1. What is the projected Compound Annual Growth Rate (CAGR) of the Vehicle Lidar System?

The projected CAGR is approximately 34.2%.

Vehicle Lidar System

Vehicle Lidar SystemVehicle Lidar System by Type (Solid State Lidar, Mechanical Lidar, World Vehicle Lidar System Production ), by Application (ADAS, Self-driving, World Vehicle Lidar System Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

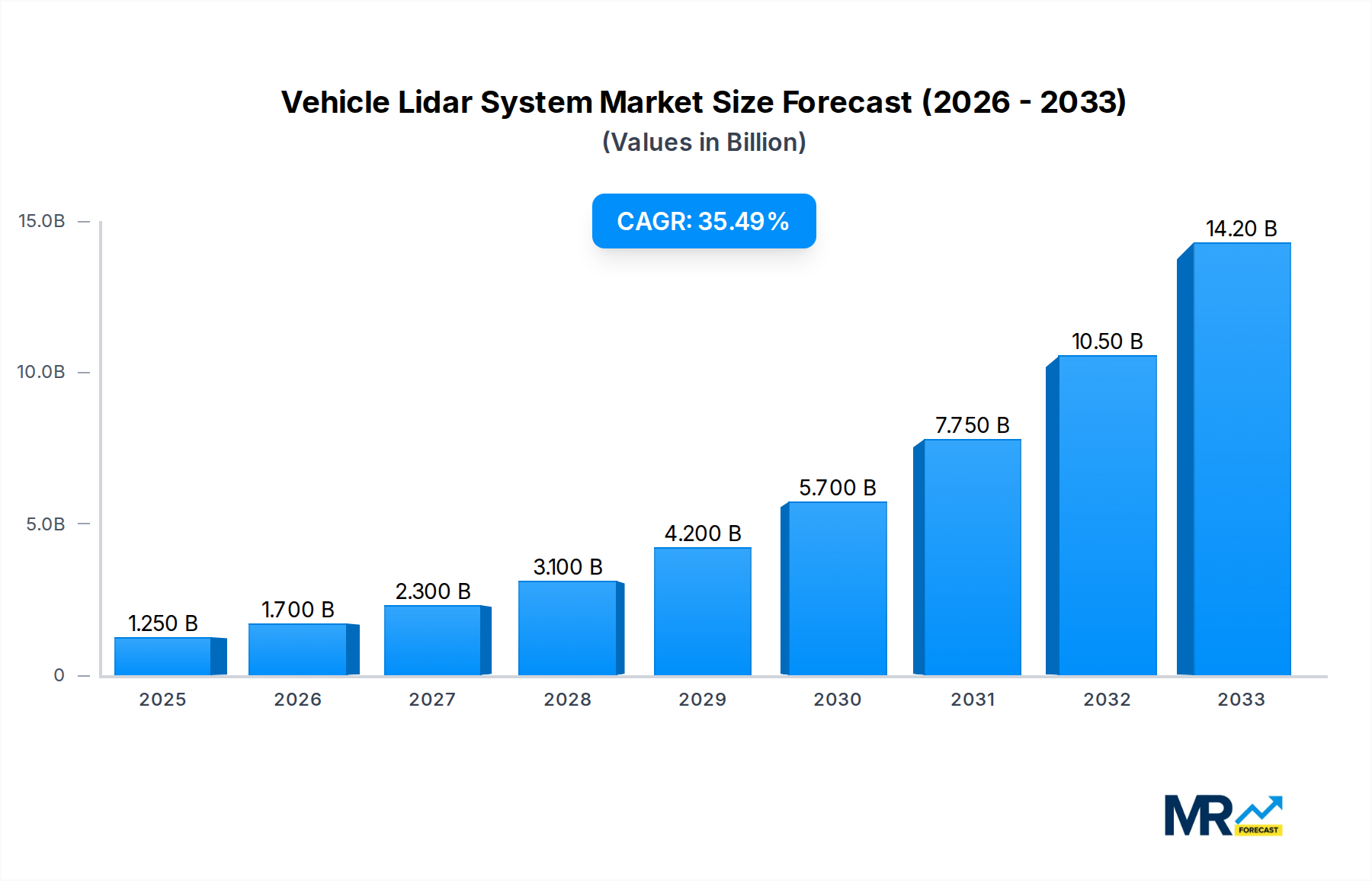

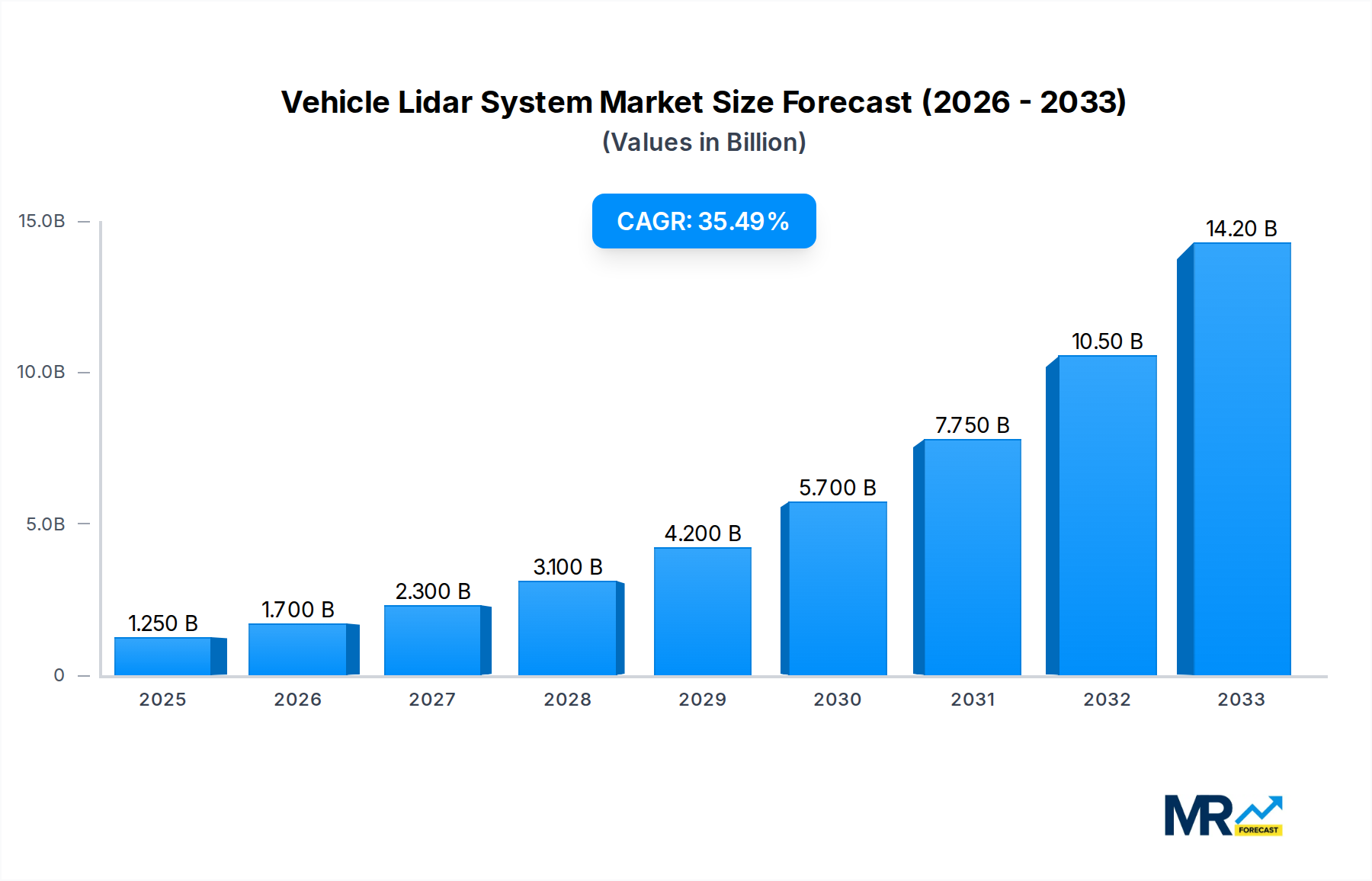

The global Vehicle Lidar System market is experiencing explosive growth, projected to reach $1.25 billion in 2025 and surge to an impressive valuation by 2033. This rapid expansion is fueled by a remarkable Compound Annual Growth Rate (CAGR) of 34.2%, indicating a significant and sustained upward trajectory for lidar technology in the automotive sector. The primary drivers behind this surge are the accelerating adoption of Advanced Driver-Assistance Systems (ADAS) and the relentless pursuit of fully autonomous driving capabilities. As regulatory frameworks evolve and consumer confidence in self-driving technology increases, the demand for sophisticated sensing solutions like lidar, which offer unparalleled accuracy in object detection, distance measurement, and environmental mapping, will only intensify. The market is witnessing a significant shift towards Solid State Lidar, which promises enhanced reliability, reduced cost, and smaller form factors compared to traditional Mechanical Lidar. This technological evolution is crucial for mass-market integration and the realization of widespread vehicle autonomy.

