1. What is the projected Compound Annual Growth Rate (CAGR) of the Vehicle Active Safety Domain Controller?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Vehicle Active Safety Domain Controller

Vehicle Active Safety Domain ControllerVehicle Active Safety Domain Controller by Type (Single Core Controller, Multiple Core Controller, World Vehicle Active Safety Domain Controller Production ), by Application (Passenger Cars, Commercial Vehicles, World Vehicle Active Safety Domain Controller Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

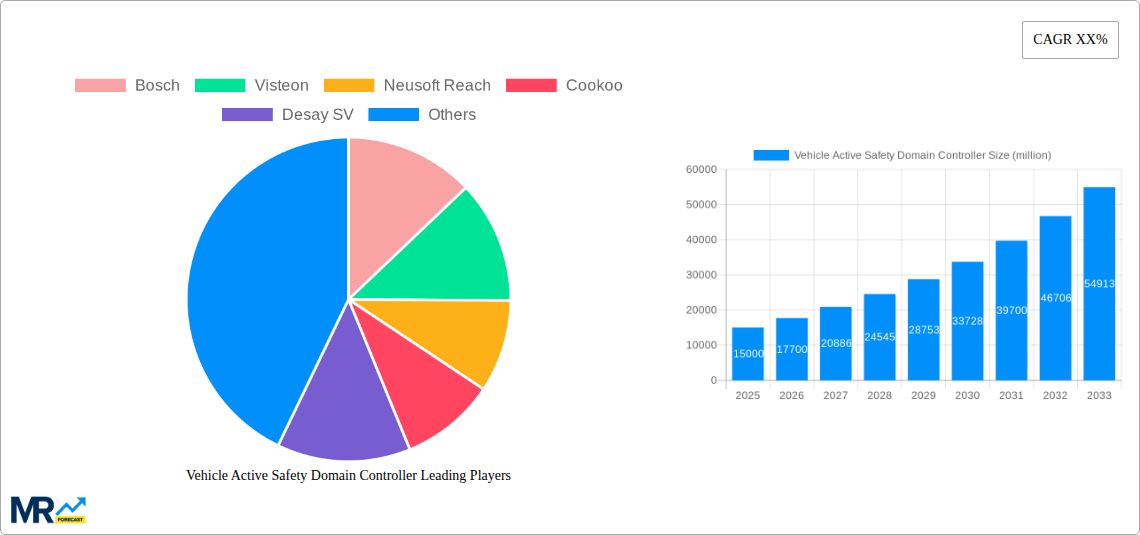

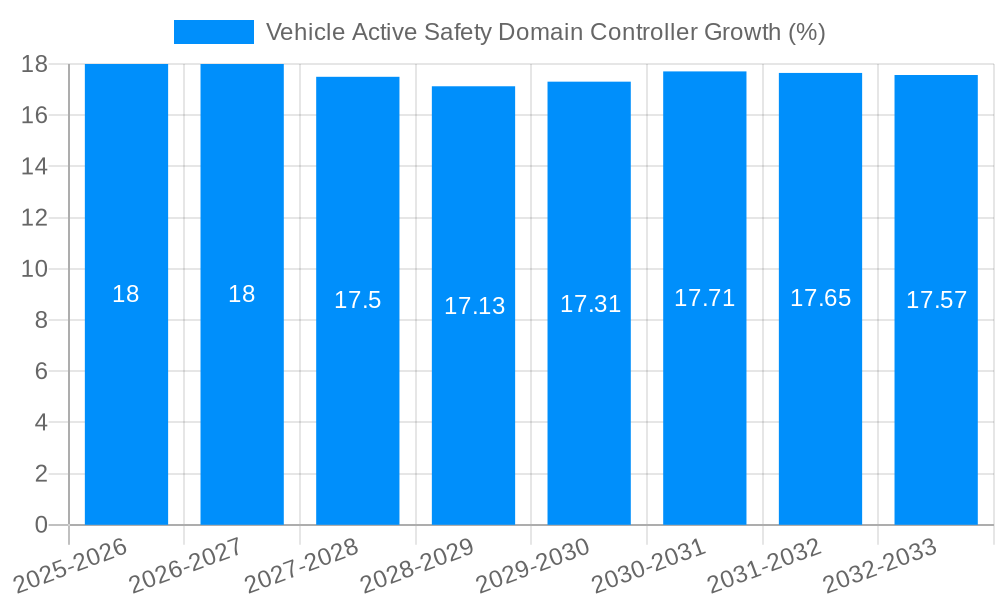

The Vehicle Active Safety Domain Controller market is experiencing robust growth, driven by increasing demand for advanced driver-assistance systems (ADAS) and autonomous driving features. The market's expansion is fueled by stricter government regulations mandating safety features in vehicles, coupled with rising consumer preference for enhanced safety and convenience. Technological advancements, such as the integration of artificial intelligence (AI) and machine learning (ML) algorithms for improved object detection and decision-making, are further propelling market growth. The rising adoption of electric vehicles (EVs) also presents a significant opportunity, as these vehicles often incorporate more sophisticated safety systems. Key players like Bosch, Continental, and Aptiv are heavily investing in research and development to enhance their domain controller offerings, leading to increased competition and innovation within the market. We estimate the market size in 2025 to be approximately $5 billion, projecting a Compound Annual Growth Rate (CAGR) of 15% through 2033, reaching a market value exceeding $15 billion. This growth, however, is subject to challenges like high initial investment costs for automakers and potential cybersecurity vulnerabilities associated with increasingly complex systems.

The market segmentation reveals significant opportunities across various vehicle types, from passenger cars to commercial vehicles. Geographically, North America and Europe currently hold a significant market share, attributed to high vehicle ownership and advanced technological adoption. However, the Asia-Pacific region is poised for substantial growth due to increasing vehicle production and expanding infrastructure development. The competitive landscape is characterized by a mix of established automotive suppliers and emerging technology companies, indicating a dynamic and rapidly evolving market. Future market trajectory will heavily rely on continued technological innovation, evolving safety standards, and consumer adoption of autonomous features. The integration of over-the-air (OTA) updates for software improvements and the development of more cost-effective solutions will be crucial for market penetration.

The vehicle active safety domain controller market is experiencing explosive growth, projected to reach multi-million unit shipments by 2033. This surge is driven by the increasing demand for advanced driver-assistance systems (ADAS) and autonomous driving functionalities. The historical period (2019-2024) witnessed a steady rise in adoption, primarily fueled by stringent safety regulations and the escalating consumer preference for enhanced vehicle safety features. Our estimations for 2025 predict significant market expansion, building upon this momentum. The forecast period (2025-2033) anticipates continued robust growth, with millions of units deployed annually. Key market insights reveal a clear shift towards centralized architectures, replacing the previously prevalent distributed approach. This centralization simplifies system integration, reduces wiring complexity, and enables faster processing speeds, ultimately leading to improved safety