1. What is the projected Compound Annual Growth Rate (CAGR) of the Laminated Can Packaging?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Laminated Can Packaging

Laminated Can PackagingLaminated Can Packaging by Type (ABL, PBL, World Laminated Can Packaging Production ), by Application (Food, Cosmetics & Personal Care, Pharma & Health, World Laminated Can Packaging Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

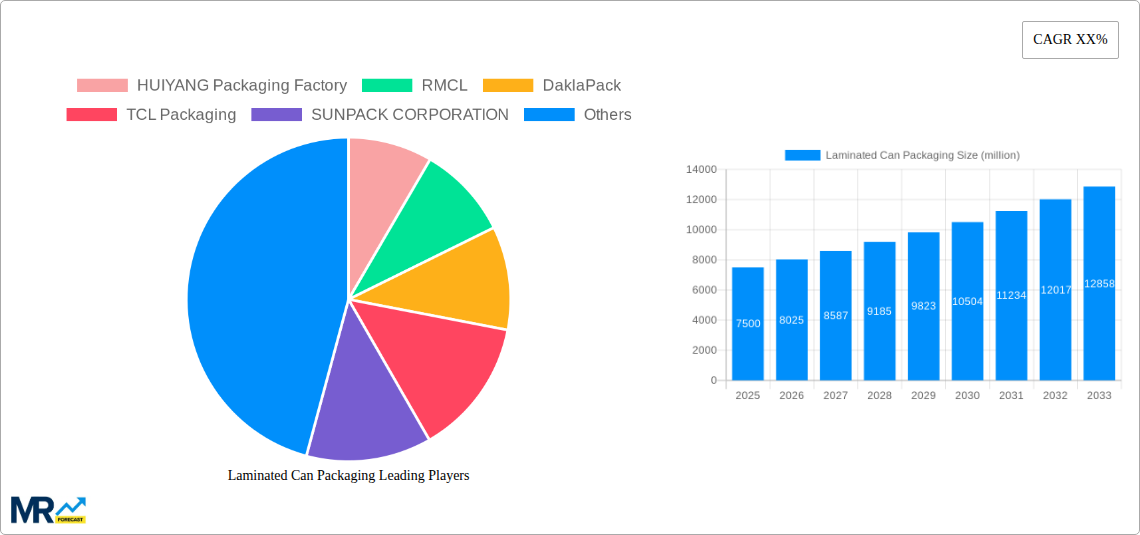

The global laminated can packaging market is poised for significant expansion, driven by an estimated market size of approximately $7.5 billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of around 6.8% through 2033. This robust growth is primarily fueled by the increasing demand for advanced packaging solutions that offer superior barrier properties, extended shelf life, and enhanced product protection. Key drivers include the burgeoning food and beverage industry's need for reliable and aesthetically pleasing packaging, coupled with the rising consumer preference for convenience and sustainable packaging alternatives. The cosmetics and personal care sector is also a substantial contributor, seeking innovative packaging that reflects brand premiumization and ensures product integrity. Furthermore, the pharmaceutical and health sectors are increasingly adopting laminated cans for their ability to maintain the sterility and efficacy of sensitive medications and health products. Emerging economies, particularly in the Asia Pacific region, are expected to be major growth engines due to rapid industrialization, a growing middle class, and increasing disposable incomes, leading to higher consumption of packaged goods.

The market is characterized by several key trends that are shaping its trajectory. Innovations in material science are leading to the development of lighter, stronger, and more sustainable laminated can structures, including advancements in barrier coatings and the incorporation of recycled content. The shift towards eco-friendly packaging solutions is a significant trend, with manufacturers focusing on recyclability and reduced environmental impact. Digital printing technologies are enabling greater customization and personalization of packaging, allowing brands to connect more effectively with consumers. However, the market also faces certain restraints, including the volatile raw material prices, particularly for aluminum and plastic components used in lamination, which can impact production costs and profitability. Stringent regulatory landscapes regarding food contact materials and environmental sustainability in certain regions can also pose challenges. Despite these hurdles, the inherent advantages of laminated can packaging, such as its durability, excellent barrier properties against moisture, oxygen, and light, and its premium appearance, are expected to sustain its growth momentum in the coming years. The competitive landscape features established players and emerging manufacturers vying for market share through product innovation, strategic partnerships, and geographical expansion.

This in-depth report provides an exhaustive analysis of the global Laminated Can Packaging market, offering critical insights and future projections from 2019 to 2033. With a robust base year of 2025, the study meticulously examines the historical performance (2019-2024) and forecasts market dynamics throughout the extensive forecast period (2025-2033). The report delves into key market segments, regional trends, and pivotal industry developments, equipping stakeholders with the knowledge to navigate this evolving landscape.

The global Laminated Can Packaging market is projected to witness significant expansion, driven by an increasing demand for lightweight, versatile, and aesthetically pleasing packaging solutions across various end-use industries. The market's trajectory will be shaped by evolving consumer preferences, technological advancements in material science, and a growing emphasis on sustainable packaging alternatives.

