1. What is the projected Compound Annual Growth Rate (CAGR) of the Connected Car?

The projected CAGR is approximately 19.8%.

Connected Car

Connected CarConnected Car by Type (Embedded solutions, Integrated solutions, Tethered solutions, World Connected Car Production ), by Application (Infotainment, Navigation, Telematics, World Connected Car Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

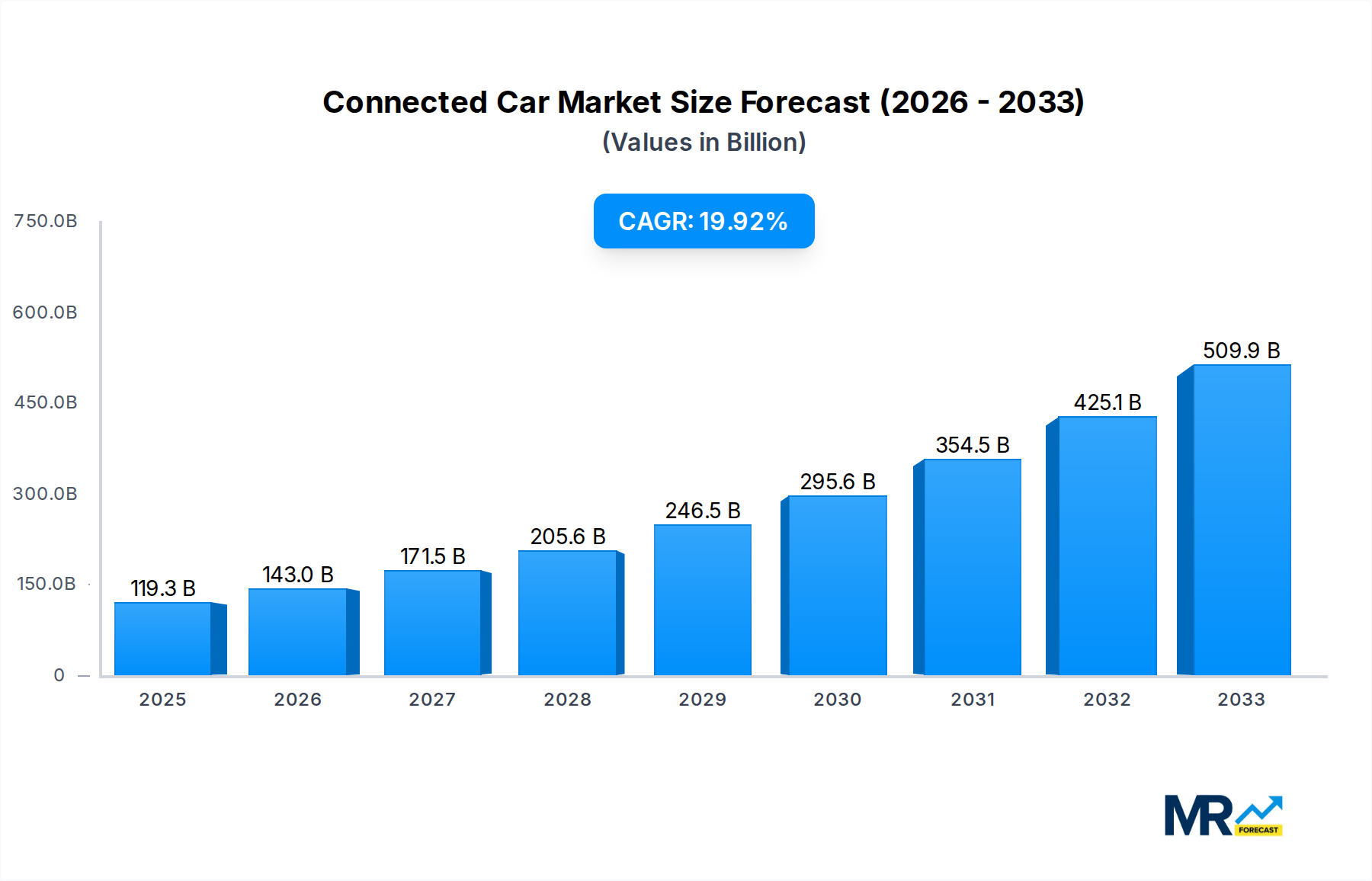

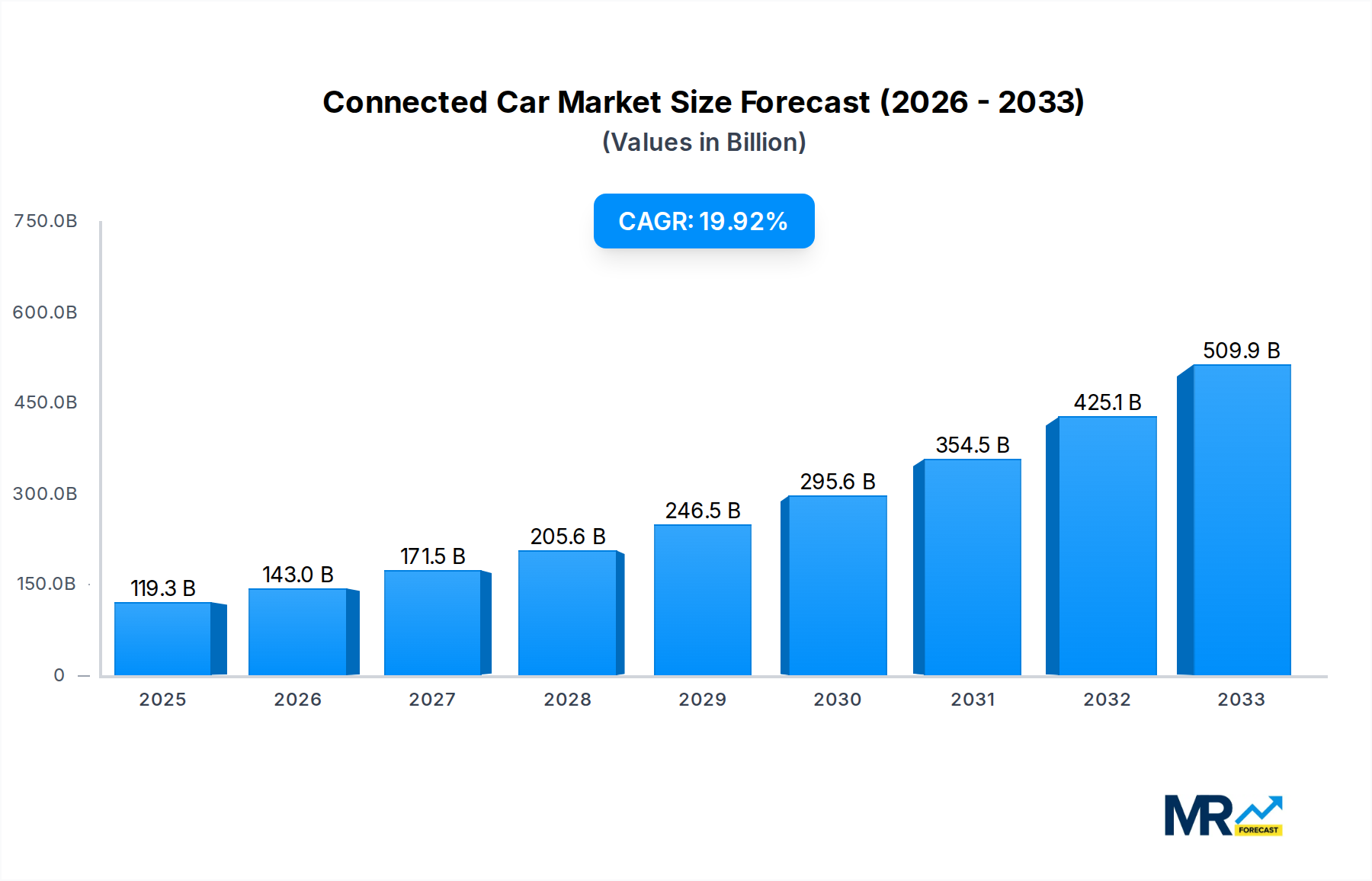

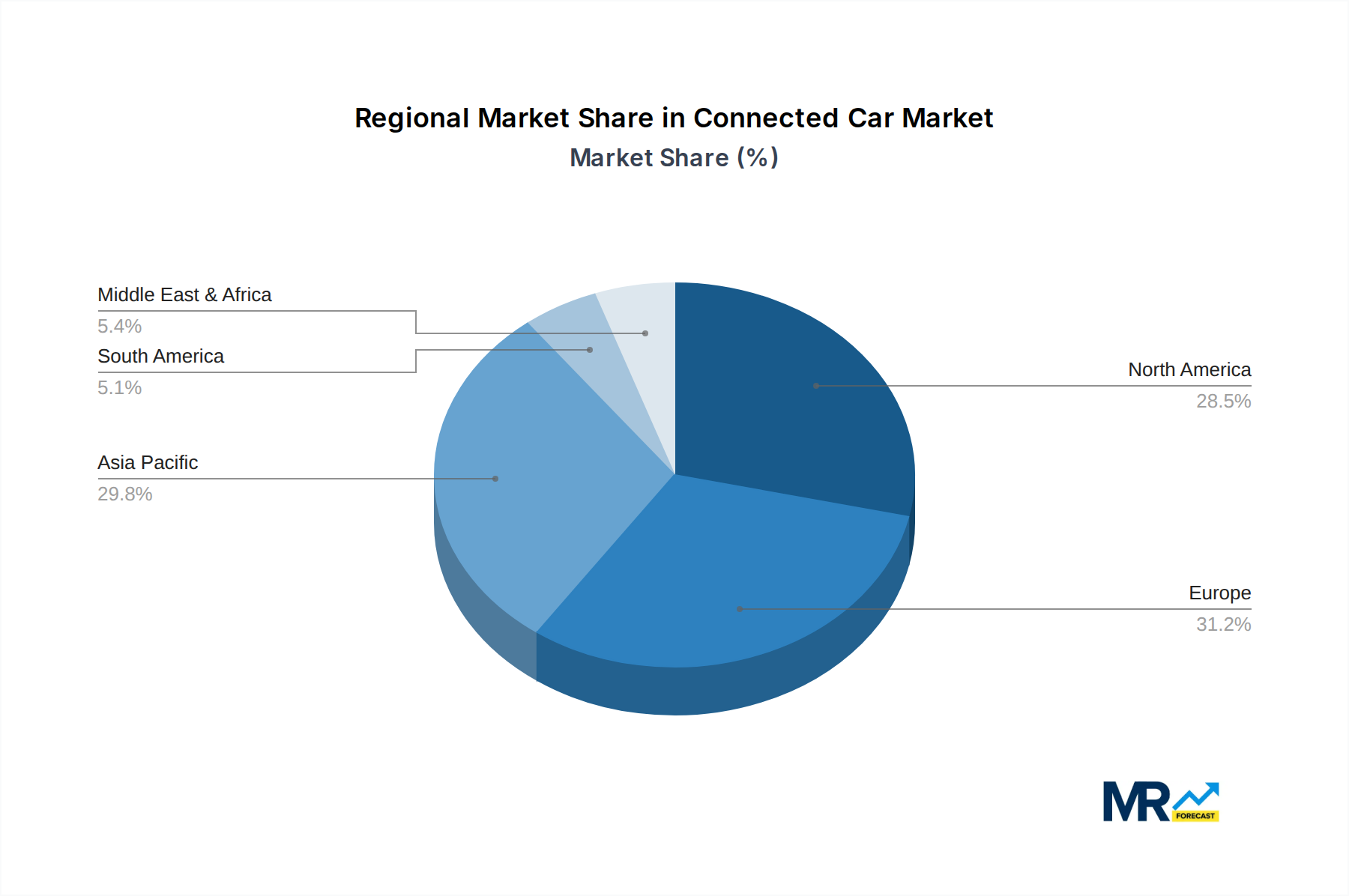

The global connected car market is experiencing robust growth, projected to reach approximately $119.27 billion in the base year 2025 and expanding at an impressive Compound Annual Growth Rate (CAGR) of 19.8% through 2033. This surge is fueled by an escalating demand for enhanced vehicle safety, improved driving experiences, and the integration of advanced digital technologies. The