1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Automotive Headlights?

The projected CAGR is approximately 12%.

Smart Automotive Headlights

Smart Automotive HeadlightsSmart Automotive Headlights by Type (Adaptive Front Lighting Headlight, Adaptive Driving Beam Headlight, World Smart Automotive Headlights Production ), by Application (OEM, Aftermarket, World Smart Automotive Headlights Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

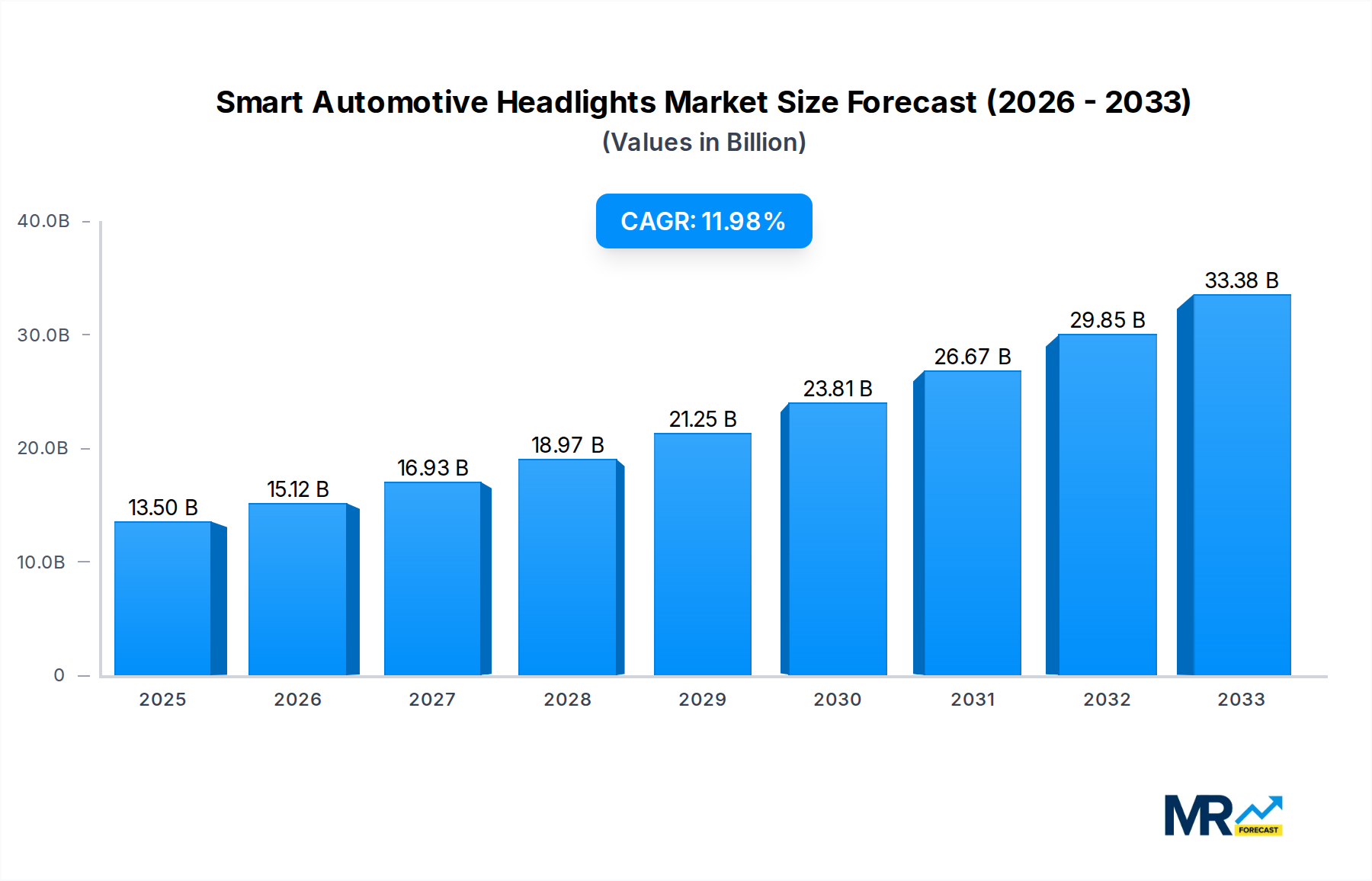

The global Smart Automotive Headlights market is experiencing robust expansion, projected to reach approximately $13.5 billion by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 12% anticipated through 2033. This growth is primarily fueled by the increasing adoption of advanced driver-assistance systems (ADAS) and the growing consumer demand for enhanced vehicle safety and comfort features. Smart headlights, encompassing technologies like Adaptive Front Lighting (AFL) and Adaptive Driving Beams (ADB), play a crucial role in improving visibility, reducing glare for oncoming drivers, and contributing to overall road safety. The OEM segment is expected to dominate the market, driven by automotive manufacturers integrating these sophisticated lighting solutions as standard or optional features in new vehicle models. Technological advancements in LED and laser lighting, coupled with the integration of sensors and AI for real-time adjustments, are key enablers of this market surge.

