1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Zero Foil Packaging?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Food Zero Foil Packaging

Food Zero Foil PackagingFood Zero Foil Packaging by Type (Single Zero Foil, Double Zero Foil), by Application (Household, Restaurant, Supermarket), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

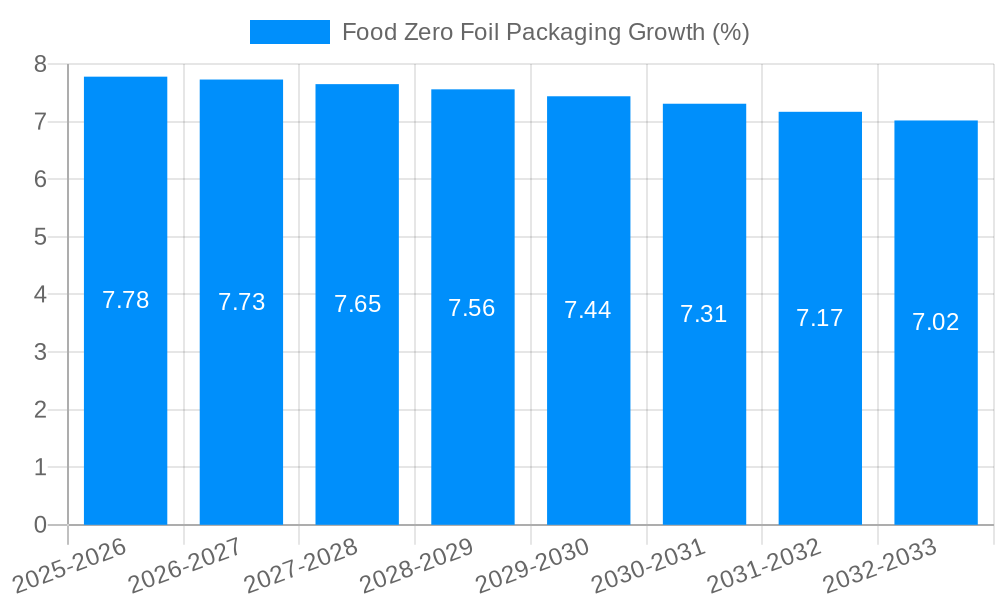

The global Food Zero Foil Packaging market is experiencing robust growth, driven by an increasing consumer demand for sustainable and eco-friendly packaging solutions. With an estimated market size of approximately USD 4,500 million in 2025, the sector is projected to expand at a Compound Annual Growth Rate (CAGR) of around 7.5% during the forecast period of 2025-2033. This upward trajectory is primarily fueled by government regulations promoting the reduction of single-use plastics, coupled with growing environmental consciousness among consumers who are actively seeking alternatives to traditional foil packaging. The convenience and perceived safety of food packaging also play a significant role, as zero foil options are increasingly being adopted across various food categories. Key market drivers include the rising adoption of advanced manufacturing technologies, the development of innovative biodegradable and recyclable materials, and strategic collaborations among key players to enhance product portfolios and expand market reach. The increasing urbanization and a burgeoning middle-class population in emerging economies further contribute to the growing demand for convenient and sustainable food packaging.

The market is segmented into Single Zero Foil and Double Zero Foil types, with the Application segment encompassing Household, Restaurant, and Supermarket sectors. The Household segment is expected to lead in terms of consumption due to the growing trend of home-cooked meals and the demand for convenient food storage solutions. Supermarkets are also witnessing a significant rise in the adoption of zero foil packaging to align with corporate sustainability goals and attract environmentally conscious shoppers. Restraints such as the higher initial cost of some zero foil materials compared to conventional options and challenges in establishing a robust recycling infrastructure in certain regions might pose hurdles. However, ongoing research and development in material science, alongside increasing economies of scale, are expected to mitigate these challenges, paving the way for widespread adoption. Companies like HTMM, Amcor PLC, and Constantia Flexibles are at the forefront, investing in innovative solutions and expanding their production capacities to meet the escalating global demand for Food Zero Foil Packaging.