The competitive landscape is robust, featuring key players such as Hesai Tech, Valeo, RoboSense, Luminar, Continental, and Velodyne, among others, all vying for market share in this dynamic sector. These companies are heavily invested in research and development, pushing the boundaries of lidar performance, cost-effectiveness, and integration. Geographically, Asia Pacific, particularly China, is emerging as a dominant force due to its substantial automotive production and proactive government initiatives supporting smart mobility and autonomous vehicle development. North America and Europe are also critical markets, driven by stringent safety regulations and significant investments in ADAS and autonomous vehicle R&D. Emerging trends include the integration of lidar with other sensor technologies for sensor fusion, the development of high-resolution and long-range lidar for enhanced safety, and the exploration of lidar applications beyond traditional ADAS and self-driving, such as predictive maintenance and in-cabin monitoring. While the growth is substantial, potential restraints could include the high initial cost of advanced lidar systems, though this is rapidly diminishing, and ongoing challenges in standardization and regulatory approval for fully autonomous systems.

This in-depth report provides a definitive look at the rapidly evolving Vehicle Lidar System market, projected to surge to over $30 billion by 2033. Spanning the Historical Period (2019-2024) and extending through the Forecast Period (2025-2033), with a detailed analysis of the Base Year (2025), this research delves into the critical trends, drivers, challenges, and pivotal players shaping the automotive perception landscape. Our comprehensive coverage includes detailed segment analysis, regional market dynamics, and an examination of groundbreaking industry developments. The report leverages a robust analytical framework, incorporating quantitative data and qualitative insights to offer actionable intelligence for stakeholders.

The Vehicle Lidar System market is experiencing a transformative surge, driven by an unprecedented demand for enhanced automotive safety and the accelerating adoption of advanced driver-assistance systems (ADAS) and fully autonomous driving capabilities. XXX, a key market insight, indicates a substantial shift from legacy mechanical lidar solutions towards more cost-effective, robust, and miniaturized solid-state lidar technologies. This evolution is not merely about technological advancement but is intrinsically linked to the economic viability of widespread lidar integration in consumer vehicles. The market is witnessing a significant bifurcation, with high-performance, long-range lidar systems primarily catering to the nascent self-driving vehicle segment, while more affordable, short-to-medium range solutions are rapidly becoming integral to ADAS features in mainstream vehicles. The projected market value underscores this rapid expansion, with billions of dollars being invested and projected to flow into research, development, and manufacturing.

