1. What is the projected Compound Annual Growth Rate (CAGR) of the Vehicle Light Weighting Technologies?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Vehicle Light Weighting Technologies

Vehicle Light Weighting TechnologiesVehicle Light Weighting Technologies by Type (/> Material, Manufacturing Process), by Application (/> Electric Car, Fuel Car), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

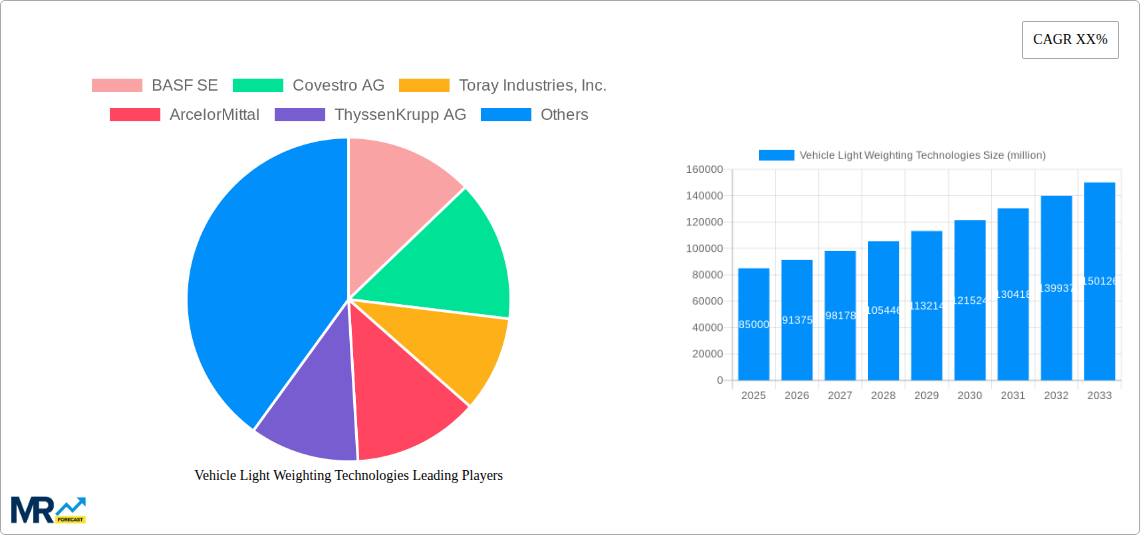

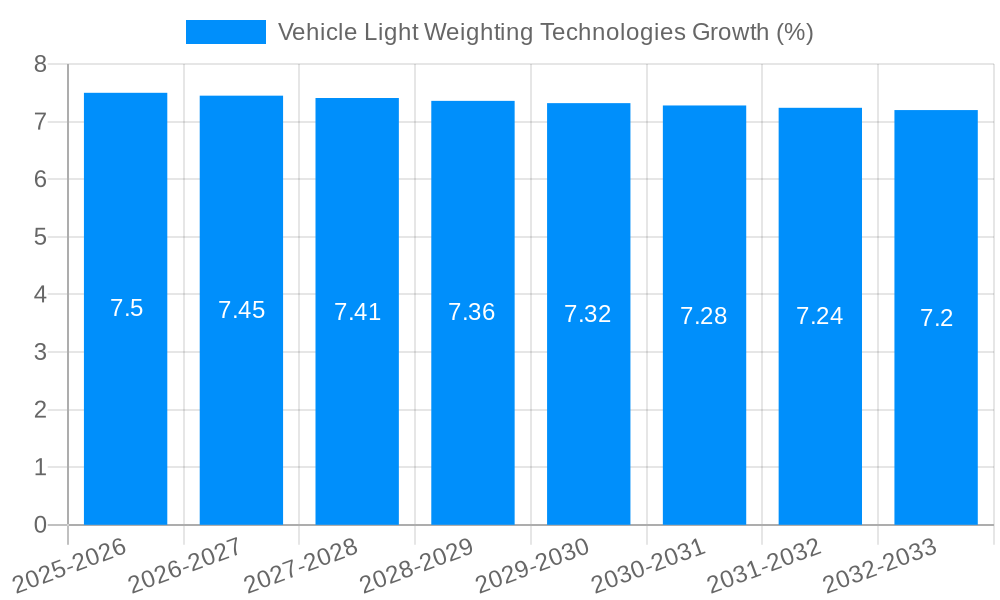

The global vehicle lightweighting technologies market is experiencing robust growth, driven by stringent fuel efficiency regulations, the increasing demand for enhanced vehicle performance, and the rising adoption of electric vehicles (EVs). The market, estimated at $50 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 7% from 2025 to 2033, reaching approximately $85 billion by 2033. Key drivers include the automotive industry's ongoing efforts to reduce greenhouse gas emissions, improve fuel economy, and enhance vehicle safety. This is further accelerated by the increasing popularity of EVs, which require lighter-weight materials to maximize battery range and performance. Major trends include the rising adoption of advanced materials like high-strength steel, aluminum alloys, carbon fiber composites, and magnesium alloys, as well as the integration of innovative manufacturing processes such as additive manufacturing (3D printing) and advanced joining techniques. While the high initial cost of some lightweighting materials presents a restraint, ongoing technological advancements and economies of scale are progressively mitigating this barrier. The market is segmented by material type (e.g., steel, aluminum, composites), application (e.g., body panels, chassis), and vehicle type (e.g., passenger cars, commercial vehicles). Leading companies such as BASF, Covestro, Toray, ArcelorMittal, and 3M are at the forefront of innovation and market share, continually developing and refining lightweighting technologies to meet the evolving needs of the automotive industry.