The Laminated Can Packaging market is poised for remarkable growth, with projections indicating a substantial increase in global production, estimated to reach XXX million units by the forecast period. This upward trend is fueled by a confluence of factors, including the inherent advantages of laminated cans over traditional metal or plastic alternatives. Their lightweight nature translates to reduced transportation costs and a lower carbon footprint, aligning with the burgeoning global emphasis on environmental sustainability. Furthermore, the superior barrier properties offered by laminated structures, protecting contents from light, moisture, and oxygen, are crucial for extending shelf life and preserving product integrity, particularly for sensitive applications like food, pharmaceuticals, and cosmetics. The aesthetic versatility of laminated cans also plays a significant role, enabling manufacturers to achieve premium finishes, intricate designs, and vibrant branding, thereby enhancing product appeal on crowded retail shelves. This visual enhancement is particularly critical in the fast-moving consumer goods (FMCG) sector, where packaging often serves as the primary point of consumer engagement. The development of innovative printing techniques and surface treatments further amplifies this aesthetic advantage, allowing for high-resolution graphics and tactile finishes that elevate brand perception. The increasing adoption of advanced manufacturing processes, leading to greater production efficiency and cost-effectiveness, is also contributing to the market's positive outlook. Moreover, the growing trend towards smaller, single-serving packaging formats, particularly in the food and beverage industry, is expected to drive demand for specialized laminated can solutions. The ability to customize and tailor laminated can designs to specific product requirements, including shape, size, and functional features like easy-open mechanisms, provides a competitive edge for manufacturers. As regulatory landscapes evolve to favor recyclable and sustainable packaging materials, laminated cans, with their potential for improved recyclability and the incorporation of bio-based components, are well-positioned to capitalize on these shifts. The report anticipates a consistent upward trajectory in production volumes, driven by both the expansion of existing applications and the emergence of novel uses for these versatile packaging containers.

The global Laminated Can Packaging market is experiencing a robust surge, propelled by several key drivers that are fundamentally reshaping its landscape. Foremost among these is the escalating consumer demand for enhanced product protection and extended shelf life. Laminated cans, with their multi-layered construction, offer superior barrier properties against moisture, oxygen, and light, significantly preserving the quality and integrity of packaged goods. This is particularly critical for perishable food items, sensitive pharmaceutical products, and premium cosmetic formulations, where spoilage and degradation can lead to significant economic losses and consumer dissatisfaction. Consequently, manufacturers are increasingly opting for laminated cans to ensure product freshness and safety, thereby reducing waste and enhancing brand reputation. Concurrently, the growing global consciousness towards environmental sustainability is a powerful catalyst. Laminated packaging, often designed for recyclability and featuring lighter-weight materials compared to traditional alternatives, appeals to eco-conscious consumers and aligns with corporate sustainability initiatives. This shift towards greener packaging solutions is not only driven by ethical considerations but also by tightening environmental regulations in various regions, compelling industries to adopt more sustainable practices. Furthermore, the aesthetic appeal and branding flexibility offered by laminated cans are increasingly recognized as crucial differentiators in competitive markets. The ability to achieve high-quality graphics, vibrant colors, and premium finishes allows brands to capture consumer attention and communicate their value proposition effectively. This visual impact is particularly important in the FMCG sector, where packaging plays a pivotal role in impulse purchases and brand recognition. The ongoing advancements in material science and manufacturing technologies are also contributing significantly to the market's expansion. Innovations in laminating techniques, substrate development, and printing processes are leading to more cost-effective, efficient, and versatile laminated can solutions, making them increasingly accessible and attractive to a wider range of industries.

Despite the promising growth trajectory of the Laminated Can Packaging market, several challenges and restraints can impede its full potential. A significant hurdle is the perceived complexity and cost associated with the manufacturing process. The multi-layer construction often requires specialized machinery and more intricate production steps compared to simpler packaging formats, which can translate to higher initial investment and operational costs for manufacturers. This cost factor can be particularly prohibitive for smaller businesses or those operating in price-sensitive markets, potentially limiting widespread adoption. Furthermore, while laminated cans are increasingly designed for recyclability, the actual end-of-life management infrastructure for these composite materials remains a concern in many regions. The separation of different layers for effective recycling can be technically challenging and requires specialized sorting facilities that are not universally available. This can lead to concerns about the true environmental sustainability of laminated cans if they end up in landfills or incineration, thus undermining their eco-friendly appeal. Consumer perception and awareness also play a role. Some consumers may still associate laminated packaging with less sustainable options or may be unaware of the advancements in recyclability that have been made. Educating the public about the environmental benefits and proper disposal methods for laminated cans is crucial for broader market acceptance. Additionally, fluctuations in the cost of raw materials, such as specific polymers and aluminum or paperboard substrates, can impact the overall pricing and profitability of laminated cans. Volatility in these commodity markets can create uncertainty for both manufacturers and their clients. Lastly, the availability of readily established and cost-effective alternatives, such as traditional metal cans or glass jars, in certain applications can present competition, especially for industries where the unique benefits of laminated packaging may not be as critical or as highly valued. Overcoming these challenges will require continued innovation in manufacturing, improved recycling infrastructure, enhanced consumer education, and strategic cost management.

