1. What is the projected Compound Annual Growth Rate (CAGR) of the Wine Packaging Containers Closures and Accessories?

The projected CAGR is approximately 6%.

Wine Packaging Containers Closures and Accessories

Wine Packaging Containers Closures and AccessoriesWine Packaging Containers Closures and Accessories by Type (Styrofoam, Paper, Wood, Glass Packaging, Others, World Wine Packaging Containers Closures and Accessories Production ), by Application (Dry Wine, Semi-dry Wine, Semi-sweet Wine, Sweet Wine, World Wine Packaging Containers Closures and Accessories Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

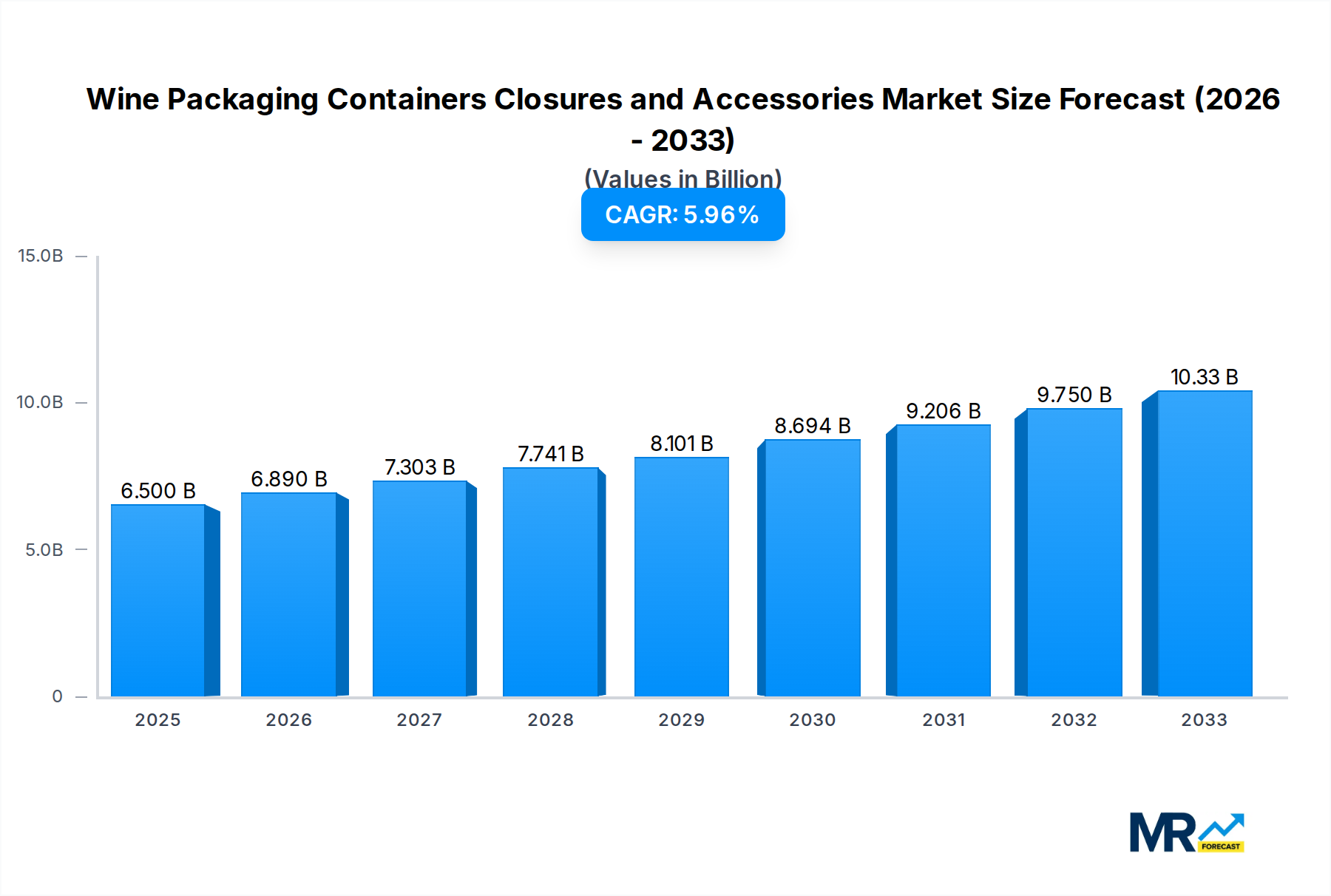

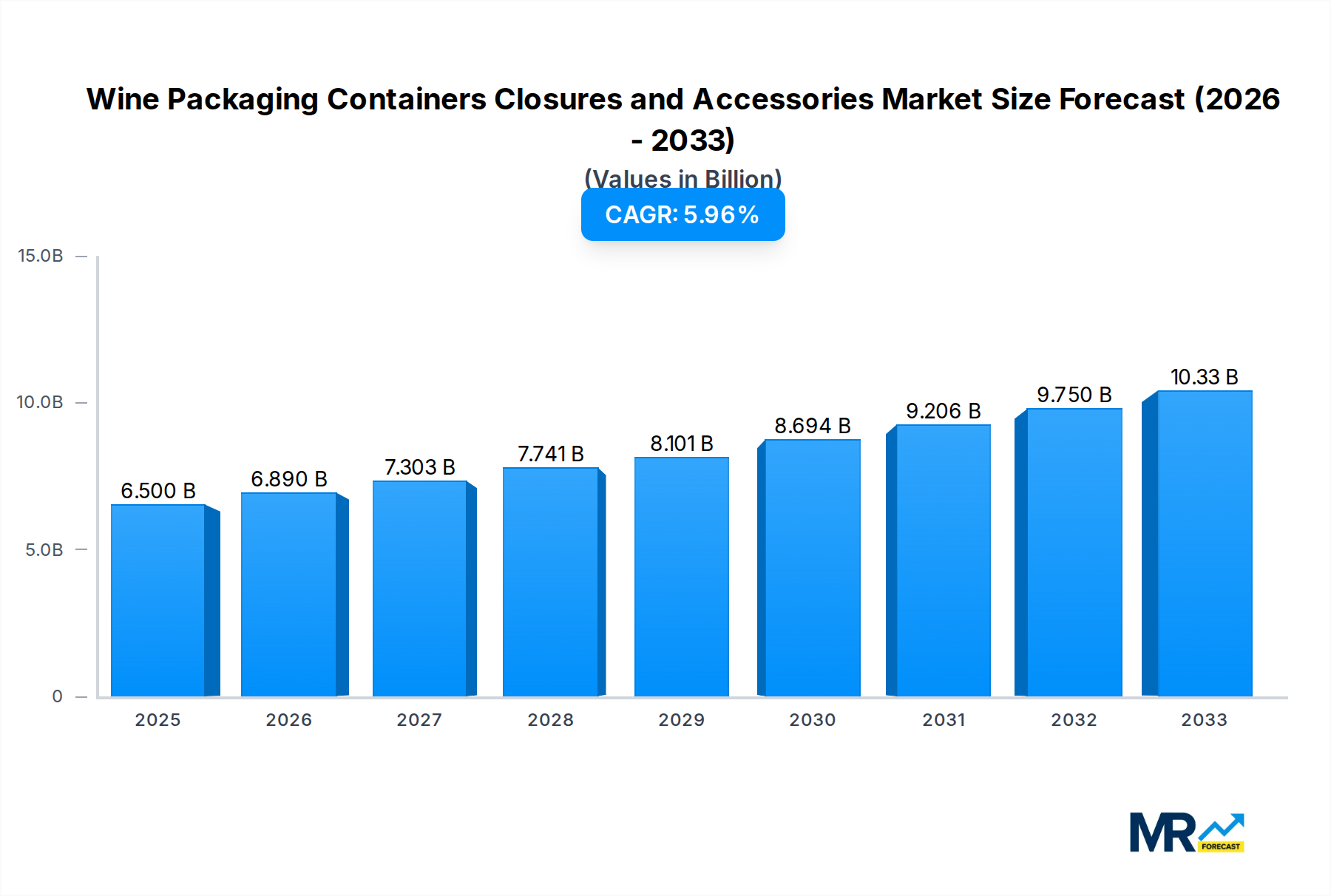

The global market for Wine Packaging Containers, Closures, and Accessories is poised for robust growth, projected to reach approximately $6.5 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 6% anticipated to propel it further through 2033. This expansion is primarily driven by evolving consumer preferences, including a rising demand for premium and eco-friendly packaging solutions. The surge in wine consumption, particularly in emerging economies, coupled with increasing global tourism and a growing appreciation for wine culture, acts as significant catalysts for market expansion. Furthermore, innovations in packaging materials, such as lightweight glass, advanced barrier coatings, and sustainable alternatives like biodegradable plastics and recycled paperboard, are continuously shaping the market landscape, offering enhanced product protection and attractive aesthetics. The market is also witnessing a greater emphasis on customization and branding, with wineries seeking unique packaging designs to differentiate their products and appeal to a wider consumer base.

