1. What is the projected Compound Annual Growth Rate (CAGR) of the Viral and Non Viral Vector Manufacturing?

The projected CAGR is approximately 21%.

Viral and Non Viral Vector Manufacturing

Viral and Non Viral Vector ManufacturingViral and Non Viral Vector Manufacturing by Type (Viral Vector, Non-viral Vector), by Application (Gene Therapy, Vaccinology, Cell Therapy, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

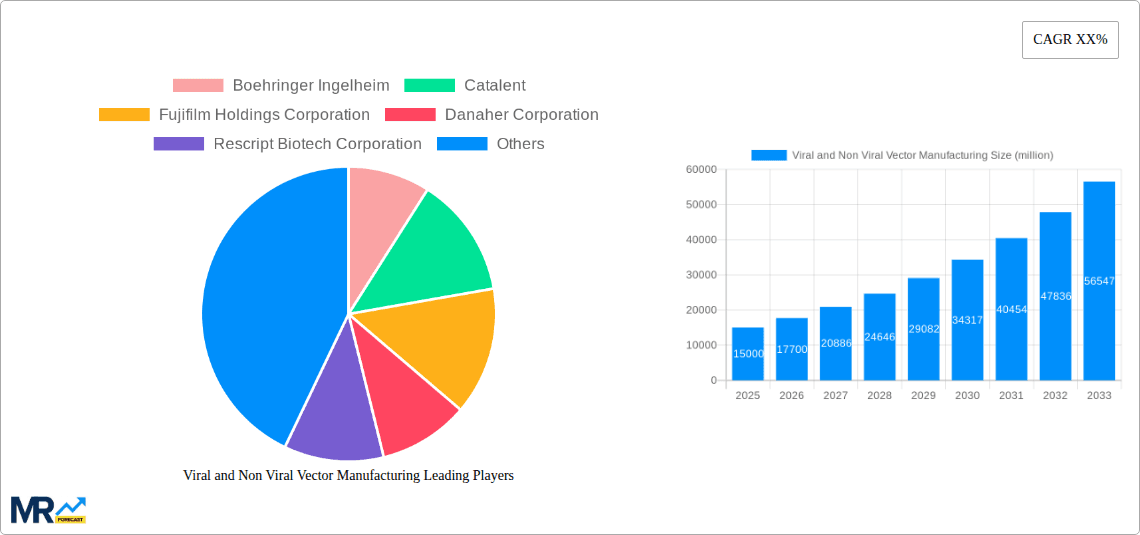

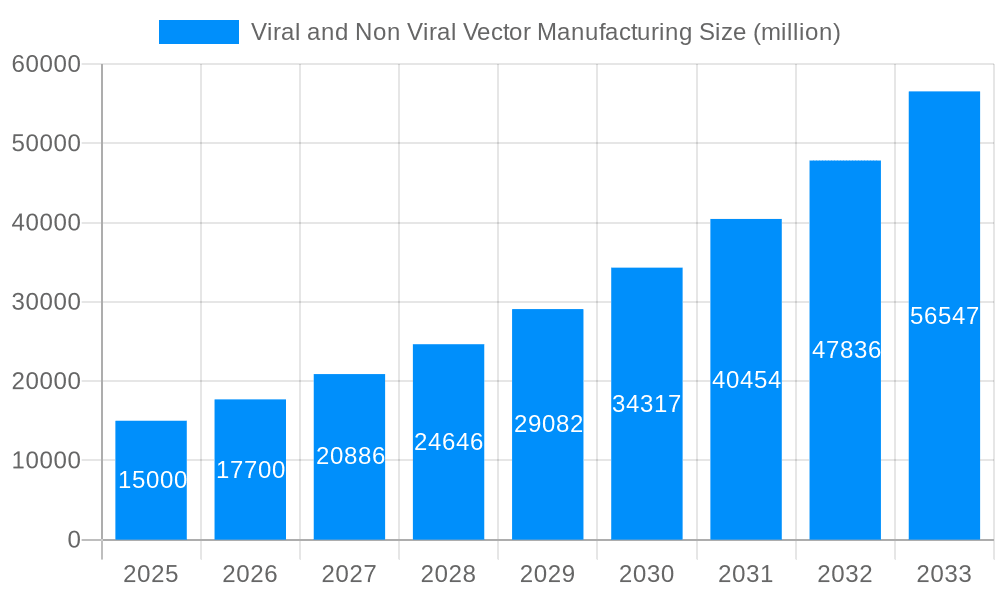

The global Viral and Non-Viral Vector Manufacturing market is set for significant expansion, driven by the escalating demand for advanced gene therapies and vaccines. The market is projected to reach $10.3 billion in 2025 and grow at a CAGR of 21% through 2033. This growth is attributed to the rising incidence of genetic disorders, advancements in gene-editing technologies, and accelerated development of novel therapeutics. Key players, including Boehringer Ingelheim, Catalent, Moderna, and Thermo Fisher Scientific, are investing heavily in R&D, further fueling market growth. The expanding pipeline of gene therapy and vaccine candidates in clinical trials, coupled with increasing regulatory approvals, are major catalysts for the manufacturing sector.

Key market trends include the increasing adoption of adeno-associated virus (AAV) vectors for gene therapy and the expanded use of mRNA and viral vectors in vaccine development, particularly in response to global health needs. Technological innovations in manufacturing, such as enhanced purification and scalable production, are addressing critical bottlenecks and contributing to market growth. While challenges like high production costs, stringent regulations, and the need for specialized expertise exist, strategic collaborations, investments from companies like Lonza Group AG and Fujifilm Holdings Corporation, and increased manufacturing capacity demonstrate a strong commitment to meeting rising demand. The market's segmentation into viral (e.g., Adenovirus, Lentivirus) and non-viral (e.g., Lipid Nanoparticles, Polymers) vectors, with applications in Gene Therapy, Vaccinology, and Cell Therapy, underscores the diverse and evolving therapeutic innovation landscape.

