1. What is the projected Compound Annual Growth Rate (CAGR) of the Disposable Plastic Food Packaging Container?

The projected CAGR is approximately 5.4%.

Disposable Plastic Food Packaging Container

Disposable Plastic Food Packaging ContainerDisposable Plastic Food Packaging Container by Type (PP (Polypropylene), PS ( Polystyrene), PET (Polyethylene Terephthalate), World Disposable Plastic Food Packaging Container Production ), by Application (Fresh, Fast Food Take-Away, Others, World Disposable Plastic Food Packaging Container Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

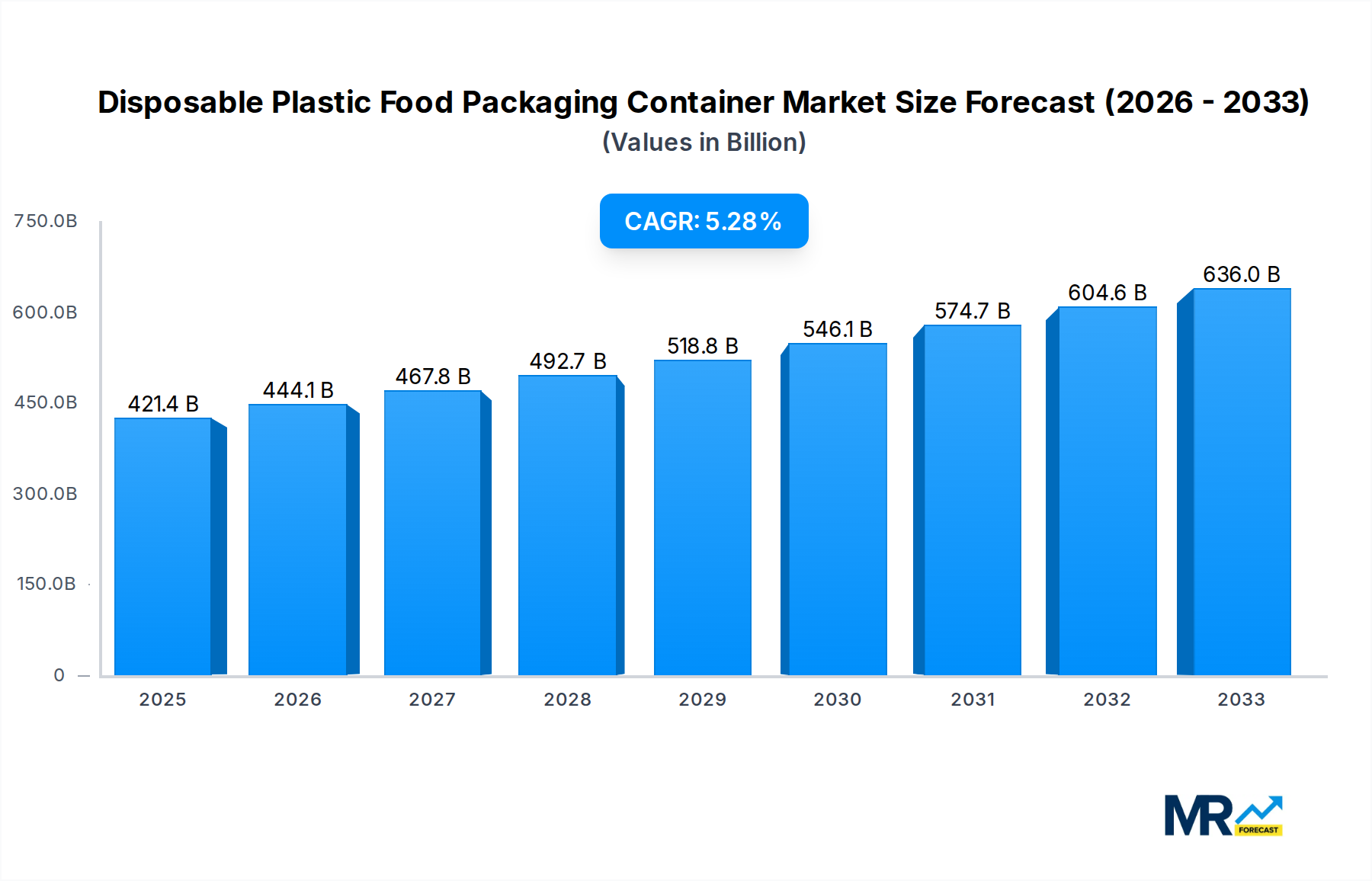

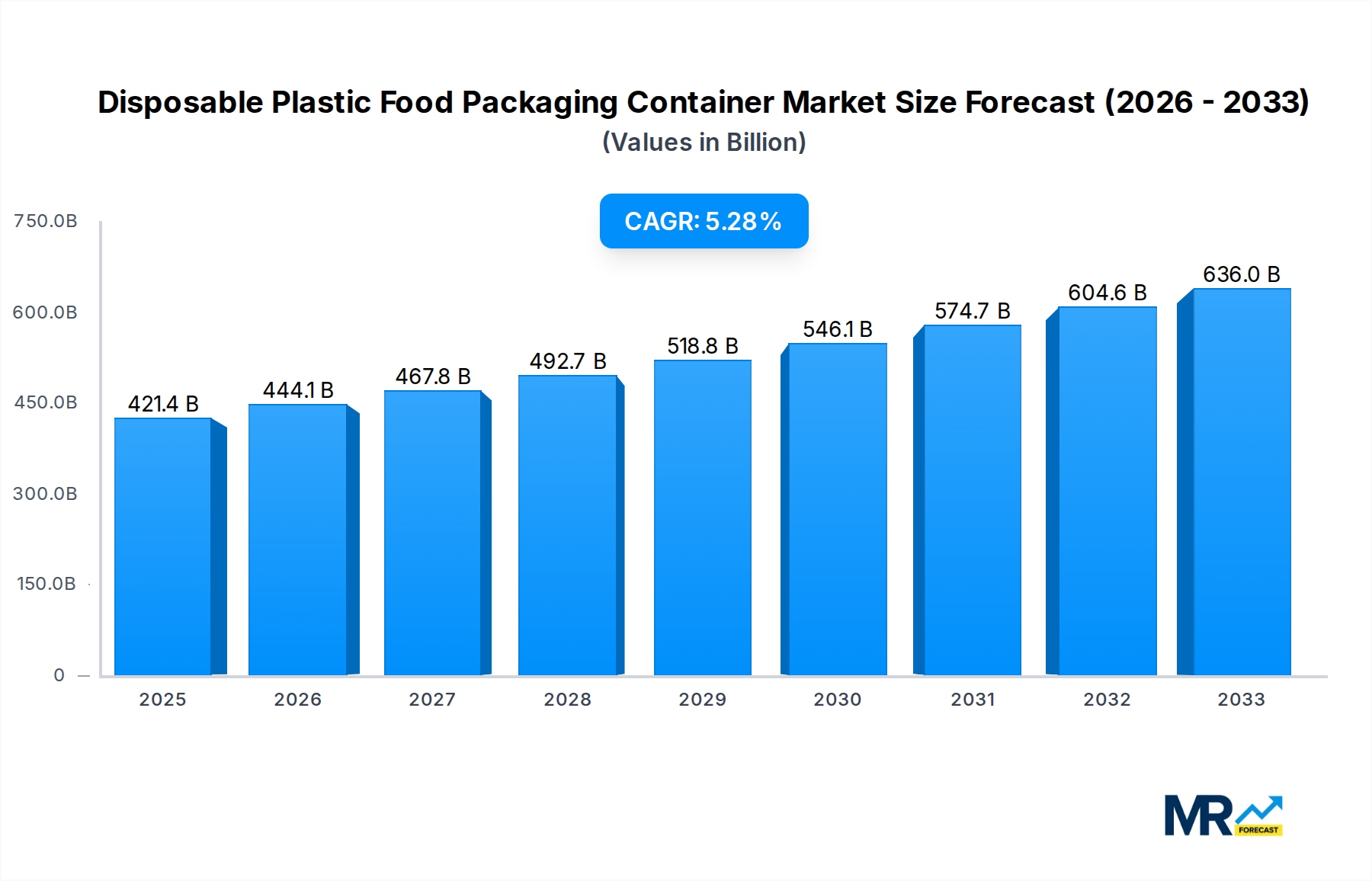

The global disposable plastic food packaging container market is experiencing robust expansion, estimated at a substantial USD 421.38 billion in the base year of 2025. This growth trajectory is further reinforced by a projected Compound Annual Growth Rate (CAGR) of 5.4% over the forecast period from 2025 to 2033. This sustained expansion is primarily fueled by the escalating demand for convenience and the widespread adoption of ready-to-eat meals and takeaway services. The increasing urbanization and the evolving lifestyles of consumers, particularly in emerging economies, are significant drivers, pushing up the consumption of disposable food packaging. Furthermore, the cost-effectiveness and durability of plastic packaging continue to make it a preferred choice for food businesses aiming to maintain product integrity and extend shelf life. Innovations in plastic materials, focusing on enhanced barrier properties and recyclability, are also contributing to market resilience, even amidst growing environmental concerns.

The market is segmented by type into Polypropylene (PP), Polystyrene (PS), and Polyethylene Terephthalate (PET), with PP likely holding a dominant share due to its versatility, heat resistance, and affordability, making it ideal for a wide range of food applications. In terms of application, the "Fresh" food segment and "Fast Food Take-Away" are expected to lead the demand, driven by the