1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive ADAS?

The projected CAGR is approximately 17.8%.

Automotive ADAS

Automotive ADASAutomotive ADAS by System Type (Adaptive Cruise Control (ACC), Automatic Emergency Braking (AEB), Lane Departure Warning (LDW), Blind Spot Detection (BSD)., Forward Collision Warning (FCW), Driver Monitoring System (DMS), Others), by Sensor Type (Radar Sensors, Camera Sensors, LiDAR Sensors, Ultrasonic Sensors, Infrared Sensors, Others), by LOA (L1, L2, L3, L4, L5), by Sales Channel (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV)), by Vehicle Type (OEM, Sales Channel), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The Global Automotive ADAS Market is exhibiting robust expansion, valued at an estimated $42.9 billion in 2024. Projections indicate a substantial growth trajectory, driven by a compound annual growth rate (CAGR) of 17.8% through the forecast period. This significant growth is underpinned by several critical demand drivers and macro tailwinds. Regulatory mandates, particularly those emphasizing occupant and pedestrian safety, are a primary catalyst, compelling automotive manufacturers to integrate advanced driver-assistance systems (ADAS) as standard features. Furthermore, increasing consumer awareness and demand for enhanced safety, convenience, and comfort features in modern vehicles are significantly contributing to market uptake. Technological advancements in sensor fusion, artificial intelligence, and machine learning algorithms are continually improving the performance and reliability of ADAS, making them more appealing to a broader consumer base.

The market’s forward-looking outlook points towards an accelerated adoption of higher levels of autonomy (L2+ to L3), characterized by sophisticated systems like Adaptive Cruise Control (ACC) and Automatic Emergency Braking (AEB). The integration of ADAS into software-defined vehicles is also a pivotal trend, enabling over-the-air updates and feature enhancements. Regional growth dynamics highlight Asia Pacific as a rapidly expanding market, fueled by burgeoning automotive production and evolving safety regulations, while mature markets like Europe and North America continue to lead in innovation and premium segment penetration. The sustained investment in sensor technologies, including the LiDAR Sensor Market and Radar Sensor Market, alongside the development of advanced perception software, will be crucial in shaping the future landscape of the Automotive ADAS Market. The strategic interplay between OEMs, Tier 1 suppliers, and technology firms is intensifying, fostering a competitive yet collaborative environment focused on innovation and scalability. The growing emphasis on integrated systems that enhance the overall driving experience while prioritizing safety remains a core objective for market participants, pushing the boundaries of what is possible in automotive intelligence.

Within the highly segmented Automotive ADAS Market, the 'System Type' category represents the most dominant segment by revenue share, with the Automatic Emergency Braking (AEB) sub-segment emerging as a cornerstone of modern automotive safety. This dominance is primarily attributable to its direct impact on collision avoidance and mitigation, which aligns with stringent global safety regulations and consumer priorities. AEB systems utilize various sensors, including radar, cameras, and sometimes lidar, to detect potential forward collisions with vehicles, pedestrians, or cyclists, automatically applying brakes if the driver fails to respond in time. This proactive safety measure has become a key criterion for vehicle safety ratings from organizations such as Euro NCAP and the National Highway Traffic Safety Administration (NHTSA), effectively making it a mandatory feature for new vehicle models aiming for top safety scores.

Key players like Robert Bosch Gmbh, Continental Ag, and Denso Corporation are at the forefront of developing and supplying advanced AEB systems. Their comprehensive portfolios often include sophisticated sensor suites, electronic control units (ECUs), and proprietary algorithms that enhance system accuracy and reduce false positives. The market share of AEB is not only growing due to regulatory impetus but also due to its foundational role in enabling higher levels of autonomous driving. As vehicles evolve towards L2+ and L3 autonomy, AEB systems become integrated components of more complex active safety platforms. Other significant sub-segments within System Type, such as Lane Departure Warning (LDW), Blind Spot Detection (BSD), and Adaptive Cruise Control (ACC), also contribute substantially to the Automotive ADAS Market, often offered in bundled safety packages. However, AEB's critical role in preventing accidents places it at the pinnacle of revenue generation and strategic importance. The continued advancements in sensor technology, including the increasingly sophisticated Radar Sensor Market and the precision offered by the LiDAR Sensor Market, are directly enhancing the effectiveness and reliability of the Automatic Emergency Braking System Market. Furthermore, the integration of these advanced systems into the broader Automotive Electronics Market is driving innovation and cost-efficiency, ensuring AEB's sustained leadership within the Automotive ADAS Market's system type segmentation.