This report offers an in-depth analysis of the global Food Zero Foil Packaging market, providing critical insights for stakeholders looking to understand and capitalize on this evolving sector. The study meticulously covers the Study Period: 2019-2033, with a dedicated focus on the Base Year: 2025 and its projected trajectory through the Forecast Period: 2025-2033. Historical data from 2019-2024 is also thoroughly examined to provide a robust understanding of past performance and emerging trends. We delve into the market dynamics of both Single Zero Foil and Double Zero Foil packaging types, assessing their market share, growth potential, and the factors influencing their adoption. Furthermore, the report scrutinizes the diverse application segments, including Household, Restaurant, Supermarket, and Industry, highlighting the specific needs and demands within each. With an estimated market size projected to reach multi-million unit values, this report provides essential data and strategic recommendations to navigate the opportunities and challenges within the Food Zero Foil Packaging landscape.

The global Food Zero Foil Packaging market is experiencing a paradigm shift driven by a confluence of escalating consumer awareness, stringent environmental regulations, and the inherent advantages of these innovative packaging solutions. Over the Study Period: 2019-2033, the market has witnessed a significant upward trajectory, with the Base Year: 2025 serving as a pivotal point for projected growth. XXX (e.g., advancements in material science, enhanced barrier properties, and improved recyclability) are key market insights that are shaping the future of food packaging. Consumers are increasingly demanding packaging that not only preserves food quality and extends shelf life but also minimizes environmental impact. This demand is directly translating into a greater preference for zero foil packaging options that offer superior protection against moisture, oxygen, and light without the environmental burden associated with traditional foil.

The Historical Period: 2019-2024 laid the groundwork for this evolution, with early adopters experimenting with and validating the efficacy of zero foil solutions. Now, in the Estimated Year: 2025, the market is poised for accelerated adoption as the benefits become more widely recognized and the technology matures. The Forecast Period: 2025-2033 is expected to see substantial expansion as governments worldwide implement stricter sustainability mandates and consumers become more discerning in their purchasing decisions. This shift is not merely a trend; it represents a fundamental reorientation of the packaging industry towards a more responsible and sustainable future. The demand for convenience, coupled with a growing consciousness about personal health and the planet, are the twin engines driving this transformative change. As the market matures, we anticipate further innovations in material composition, design, and manufacturing processes, further solidifying the position of zero foil packaging as a cornerstone of modern food preservation. The increasing focus on circular economy principles will also play a crucial role, with manufacturers investing in research and development to create truly recyclable or compostable zero foil solutions. This proactive approach to sustainability is not only a response to regulatory pressures but also a strategic imperative for long-term market relevance and competitive advantage.

The surge in demand for Food Zero Foil Packaging is underpinned by a powerful set of driving forces that are reshaping the food industry's approach to preservation and presentation. Foremost among these is the escalating global environmental consciousness. Consumers, armed with readily available information on the detrimental effects of traditional packaging waste, are actively seeking out brands that demonstrate a commitment to sustainability. This ethical consumerism translates directly into market preference for solutions like zero foil packaging, which are perceived as more eco-friendly alternatives. Regulatory bodies worldwide are also playing a significant role. A growing number of governments are enacting stricter policies aimed at reducing plastic waste and promoting the use of recyclable or biodegradable materials. These regulations, often implemented with phased timelines, create a strong impetus for manufacturers and food producers to transition towards sustainable packaging options, with zero foil emerging as a viable and effective choice.

Furthermore, the inherent benefits of zero foil packaging in terms of product protection and shelf-life extension are undeniable. These advanced materials offer excellent barrier properties against moisture, oxygen, and light, crucial factors in maintaining food freshness, flavor, and nutritional value. This not only reduces food waste but also enhances consumer satisfaction by ensuring product quality upon arrival. The pursuit of premium product presentation also contributes to the growth of zero foil. The sophisticated aesthetic appeal and tactile qualities of many zero foil materials allow brands to differentiate themselves on store shelves, aligning with consumer expectations for high-quality, modern packaging. The economic viability of zero foil packaging is also improving as economies of scale are achieved and manufacturing processes become more efficient, making it a competitive alternative to traditional packaging in the long run.