convenience-oriented consumer base and the booming food delivery industry. While the market is poised for significant growth, potential restraints such as increasing regulatory pressures for sustainable packaging alternatives and growing consumer awareness regarding plastic pollution could pose challenges. However, advancements in recycling technologies and the development of bio-based or compostable plastic alternatives are emerging trends that could mitigate these restraints and shape the future landscape of disposable plastic food packaging.

This comprehensive report delves into the dynamic global market for Disposable Plastic Food Packaging Containers, offering an in-depth analysis spanning the Historical Period (2019-2024), the Base Year (2025), and the extensive Forecast Period (2025-2033). The study meticulously examines production volumes, market trends, driving forces, inherent challenges, and significant industry developments, all underpinned by data expressed in billions. Our projections are anchored by the Estimated Year (2025), providing a robust foundation for understanding future market trajectories.

The report scrutinizes the market across key segments, including material types such as PP (Polypropylene), PS (Polystyrene), and PET (Polyethylene Terephthalate), alongside application segments like Fresh Food, Fast Food Take-Away, and Others. We provide detailed insights into World Disposable Plastic Food Packaging Container Production volumes, offering a clear quantitative perspective. Furthermore, the report highlights crucial Industry Developments that are shaping the competitive landscape and consumer preferences.

XXX The global disposable plastic food packaging container market is poised for significant evolution, driven by an intricate interplay of evolving consumer habits, economic factors, and increasing regulatory scrutiny. Throughout the Study Period (2019-2033), a consistent upward trajectory in World Disposable Plastic Food Packaging Container Production is projected, moving from an estimated X billion units in the Base Year (2025) to a