The global Viral and Non-Viral Vector Manufacturing market is poised for unprecedented growth, driven by a confluence of scientific advancements, increasing therapeutic applications, and a robust pipeline of innovative treatments. XXX, representing a substantial market size in the hundreds of millions of units, is projected to expand at a significant CAGR during the forecast period of 2025-2033. This growth is underpinned by a surge in demand for gene therapies and vaccines, where viral and non-viral vectors serve as crucial delivery mechanisms. The historical period (2019-2024) witnessed foundational developments and early-stage clinical successes, laying the groundwork for the current exponential trajectory. The estimated market size for 2025, at hundreds of millions of units, reflects the accelerating pace of drug development and commercialization within this sector. Looking ahead, the forecast period is expected to see continued innovation in vector design, production scalability, and regulatory approvals, further solidifying the market's expansion. Key insights reveal a strong preference for viral vectors, particularly adeno-associated viruses (AAVs) and lentiviruses, due to their established efficacy in gene delivery. However, non-viral vectors are rapidly gaining traction, offering advantages in terms of safety, immunogenicity, and manufacturing simplicity. This dual approach, addressing both viral and non-viral modalities, is a hallmark of the current market landscape, catering to a diverse range of therapeutic targets and patient populations. The industry is witnessing a significant shift towards integrated manufacturing solutions, with companies focusing on optimizing upstream and downstream processes to achieve higher yields and purity at a reduced cost. Furthermore, the increasing investment in advanced manufacturing technologies, such as continuous manufacturing and single-use systems, is expected to play a pivotal role in meeting the escalating demand for these complex biological products. The evolving regulatory landscape, while presenting its own set of challenges, is also becoming more conducive to the approval and commercialization of gene and cell therapies, further stimulating market growth. The market is characterized by a dynamic interplay between established pharmaceutical giants and agile biotechnology firms, each contributing to the innovation and expansion of the vector manufacturing ecosystem.