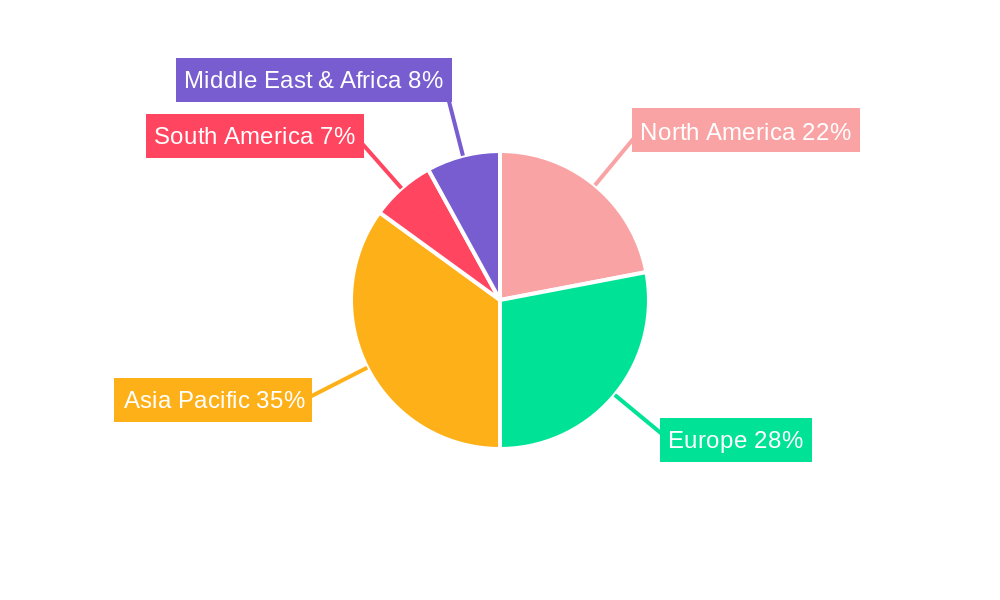

The global Laminated Can Packaging market is characterized by regional variations in adoption and growth, with certain regions and segments exhibiting a more pronounced dominance.

Dominant Regions:

Asia Pacific: This region is expected to be a significant powerhouse in the Laminated Can Packaging market, driven by its vast and rapidly growing consumer base, particularly in countries like China and India. The burgeoning middle class, coupled with increasing disposable incomes, fuels demand across food and beverage, personal care, and pharmaceutical sectors.

North America: This region stands as another critical market for Laminated Can Packaging, driven by advanced consumer preferences for convenience, product quality, and sustainable packaging.

Dominant Segments:

ABL (Aluminum-Plastic Laminates): This type of laminated can packaging is expected to hold a substantial market share due to its excellent barrier properties, lightweight nature, and good printability. The combination of aluminum's impermeability and plastic's flexibility and cost-effectiveness makes ABL cans highly versatile for a wide range of applications.

PBL (Plastic-Barrier Laminates): While potentially having a smaller share than ABL, PBL is experiencing robust growth, particularly as advancements in barrier polymers improve their performance. These offer a lighter alternative and can be cost-effective in certain applications.

The World Laminated Can Packaging Production itself, as a broad indicator, will naturally correlate with the dominance of these regions and segments. The report forecasts a steady increase in overall production, with Asia Pacific leading in volume and North America driving innovation and demand for high-value applications. The interplay between specific laminated can types and their suitability for various end-use applications will define the market's future landscape, with a continuous drive towards more sustainable and high-performance solutions.

The Laminated Can Packaging industry is experiencing robust growth, propelled by several key catalysts. The increasing consumer demand for enhanced product protection and extended shelf life is a primary driver, with laminated cans offering superior barrier properties against moisture, oxygen, and light. Simultaneously, a growing global emphasis on sustainability is encouraging the adoption of lighter-weight and recyclable packaging solutions, aligning with corporate environmental goals and stricter regulations. Furthermore, advancements in material science and manufacturing technologies are leading to more cost-effective and versatile laminated can options, making them attractive to a wider range of industries. The versatility in design and branding possibilities also plays a crucial role, enabling companies to enhance product appeal and market differentiation.

This comprehensive report offers an exhaustive exploration of the Laminated Can Packaging market, providing invaluable data and analysis for industry stakeholders. It meticulously examines market size, growth rates, and key trends from the historical period of 2019-2024 through to the projected forecast period of 2025-2033, with a dedicated base year analysis for 2025. The report delves into the driving forces and challenges shaping the market, offering insights into the strategic initiatives of leading players and significant industry developments. Furthermore, it provides an in-depth regional and segment-wise analysis, highlighting dominant areas and growth catalysts, thus equipping readers with a holistic understanding of this dynamic sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include HUIYANG Packaging Factory, RMCL, DaklaPack, TCL Packaging, SUNPACK CORPORATION, OPM Group, API, Glenroy, BPI Protec, Granitol.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Laminated Can Packaging," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Laminated Can Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.