projected X billion units by 2033. This growth is largely fueled by the ever-increasing demand for convenience, particularly within the Fast Food Take-Away segment, which is anticipated to remain a dominant application. Consumer preferences are leaning towards lightweight, durable, and cost-effective packaging solutions, attributes that disposable plastics inherently possess. However, this growth is increasingly being tempered by a burgeoning global awareness of environmental sustainability. Consumers and governments alike are actively seeking alternatives and advocating for reduced plastic waste. This has led to a burgeoning trend towards the development and adoption of more sustainable plastic formulations, including those with higher recycled content and improved recyclability. The market is also witnessing a surge in innovation geared towards minimizing material usage without compromising functionality, leading to thinner yet stronger container designs. Furthermore, the "on-the-go" lifestyle, amplified by urbanization and busier schedules, continues to bolster the demand for single-use food packaging. While the sheer volume of production is expected to rise, the composition of this production is likely to see a shift. The demand for PP (Polypropylene), known for its versatility and heat resistance, is projected to remain robust, especially for hot food applications. Simultaneously, PET (Polyethylene Terephthalate), valued for its clarity and barrier properties, will continue to be a strong contender for fresh produce and other visually appealing food items. The PS (Polystyrene) segment, while facing some environmental concerns, will likely maintain its presence in cost-sensitive applications. The market is thus characterized by a dichotomy: continued reliance on the inherent advantages of disposable plastics for convenience and cost-efficiency, juxtaposed with a growing imperative to embrace more environmentally responsible practices. The coming years will see a continuous push and pull between these forces, shaping the future of disposable plastic food packaging.