The trajectory of the Viral and Non-Viral Vector Manufacturing market is being propelled by a powerful synergy of scientific breakthroughs and evolving healthcare needs. At the forefront is the remarkable progress in gene therapy, a field that has transitioned from theoretical promise to tangible clinical success. The development of highly effective gene therapies for previously intractable genetic disorders is creating a substantial and growing demand for reliable and scalable vector manufacturing. Furthermore, the global emphasis on public health and pandemic preparedness has significantly boosted the vaccinology segment, with viral vectors playing a central role in the development of novel vaccines. The increasing understanding of cellular mechanisms and the potential of cell therapies are also contributing to the demand for both viral and non-viral vectors as tools for therapeutic interventions. Technological advancements in bioprocessing, including improvements in cell culture techniques, downstream purification, and analytical methods, are enabling manufacturers to produce vectors at higher titers and with greater purity. This enhanced manufacturing capability is crucial for meeting the stringent quality requirements for therapeutic applications. The growing investment in research and development by both public and private entities, coupled with strategic partnerships and collaborations, is continuously expanding the pipeline of potential vector-based therapeutics, further fueling market expansion. The base year of 2025 and the forecast period of 2025-2033 are expected to witness a substantial acceleration in these driving forces, translating into significant market growth.

Despite the promising outlook, the Viral and Non-Viral Vector Manufacturing market faces several significant challenges and restraints that could temper its growth. One of the primary hurdles is the inherent complexity and cost associated with the production of viral vectors. Large-scale manufacturing requires specialized facilities, stringent containment measures, and highly skilled personnel, contributing to high production costs. The development of efficient and scalable downstream purification processes remains a critical challenge, impacting overall yield and cost-effectiveness. Furthermore, immunogenicity of viral vectors, though often engineered for reduced immunogenicity, can still pose a challenge, potentially leading to adverse immune responses in patients and limiting their therapeutic application. Regulatory pathways for gene and cell therapies, while evolving, can be complex and lengthy, requiring extensive preclinical and clinical data to gain approval. This can lead to extended timelines for product commercialization and increased development costs. The consistent supply of raw materials, especially specialized cell culture media and reagents, at the required quality and scale can also be a bottleneck. For non-viral vectors, challenges include achieving efficient cellular uptake and intracellular delivery, as well as ensuring adequate payload release at the target site. The relatively nascent stage of some non-viral vector technologies means they may require further optimization before widespread clinical adoption. Finally, the high cost of gene and cell therapies, directly linked to manufacturing expenses, can pose an affordability challenge for patients and healthcare systems, potentially limiting market penetration. These challenges, though significant, are being actively addressed through ongoing research and innovation, aiming to overcome these limitations and unlock the full potential of vector-based therapies.

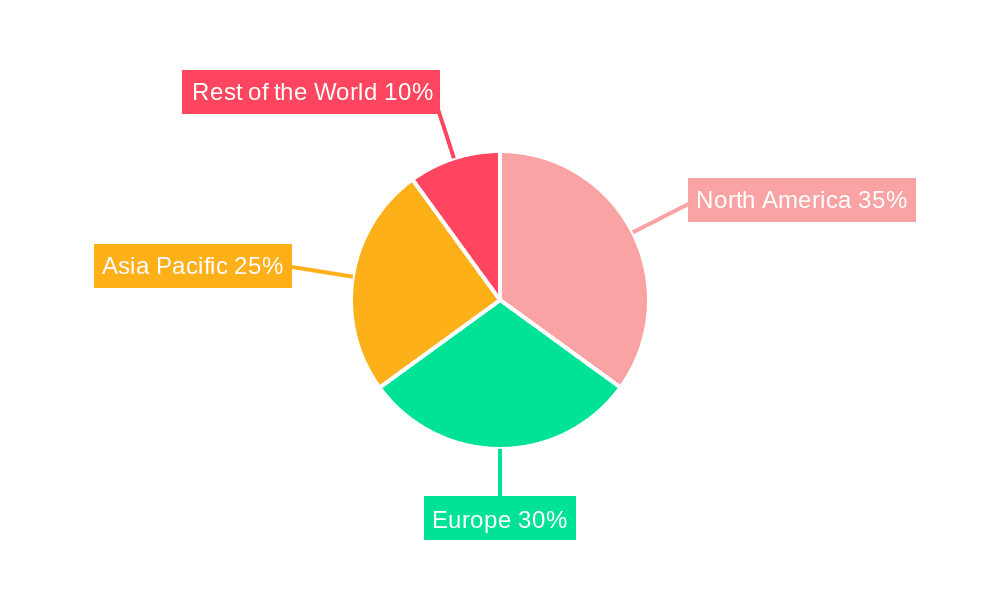

The global Viral and Non-Viral Vector Manufacturing market is poised for dominance by the Gene Therapy segment within the North America region. This dominance is a multifaceted phenomenon driven by a confluence of pioneering research, robust investment, a favorable regulatory environment, and a significant unmet medical need.