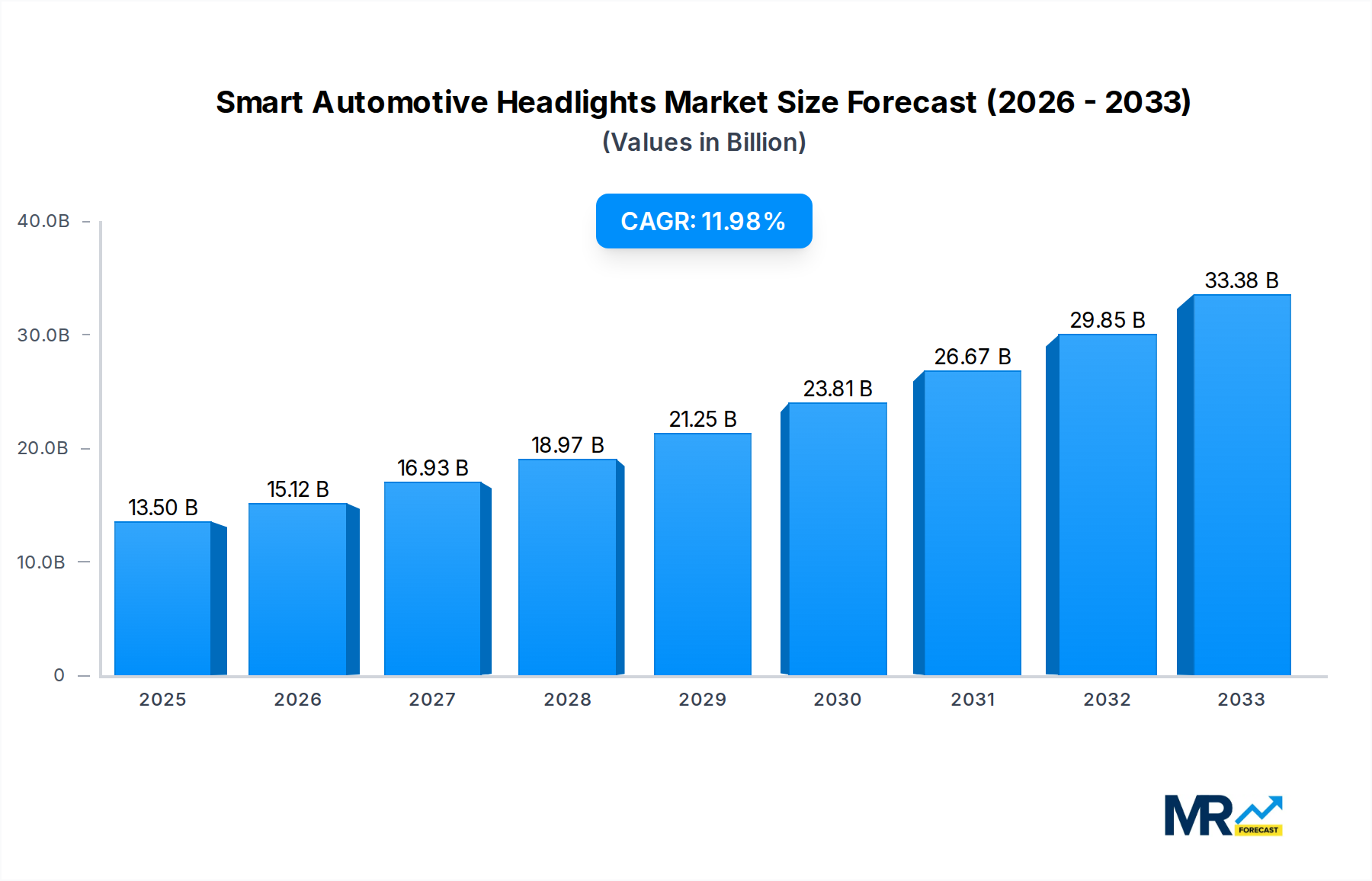

The market's trajectory is further shaped by evolving regulatory landscapes and consumer expectations for premium automotive experiences. While the market benefits from strong drivers such as safety regulations and technological innovation, potential restraints include the high cost of implementation for some advanced features and the need for significant R&D investment by manufacturers. However, the increasing production of vehicles equipped with smart lighting, coupled with a growing aftermarket for upgrades, underscores the market's resilience and potential. Asia Pacific is poised to be a significant growth engine, driven by the burgeoning automotive industry in China and India, followed closely by Europe and North America, where stringent safety standards and a high adoption rate of new technologies are prevalent. Key players like Koito, Valeo, Marelli, and Hella are actively investing in R&D to capture market share and introduce innovative solutions in this dynamic sector.

This comprehensive report delves into the rapidly evolving global Smart Automotive Headlights market, projecting a robust expansion trajectory. The market is anticipated to witness substantial growth, driven by increasing adoption of advanced automotive technologies and stringent safety regulations. The study period spans from 2019 to 2033, with a base year of 2025 and an estimated year also of 2025, providing an in-depth analysis of the historical landscape (2019-2024) and a detailed forecast for the period 2025-2033. The market is expected to reach an impressive valuation of hundreds of billions of USD by the end of the forecast period, signifying a significant economic impact. Key segments analyzed include the types of smart headlights such as Adaptive Front Lighting Headlights and Adaptive Driving Beam Headlights, alongside the primary applications in OEM and Aftermarket. The report provides critical insights into the production volumes and industry developments shaping this dynamic sector.