performance. The market is also witnessing increased adoption of artificial intelligence (AI) and machine learning (ML) algorithms within domain controllers to enhance situational awareness and decision-making capabilities. Furthermore, the rising integration of over-the-air (OTA) software updates facilitates continuous improvement and the rapid deployment of new safety features, expanding the market’s potential significantly. The competitive landscape is fiercely dynamic, with established automotive suppliers and emerging technology companies vying for market share through innovation and strategic partnerships. The shift towards software-defined vehicles further intensifies this competition, focusing attention on the development of advanced software capabilities and efficient platform architectures. The market's growth hinges on several factors, including advancements in sensor technologies, the expansion of 5G connectivity, and the development of robust cybersecurity measures to protect increasingly complex vehicle systems.

Several key factors are accelerating the growth of the vehicle active safety domain controller market. Firstly, the rising adoption of ADAS features, such as adaptive cruise control, lane keeping assist, automatic emergency braking, and blind-spot monitoring, is a major driver. Consumers increasingly prioritize safety, leading to higher demand for vehicles equipped with these features. Secondly, government regulations worldwide are mandating the inclusion of certain ADAS technologies in new vehicles, further propelling market expansion. The push towards autonomous driving is another significant catalyst, as domain controllers are essential components for self-driving capabilities. These controllers centralize and process data from various sensors, enabling the vehicle to make informed decisions about navigation and control. Technological advancements, including the development of more powerful and efficient processors, are also contributing to the growth. These advancements enable the integration of more complex algorithms and improved processing speeds, paving the way for more sophisticated ADAS and autonomous driving features. The cost reduction of components like sensors and processors also plays a role. Finally, the increasing connectivity of vehicles through 5G and other technologies facilitates data exchange and enables remote diagnostics and updates, enhancing the functionality and longevity of domain controllers.

Despite the significant growth potential, the vehicle active safety domain controller market faces several challenges. A primary concern is the high cost of development and integration, particularly for advanced autonomous driving systems. The complexity of these systems demands considerable investment in research and development, potentially hindering widespread adoption, especially in lower-cost vehicle segments. Ensuring functional safety and cybersecurity is paramount. The sophisticated nature of these controllers makes them vulnerable to cyberattacks, potentially leading to safety risks. Developing robust security protocols is crucial to mitigating these risks and building consumer trust. The need for extensive testing and validation adds to the cost and time-to-market. Meeting stringent safety standards requires rigorous testing procedures, delaying product launches and impacting overall profitability. Furthermore, the lack of standardized architectures and interfaces across different vehicle platforms can complicate integration and interoperability. This lack of standardization leads to increased development costs and delays in the deployment of new features. Finally, the dependence on reliable sensor data presents challenges in adverse weather conditions or challenging environments, potentially impacting system performance and safety.

