1. What is the projected Compound Annual Growth Rate (CAGR) of the Thoracic Retractor?

The projected CAGR is approximately 7.3%.

Thoracic Retractor

Thoracic RetractorThoracic Retractor by Type (Stainless Steel, Aluminium, Titanium Alloy, Others), by Application (Hospitals, Ambulatory Surgery Centers, Clinics, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

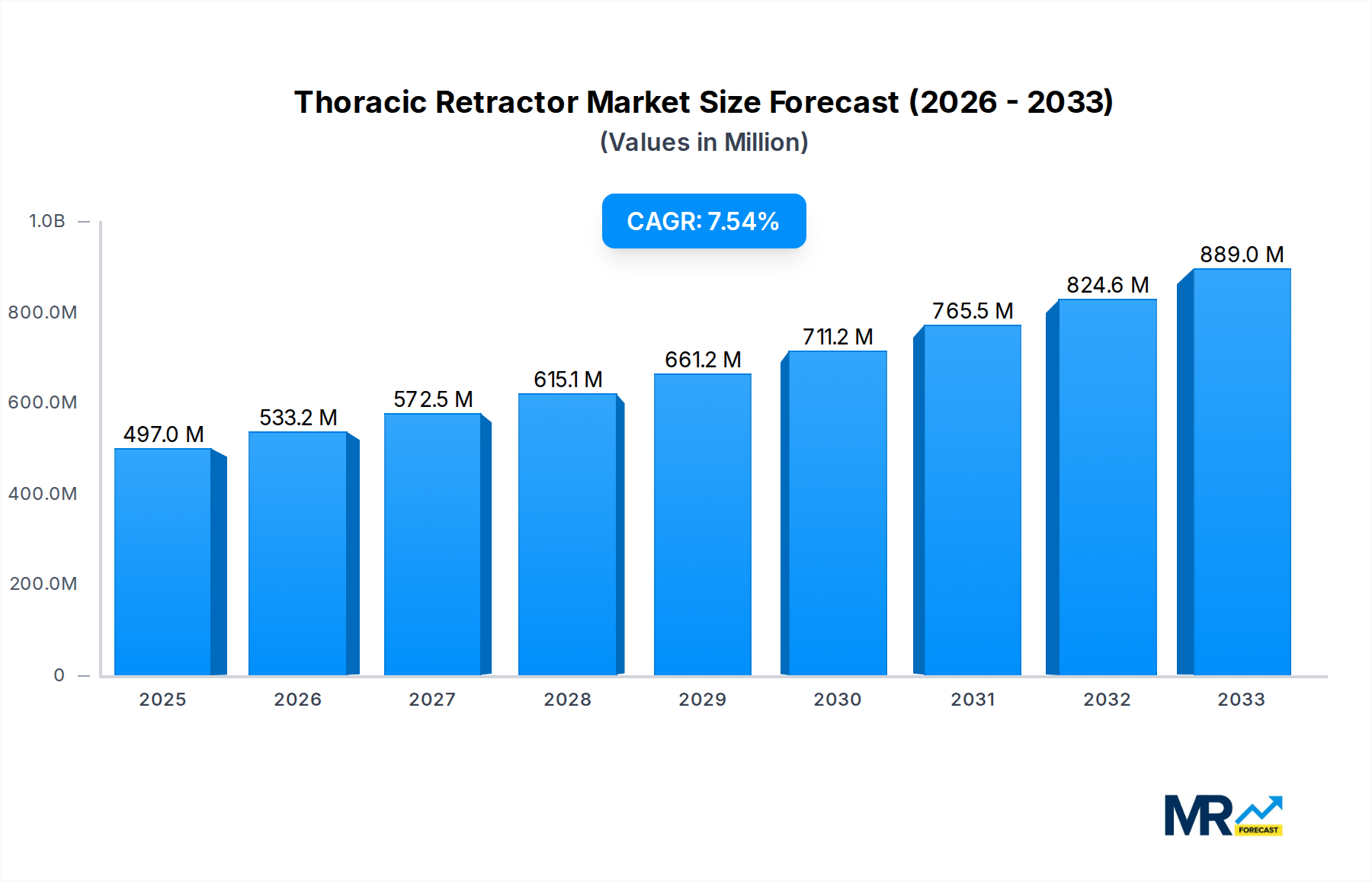

The global Thoracic Retractor market is poised for significant expansion, projecting a market size of $497 million in 2025 and demonstrating a robust Compound Annual Growth Rate (CAGR) of 7.3% throughout the forecast period of 2025-2033. This upward trajectory is primarily fueled by the increasing prevalence of thoracic surgeries, driven by a higher incidence of cardiovascular diseases, lung cancer, and other respiratory conditions. Advancements in surgical techniques, including minimally invasive procedures, further necessitate the use of sophisticated thoracic retractors, contributing to market demand. The growing adoption of these devices in ambulatory surgery centers and specialized clinics, alongside traditional hospitals, highlights a broadening application base. The market's expansion is also supported by investments in healthcare infrastructure, particularly in emerging economies, and the continuous innovation by leading manufacturers like B. Braun, Teleflex, and Medtronic, who are introducing enhanced designs for improved patient outcomes and surgeon ergonomics.

