1. What is the projected Compound Annual Growth Rate (CAGR) of the Stationary Incinerator?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Stationary Incinerator

Stationary IncineratorStationary Incinerator by Type (Vertical, Horizontal), by Application (Mining, Waste Disposal, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

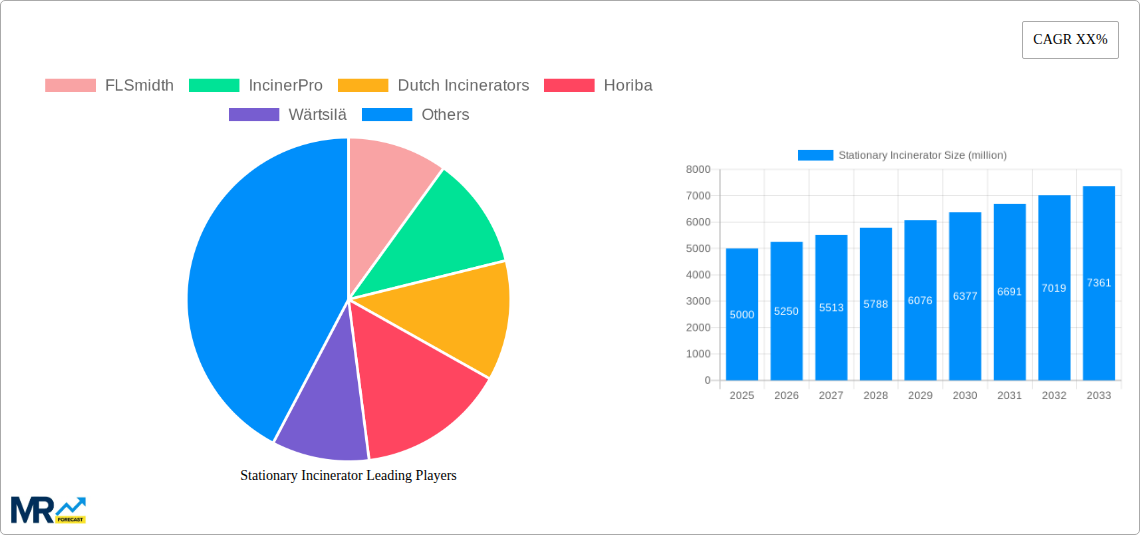

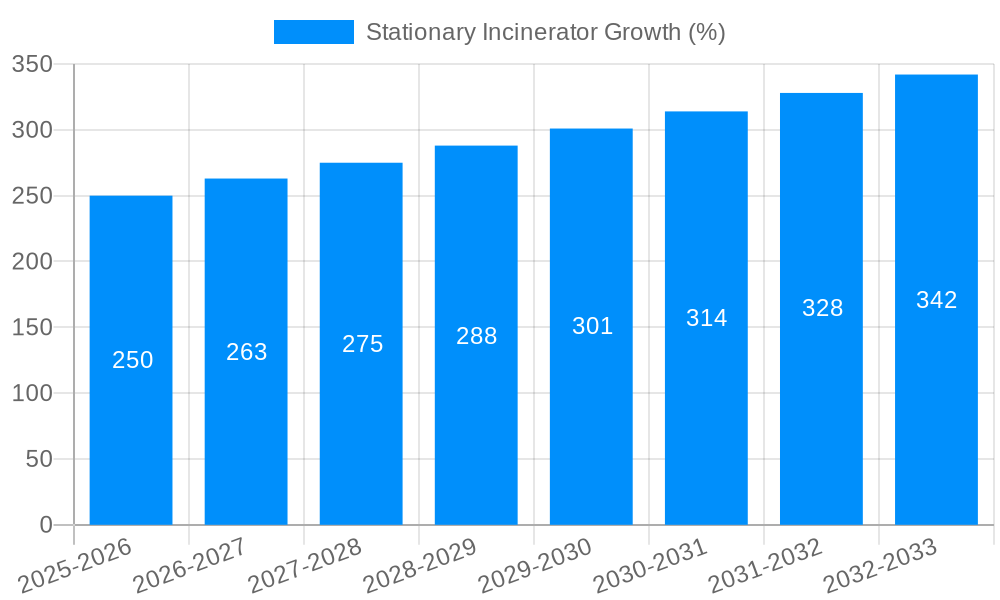

The stationary incinerator market is experiencing robust growth, driven by increasing waste generation, stringent environmental regulations promoting waste-to-energy solutions, and advancements in incineration technologies offering higher efficiency and reduced emissions. The market size, while not explicitly stated, can be reasonably estimated based on industry trends and the presence of major players like FLSmidth, Wärtsilä, and others. Considering similar markets and typical CAGR values for industrial equipment, a plausible market size in 2025 could be around $5 billion. A compound annual growth rate (CAGR) of 5-7% seems realistic for the forecast period (2025-2033), indicating continuous expansion. Key drivers include the need for efficient waste management in densely populated areas, rising energy costs motivating waste-to-energy projects, and stricter regulations on landfill disposal. Emerging trends such as improved air pollution control technologies, advanced waste sorting systems to maximize energy recovery, and the integration of smart technologies for monitoring and optimizing incineration processes are significantly impacting market growth. Potential restraints include high initial investment costs associated with incinerator installation, public concerns regarding potential environmental impacts, and the need for skilled labor to operate and maintain these complex systems. Market segmentation likely includes variations based on incinerator capacity, waste type handled, and geographical location.

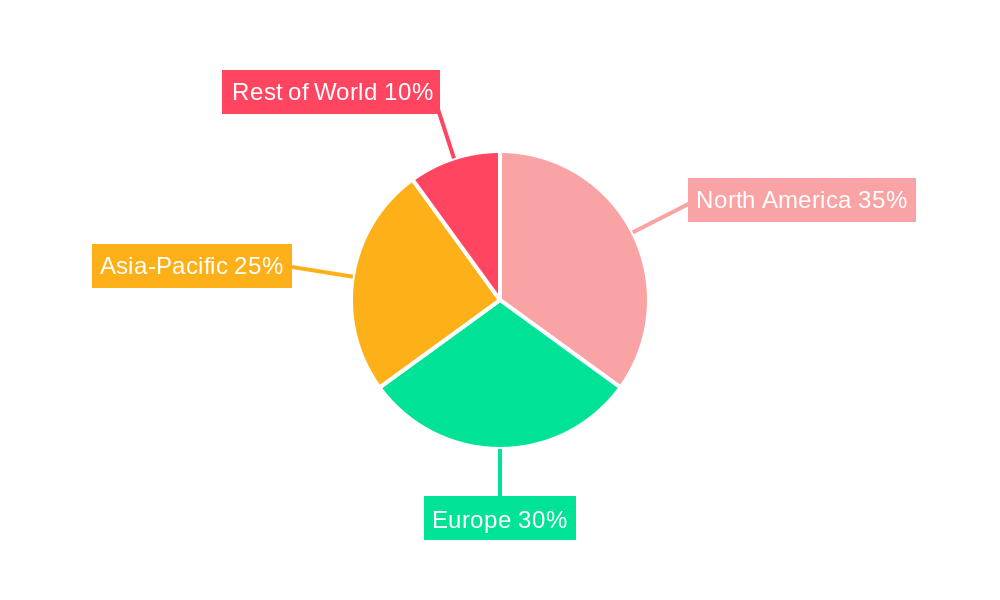

The competitive landscape is moderately concentrated, with established players such as FLSmidth, IncinerPro, Dutch Incinerators, Horiba, Wärtsilä, Takuma, and Thermax holding significant market shares. These companies are focusing on technological innovations, strategic partnerships, and geographic expansion to maintain a competitive edge. The future will likely see continued consolidation through mergers and acquisitions, along with increased focus on sustainability and circular economy principles