increasing adoption of features like real-time traffic updates, remote diagnostics, over-the-air software updates, and sophisticated infotainment systems are key drivers. Furthermore, the growing emphasis on autonomous driving capabilities and the development of smart city infrastructure are creating new avenues for connected car services, contributing significantly to market expansion. Emerging economies, particularly in the Asia Pacific region, are poised to become major growth centers due to rapid urbanization, rising disposable incomes, and government initiatives promoting smart mobility solutions.

The market is segmented into various types of solutions, including embedded, integrated, and tethered systems, catering to diverse automotive manufacturing strategies and consumer preferences. Applications within the connected car ecosystem are broadly categorized into infotainment, navigation, and telematics, each offering unique value propositions. Infotainment systems are evolving to provide seamless connectivity to personal devices and cloud-based services, while advanced navigation solutions are integrating real-time data for optimized routing. Telematics is playing a crucial role in fleet management, vehicle health monitoring, and the enablement of new insurance models. Despite the immense growth potential, potential restraints such as data security concerns, privacy issues, and the high cost of implementing advanced connectivity features in all vehicle segments need to be addressed to ensure sustained market penetration and consumer trust. However, continuous innovation and strategic partnerships among automotive manufacturers, technology providers, and telecommunication companies are expected to overcome these challenges, driving the connected car market towards a transformative future.