The Thoracic Retractor market is characterized by a dynamic landscape with key drivers such as the aging global population, which leads to a higher susceptibility to thoracic ailments, and the increasing demand for sophisticated surgical instruments that enable precision and efficiency. While the market enjoys strong growth, certain restraints may emerge, such as the high cost of advanced retractor systems and the potential for reimbursement challenges in some regions. However, the overwhelming positive outlook is sustained by the consistent development of new product lines and the strategic collaborations among key players to enhance market reach and product development. The dominant presence of North America and Europe in the market is expected to continue, owing to well-established healthcare systems and a higher adoption rate of advanced surgical technologies. Asia Pacific is anticipated to be the fastest-growing region, driven by increasing healthcare expenditure and a growing number of surgical procedures. The market segments of Stainless Steel and Aluminium retractors are expected to lead in terms of volume, with Titanium alloys gaining traction for specialized applications due to their superior strength-to-weight ratio.

This comprehensive report delves into the intricate dynamics of the global Thoracic Retractor market, projecting a significant expansion from a market value of approximately \$500 million in the historical period of 2019-2024 to an estimated \$1,200 million by the end of the forecast period in 2033. The Base Year of 2025 will see the market valued at an estimated \$700 million, providing a crucial benchmark for understanding the trajectory of this essential surgical instrument. This analysis offers an in-depth exploration of market trends, driving forces, challenges, key regional and segmental dominance, growth catalysts, leading players, and significant industry developments. The Study Period encompasses 2019-2033, with a particular focus on the Forecast Period of 2025-2033, offering a robust outlook for stakeholders.

The thoracic retractor market is experiencing a nuanced yet consistently upward trend, driven by a confluence of factors that are reshaping surgical practices and patient care. The increasing prevalence of minimally invasive cardiac surgery (MICS) and other thoracic procedures is a primary accelerator, necessitating advanced retraction solutions that offer superior visualization and access while minimizing tissue trauma. This shift towards less invasive techniques has fueled innovation in retractor design, leading to the development of more specialized and user-friendly devices. The growing adoption of sophisticated surgical tools, coupled with an expanding patient base requiring thoracic interventions, particularly in aging populations with a higher incidence of cardiovascular and respiratory diseases, forms a bedrock of sustained demand. Furthermore, advancements in material science are leading to the introduction of lighter, stronger, and more biocompatible retractors, such as those made from Titanium Alloy, enhancing surgeon confidence and patient outcomes. The market is also witnessing a steady integration of ergonomic designs and automated functionalities, aiming to reduce surgeon fatigue during lengthy procedures and improve overall surgical efficiency. The projected growth is not merely a quantitative expansion but also reflects a qualitative evolution in the type of retractors being favored, moving towards integrated systems that can adapt to diverse anatomical variations and surgical approaches. This trend underscores a market that is both responsive to current surgical needs and proactively anticipating future advancements in thoracic surgery. The estimated market value in the Estimated Year of 2025 is approximately \$700 million, signaling a robust foundation for the projected growth.

The thoracic retractor market's robust growth is underpinned by several powerful driving forces, primarily stemming from the evolving landscape of medical technology and patient demographics. A significant catalyst is the escalating global burden of cardiovascular and respiratory diseases. Conditions such as coronary artery disease, lung cancer, and chronic obstructive pulmonary disease necessitate surgical interventions, directly increasing the demand for thoracic retractors. As healthcare infrastructure improves and access to advanced surgical care expands, particularly in emerging economies, the volume of thoracic procedures is expected to rise substantially. Furthermore, the relentless pursuit of less invasive surgical techniques across all medical disciplines profoundly impacts the thoracic retractor market. Surgeons are increasingly opting for minimally invasive approaches, which require specialized retractors that provide precise tissue retraction with minimal disruption. This trend not only enhances patient recovery times and reduces post-operative complications but also drives innovation in retractor design, leading to the development of more sophisticated and application-specific instruments. The growing number of ambulatory surgery centers (ASCs) also contributes to market expansion, as these facilities are increasingly equipped to handle a wider range of surgical procedures, including those requiring thoracic retractors, often at a lower cost compared to traditional hospital settings. The ongoing technological advancements, including the integration of robotics and enhanced imaging capabilities in surgical suites, further necessitate compatible and advanced retractor systems, creating a synergistic effect on market growth.