within the industry. The market presents lucrative opportunities for companies offering advanced, eco-friendly incineration technologies and comprehensive waste management solutions. Regional variations in market growth will depend on factors such as waste generation patterns, regulatory frameworks, and economic development levels. North America and Europe are expected to be leading markets, but significant growth potential exists in Asia-Pacific and other emerging economies.

The global stationary incinerator market is experiencing a period of significant transformation, driven by a complex interplay of factors. Over the study period (2019-2033), the market has shown robust growth, exceeding several million units in annual sales by 2025 (estimated year). This expansion is projected to continue throughout the forecast period (2025-2033), although at a potentially moderated pace compared to the historical period (2019-2024), which saw particularly strong growth fueled by increasing waste generation and stringent environmental regulations in several key regions. The market's trajectory is intricately linked to the evolving regulatory landscape, with stricter emission standards prompting a shift towards more efficient and environmentally friendly incineration technologies. This has created opportunities for companies offering advanced incineration systems equipped with emission control technologies like scrubbers and filters, which significantly reduce air pollutants. However, growing public concern about potential environmental risks associated with incineration, especially the release of dioxins and furans, poses a challenge. This has led to increased scrutiny of incineration projects, necessitating robust environmental impact assessments and public consultations before project approval. Consequently, market growth is also influenced by the availability of sustainable alternatives like waste-to-energy (WtE) technologies and advancements in recycling and composting infrastructure. The competitive landscape is dynamic, with established players like FLSmidth and Wärtsilä vying for market share with newer entrants offering innovative solutions. Further diversification is expected, with several niche players focusing on specialized incinerator types for specific waste streams. The overall market outlook remains positive, albeit contingent upon continued technological innovation and the effective management of environmental and regulatory considerations.