Furthermore, XXX highlights the growing trend of lidar system commoditization, leading to intensified price competition and a push for higher production volumes. This is fueled by an expanding ecosystem of lidar manufacturers, including established automotive suppliers and innovative startups, all vying for market share. The increasing integration of lidar with other sensor modalities, such as radar and cameras, forms a crucial trend, enabling sensor fusion for superior environmental perception and redundancy. This multi-sensor approach is vital for achieving the stringent safety standards required for autonomous driving. The report also scrutinizes the geographical distribution of these trends, noting the significant influence of regions with strong automotive manufacturing bases and aggressive government initiatives promoting autonomous vehicle development. The convergence of technological innovation, cost reduction, and regulatory support is creating a fertile ground for lidar technology to become a ubiquitous component of future mobility. The sheer scale of the projected market growth, reaching tens of billions of dollars, speaks volumes about the fundamental shift in automotive perception technology.

The Vehicle Lidar System market is being propelled by a confluence of powerful forces, fundamentally reshaping the automotive industry. The paramount driver is the relentless pursuit of enhanced vehicle safety. Lidar's ability to provide precise 3D environmental mapping, even in challenging lighting and weather conditions, offers a significant leap forward in collision avoidance, pedestrian detection, and overall situational awareness, crucial for reducing road fatalities and accidents. This intrinsic safety advantage is directly fueling the demand for lidar integration in ADAS features, from adaptive cruise control and automatic emergency braking to more sophisticated lane-keeping and blind-spot monitoring systems.

Beyond safety, the burgeoning ambition of self-driving technology stands as another immense catalyst. As the automotive industry races towards Level 4 and Level 5 autonomy, lidar systems are considered an indispensable component for reliable perception and navigation. The ability of lidar to accurately detect and track objects, understand complex road geometries, and build detailed environmental maps is critical for vehicles to operate safely without human intervention. This push for autonomy, backed by substantial investments from tech giants and automotive manufacturers alike, directly translates into a burgeoning demand for high-performance lidar solutions. The economic implications are profound, with the market poised for exponential growth as these technologies mature and become more accessible for widespread deployment. The ongoing advancements in lidar technology, leading to reduced costs and improved performance, further amplify these driving forces, making lidar an increasingly attractive and feasible solution for a wide spectrum of automotive applications.

Despite the immense growth potential, the Vehicle Lidar System market faces significant hurdles and restraints that could temper its trajectory. A primary challenge remains the cost of lidar sensors. While prices have been declining, especially for solid-state variants, the current cost of high-performance lidar units can still be prohibitively expensive for mass-market passenger vehicles, making them a premium feature rather than a standard offering. This cost barrier directly impacts the speed of adoption for ADAS and autonomous driving features in more affordable car segments.

Another critical restraint is standardization and regulatory clarity. The absence of universally agreed-upon performance standards and safety regulations for lidar systems can create uncertainty for manufacturers and hinder widespread deployment. Different regions and countries may have varying requirements, leading to fragmentation in development efforts and increased compliance costs. Furthermore, public perception and trust in autonomous driving technology, heavily reliant on sensors like lidar, can be fragile. High-profile accidents, even if not directly attributable to lidar failures, can sow seeds of doubt among consumers, impacting the willingness to adopt vehicles equipped with such advanced perception systems. Finally, manufacturing scalability and supply chain robustness present ongoing challenges. As demand surges, ensuring a consistent and high-quality supply of lidar components and finished systems at a global scale requires significant investment in manufacturing infrastructure and a resilient supply chain, susceptible to disruptions.

