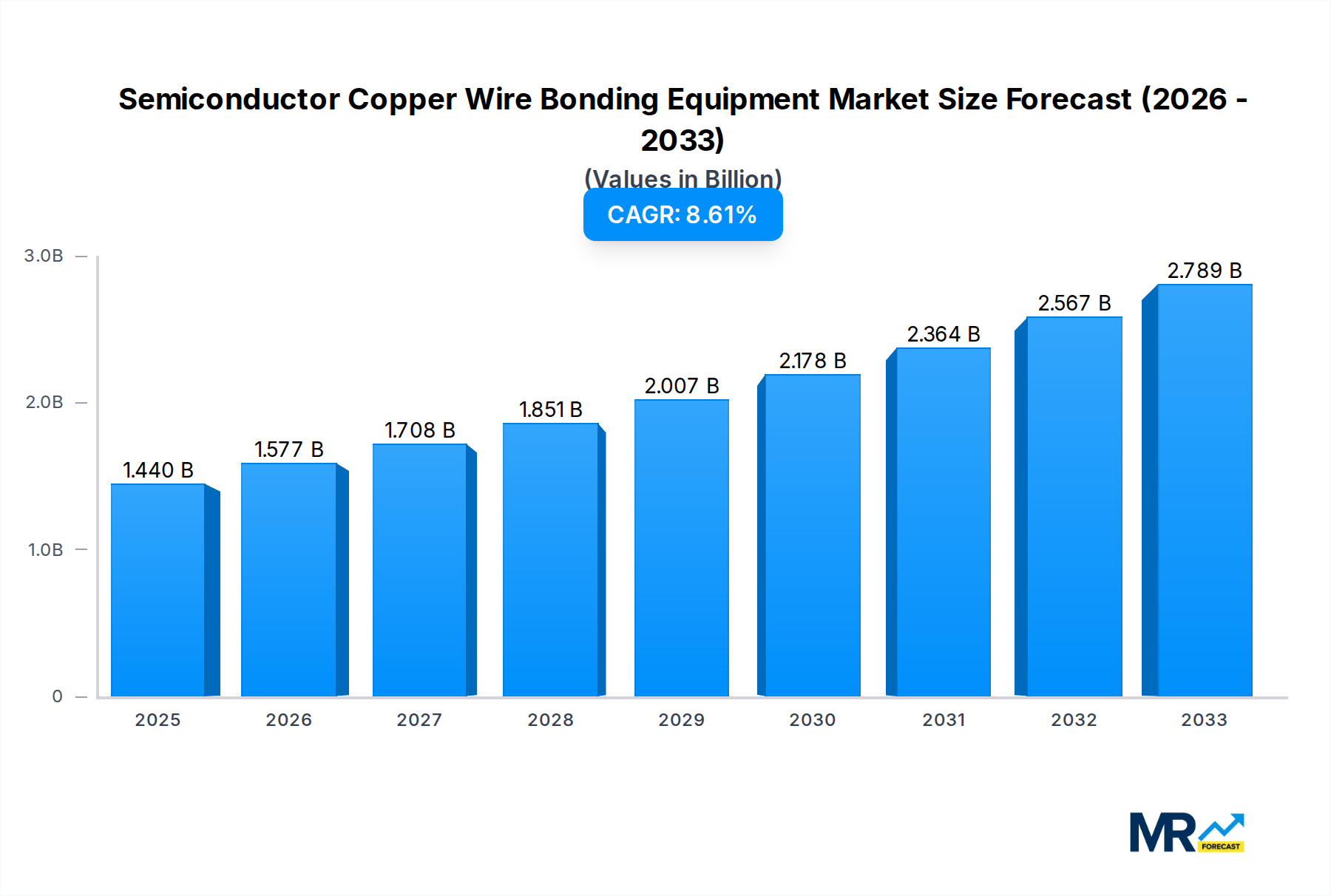

The global semiconductor copper wire bonding equipment market is poised for substantial growth, projected to reach \$1.44 billion in 2025 and expand at a Compound Annual Growth Rate (CAGR) of 9.6% through 2033. This robust expansion is primarily fueled by the escalating demand for advanced semiconductor devices across a multitude of industries. The burgeoning consumer electronics sector, with its continuous innovation in smartphones, wearables, and smart home devices, is a significant driver. Furthermore, the automotive industry's rapid electrification and the increasing integration of sophisticated electronic control units (ECUs) for autonomous driving functionalities are creating immense opportunities for copper wire bonding equipment. Industrial automation, with its focus on smart factories and the Industrial Internet of Things (IIoT), also contributes significantly to market growth, demanding high-performance and reliable semiconductor components.