Key trends shaping the wine packaging sector include the shift towards sustainable and recyclable materials, driven by increasing environmental awareness among consumers and stricter regulatory frameworks. The adoption of lightweight glass bottles and alternative closure systems, such as screw caps and synthetic corks, reflects a commitment to reducing carbon footprints and improving convenience. Technological advancements in printing and labeling are also playing a crucial role, enabling intricate designs and personalized branding that enhance the perceived value of wine products. While the market exhibits strong growth potential, certain restraints, such as fluctuating raw material costs and the established preference for traditional packaging in some mature markets, need to be carefully navigated. Nonetheless, the overall outlook remains highly positive, with continued innovation and a focus on sustainability expected to drive significant value creation across all market segments.

Here is a unique report description on Wine Packaging Containers, Closures, and Accessories, incorporating your specified elements:

This comprehensive report delves into the dynamic global market for wine packaging containers, closures, and accessories. Spanning a detailed Study Period from 2019-2033, with a sharp focus on the Base Year and Estimated Year of 2025, and an extended Forecast Period of 2025-2033, this analysis builds upon a robust Historical Period from 2019-2024. We quantify market opportunities, with key figures often presented in the billions of units, offering an unparalleled understanding of market scale and potential. The report meticulously examines market trends, driving forces, challenges, key regional and segment dominance, growth catalysts, leading industry players, and significant developments, providing actionable insights for stakeholders.

XXX The global wine packaging market is undergoing a significant transformation, driven by evolving consumer preferences, technological advancements, and increasing regulatory scrutiny. A prominent trend is the growing demand for sustainable packaging solutions. Consumers are increasingly aware of the environmental impact