The Automotive ADAS Market is primarily propelled by a confluence of stringent regulatory mandates and rapid technological advancements. A significant driver is the global push for enhanced vehicle safety, quantified by evolving safety ratings from bodies like Euro NCAP and NHTSA. For instance, Euro NCAP’s updated protocols increasingly reward vehicles with robust Automatic Emergency Braking System Market capabilities, pedestrian and cyclist detection, and effective Lane Departure Warning (LDW) systems. This regulatory pressure directly incentivizes OEMs to integrate these advanced functionalities to achieve higher safety scores, thereby bolstering market adoption across various vehicle segments. The implementation of minimum safety standards in key regions has established a foundational demand for ADAS solutions.

Technological innovation, particularly in sensor technology, serves as another critical driver. Progress in Radar Sensor Market technology, offering improved range, resolution, and all-weather performance, and the miniaturization and cost reduction within the LiDAR Sensor Market, are enabling more accurate and reliable perception systems. These advancements enhance the capability of ADAS to precisely detect, classify, and track objects in complex driving environments, which is fundamental for systems ranging from Blind Spot Detection (BSD) to advanced L3 autonomous functionalities. Moreover, the integration of sophisticated artificial intelligence and machine learning algorithms is transforming raw sensor data into actionable insights, facilitating more intelligent decision-making by the ADAS. This computational power is a prerequisite for the progression of the Autonomous Driving Market. The rising demand within the Passenger Vehicles Market for premium safety features and driver comfort also acts as a powerful market stimulant. Consumers are increasingly valuing features like adaptive cruise control, parking assist, and the Driver Monitoring System Market in their purchasing decisions, moving ADAS from a luxury option to a mainstream expectation. Conversely, a primary constraint remains the high development and integration costs for advanced L3 and L4 systems, which can limit broader market penetration, particularly in cost-sensitive vehicle segments. Furthermore, the burgeoning complexity of these systems necessitates robust solutions in the Automotive Cybersecurity Market to prevent vulnerabilities, adding another layer of cost and developmental challenge.

The Automotive ADAS Market is characterized by intense competition among established Tier 1 suppliers, technology giants, and specialized startups, all vying for market share through innovation and strategic partnerships.