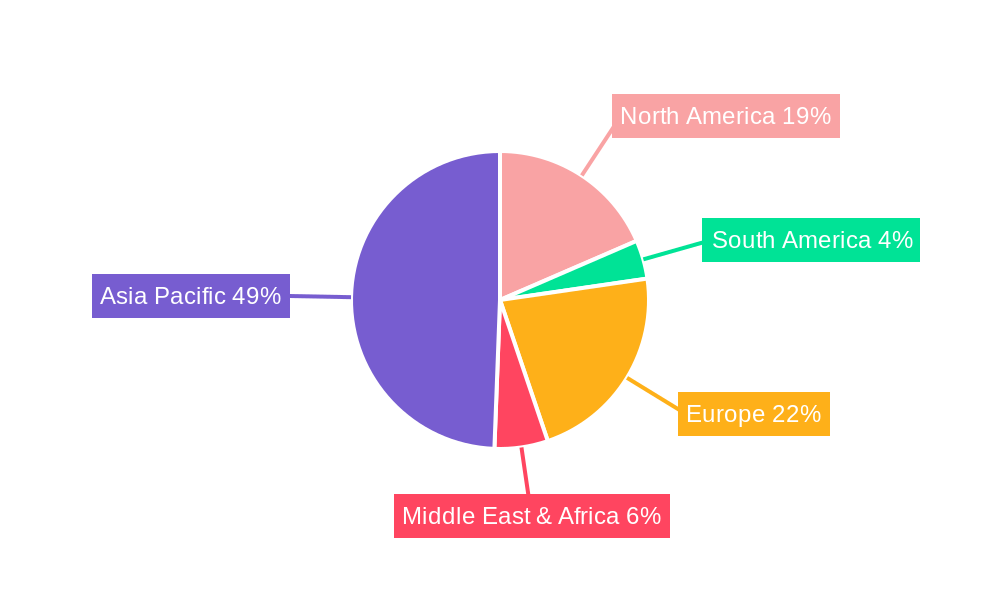

Key trends shaping the market include the increasing adoption of advanced bonding techniques such as ultrasonic bonding for enhanced performance and miniaturization. The shift towards copper wire as a cost-effective and high-performance alternative to gold wire is also a dominant trend, driving innovation in bonding equipment design and capabilities. However, the market faces certain restraints, including the high initial investment cost for cutting-edge bonding equipment and the stringent quality control requirements in semiconductor manufacturing. Geographically, Asia Pacific, led by China and South Korea, is expected to dominate the market due to its substantial semiconductor manufacturing base. North America and Europe are also critical markets, driven by their strong presence in advanced electronics and automotive sectors. Key players like Kulicke & Soffa and ASM Pacific Technology are continuously investing in research and development to cater to the evolving needs of the semiconductor industry.