This comprehensive report delves deep into the dynamic and rapidly evolving Connected Car market, projecting its valuation to surpass an astounding $1.2 trillion by 2033. With a meticulous Study Period spanning from 2019 to 2033, the analysis provides an in-depth understanding of market trajectories, underpinned by robust data from the Base Year of 2025 and insightful projections for the Estimated Year of 2025. The Forecast Period, from 2025 to 2033, is meticulously examined, building upon the foundation of the Historical Period between 2019 and 2024. This report is an indispensable resource for stakeholders seeking to navigate the complexities and capitalize on the immense opportunities within the connected automotive ecosystem.

XXX, the connected car market is on an unprecedented growth trajectory, driven by an insatiable consumer demand for enhanced in-vehicle experiences and the automotive industry's strategic pivot towards software-defined vehicles. Over the historical period of 2019-2024, we witnessed the nascent stages of widespread adoption, with early investments primarily focused on basic connectivity features like GPS navigation and rudimentary telematics. The base year of 2025 marks a significant inflection point, with the market exhibiting a more mature understanding of consumer needs and technological capabilities. The projected growth from 2025 to 2033 is staggering, fueled by advancements in artificial intelligence, 5G connectivity, and the burgeoning ecosystem of third-party applications. Consumers are no longer content with just getting from point A to point B; they expect their vehicles to be seamless extensions of their digital lives, offering personalized infotainment, proactive maintenance alerts, and advanced safety features that contribute to a more intuitive and secure driving experience. The market is increasingly segmenting, with a clear distinction emerging between the more accessible tethered solutions and the increasingly sophisticated embedded and integrated systems that promise a richer, more immersive user interface. The proliferation of over-the-air (OTA) updates is revolutionizing vehicle ownership, enabling manufacturers to continuously improve functionality and introduce new features post-purchase, thereby extending vehicle lifespan and customer loyalty. Furthermore, the rise of autonomous driving technologies is intrinsically linked to the connected car paradigm, as advanced sensor fusion, real-time data processing, and V2X (Vehicle-to-Everything) communication are paramount for safe and efficient self-driving operations. This interconnectedness extends beyond the vehicle itself, fostering a broader smart city infrastructure where connected cars play a pivotal role in traffic management, public safety, and resource optimization. The sheer volume of data generated by connected vehicles is also creating new revenue streams for automakers and third-party providers, from personalized advertising to usage-based insurance models. The competitive landscape is becoming increasingly fierce, with traditional automotive giants forging strategic alliances with tech behemoths to leverage their expertise in software development and cloud computing, ensuring that the connected car is not just a mode of transport but a sophisticated, intelligent, and indispensable component of modern life. The projected market value reaching over $1.2 trillion by 2033 underscores the transformative impact of this technological revolution on the automotive industry and beyond.

The accelerated adoption and expansion of the connected car market are propelled by a confluence of compelling factors, fundamentally reshaping the automotive landscape. At the forefront is the escalating consumer demand for personalized and intuitive in-vehicle experiences. Modern drivers and passengers expect seamless integration of their digital lives into their commutes, demanding sophisticated infotainment systems, advanced navigation capabilities, and instant access to a plethora of applications. This desire for a connected lifestyle is a primary catalyst, pushing manufacturers to invest heavily in technologies that deliver on these expectations. Furthermore, the rapid advancements in wireless communication technologies, particularly the rollout of 5G networks, are instrumental. 5G’s higher bandwidth, lower latency, and increased capacity are crucial for supporting the data-intensive applications inherent in connected cars, from real-time traffic updates and high-definition streaming to enabling critical V2X (Vehicle-to-Everything) communication for enhanced safety and traffic efficiency. The automotive industry's strategic shift towards software-defined vehicles also plays a pivotal role. Manufacturers are recognizing the long-term revenue potential and customer engagement opportunities offered by software-centric architectures, enabling over-the-air (OTA) updates for continuous improvement and feature additions, thereby fostering a subscription-based revenue model and extending the relevance of vehicles long after their initial purchase. Government initiatives and regulatory frameworks promoting vehicle safety and data-driven urban planning are also indirectly driving connectivity. The push for intelligent transportation systems (ITS) and smart cities necessitates connected vehicles to effectively communicate with infrastructure and other road users, ultimately leading to improved traffic flow, reduced emissions, and enhanced public safety. Finally, the burgeoning ecosystem of third-party developers and service providers is continuously innovating, creating a vibrant marketplace of applications and services that enrich the connected car experience, ranging from advanced diagnostics and predictive maintenance to in-car commerce and personalized entertainment.