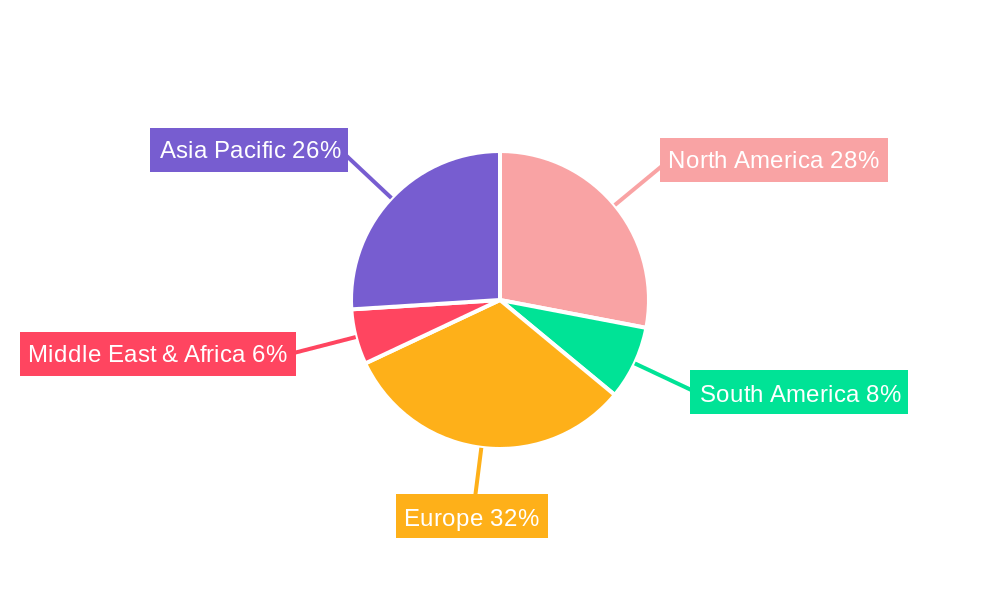

The competitive landscape is characterized by both established materials suppliers and automotive manufacturers actively investing in R&D to develop and integrate lighter materials. This necessitates strategic collaborations and partnerships to leverage each other's strengths in materials science, manufacturing, and vehicle design. Regional variations exist, with North America and Europe currently holding significant market shares, while Asia-Pacific is poised for substantial growth due to the rapid expansion of the automotive industry in this region. Future growth will be further fueled by continuous research into even lighter and more sustainable materials, alongside advances in simulation and modelling techniques for optimal lightweighting design. This ongoing evolution will shape the market landscape in the coming years, driving innovation and increased adoption of vehicle lightweighting technologies across all vehicle segments.

The global vehicle lightweighting technologies market is experiencing robust growth, projected to reach multi-million unit sales by 2033. Driven by stringent fuel efficiency regulations, increasing demand for electric vehicles (EVs), and the pursuit of enhanced vehicle performance, the adoption of lightweighting materials and technologies is accelerating across the automotive industry. The market witnessed significant growth during the historical period (2019-2024), exceeding expectations in several key segments. The estimated year 2025 reveals a market already demonstrating substantial expansion, laying the groundwork for the robust forecast period (2025-2033). Key market insights reveal a strong preference for advanced materials like carbon fiber reinforced polymers (CFRP), aluminum alloys, and high-strength steels, alongside innovative manufacturing techniques like advanced casting and forming processes. The shift towards EVs is a pivotal driver, as lightweighting directly impacts battery range and overall vehicle efficiency. This trend is further amplified by the rising consumer preference for fuel-efficient and environmentally friendly vehicles. While the base year (2025) shows strong performance, the forecast period anticipates even greater expansion, spurred by continuous technological advancements, strategic collaborations between material suppliers and automotive manufacturers, and supportive government policies promoting sustainable transportation. The market is seeing a gradual shift from traditional steel-intensive designs towards a more diversified material portfolio, reflecting the industry's commitment to optimizing vehicle weight without compromising safety or durability. This transition demands substantial investment in research and development, resulting in the emergence of increasingly sophisticated and cost-effective lightweighting solutions. Competition amongst material suppliers is fierce, pushing innovation and creating a dynamic market landscape characterized by continuous improvement and the introduction of new, advanced materials.