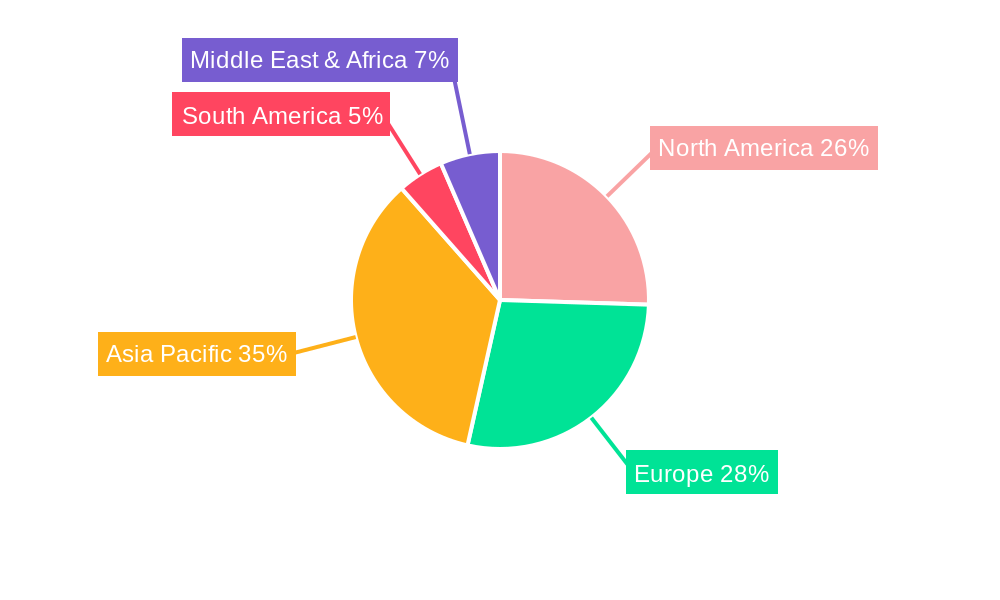

North America: The region's robust automotive industry, stringent safety regulations, and high consumer demand for advanced safety features make it a leading market for vehicle active safety domain controllers. Early adoption of advanced technologies and the presence of major automotive manufacturers and technology suppliers further contribute to its dominance.

Europe: Similar to North America, Europe demonstrates strong growth due to stringent safety regulations (e.g., Euro NCAP ratings) and high consumer awareness of vehicle safety.

Asia-Pacific: This region is experiencing rapid growth, driven by increasing vehicle production, rising disposable incomes, and growing government support for technological advancements in the automotive sector. China, in particular, is a significant market due to its large automotive market and strong government push for autonomous driving technology.

Segments: The luxury and premium vehicle segments are currently leading adoption, followed by the mid-size and compact segments. This is mainly due to higher willingness to pay for advanced safety features and higher profit margins. However, as technology costs decrease, it is expected that the adoption rate will increase significantly in the mass-market segment in the coming years. The shift towards centralized architectures is also a key segmental driver, offering improved efficiency and cost-effectiveness compared to distributed architectures.

The projected growth in all these regions and segments signifies the increasing importance of vehicle active safety in consumer preferences and regulatory mandates. The market's dynamic evolution creates significant opportunities for companies capable of adapting to technological advancements and evolving consumer demands.

The convergence of several factors fuels the growth of this sector. The increasing integration of artificial intelligence (AI) and machine learning (ML) algorithms within domain controllers significantly enhances safety functions. Government regulations pushing for ADAS features and autonomous driving technologies are also compelling automakers to adopt these systems. Furthermore, the ongoing advancements in sensor technology, processing power, and communication protocols like 5G are enabling the development of more sophisticated and reliable domain controllers. These developments are not only improving safety but also opening new possibilities for innovative features and services.

This report offers a comprehensive analysis of the vehicle active safety domain controller market, covering historical data (2019-2024), current estimations (2025), and future forecasts (2025-2033). It provides detailed insights into market trends, growth drivers, challenges, key players, and significant developments. The report also offers a granular segment analysis and regional breakdown, allowing for a precise understanding of the market landscape and its future evolution. This in-depth analysis provides valuable information for industry stakeholders, including automotive manufacturers, suppliers, and investors.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Bosch, Visteon, Neusoft Reach, Cookoo, Desay SV, Continental, ZF, Magna, Aptiv, Tttech, Veoneer, Higo Automotive, In-Driving, Baidu Domain Controller, iMotion, Hirain Technologies, Eco-Ev, Tesla AD Platform.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Vehicle Active Safety Domain Controller," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Vehicle Active Safety Domain Controller, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.