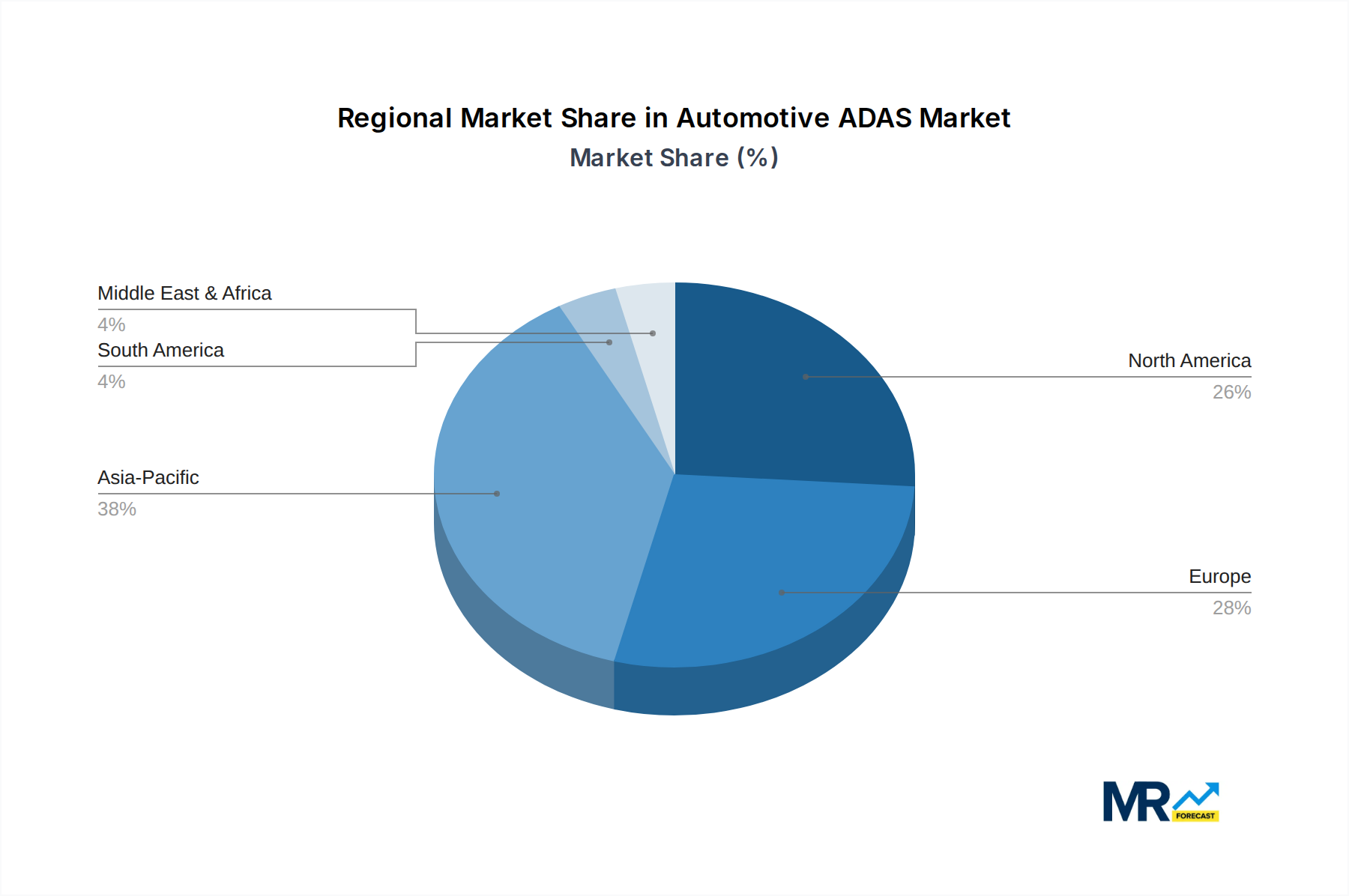

The global Automotive ADAS Market demonstrates significant regional disparities in adoption and growth, influenced by varying regulatory landscapes, consumer preferences, and technological infrastructures. Asia Pacific currently stands as the dominant region in terms of market share and is also projected to be the fastest-growing market. This growth is primarily fueled by major automotive manufacturing hubs in China, Japan, and South Korea, coupled with increasing consumer demand for advanced features in the Passenger Vehicles Market and evolving safety regulations. Governments in this region are actively promoting ADAS adoption to curb road fatalities, creating a robust demand environment.

Europe represents a highly mature market, characterized by early adoption and stringent safety mandates from organizations like Euro NCAP, which has significantly driven the penetration of Automatic Emergency Braking System Market, Lane Departure Warning (LDW), and Adaptive Cruise Control (ACC). The region maintains a strong focus on innovation and the integration of ADAS into premium and luxury vehicle segments, acting as a benchmark for safety standards globally. North America holds a substantial market share, driven by a technologically advanced automotive industry and high consumer awareness regarding vehicle safety and convenience features. Demand for sophisticated L2 and L2+ systems is robust, with significant investment directed towards the development and deployment of Autonomous Driving Market technologies.

In contrast, regions within the Middle East & Africa and South America are emerging markets for ADAS. While penetration rates are currently lower, increasing urbanization, rising disposable incomes, and growing awareness of safety benefits are expected to drive gradual adoption. However, these regions face challenges related to infrastructure, regulatory frameworks, and affordability, which may temper the pace of growth compared to developed economies. The overall Automotive ADAS Market is expected to witness continued expansion globally, with regional strategies often tailored to address specific market characteristics, such as vehicle parc composition, economic conditions, and local regulatory environments.