Despite the promising growth trajectory of the Food Zero Foil Packaging market, several challenges and restraints could temper its widespread adoption and overall expansion. A significant hurdle remains the initial cost of implementation. While long-term benefits are evident, the upfront investment required for new machinery, research and development, and the retooling of existing production lines can be substantial for many food manufacturers, particularly smaller enterprises. This economic barrier can slow down the transition from established, cost-effective traditional packaging solutions.

Another considerable challenge lies in consumer education and perception. While awareness of sustainability is growing, there can still be a lack of understanding regarding the specific benefits and functionalities of zero foil packaging. Consumers may equate "foil-free" with a perceived reduction in barrier properties or protective capabilities, leading to apprehension about food safety and quality. Overcoming these ingrained perceptions requires concerted marketing efforts and clear communication from brands about the efficacy of these new materials.

The complexity of the supply chain and recycling infrastructure also presents a restraint. For zero foil packaging to truly achieve its environmental potential, robust and widely accessible recycling or composting facilities are essential. The absence of a standardized and efficient end-of-life management system for many of these novel materials can lead to confusion among consumers and ultimately contribute to them ending up in landfills, negating the intended environmental benefits. Furthermore, regulatory inconsistencies across different regions can create complexities for global food companies attempting to standardize their packaging strategies. While some countries are at the forefront of promoting sustainable packaging, others may lag, leading to fragmented compliance requirements and increased operational costs. Finally, technical limitations in certain specialized applications might still require the unique properties offered by traditional foil in specific high-barrier or high-temperature scenarios, limiting the immediate applicability of zero foil in all food packaging segments.