The global Smart Automotive Headlights market is experiencing a transformative era, characterized by an insatiable demand for enhanced safety, improved driving visibility, and the integration of sophisticated automotive features. XXX, a prominent trend observed is the escalating adoption of Adaptive Driving Beam (ADB) technology. This advanced system, which can selectively dim sections of the headlight beam to avoid dazzling oncoming or preceding drivers while illuminating the rest of the road, is no longer a luxury feature but is increasingly becoming a standard in premium and mid-range vehicles. The market is witnessing a paradigm shift from conventional lighting solutions to intelligent systems that offer dynamic and context-aware illumination. Furthermore, the integration of Artificial Intelligence (AI) and sensor fusion is becoming a cornerstone of smart headlight development, enabling these systems to react to changing road conditions, weather, and the presence of other road users with unprecedented precision. The increasing regulatory push for enhanced road safety, particularly in regions like Europe and North America, is a significant catalyst, mandating features that reduce accident risks. This regulatory impetus is directly translating into higher production volumes for smart automotive headlights. The OEM segment is expected to continue its dominance, as manufacturers embed these advanced lighting solutions to differentiate their offerings and meet evolving consumer expectations for intelligent vehicle features. The aftermarket segment, while currently smaller, is poised for significant growth as older vehicles are retrofitted with these advanced technologies and as repair and replacement needs arise for vehicles already equipped with smart headlights. The development of advanced materials and manufacturing processes is also contributing to cost reduction and performance enhancement, making smart headlights more accessible and driving broader market penetration. The competitive landscape is intensifying, with established players investing heavily in research and development to stay ahead of the curve.