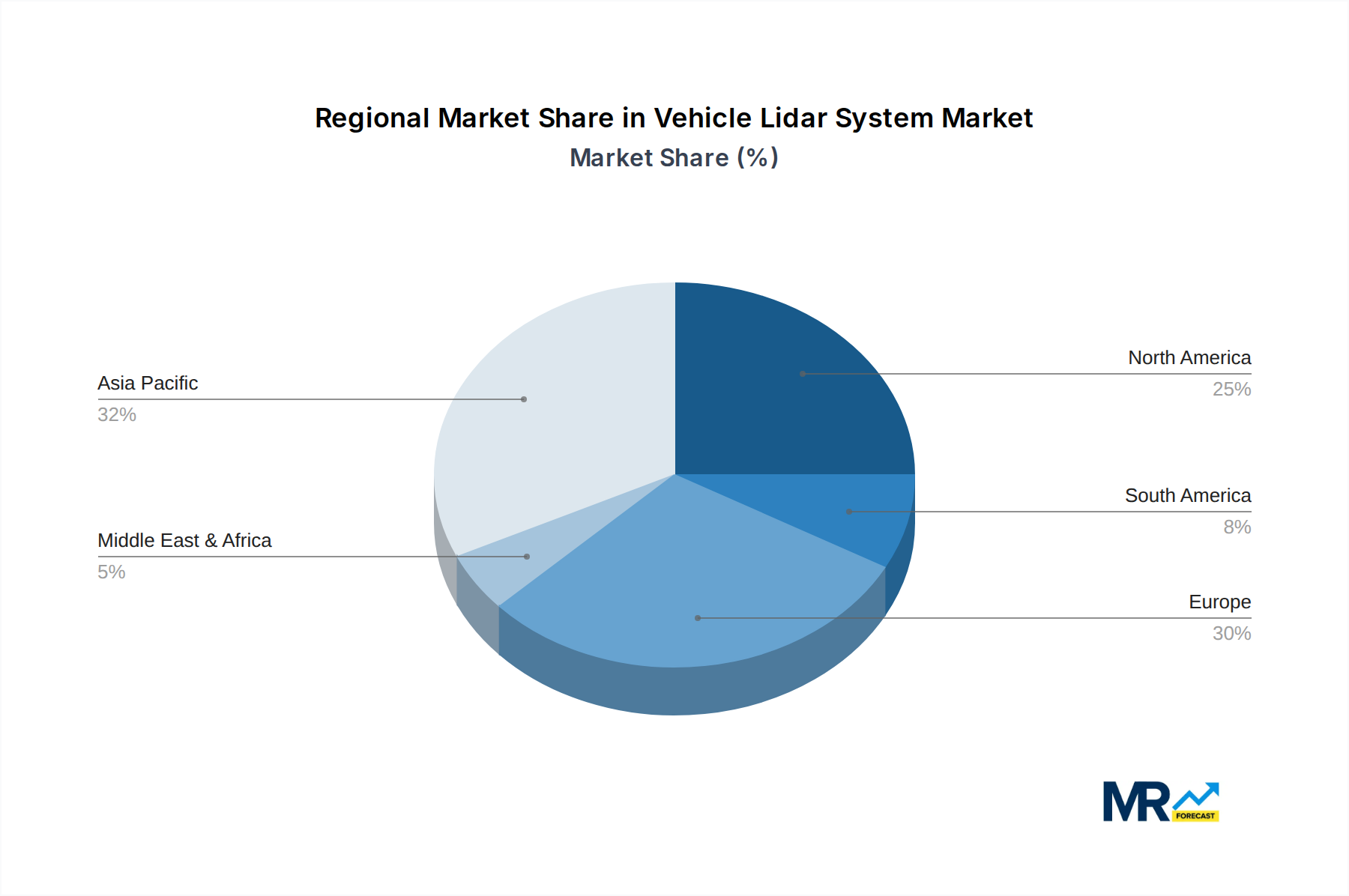

The North American region, particularly the United States, is poised to emerge as a dominant force in the Vehicle Lidar System market. This dominance is underpinned by a powerful combination of factors: a robust automotive industry with a strong appetite for technological innovation, a leading position in the development and testing of autonomous vehicle technology, and substantial government support for research and development in this sector. The presence of major automotive OEMs, established lidar manufacturers, and numerous cutting-edge startups, particularly in California, creates a vibrant ecosystem driving significant demand and advancements. Furthermore, the regulatory environment in the US, while evolving, has generally been more conducive to the testing and deployment of autonomous vehicle technologies compared to some other regions, encouraging early adoption of lidar.