Several factors are significantly contributing to the growth of the stationary incinerator market. The ever-increasing volume of municipal solid waste (MSW) globally is a primary driver. As urbanization accelerates and populations grow, so does the amount of waste generated, creating a critical need for efficient waste management solutions. Incineration, especially when integrated with energy recovery systems, offers an attractive method for reducing landfill burden and generating renewable energy. Stricter environmental regulations regarding landfill disposal and waste management in many countries are also pushing the adoption of incineration as a cleaner alternative. Regulations limiting the amount of waste sent to landfills and mandating waste-to-energy solutions are key catalysts for growth. The economic benefits associated with incineration, such as the generation of electricity or steam from waste heat, are further bolstering its attractiveness. This is particularly important in regions with limited access to other forms of energy, creating a favorable cost-benefit equation for incineration facilities. Furthermore, technological advancements in incinerator design and emission control have mitigated some of the environmental concerns associated with traditional incineration methods. Modern incinerators incorporate advanced technologies to minimize emissions and maximize energy recovery, enhancing their viability and appeal in the market.

Despite the positive market trends, several challenges and restraints hinder the widespread adoption of stationary incinerators. Public opposition remains a significant hurdle. Concerns about air pollution, potential health risks from emissions, and the aesthetic impact of incinerator facilities often lead to protests and delays in project implementation. This necessitates extensive public engagement and transparent communication strategies from developers. The high initial capital investment required for constructing incineration plants can be prohibitive, especially for smaller municipalities or developing countries. Securing funding and attracting investors can be a complex process. Furthermore, stringent environmental regulations and the need for advanced emission control technologies increase the overall cost of incineration. Compliance with these regulations demands significant investment in equipment and ongoing maintenance, potentially impacting the financial viability of projects. Competition from alternative waste management technologies, such as advanced recycling processes, anaerobic digestion, and waste-to-biofuel conversion, presents a challenge. These alternatives offer potentially more environmentally sustainable solutions, diverting waste away from incineration. Lastly, the scarcity of suitable locations for incineration plants, due to zoning regulations and proximity to residential areas, can further restrict market growth.

Several regions and segments are expected to drive the growth of the stationary incinerator market.

Developed Nations: Countries in North America, Europe, and parts of Asia-Pacific with robust economies, established waste management infrastructure, and stringent environmental regulations will continue to lead the market. These regions are characterized by high waste generation rates and a willingness to invest in advanced waste management technologies. The demand for efficient waste management and energy recovery is driving the adoption of advanced incineration technologies. In particular, countries with stringent environmental regulations and a focus on sustainable energy solutions are particularly active.

Emerging Economies: While initially slower, emerging economies in Asia, South America, and Africa present significant growth potential. Rapid urbanization and increasing waste generation are forcing these regions to invest in improved waste management solutions. The adoption may initially focus on less expensive, smaller scale facilities, before eventually leading to larger, more sophisticated projects as the demand grows.

Segments: The industrial waste segment is anticipated to experience significant growth, fueled by the increasing industrialization in developing countries and the rising demand for safe and efficient disposal of hazardous industrial wastes. This contrasts with the municipal solid waste segment, which while still growing, may show slightly slower growth rates. The healthcare waste segment is also critical; it requires specialized incineration technologies capable of handling infectious and biomedical waste materials.

The overall dominance will depend on the balance of various factors, including economic development, environmental policies, and waste management strategies.

The stationary incinerator industry is propelled by several key factors: increasing waste generation, stringent environmental regulations, the economic benefits of energy recovery, technological advancements in emission control, and the growing awareness of the need for sustainable waste management practices. These elements combine to create a strong market outlook.

This report offers a comprehensive analysis of the stationary incinerator market, providing valuable insights into current trends, driving forces, challenges, leading players, and future growth prospects. It offers detailed segmentation, geographical analysis, and a forecast for the coming decade, allowing stakeholders to make informed decisions. The report's robust methodology combines market research data, expert interviews, and thorough analysis to provide a reliable and accurate picture of this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include FLSmidth, IncinerPro, Dutch Incinerators, Horiba, Wärtsilä, Takuma, Thermax, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Stationary Incinerator," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Stationary Incinerator, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.