1. What is the projected Compound Annual Growth Rate (CAGR) of the SUV Connector?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

SUV Connector

SUV ConnectorSUV Connector by Type (Wire to Wire Connector, Wire to Board Connector, Board to Board Connector, World SUV Connector Production ), by Application (CCE, Powertrain, Safety & Security, Body Wiring & Power Distribution, Others, World SUV Connector Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

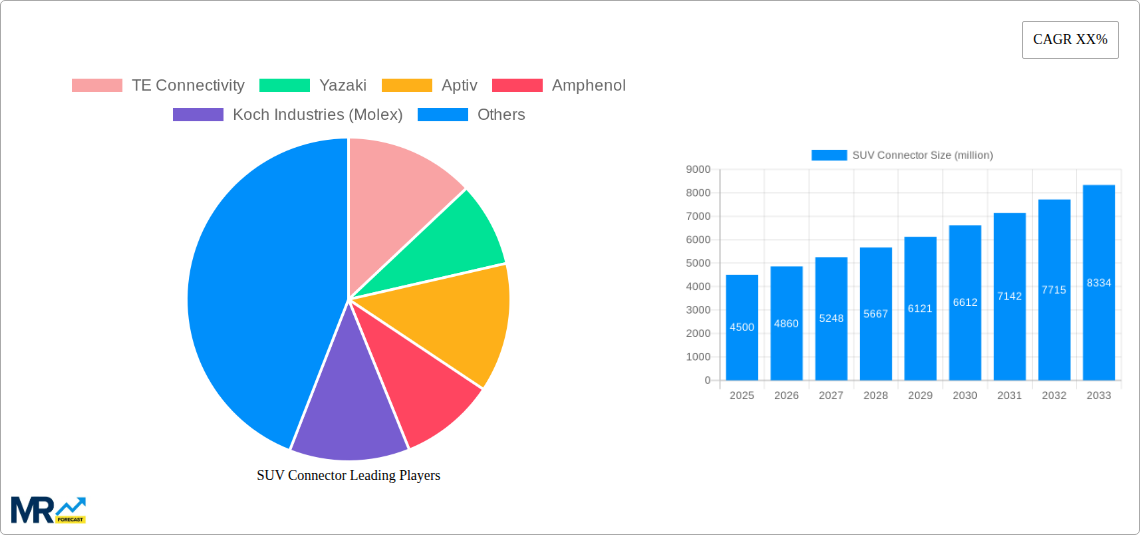

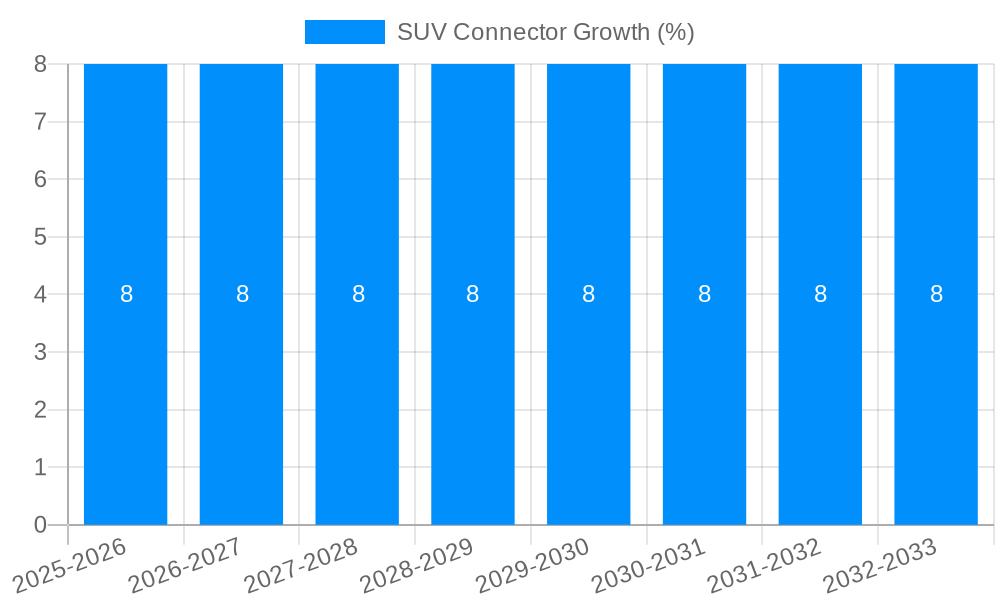

The global SUV connector market is experiencing robust growth, projected to reach a significant valuation of approximately $4,500 million by 2025, with a compound annual growth rate (CAGR) of around 8% anticipated through 2033. This expansion is primarily fueled by the escalating demand for Sports Utility Vehicles (SUVs) globally, driven by evolving consumer preferences for larger, more versatile, and feature-rich vehicles. The increasing integration of advanced automotive technologies, including sophisticated infotainment systems, enhanced safety features like advanced driver-assistance systems (ADAS), and complex powertrain electronics, necessitates a higher number and greater sophistication of connectors. Furthermore, the electrification trend within the SUV segment, with the rise of hybrid and fully electric SUVs, is a major catalyst, requiring specialized high-voltage and data connectors for battery management systems, charging infrastructure, and electric powertrains. The production of World SUV Connectors is thus directly tied to the overall health and technological advancements within the SUV industry.