Within North America, the Self-driving application segment is expected to be a primary driver of market growth. The aggressive pursuit of fully autonomous vehicles by tech companies and automotive giants headquartered in the region necessitates the integration of advanced perception systems, with lidar playing a critical role. Companies are investing heavily in developing and validating lidar technologies capable of meeting the stringent requirements for Level 4 and Level 5 autonomy. This focus on high-end autonomous applications will naturally lead to a higher demand for sophisticated and often more expensive lidar systems.

However, the ADAS application segment is not to be underestimated and will contribute significantly to the overall market volume, especially in the latter half of the forecast period. As costs continue to decrease and regulations evolve, lidar integration into advanced driver-assistance systems for mainstream passenger vehicles will become increasingly prevalent. This includes features like advanced pedestrian detection, improved adaptive cruise control, and enhanced blind-spot monitoring, which will drive widespread adoption across a broader range of vehicles.

Geographically, while North America is expected to lead, Europe will also be a significant market, driven by strong automotive manufacturing, stringent safety regulations, and a growing interest in sustainable mobility solutions. The region's focus on safety and its established automotive supply chains will foster steady growth. Asia-Pacific, particularly China, presents a rapidly expanding market with enormous potential, fueled by a massive domestic automotive market, aggressive government initiatives to promote electric vehicles and autonomous driving, and a growing number of domestic lidar manufacturers. The competitive landscape in China is intense, with rapid technological advancements and a strong push for localized solutions.

Considering the Segment Type, Solid State Lidar is anticipated to witness the most substantial growth and eventually dominate the market. This is due to its inherent advantages over traditional mechanical lidar, including smaller form factors, increased durability, lower power consumption, and, crucially, the potential for significantly lower production costs at scale. As manufacturing processes mature and economies of scale are achieved, solid-state lidar will become the de facto standard for both ADAS and autonomous driving applications, gradually phasing out its mechanical counterparts in most new vehicle deployments. This technological shift is a critical trend shaping the future of the Vehicle Lidar System market.

Several factors are acting as potent growth catalysts for the Vehicle Lidar System industry. The relentless pursuit of enhanced automotive safety standards by regulatory bodies worldwide is a major catalyst, pushing OEMs to adopt lidar for superior object detection and avoidance capabilities. Concurrently, the accelerating development and commercialization of autonomous driving technologies by tech giants and automotive manufacturers are creating a substantial demand for reliable perception sensors like lidar. Furthermore, ongoing advancements in lidar technology are leading to cost reductions and performance improvements, making it more accessible for broader adoption in both ADAS and full autonomy. The increasing investment from venture capital firms and strategic partnerships among key players are also fueling innovation and market expansion.

This comprehensive report offers an unparalleled deep dive into the global Vehicle Lidar System market, extending from the Historical Period (2019-2024) through to the Forecast Period (2025-2033), with a focused analysis of the Base Year (2025). It meticulously dissects the market dynamics, examining key trends such as the transition to solid-state lidar and the increasing integration with other sensor technologies. The report extensively analyzes the Driving Forces, including the unwavering demand for enhanced automotive safety and the accelerating progress in autonomous driving. It also critically evaluates the Challenges and Restraints, such as cost barriers, standardization issues, and public perception. A significant portion of the report is dedicated to identifying Key Regions and Segments poised for dominance, particularly focusing on North America and the self-driving application segment, while also acknowledging the growing importance of ADAS. The report further illuminates Growth Catalysts, highlighting regulatory pushes and technological advancements. Finally, it provides a detailed overview of Leading Players and Significant Developments, offering a holistic perspective on the current and future landscape of this transformative automotive technology.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 34.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 34.2%.

Key companies in the market include Hesai Tech, Valeo, RoboSense, Luminar, Continental, Velodyne, Ouster, Livox, Innoviz, Cepton, Aeva, .

The market segments include Type, Application.

The market size is estimated to be USD 1.25 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Vehicle Lidar System," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Vehicle Lidar System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.