of their purchases, leading to a surge in demand for recyclable, biodegradable, and reusable materials. This is evident in the rising adoption of lightweight glass bottles, innovative paper-based packaging, and even biodegradable closures. The traditional dominance of glass bottles, particularly for premium wines, remains strong, driven by its perceived elegance and inertness, essential for preserving wine quality. However, alternatives like Bag-in-Box packaging are gaining traction, especially in markets where convenience and value are paramount, facilitating extended shelf life and reducing wine wastage. Closure innovations are also a key trend, with screw caps continuing their ascendance over corks, offering superior seal integrity and ease of use, particularly for everyday wines. The rise of alternative closures, such as synthetic corks and innovative dispensing systems, further reflects the industry's pursuit of performance and consumer convenience. Furthermore, the integration of smart packaging technologies, including QR codes and NFC tags, is becoming increasingly prevalent, offering consumers enhanced product traceability, authentication, and interactive experiences, thereby deepening brand engagement. The aesthetic appeal of wine packaging is also a critical differentiator. Manufacturers are investing heavily in advanced printing techniques, premium finishes, and unique bottle shapes to capture consumer attention on crowded retail shelves. This trend is particularly pronounced in the premium and luxury wine segments, where packaging plays a pivotal role in conveying brand prestige and product quality. The market is also witnessing a growing interest in personalized and customizable packaging options, catering to special occasions and niche markets. The overarching trend is a move towards packaging that is not only functional and protective but also aesthetically appealing, environmentally responsible, and capable of enhancing the consumer experience.