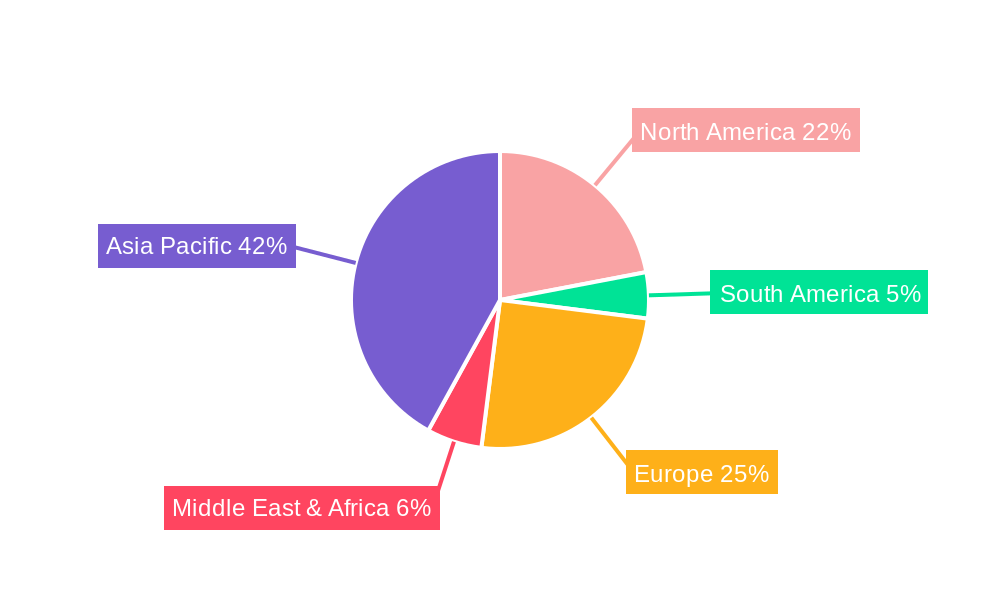

Key segments driving this market include Wire to Wire Connectors, Wire to Board Connectors, and Board to Board Connectors, each playing a crucial role in the intricate electrical and electronic architecture of modern SUVs. Applications such as Connectivity & Entertainment (CCE), Powertrain, Safety & Security, and Body Wiring & Power Distribution are experiencing substantial connector adoption. Geographically, Asia Pacific, led by China, is emerging as a dominant region due to its massive automotive manufacturing base and burgeoning SUV sales. North America and Europe also represent substantial markets, driven by a strong existing SUV fleet and the rapid adoption of new automotive technologies. However, challenges such as the increasing complexity of connector designs, stringent regulatory requirements for safety and performance, and the need for supply chain resilience in the face of potential disruptions could pose restraints to the market. Key players like TE Connectivity, Yazaki, Aptiv, and Amphenol are at the forefront, actively investing in research and development to meet these evolving demands.

Here is a unique report description for "SUV Connectors," incorporating your requested elements:

The global SUV connector market is poised for a significant surge, driven by escalating SUV production and the increasing complexity of automotive electronics. XXX anticipates the market to reach an astounding value of USD 12,500 million by 2033, up from an estimated USD 7,800 million in 2025. This growth is intricately linked to the evolving automotive landscape, where SUVs continue to capture a dominant share of global vehicle sales. The proliferation of advanced driver-assistance systems (ADAS), sophisticated infotainment, and enhanced powertrain technologies within SUVs necessitates a robust and reliable connector infrastructure. Wire to wire connectors remain the backbone of automotive electrical systems, but the demand for wire to board and board to board connectors is rapidly expanding as vehicles integrate more complex printed circuit boards (PCBs) for various electronic control units (ECUs). The historical period (2019-2024) has witnessed steady growth, fueled by the initial adoption of electrification and connectivity features. The base year of 2025 marks a pivotal point, with the market expected to accelerate significantly in the forecast period (2025-2033) as major automotive manufacturers push forward with ambitious electrification targets and introduce a higher degree of technological integration in their SUV offerings. Factors such as stringent safety regulations, consumer demand for premium features, and the ongoing transition towards autonomous driving functionalities will further solidify the upward trajectory of this market. The increasing emphasis on lightweighting and space optimization within vehicles also places a premium on compact and high-performance connector solutions, driving innovation in materials and design. The sheer volume of SUVs rolling off production lines globally, combined with the intrinsic need for more electrical connections per vehicle, paints a picture of robust and sustained expansion for the SUV connector industry.