The global semiconductor copper wire bonding equipment market, projected to reach $5.2 billion by 2025 and expanding to an estimated $8.1 billion by 2033, is experiencing a significant transformation driven by the relentless evolution of semiconductor technology and the burgeoning demand across various end-use industries. The historical period of 2019-2024 witnessed a steady upward trajectory, fueled by advancements in miniaturization, increased processing power, and the growing complexity of integrated circuits. This momentum is set to accelerate throughout the study period of 2019-2033, with the forecast period of 2025-2033 anticipating robust growth. A key trend is the shift towards more sophisticated bonding techniques that offer enhanced reliability, faster throughput, and superior electrical performance. Hot Ultrasonic Bonding Equipment, combining the benefits of both thermal and ultrasonic energy, is emerging as a dominant force, addressing the need for robust interconnections in high-power and high-frequency applications. This is particularly evident in the power electronics and automotive sectors, where the demand for efficient and durable power management solutions is paramount. Furthermore, the increasing integration of advanced driver-assistance systems (ADAS) and the electrification of vehicles are creating unprecedented opportunities for copper wire bonding equipment manufacturers. The intricate circuitry and higher power densities required in these applications necessitate advanced bonding solutions that can handle larger wire diameters and deliver exceptional bond strength. The report delves into the nuanced interplay of technological innovation and market demand, highlighting how the industry is adapting to accommodate these evolving requirements. The base year 2025 serves as a crucial reference point, allowing for a comprehensive analysis of current market dynamics and future projections. The growing adoption of AI and machine learning in semiconductor manufacturing is also indirectly impacting the bonding equipment sector, as manufacturers strive for greater automation, precision, and data-driven process optimization. This focus on intelligent manufacturing is pushing the boundaries of what is possible in terms of speed, accuracy, and overall efficiency. The inherent advantages of copper over gold in terms of cost and conductivity continue to solidify its position as the preferred material for wire bonding, further driving the demand for specialized copper wire bonding equipment.

The semiconductor copper wire bonding equipment market is propelled by a confluence of powerful driving forces that are reshaping its trajectory. Foremost among these is the insatiable demand for advanced electronic devices across an expansive range of consumer, industrial, and automotive applications. The exponential growth of the Internet of Things (IoT), the proliferation of 5G technology, and the continuous innovation in smart devices are all contributing to an escalating need for more sophisticated and higher-performing semiconductors. This, in turn, directly translates to an increased requirement for reliable and efficient wire bonding processes. The automotive industry, with its rapid transition towards electric vehicles (EVs) and the widespread adoption of autonomous driving technologies, is a particularly significant driver. The intricate and power-intensive circuitry required for EVs necessitates highly reliable and robust interconnections, making advanced copper wire bonding equipment indispensable. Moreover, the pursuit of miniaturization and enhanced performance in mobile devices, wearable technology, and high-performance computing continues to push the boundaries of semiconductor design, demanding bonding solutions that can accommodate increasingly complex and dense packaging. The cost-effectiveness of copper as a bonding material compared to gold, coupled with its superior electrical and thermal conductivity, further solidifies its adoption and drives the demand for specialized copper wire bonding equipment capable of handling this material efficiently and reliably.

Despite the robust growth prospects, the semiconductor copper wire bonding equipment market is not without its share of challenges and restraints. A primary concern revolves around the escalating complexity and precision required in modern wire bonding processes. As semiconductor devices become smaller and more intricate, achieving reliable and consistent wire bonds demands extremely high levels of accuracy and control. This necessitates significant investment in research and development for equipment manufacturers, as well as advanced training for operators, which can pose a barrier to entry for smaller players and lead to higher operational costs. Furthermore, the volatile nature of raw material prices, particularly for copper and precious metals used in certain components of the equipment, can impact profit margins for manufacturers. Supply chain disruptions, exacerbated by geopolitical events and global trade tensions, can also lead to delays in production and increase the overall cost of equipment. The stringent quality control and reliability standards in the semiconductor industry, especially for applications in critical sectors like automotive and aerospace, place immense pressure on equipment manufacturers to ensure their products meet the highest benchmarks. Any failure in the bonding process can have significant consequences, leading to product recalls and reputational damage. The rapid pace of technological advancement also presents a challenge, as equipment needs to be constantly updated and upgraded to remain competitive, requiring continuous capital investment from both manufacturers and end-users.

The global semiconductor copper wire bonding equipment market is experiencing significant dominance from key regions and specific segments, driven by a combination of manufacturing prowess, technological adoption, and end-user demand.