The global wine packaging market is experiencing robust growth propelled by a confluence of powerful driving forces. Foremost among these is the consistent expansion of the global wine consumption market, fueled by rising disposable incomes in emerging economies and a growing appreciation for wine as a social beverage. As more consumers worldwide embrace wine, the demand for its packaging components naturally escalates. Furthermore, the increasing focus on premiumization within the wine industry is a significant catalyst. Winemakers are investing more in high-quality packaging to differentiate their products, enhance brand perception, and justify premium pricing. This translates into a demand for more sophisticated glass bottles, specialized closures, and elaborate accessory designs. The growing emphasis on sustainability and eco-friendly practices by both consumers and manufacturers is another crucial driver. The push for recyclable, biodegradable, and reusable packaging materials is reshaping the industry, encouraging innovation in materials science and manufacturing processes. This is leading to increased adoption of alternative materials and designs that minimize environmental impact. Technological advancements in packaging machinery and materials also play a vital role, enabling more efficient production, enhanced product protection, and innovative design possibilities. These advancements allow for greater customization, improved barrier properties, and more visually appealing packaging. Finally, the rise of e-commerce for wine sales has created new packaging demands. Online retailers require packaging that is robust enough to withstand shipping and handling while also maintaining the aesthetic appeal of the product, driving innovation in protective and visually attractive shipping solutions.

Despite the optimistic outlook, the wine packaging containers, closures, and accessories market faces several significant challenges and restraints that could temper its growth trajectory. One of the primary concerns is the increasing cost of raw materials, particularly glass and aluminum, which are subject to fluctuations in global commodity prices and energy costs. This can directly impact the profitability of packaging manufacturers and potentially lead to price increases for wineries, which may then be passed on to consumers. Stringent environmental regulations and policies in various regions regarding packaging waste and material sourcing can also pose a challenge. While sustainability is a driving force, adapting to evolving regulatory frameworks and investing in compliance can be costly and time-consuming for businesses. The complex global supply chains, often exacerbated by geopolitical events and trade disputes, can lead to disruptions, affecting the availability and timely delivery of packaging materials. This can result in production delays and increased logistical expenses for wineries. Furthermore, the inertia of tradition and established practices within the wine industry can sometimes hinder the adoption of new and innovative packaging solutions. Some segments of the market, particularly those focused on heritage and terroir, may be resistant to adopting materials or designs that deviate significantly from traditional norms. The need for specialized equipment and infrastructure to handle certain types of packaging, such as Bag-in-Box systems or advanced labeling technologies, can also represent a significant barrier to entry or expansion for smaller wineries or those with limited capital. Finally, the potential for counterfeit products and the need for robust anti-counterfeiting measures add another layer of complexity and cost to the packaging process, demanding innovative security features.