The automotive industry's relentless pursuit of improved fuel economy and reduced emissions is the primary driver behind the booming vehicle lightweighting technologies market. Stringent government regulations worldwide, mandating improved fuel efficiency standards, are forcing automakers to explore and implement lightweighting strategies as a crucial approach to compliance. Furthermore, the surging popularity of electric vehicles significantly intensifies this trend. Lightweighting directly translates to extended battery range and improved overall vehicle performance in EVs, making it a critical factor in their design and production. The growing consumer demand for fuel-efficient and environmentally conscious vehicles further complements these factors. Consumers are increasingly willing to pay a premium for vehicles that offer better fuel economy and reduced environmental impact, creating a strong market pull for lightweighting technologies. The continuous advancements in materials science and manufacturing processes contribute significantly to the market's expansion. New lightweight materials with enhanced properties are constantly being developed, while innovative manufacturing techniques are enhancing the cost-effectiveness and efficiency of lightweighting implementation. Finally, strategic collaborations between material suppliers and automotive manufacturers are accelerating the adoption and integration of advanced lightweighting solutions, fostering a synergistic environment for growth.

Despite the significant growth potential, the vehicle lightweighting technologies market faces several challenges. The high initial cost associated with some advanced lightweight materials, such as carbon fiber, poses a considerable barrier to entry for many automakers, particularly those operating in price-sensitive market segments. The complexity of designing and manufacturing vehicles with unconventional lightweight materials requires substantial investment in research, development, and specialized equipment, adding to the overall cost. Ensuring the safety and durability of vehicles incorporating lightweight materials is paramount, necessitating rigorous testing and certification processes. The challenge lies in achieving a balance between weight reduction and the structural integrity needed to meet stringent safety standards. Furthermore, the recyclability and environmental impact of certain lightweight materials remain a concern, prompting a need for sustainable solutions and responsible material sourcing. The supply chain complexity involved in sourcing and integrating these materials into the manufacturing process adds another layer of challenges, requiring seamless collaboration across various stakeholders. Finally, the lack of awareness and understanding among consumers about the benefits of lightweighting technologies can hinder market adoption.

North America: The region's stringent fuel efficiency standards and strong presence of major automotive manufacturers, like General Motors and Ford, drive significant demand. The ongoing investments in electric vehicle development further fuel the adoption of lightweighting technologies.

Europe: The EU's commitment to reducing CO2 emissions has spurred substantial growth in this market. The presence of leading automotive manufacturers and a robust supplier network ensures the region's continued dominance.

Asia-Pacific: Rapid industrialization, increasing vehicle production, and the growing popularity of EVs in countries like China, Japan, and South Korea are key drivers. The region's cost-competitive manufacturing capabilities also make it attractive for lightweighting material production.

Segments:

Aluminum Alloys: Their relatively high strength-to-weight ratio makes them a preferred choice for various automotive components. The continued advancement in aluminum alloy technology, focusing on improved formability and corrosion resistance, promises further market expansion.

High-Strength Steels: These offer a cost-effective solution for lightweighting, with advancements focusing on improving tensile strength and formability.

CFRP (Carbon Fiber Reinforced Polymers): While more expensive, CFRP provides superior strength and weight reduction benefits, leading to its increasing adoption in high-performance and luxury vehicles. Technological advancements are focusing on reducing the cost and improving the manufacturing processes of CFRP components.

Magnesium Alloys: These offer the lowest density among structural metals, making them attractive for lightweighting applications. However, limitations in formability and corrosion resistance are areas that need continued improvement.

The combination of these factors positions North America and Europe as key regions, with Aluminum Alloys and High-Strength Steels dominating the segment landscape due to their cost-effectiveness and widespread adoption. The Asia-Pacific region is poised for rapid growth, with its increasing vehicle production and shift towards electric vehicles driving demand for all lightweighting segments.

The convergence of stringent fuel economy regulations, the rise of electric vehicles, and continuous advancements in material science and manufacturing technology are collectively acting as powerful catalysts for the growth of the vehicle lightweighting technologies industry. These factors create a synergistic effect, driving demand for innovative lightweight materials and spurring significant investment in research and development, ultimately propelling market expansion. Growing consumer awareness of environmental concerns and the desire for fuel-efficient vehicles further amplify this growth trajectory.

This report provides a comprehensive overview of the vehicle lightweighting technologies market, encompassing historical data, current market trends, future projections, and key industry players. It offers deep insights into driving forces, challenges, and growth catalysts, helping stakeholders understand the market dynamics and make informed decisions. The report also provides granular segment analysis, examining various material types and geographic regions to give a complete picture of the market landscape. The inclusion of profiles of leading industry players helps to provide a competitive analysis of the sector and identify key market trends.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include BASF SE, Covestro AG, Toray Industries, Inc., ArcelorMittal, ThyssenKrupp AG, 3M, Toyota, General Motors, Tata Steel, Honda Motor Co., Ltd., DuPont.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Vehicle Light Weighting Technologies," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Vehicle Light Weighting Technologies, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.