Despite the undeniable growth potential, the connected car market faces significant hurdles and restraints that could temper its expansion. Foremost among these is the paramount concern of cybersecurity. The increasing connectivity of vehicles makes them vulnerable to cyberattacks, potentially compromising sensitive personal data, vehicle control systems, and even passenger safety. The sheer volume and interconnectedness of data generated necessitate robust security protocols, which are complex and costly to implement and maintain. Following closely is the issue of data privacy. Connected cars collect vast amounts of personal information, including driving habits, location data, and even in-car conversations. Ensuring transparent data collection practices, obtaining explicit user consent, and adhering to evolving data protection regulations (such as GDPR and CCPA) are critical challenges for automakers and service providers. The high cost of implementation for advanced connectivity features and the associated hardware and software can also be a significant restraint, particularly for mass-market vehicles. This can lead to a price premium that may deter a segment of price-sensitive consumers, limiting the widespread adoption of the most sophisticated connected solutions. Furthermore, the lack of standardization across different vehicle platforms and operating systems creates interoperability issues. This fragmentation can hinder the seamless integration of third-party applications and services, leading to a fragmented user experience and increased development costs for service providers. The regulatory landscape, while often supportive, can also be a restraint due to its evolving nature and the potential for new mandates that require significant investment and adaptation from manufacturers. The infrastructure for reliable high-speed connectivity, especially in rural or remote areas, also remains a challenge, limiting the full potential of data-intensive applications. Finally, consumer trust and awareness regarding the benefits and security of connected car technologies are still developing. Overcoming skepticism and educating consumers about the value proposition and safety measures are crucial for sustained growth.

The global Connected Car market is poised for significant dominance by North America, particularly the United States, and the Embedded Solutions segment, as well as the Infotainment application. These regions and segments are at the forefront of technological adoption, innovation, and consumer demand.

North America (United States): The United States stands as a titan in the connected car arena due to several key drivers.

Embedded Solutions (Type Segment): This segment is projected to dominate due to its inherent advantages and increasing integration into vehicle architecture.

Infotainment (Application Segment): The demand for enhanced in-car entertainment and information services is a primary driver for this segment's dominance.

The synergy between a technologically progressive region like North America, the robust foundation provided by embedded solutions, and the consumer-facing appeal of infotainment applications creates a powerful nexus that will likely define the dominant forces in the global connected car market throughout the forecast period.

Several potent growth catalysts are fueling the expansion of the connected car industry. The increasing integration of AI and machine learning enables predictive maintenance, personalized user experiences, and enhanced safety features. The ubiquitous rollout of 5G technology is a critical enabler, providing the necessary bandwidth and low latency for real-time data exchange, V2X communication, and advanced in-car services. Furthermore, the growing consumer appetite for seamless digital integration within their vehicles, demanding advanced infotainment, navigation, and connectivity options, is a significant driver. The evolving automotive ecosystem, with manufacturers embracing software-defined vehicles and over-the-air updates, unlocks new revenue streams and enhances customer loyalty.

This comprehensive report offers an unparalleled deep dive into the $1.2 trillion Connected Car market, spanning the historical period of 2019-2024 and projecting its trajectory through 2033. It provides granular analysis across key segments like Embedded, Integrated, and Tethered solutions, alongside critical applications such as Infotainment, Navigation, and Telematics. The report meticulously examines industry developments, identifies pivotal growth catalysts like AI integration and 5G deployment, and details the driving forces behind this revolution, including evolving consumer demands and strategic automotive industry shifts. Furthermore, it critically assesses the challenges and restraints, such as cybersecurity concerns and data privacy, that stakeholders must navigate. With detailed insights into leading players like BMW, Ford Motor, Google, and Bosch, and highlighting dominant regions like North America, this report is an essential strategic roadmap for understanding the future of automotive mobility and capitalizing on its immense opportunities.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 19.8%.

Key companies in the market include Alpine Electronics, BMW, Delphi Automotive, Ford Motor, NXP Semiconductors, Audi, Bosch, Continental, Google, Mercedes-Benz, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Connected Car," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Connected Car, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.