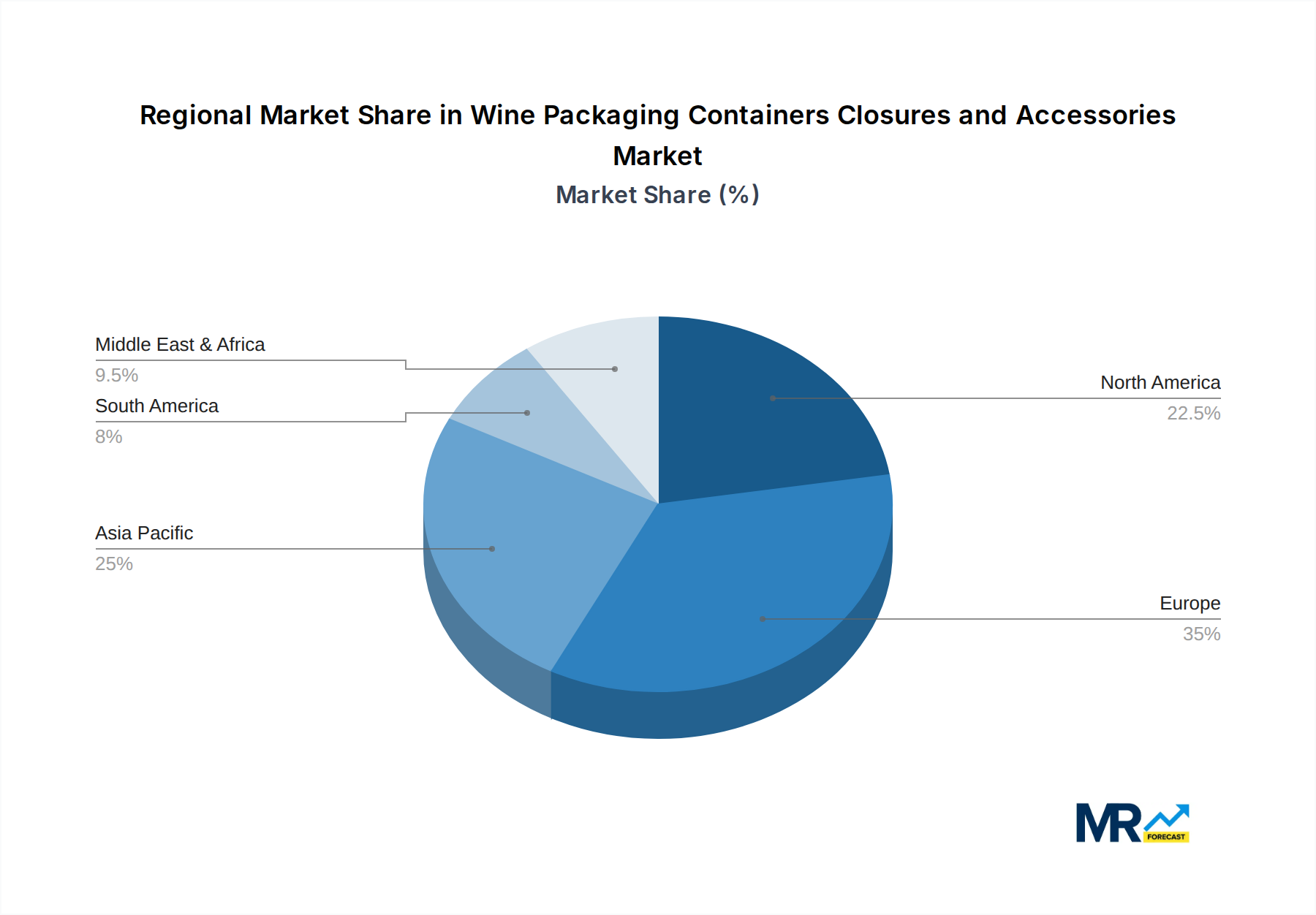

The global wine packaging containers, closures, and accessories market is characterized by significant regional variations and segment dominance. Glass Packaging is poised to remain a dominant segment, particularly in established wine-producing and consuming regions such as Europe and North America. Countries like France, Italy, and the United States continue to be major consumers and producers of wine, with a strong preference for traditional glass bottles that convey quality and heritage. The perceived inertness of glass, which prevents chemical reactions that can alter wine flavor and aroma, remains a critical factor in its enduring popularity, especially for premium and aged wines. This segment is expected to witness substantial growth driven by the increasing demand for premium and super-premium wines, where packaging plays a crucial role in brand perception and value proposition. The innovation within glass packaging, such as lightweighting and the development of recycled glass content, further strengthens its market position by addressing sustainability concerns.