The Automotive ADAS Market relies heavily on complex global supply chains for its components, impacting export and trade flows significantly. Major trade corridors for high-value ADAS components, such as radar sensors, camera modules, LiDAR units, and electronic control units (ECUs), typically flow from advanced manufacturing economies in Asia (Japan, South Korea, China) and Europe (Germany, France) to assembly plants and Tier 1 suppliers globally. Germany and Japan are leading exporters of advanced automotive electronics and sensors, while China and the United States are primary importers, driven by their vast automotive production and demand for sophisticated vehicle features.

Tariff and non-tariff barriers can profoundly impact the cross-border volume and cost structure within the Automotive ADAS Market. Historically, trade tensions, such as those between the U.S. and China, have led to increased tariffs on specific Automotive Electronics Market and semiconductor components. These tariffs can escalate production costs for OEMs and suppliers, potentially slowing down the integration of ADAS features into more affordable vehicle segments. Regional trade agreements, such as the EU's single market, NAFTA/USMCA in North America, and various ASEAN agreements, generally facilitate smoother trade flows by reducing or eliminating duties and harmonizing technical standards. However, differing regulatory certification requirements across countries can still act as non-tariff barriers, necessitating customized solutions and testing for global market access.

Supply chain disruptions, as experienced during recent global events, have also highlighted the vulnerability of this complex trade network, leading to increased efforts towards regionalizing production or diversifying sourcing strategies. The strategic importance of ADAS components for vehicle safety and future mobility means that governments and industry players are keenly observing trade policies to ensure uninterrupted access to critical technologies, impacting global investment and manufacturing footprint decisions.

Investment and funding activity within the Automotive ADAS Market has been robust over the past 2-3 years, reflecting the industry's commitment to advancing vehicle autonomy and safety. Mergers and acquisitions (M&A) have been a prominent feature, with larger Tier 1 suppliers and technology conglomerates acquiring specialized firms to bolster their ADAS capabilities. A notable example is Intel's acquisition of Mobileye, solidifying its position in computer vision and ADAS chipsets. This trend of consolidation aims to integrate diverse technologies, from advanced sensors to software platforms, under larger entities capable of offering comprehensive solutions.

Venture capital and private equity funding have seen significant deployment into startups focused on next-generation ADAS technologies. Sub-segments attracting the most capital include solid-state LiDAR Sensor Market development, high-resolution imaging Radar Sensor Market systems, and AI-driven perception software. Companies developing new approaches to sensor fusion, predictive analytics, and high-performance computing platforms for L3/L4 autonomous driving are particularly favored. For instance, numerous startups working on novel LiDAR technologies have secured substantial funding rounds to scale their production and accelerate R&D efforts aimed at reducing cost and improving performance, crucial for broader automotive integration. Furthermore, the increasing complexity and connectivity of ADAS systems have also driven investment into the Automotive Cybersecurity Market, with startups specializing in secure vehicle architectures and data protection attracting significant capital.

Strategic partnerships between traditional automotive OEMs and technology companies are also flourishing. These collaborations often focus on co-developing Autonomous Driving Market software stacks, shared mapping initiatives, and joint ventures for testing and deploying highly automated vehicles. These alliances are crucial for sharing the immense R&D burden and accelerating time-to-market for advanced ADAS functionalities. The continuous influx of capital underscores the long-term potential of the Automotive ADAS Market, with investors keen on enabling the next generation of safe and intelligent mobility solutions, particularly in areas that enhance the capabilities of the Automatic Emergency Braking System Market and other critical active safety features.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 17.8%.

Key companies in the market include Continental Ag, Delphi Automotive PLC, Robert Bosch Gmbh, Aisin Seiki Co. Ltd., Denso Corporation, Trw Automotive Holdings Corp., Mobileye NV, .

The market segments include System Type, Sensor Type, LOA, Sales Channel, Vehicle Type.

The market size is estimated to be USD 42.9 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Automotive ADAS," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive ADAS, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.