The automotive industry's unwavering commitment to electrification stands as a primary propellant for the SUV connector market. As consumers increasingly embrace hybrid and fully electric SUVs, the demand for specialized, high-voltage, and high-performance connectors escalates dramatically. These connectors are crucial for the safe and efficient operation of battery systems, power inverters, and charging infrastructure within electric SUVs. Furthermore, the relentless pursuit of enhanced safety features, including advanced driver-assistance systems (ADAS) like adaptive cruise control, lane-keeping assist, and automated emergency braking, mandates a substantial increase in the number and type of connectors employed. Each sensor, camera, and radar unit requires secure and reliable electrical pathways, directly impacting connector demand. The integration of sophisticated in-car entertainment and connectivity solutions, ranging from large touchscreens and advanced navigation systems to seamless smartphone integration and over-the-air updates, further contributes to the growing connector footprint within SUVs. This trend is amplified by consumer expectations for a highly personalized and connected driving experience, pushing manufacturers to pack more electronic modules into their vehicles.

Despite the promising growth outlook, the SUV connector market faces several significant challenges and restraints. The increasingly stringent regulatory landscape surrounding automotive electronics and safety standards can create hurdles for manufacturers, requiring continuous investment in research and development to ensure compliance. The rapid pace of technological evolution also presents a challenge; connectors must not only meet current demands but also be adaptable to future advancements in vehicle architecture and functionality. Supply chain volatility, exacerbated by geopolitical events and raw material price fluctuations, can impact production costs and lead times, potentially affecting market stability. Moreover, the miniaturization trend, while a driver of innovation, also demands more sophisticated manufacturing processes and higher precision, which can increase production complexity and costs. The significant capital investment required for developing and producing advanced connector solutions, particularly those designed for high-voltage and extreme environmental conditions, can also act as a barrier to entry for smaller players and necessitate substantial financial backing for established companies. Finally, the competitive intensity within the market, with numerous established global players, can lead to price pressures and the need for continuous differentiation through technological innovation and cost-efficiency.

The Asia-Pacific region, particularly China, is poised to be a dominant force in the global SUV connector market, driven by its massive automotive production volume and a rapidly growing demand for SUVs. China's robust manufacturing ecosystem, coupled with its strong governmental support for the automotive industry and a burgeoning middle class with increasing purchasing power for SUVs, creates a fertile ground for connector suppliers. The region’s leading position is further bolstered by its significant role in electric vehicle (EV) production, a segment intrinsically linked to higher connector volumes and specialized requirements.

Within the segments, the Body Wiring & Power Distribution segment is expected to be a substantial contributor to market dominance.

The convergence of these factors, especially the sheer volume of SUV production in Asia-Pacific and the critical role of Body Wiring & Power Distribution, Powertrain, and Safety & Security segments, positions these as the key drivers of market dominance.

The SUV connector industry is fueled by several powerful growth catalysts. The accelerating global trend of vehicle electrification, with SUVs leading the charge in adoption rates, is a primary driver. Increased integration of advanced driver-assistance systems (ADAS) and autonomous driving technologies necessitates more complex and higher-performance connectors for sensors, cameras, and ECUs. Furthermore, the consumer demand for advanced infotainment, connectivity features, and personalized in-car experiences continuously pushes for more electronic integration, thereby increasing the connector footprint. Finally, stringent automotive safety regulations and evolving emission standards compel manufacturers to adopt more sophisticated electronic control systems, all of which rely heavily on a robust connector infrastructure.

This comprehensive report provides an in-depth analysis of the global SUV connector market, covering the historical period from 2019 to 2024 and projecting growth through to 2033, with a base year of 2025. The study meticulously examines key market trends, including the evolving demand for wire to wire, wire to board, and board to board connectors, driven by the increasing complexity of SUV electronics across applications like CCE, Powertrain, Safety & Security, and Body Wiring & Power Distribution. It delves into the significant driving forces such as vehicle electrification and ADAS adoption, alongside critical challenges like supply chain volatility and technological evolution. The report also highlights dominant regions and segments, offering strategic insights into market leadership. Furthermore, it identifies key growth catalysts and provides a detailed overview of leading players and their significant developments, offering a holistic understanding of the SUV connector industry's past, present, and future trajectory.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include TE Connectivity, Yazaki, Aptiv, Amphenol, Koch Industries (Molex), Sumitomo, JAE, KET, JST, Rosenberger, LUXSHARE, AVIC Jonhon, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "SUV Connector," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the SUV Connector, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.