Regionally, Europe is expected to continue its dominance in the wine packaging market. This is attributed to its long-standing wine culture, the presence of numerous established wineries across countries like France, Italy, Spain, and Germany, and a strong consumer preference for wine. The region's mature market is characterized by a high demand for both everyday wines and premium vintages, driving a consistent need for diverse packaging solutions. Within Europe, countries with significant wine production and consumption, such as France and Italy, are key contributors to market growth. Their focus on quality, tradition, and export markets necessitates packaging that aligns with these attributes.

Within the Application segment, Dry Wine applications are expected to dominate the market. This is primarily due to the fact that dry wines constitute the largest share of global wine production and consumption. As consumer palates increasingly favor drier profiles, the demand for packaging solutions tailored to preserve the characteristics of these wines remains consistently high. The need for effective barrier properties to maintain freshness and prevent oxidation in dry wines is a critical consideration that drives demand for specialized glass bottles, advanced closures, and appropriate secondary packaging.

The Type segment of Glass Packaging is projected to be a leading contributor to market value and volume. Its enduring appeal stems from its inert nature, ability to preserve wine quality, and its association with premiumization and perceived luxury. While other materials are gaining traction, glass continues to be the preferred choice for a significant portion of the wine market, from everyday bottles to high-end vintage containers. The continuous innovation in glass manufacturing, including the use of recycled materials and lightweighting techniques, further solidifies its position and addresses growing environmental consciousness among consumers.

Several key growth catalysts are propelling the wine packaging containers, closures, and accessories industry forward. The burgeoning global wine market, driven by increasing consumption in emerging economies and a growing appreciation for wine as a lifestyle beverage, is a fundamental driver. As more consumers turn to wine, the demand for its essential packaging components escalates. The persistent trend of premiumization within the wine sector is another significant catalyst. Wineries are increasingly investing in sophisticated and aesthetically pleasing packaging to enhance brand value and command higher prices, fostering innovation in bottle designs, closures, and decorative accessories. Furthermore, the widespread consumer and industry focus on sustainability is a powerful catalyst, spurring the development and adoption of eco-friendly materials like recycled glass, biodegradable alternatives, and lightweight packaging options. Technological advancements in manufacturing processes and material science enable the creation of more efficient, protective, and visually appealing packaging solutions.

This report offers a holistic and in-depth analysis of the global wine packaging containers, closures, and accessories market. It provides a granular view of market dynamics, meticulously examining historical data from 2019-2024 and projecting future trends through 2033, with a critical focus on the Estimated Year of 2025. The report quantifies market size and growth potential in billions of units, offering actionable insights for strategic decision-making. It identifies and elaborates on key market trends, driving forces, and prevailing challenges, providing a balanced perspective on the industry's landscape. Furthermore, the report highlights dominant regions and segments, offering a clear understanding of where market opportunities are most concentrated. The analysis also pinpoints crucial growth catalysts and provides an exhaustive list of leading industry players, alongside a timeline of significant developments. This comprehensive coverage ensures that stakeholders are equipped with the knowledge to navigate this complex and evolving market effectively.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6%.

Key companies in the market include Berry Global Group, Smurfit Kappa, Rexam, Owens- Illinois, Gerresheimer, Amcor, Ball Corp, Saxco, GloPak USA Corp, G3 Enterprises Inc, Ardagh Group, Oeneo, Multi-Color, Snyder Industries, Nampak.

The market segments include Type, Application.

The market size is estimated to be USD 6.5 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Wine Packaging Containers Closures and Accessories," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Wine Packaging Containers Closures and Accessories, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.