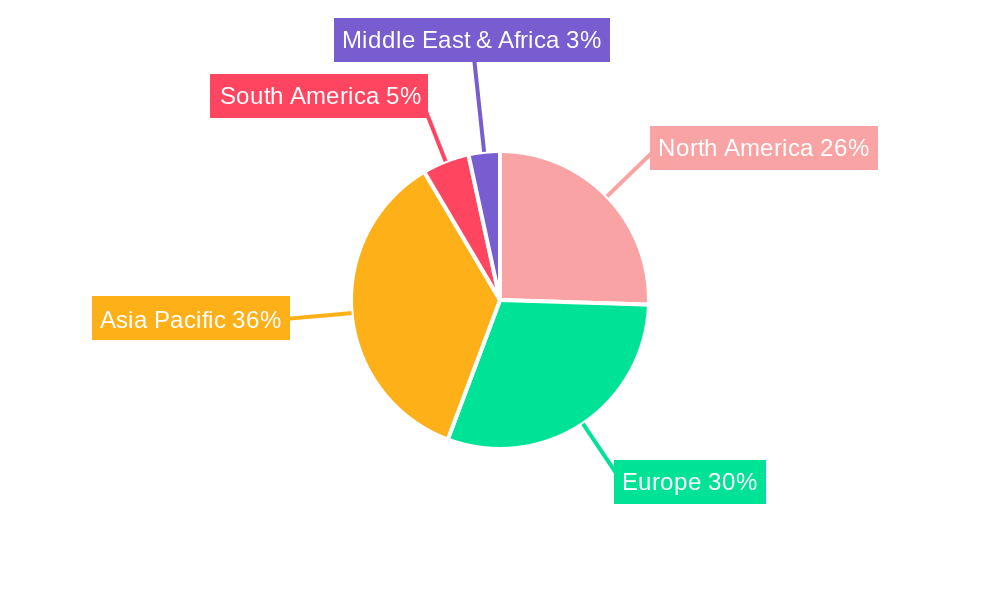

The global Food Zero Foil Packaging market is anticipated to witness significant dominance from North America and Europe in terms of market share and growth, driven by a confluence of strong consumer demand for sustainable products, stringent environmental regulations, and a well-established food processing industry. These regions have consistently been at the forefront of environmental consciousness, with consumers actively seeking out eco-friendly alternatives and willing to pay a premium for them. The presence of leading packaging manufacturers and food brands in these regions also fosters innovation and drives the adoption of advanced packaging technologies. Furthermore, the robust regulatory frameworks in both North America and Europe, focused on waste reduction and the promotion of circular economy principles, create a fertile ground for the growth of zero foil packaging. Initiatives such as bans on single-use plastics and incentives for adopting sustainable packaging materials directly encourage manufacturers to invest in and implement zero foil solutions.

Within these dominant regions, the Supermarket segment is expected to exhibit the most substantial growth and market penetration. Supermarkets, as major retailers of a vast array of food products, are under immense pressure from both consumers and regulatory bodies to offer sustainable packaging options. They act as a crucial touchpoint for consumers and are often the first to adopt and promote new packaging trends. The sheer volume of products they handle necessitates efficient, safe, and increasingly eco-conscious packaging solutions. The Household application segment also represents a significant market, driven by direct consumer purchasing decisions and the growing awareness of at-home environmental impact. As zero foil packaging becomes more accessible and its benefits are more widely communicated, households will increasingly opt for these options for their everyday food storage and preparation needs.

The Single Zero Foil type is projected to hold a larger market share, particularly in the initial stages of market development. This is primarily due to its comparative cost-effectiveness and ease of integration into existing production lines for many applications. Single zero foil packaging offers a viable entry point for businesses looking to transition towards more sustainable options without a complete overhaul of their infrastructure. However, the Double Zero Foil segment is expected to witness rapid growth as technological advancements lead to improved performance, barrier properties, and cost efficiencies. Double zero foil, with its enhanced protective capabilities, will become increasingly critical for products requiring superior preservation and extended shelf life, further solidifying its position in premium food packaging. The interplay between these segments and regions will be crucial in shaping the overall market dynamics, with continuous innovation and adaptation being key to sustained success.

Several key growth catalysts are propelling the Food Zero Foil Packaging industry forward. The relentless pursuit of sustainability by consumers, driven by increasing environmental awareness and a desire to reduce their ecological footprint, is a primary driver. This ethical consumption trend is pushing food manufacturers to adopt eco-friendly packaging solutions. Simultaneously, stringent government regulations globally, aimed at curbing plastic waste and promoting recyclable materials, are creating a strong impetus for the adoption of zero foil alternatives. The inherent advantages of zero foil in terms of superior barrier properties, extending food shelf life, and reducing food waste also contribute significantly to its growth. Furthermore, continuous innovation in material science and manufacturing technologies is making zero foil packaging more cost-effective and performant, broadening its applicability across a wider range of food products.

This comprehensive report provides an indispensable resource for understanding the intricate landscape of the Food Zero Foil Packaging market. We have meticulously analyzed the market dynamics from 2019 to 2033, with a keen focus on the Base Year: 2025 and its projected trajectory through the Forecast Period: 2025-2033. The report delves into the nuances of both Single Zero Foil and Double Zero Foil types, alongside an exhaustive examination of their application in Household, Restaurant, Supermarket, and Industry sectors. By providing an in-depth look at the driving forces, challenges, and key regions poised for dominance, this report equips stakeholders with the strategic intelligence needed to navigate this rapidly evolving industry. The inclusion of a detailed list of leading players and significant developments further enhances its value, offering a holistic view of the market's present state and future potential, ultimately empowering informed decision-making for growth and innovation.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include HTMM, Amcor PLC, Constantia Flexibles, Novelis, Raviraj Foils, Ampco, Symetal, Aliberico S.L.U., Coppice Alupack, Eurofoil, Reynolds Group Holdings, KM Packaging, Shanghai Kemao Medical Packing Co., Ltd., YIDIAN Holding Group, Henan Mingtai Al.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Food Zero Foil Packaging," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Food Zero Foil Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.