The sustained growth of the disposable plastic food packaging container market is propelled by a confluence of powerful economic and societal factors that underscore the increasing demand for convenience and affordability in modern life. The burgeoning global population, coupled with rapid urbanization, has led to a significant rise in the number of dual-income households and individuals living alone. This demographic shift directly translates into a greater reliance on ready-to-eat meals and take-away options, a core application for disposable plastic containers. The Fast Food Take-Away segment, in particular, is a primary beneficiary of this trend, with consumers prioritizing speed and ease of consumption. Furthermore, the inherent cost-effectiveness of plastic packaging remains a significant driver. For both manufacturers and consumers, disposable plastic containers offer a budget-friendly solution compared to reusable alternatives or other packaging materials, especially when considering the entire lifecycle and logistical costs. The World Disposable Plastic Food Packaging Container Production is thus intrinsically linked to these fundamental economic realities. The resilience and versatility of materials like PP (Polypropylene), PS (Polystyrene), and PET (Polyethylene Terephthalate) also play a crucial role. These plastics are lightweight, durable, and offer excellent barrier properties against moisture and oxygen, ensuring food safety and extending shelf life. Their ability to be molded into a vast array of shapes and sizes caters to diverse food products, from delicate pastries to robust meals, further solidifying their market position. The continuous expansion of the food service industry globally, including restaurants, catering services, and food delivery platforms, directly amplifies the demand for these packaging solutions, creating a robust and ongoing impetus for market growth.

Despite its considerable market momentum, the disposable plastic food packaging container sector faces significant headwinds and restraining forces that threaten to impede its unbridled expansion. The most prominent challenge stems from mounting environmental concerns and the growing global push towards sustainability. Public perception and increasing governmental regulations are actively targeting single-use plastics, leading to bans, taxes, and stringent disposal requirements in many regions. This escalating pressure is forcing manufacturers and consumers to re-evaluate their reliance on conventional plastic packaging. The perceived negative environmental impact, including issues related to plastic pollution in oceans and landfills, is a powerful deterrent for environmentally conscious consumers and businesses. Furthermore, the volatility of raw material prices, primarily crude oil and natural gas derivatives, can significantly impact the production costs of plastic packaging, leading to price fluctuations and impacting profitability. This economic uncertainty can make long-term planning and investment more challenging. The development and widespread adoption of viable and cost-competitive alternative packaging materials, such as biodegradable plastics, paper-based containers, and compostable options, present a direct competitive threat. While often more expensive, these alternatives are gaining traction due to consumer and regulatory demand for eco-friendlier solutions. The logistical complexities and costs associated with recycling and waste management of disposable plastics also pose a significant challenge. Inadequate recycling infrastructure in many parts of the world means that a substantial portion of plastic packaging ends up as waste, further fueling environmental concerns and regulatory action. The inherent disposability also contributes to a linear economic model, which is increasingly being challenged by circular economy principles that advocate for reuse and minimal waste.