North America, particularly the United States, has historically been at the vanguard of biotechnology and pharmaceutical innovation. This leadership is evident in the high concentration of leading research institutions, academic centers, and pharmaceutical and biotech companies actively engaged in the development of gene and cell therapies. The region boasts a well-established ecosystem that supports the entire value chain, from early-stage discovery and preclinical research to clinical trials and commercial manufacturing. Government funding for biomedical research, coupled with substantial venture capital investment, has created a fertile ground for the growth of gene therapy companies. This financial backing is crucial for the capital-intensive nature of vector manufacturing.

The Gene Therapy segment is experiencing explosive growth due to its transformative potential in treating a wide range of inherited and acquired diseases. These therapies offer the promise of one-time cures for conditions that were previously managed with lifelong treatments, or that had no effective treatment options at all.

The Viral Vector type segment within gene therapy is particularly dominant. Adeno-associated viruses (AAVs) and lentiviruses are widely employed due to their established safety profiles and efficient transduction capabilities. The manufacturing of these viral vectors, with an estimated volume in the hundreds of millions of units annually, is critical for the success of numerous approved and pipeline gene therapies. The ability to produce these vectors consistently, at high purity, and at scale is a testament to the advanced manufacturing capabilities present in North America.

In summary, the Gene Therapy segment in North America, propelled by continuous innovation, substantial investment, and a supportive regulatory framework, is set to lead the Viral and Non-Viral Vector Manufacturing market. The region's advanced manufacturing infrastructure and its central role in the global gene therapy pipeline solidify its position of dominance.

The Viral and Non-Viral Vector Manufacturing industry is experiencing robust growth fueled by several key catalysts. The accelerating development and approval of gene and cell therapies, offering potential cures for previously untreatable diseases, directly translate into increased demand for vector production. Advances in manufacturing technologies, such as single-use systems and continuous bioprocessing, are enhancing scalability, efficiency, and cost-effectiveness. Growing investment in R&D by pharmaceutical companies and biotechnology firms, coupled with increasing government support for advanced therapies, further propels innovation and market expansion. The expanding pipeline of novel vaccines utilizing viral vectors also contributes significantly to this growth trajectory.

This comprehensive report offers an in-depth analysis of the global Viral and Non-Viral Vector Manufacturing market, providing detailed insights into its current landscape and future trajectory. The study encompasses a thorough examination of market dynamics, including driving forces, challenges, and key growth catalysts. It delves into specific industry developments, technological advancements, and the evolving regulatory environment that shapes the market. The report presents a robust market segmentation analysis, covering vector types (viral and non-viral), applications (gene therapy, vaccinology, cell therapy, others), and regional market breakdowns. With a detailed study period spanning from 2019-2033, a base year of 2025, and a forecast period of 2025-2033, the report provides a data-rich perspective for stakeholders. The analysis includes market size estimations in millions of units and highlights the strategic initiatives and contributions of leading industry players, offering a holistic understanding of this rapidly evolving sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 21%.

Key companies in the market include Boehringer Ingelheim, Catalent, Fujifilm Holdings Corporation, Danaher Corporation, Rescript Biotech Corporation, Lonza Group Ag, Merck Kagan, Oxford Biomedical Plc, Sartorius Ag, Takara Bio, Thermo Fisher Scientific, Wuxi Optec, Acuities Therapeutic, Evonik Industries Ag, Exiled, Entos Pharmaceuticals, Genevant Sciences Gmbh, T&T Scientific Corporation, Moderna, Curevac Nv.

The market segments include Type, Application.

The market size is estimated to be USD 10.3 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Viral and Non Viral Vector Manufacturing," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Viral and Non Viral Vector Manufacturing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.