Despite the promising growth trajectory, the thoracic retractor market is not without its challenges and restraints. A primary concern is the high cost of advanced retractor systems. While innovative designs and materials offer significant benefits, they often come with a premium price tag, which can be a barrier to adoption, especially for smaller healthcare facilities or in regions with limited healthcare budgets. This cost factor can influence purchasing decisions, leading some institutions to opt for more traditional or basic retractor models. Another significant restraint is the need for specialized training and expertise for operating advanced retractor systems. Surgeons and surgical teams require adequate training to effectively utilize the full capabilities of these sophisticated instruments, ensuring optimal patient outcomes. The learning curve associated with new technologies can slow down their widespread implementation. Furthermore, stringent regulatory approvals and lengthy clearance processes for new medical devices can impede the timely introduction of innovative thoracic retractors into the market. Manufacturers must navigate complex regulatory frameworks in different regions, which can be time-consuming and resource-intensive. The risk of complications and adverse events, although rare with proper use, remains a persistent concern in any surgical instrument. Issues such as tissue damage, nerve injury, or infection, however infrequent, can lead to recalls, lawsuits, and a decline in market confidence. Finally, reimbursement policies and their variability across different healthcare systems can also impact the adoption rates of advanced thoracic retractors, as they influence the financial viability of surgical procedures for healthcare providers.

The global thoracic retractor market is poised for significant growth, with particular dominance expected from Hospitals as a key application segment and North America as a leading region. The Hospitals segment is projected to maintain its leading position throughout the forecast period, from 2025 to 2033. This dominance is attributable to several factors. Hospitals, particularly large tertiary care centers and teaching hospitals, are at the forefront of performing complex thoracic surgeries, including cardiac surgeries, thoracic oncology procedures, and complex reconstructive operations. These institutions are equipped with the latest technology, possess highly specialized surgical teams, and have the financial resources to invest in premium thoracic retractors that offer advanced features and superior performance. The increasing volume of patient admissions for thoracic conditions, coupled with the preference for advanced surgical interventions in a hospital setting, directly translates into sustained demand for a wide array of thoracic retractors. The ongoing trend of centralization of specialized surgical procedures in hospitals further consolidates this segment's dominance.

In terms of regional dominance, North America, encompassing the United States and Canada, is anticipated to continue its leadership in the thoracic retractor market. This leadership is driven by a confluence of factors, including a high prevalence of cardiovascular and respiratory diseases, a well-established healthcare infrastructure, significant healthcare expenditure, and a strong emphasis on technological innovation and adoption. The region boasts a large number of advanced medical facilities, a high density of board-certified thoracic surgeons, and a favorable reimbursement landscape for complex procedures. The robust research and development ecosystem in North America also fosters the continuous introduction of novel thoracic retractor designs and technologies, which are readily adopted by the market. Furthermore, the increasing aging population in North America contributes to a higher incidence of conditions requiring thoracic surgery, thereby fueling market demand. The focus on patient outcomes and the adoption of minimally invasive surgical techniques are also significantly higher in this region, further reinforcing the demand for sophisticated retractor solutions. While other regions like Europe and Asia-Pacific are also experiencing substantial growth, North America's established infrastructure, high healthcare spending, and early adoption of new technologies are likely to keep it at the forefront of the thoracic retractor market throughout the study period.

The thoracic retractor industry is energized by several key growth catalysts. The escalating global prevalence of chronic diseases, particularly cardiovascular and respiratory ailments, is a fundamental driver, necessitating a greater number of surgical interventions. Concurrently, the unwavering advancement in surgical techniques, with a pronounced shift towards minimally invasive procedures, demands more sophisticated and adaptable retractor systems. Furthermore, continuous technological innovation in materials science and device engineering is yielding lighter, stronger, and more precise retractors, enhancing surgical efficacy and patient safety. The expansion of healthcare infrastructure, especially in emerging economies, coupled with increasing disposable incomes, is broadening access to advanced surgical care, thereby amplifying the market for thoracic retractors.

This report offers an exhaustive examination of the thoracic retractor market, providing stakeholders with critical insights and actionable intelligence. It delves into the market size and segmentation, offering detailed projections from the Study Period of 2019-2033, with a strong focus on the Forecast Period of 2025-2033, using 2025 as the Base Year and Estimated Year. The analysis meticulously covers market drivers, restraints, opportunities, and challenges, offering a nuanced understanding of the competitive landscape. Regional analysis provides a granular view of market dynamics across key geographies, while segment-wise analysis details trends in Type (Stainless Steel, Aluminium, Titanium Alloy, Others) and Application (Hospitals, Ambulatory Surgery Centers, Clinics, Others). Furthermore, the report highlights significant industry developments, strategic initiatives of leading players, and emerging technological advancements, equipping readers with a comprehensive perspective to navigate this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.3% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.3%.

Key companies in the market include B. Braun, Teleflex, Integra LifeSciences, Sklar Corporation, Medline, Vitalcor, Surtex Instruments, Mediflex, Medtronic, .

The market segments include Type, Application.

The market size is estimated to be USD 497 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Thoracic Retractor," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Thoracic Retractor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.