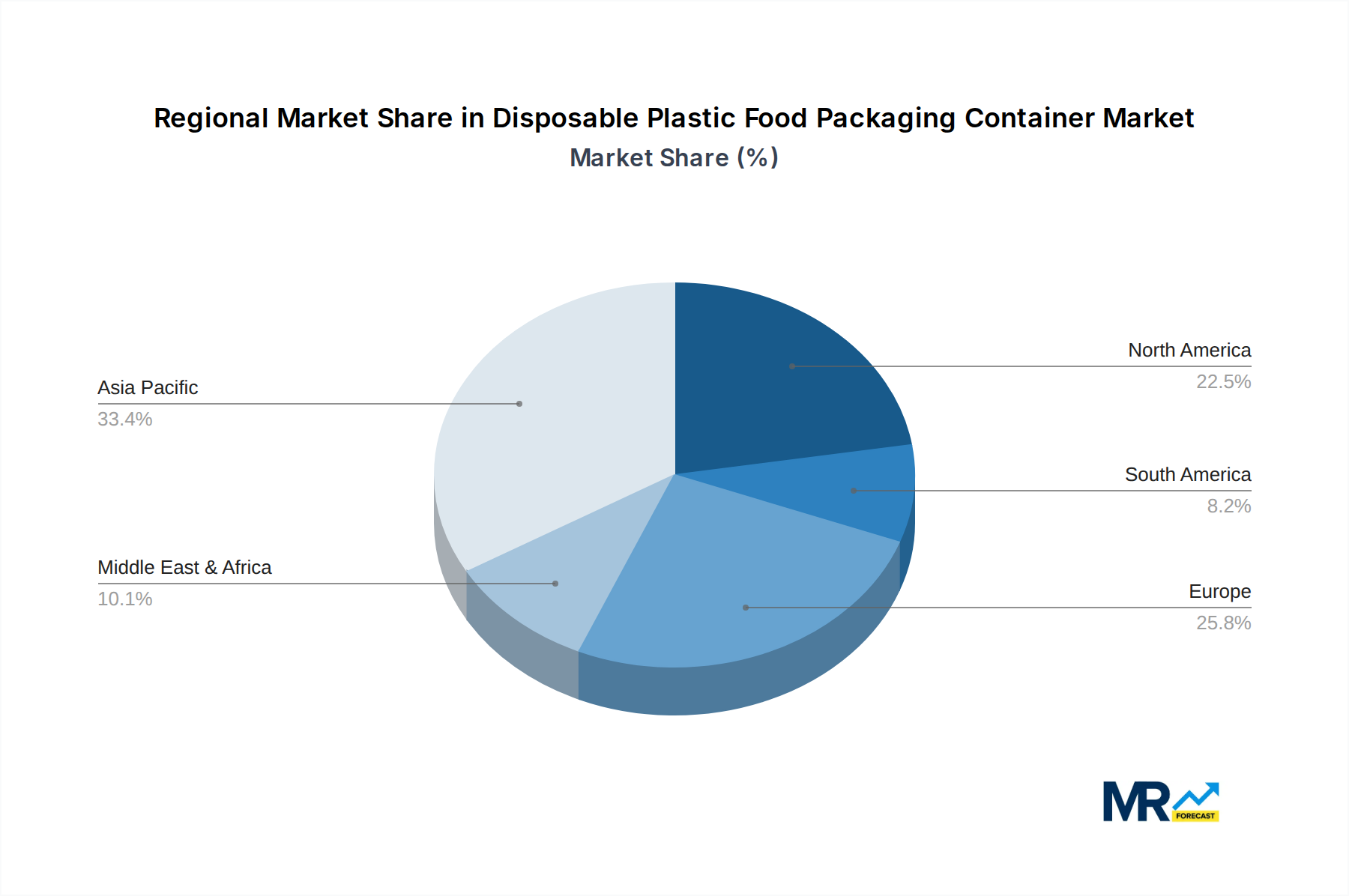

The global disposable plastic food packaging container market is characterized by a complex interplay of regional demands and segment dominance, with Asia-Pacific emerging as a powerhouse, driven by its immense population and rapidly expanding food service industry. Within this region, China stands out as a pivotal player, not only in terms of World Disposable Plastic Food Packaging Container Production but also as a significant consumer. The sheer scale of its domestic market, coupled with its robust manufacturing capabilities, positions China at the forefront. This dominance is further amplified by the strong growth in the Fast Food Take-Away application segment across the continent. The burgeoning middle class, increasing disposable incomes, and the widespread adoption of food delivery apps are creating an insatiable demand for convenient, single-use packaging solutions. India also presents a significant growth opportunity, with its large population and a rapidly evolving food landscape.

When examining the material segments, PP (Polypropylene) is projected to witness substantial growth, particularly within the Asia-Pacific region. Its versatility, cost-effectiveness, and excellent heat resistance make it ideal for a wide range of applications, including hot food containers, trays, and lids. The increasing demand for microwaveable and oven-safe containers further bolsters the position of PP. Its dominance is particularly pronounced in the Fast Food Take-Away and Fresh Food segments where it can be used for a variety of food types.

However, it is crucial to acknowledge the significant and enduring role of PET (Polyethylene Terephthalate). While facing some competition, PET’s superior clarity and barrier properties make it indispensable for packaging fresh produce, salads, and other visually appealing food items. Its lightweight nature and recyclability also contribute to its continued relevance. The Fresh Food application segment heavily relies on PET for its ability to showcase products effectively and maintain freshness.

While PS (Polystyrene), particularly expanded polystyrene (EPS), has historically been a dominant material due to its excellent insulation properties and low cost, it is facing increasing scrutiny due to environmental concerns and potential bans in various regions. Despite this, it continues to hold a significant share in certain applications, especially in the Fast Food Take-Away segment where affordability and insulation are paramount.