Asia-Pacific Region: This region stands as a titan in the semiconductor manufacturing landscape, with countries like China, South Korea, Taiwan, and Japan housing a substantial portion of global wafer fabrication plants and assembly and testing facilities. China, in particular, is rapidly expanding its domestic semiconductor capabilities, leading to a surge in demand for advanced wire bonding equipment. The government's strong focus on self-sufficiency in critical technologies, including semiconductors, is a major impetus. South Korea and Taiwan, already established leaders in chip manufacturing, continue to invest heavily in upgrading their facilities and adopting the latest bonding technologies. Japan, with its legacy of precision engineering and innovation, also contributes significantly to the demand for high-end equipment.

United States: While not having the same sheer volume of manufacturing as Asia-Pacific, the US remains a crucial market due to its leadership in semiconductor design, R&D, and the presence of major chip manufacturers with advanced packaging needs. The growing focus on reshoring semiconductor manufacturing in the US will further bolster demand for advanced bonding equipment.

Europe: Europe is a significant market, particularly driven by its strong automotive and industrial automation sectors. The increasing sophistication of automotive electronics and the growing implementation of Industry 4.0 initiatives are fueling the demand for high-reliability wire bonding solutions. Germany, with its strong automotive industry and advanced manufacturing capabilities, is a key contributor to this demand.

Dominant Segment by Type:

Dominant Segment by Application:

Automotive Electronics: The electrification of vehicles, the proliferation of ADAS, and the increasing complexity of in-car infotainment systems are creating an unprecedented demand for semiconductors. These applications require highly reliable and robust interconnections to ensure safety and performance. Copper wire bonding plays a critical role in Power modules, sensor packaging, and microcontrollers within automotive systems. The stringent reliability standards of the automotive industry necessitate advanced bonding solutions.

Power Electronics: With the global push towards renewable energy, energy efficiency, and electrification across various industries, the demand for advanced power semiconductors is soaring. Copper wire bonding is essential for interconnecting power devices, and the growing need for higher power densities and improved thermal management in power modules directly translates to increased demand for high-performance copper wire bonding equipment.

The growth of the semiconductor copper wire bonding equipment industry is primarily catalyzed by the insatiable demand for advanced electronics driven by the IoT, 5G, and AI revolutions. The accelerating transition to electric vehicles and the increasing sophistication of automotive electronics create a substantial pull for reliable and high-performance bonding solutions. Furthermore, the continuous pursuit of miniaturization and enhanced functionality in consumer electronics necessitates more advanced and precise wire bonding techniques. The inherent cost advantages and superior conductivity of copper over gold as a bonding material solidify its adoption, thereby boosting the demand for specialized copper wire bonding equipment.

This comprehensive report offers an in-depth analysis of the global semiconductor copper wire bonding equipment market, projecting a substantial valuation of $5.2 billion by 2025, with an ambitious expansion to $8.1 billion by 2033. Covering the extensive 2019-2033 study period, with a focus on the 2019-2024 historical period and the 2025-2033 forecast period, the report provides critical insights into market dynamics. It meticulously examines key segments, including Hot Press Bonding Equipment, Ultrasonic Bonding Equipment, and Hot Ultrasonic Bonding Equipment, alongside an assessment of World Semiconductor Copper Wire Bonding Equipment Production. The report also dissects the market by application, highlighting the pivotal roles of Power Electronics, Automotive Electronics, Industrial Automation, Consumer Electronics, and Others. It delves into the intricate growth catalysts, such as the burgeoning demand from the automotive sector and the pervasive adoption of IoT and 5G technologies, while also scrutinizing challenges like the need for extreme precision and supply chain volatilities. Furthermore, the report identifies dominant regions and segments poised for significant market share, offering a granular view of the competitive landscape and the strategic developments shaping the future of semiconductor interconnect technologies.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.6% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 9.6%.

Key companies in the market include Kulicke & Soffa, ASM Pacific Technology, Ultrasonic Engineering, F & K Delvotec, TPT, Hesse GmbH, West Bond, Hybond, KAIJO Corporation, Palomar Technologies, SBT Ultrasonic, Hanxiantech, Wuxi Autowell Technology, Green Intelligent Equipment, Teda, Ningbo Advance Automation Technology.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Semiconductor Copper Wire Bonding Equipment," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Copper Wire Bonding Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.