The "Others" application segment, which encompasses a wide array of uses beyond fresh food and fast food take-away, including catering, institutional food services, and ready-to-eat meals, also contributes significantly to overall World Disposable Plastic Food Packaging Container Production. This segment is expected to grow steadily as food service operations continue to expand and diversify. The demand for specialized containers for various culinary needs will drive innovation and production within this broader category. The interplay between these material and application segments, within the overarching regional dominance of Asia-Pacific, paints a clear picture of the market's most impactful areas.

The disposable plastic food packaging industry is poised for further expansion, propelled by several key growth catalysts. The relentless urbanization trend and the resultant increase in disposable incomes globally are fostering a greater demand for convenient and on-the-go food options, directly benefiting the Fast Food Take-Away and Ready-to-Eat Meal segments. Furthermore, the robust expansion of the global food delivery ecosystem, facilitated by technological advancements and evolving consumer lifestyles, is a significant accelerator for the industry. Innovation in material science, leading to the development of lighter, stronger, and more resource-efficient plastic containers, also plays a vital role in maintaining competitiveness and meeting evolving consumer expectations.

This report provides an all-encompassing analysis of the disposable plastic food packaging container market, offering invaluable insights for stakeholders. It meticulously details World Disposable Plastic Food Packaging Container Production volumes and growth projections across the Study Period (2019-2033), with a deep dive into the Base Year (2025). The report dissects the market by material type, including PP (Polypropylene), PS (Polystyrene), and PET (Polyethylene Terephthalate), and by application, such as Fresh Food, Fast Food Take-Away, and Others. Key drivers, challenges, regional dynamics, and significant industry developments are thoroughly examined, presenting a holistic view. This comprehensive coverage empowers businesses to make informed strategic decisions in this evolving market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.4%.

Key companies in the market include Tianjin Yihsin Packing Plastic, Meiyang Plastic Metals Products, Zhejiang Great Southeast, Shenzhen Saizhuo Plastic, Beijing Yilong, Huaining County Delin Industry, Zhejiang Tianhe Environmental Technology, Taizhou Fenghua Packaging Container.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Disposable Plastic Food Packaging Container," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Disposable Plastic Food Packaging Container, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.