Several potent forces are propelling the Smart Automotive Headlights market towards unprecedented growth. Foremost among these is the unwavering global emphasis on automotive safety. As road fatalities remain a critical concern, governments and regulatory bodies worldwide are actively encouraging or mandating advanced driver-assistance systems (ADAS), with smart headlights playing a pivotal role in enhancing nighttime visibility and reducing glare for other drivers. This translates directly into a demand for sophisticated lighting technologies. Secondly, the rapid advancement and miniaturization of sensor technologies, coupled with the decreasing cost of processing power, have made the integration of complex smart headlight functions more economically viable for automakers. Features such as matrix LED technology, laser headlights, and predictive lighting, which adjust the beam based on navigation data, are becoming increasingly feasible. Thirdly, the evolving consumer preference for technologically advanced and feature-rich vehicles is a significant driver. Consumers are increasingly associating advanced lighting with superior vehicle quality and safety, creating a pull effect for smart headlights. The luxury and premium segments are leading this trend, but it is rapidly cascading down to mid-segment vehicles. Finally, the growing sophistication of autonomous driving systems creates a symbiotic relationship with smart headlights. These intelligent lighting systems can provide crucial real-time data to the vehicle’s perception system, contributing to a more comprehensive understanding of the driving environment.

Despite the robust growth potential, the Smart Automotive Headlights market faces certain challenges and restraints that could temper its trajectory. One significant hurdle is the high initial cost of implementation. Advanced smart headlight systems, with their complex electronics, sensors, and sophisticated software, are considerably more expensive than traditional halogen or even basic LED headlights. This cost can be a deterrent for mass-market adoption, particularly in price-sensitive regions or for entry-level vehicle segments. Another challenge lies in the complexity of integration and calibration. Integrating these advanced lighting systems into a vehicle's existing electrical architecture and ensuring accurate calibration requires specialized expertise and rigorous testing, adding to development timelines and costs for automotive manufacturers. Maintenance and repair costs also present a potential restraint. If a component within a complex smart headlight system fails, replacing the entire module can be significantly more expensive than replacing a traditional bulb. This could lead to higher insurance premiums or deter consumers from opting for these features. Furthermore, regulatory fragmentation and varying standards across different countries can pose challenges for global automakers. Ensuring compliance with diverse safety and performance standards for smart headlights in every target market requires extensive localization and testing efforts. Finally, public perception and understanding of the benefits of smart headlights, while growing, may still lag behind the technological advancements, requiring ongoing education and awareness campaigns.

The global Smart Automotive Headlights market is characterized by regional dominance and segment leadership that will shape its future. In terms of geographical regions, North America and Europe are poised to emerge as the leading markets for smart automotive headlights. This dominance is driven by a confluence of factors, including stringent automotive safety regulations, a high concentration of premium and luxury vehicle manufacturers, and a tech-savvy consumer base that readily embraces advanced automotive technologies. Both regions have proactively implemented safety standards that encourage or mandate advanced lighting features to reduce road accidents, particularly during nighttime driving. The presence of major automotive OEMs with a strong focus on innovation and R&D in these regions further fuels the demand for cutting-edge smart headlight solutions.

Within these leading regions, the OEM segment is undeniably the primary driver of smart automotive headlights production and adoption. Automakers are increasingly integrating these advanced lighting systems as standard or optional features in new vehicle models to enhance vehicle appeal, meet evolving consumer expectations, and comply with safety mandates. The competitive landscape among OEMs often hinges on the inclusion of sophisticated technologies, and smart headlights have become a key differentiator. This segment accounts for the vast majority of smart headlight sales and is expected to maintain its leading position throughout the forecast period.

Delving deeper into the segments by type, the Adaptive Driving Beam (ADB) Headlight segment is predicted to witness the most significant growth and eventually dominate the market. ADB technology, with its ability to precisely control light distribution and avoid dazzling oncoming drivers while maximizing illumination of the road ahead, offers a substantial safety advantage. As the technology matures and becomes more cost-effective, its penetration into mainstream vehicle models will accelerate. The regulatory push for enhanced visibility and glare reduction further bolsters the demand for ADB systems. While Adaptive Front Lighting Headlight (which typically involves cornering lights and automatic leveling) is also a crucial component of smart lighting, ADB’s direct impact on nighttime collision avoidance and driver comfort is expected to drive its market leadership.

The World Smart Automotive Headlights Production metric is intrinsically linked to these regional and segment dynamics. The production volume of smart headlights will be highest in regions with a strong automotive manufacturing base and high demand for advanced features, directly correlating with the dominance of North America and Europe. The OEM segment's need to equip millions of new vehicles annually will dictate the overall production scale. The increasing sophistication of ADB technology, moving from complex mechanical systems to more integrated LED matrix solutions, will also influence production processes and volumes. The Aftermarket segment, while not as dominant in terms of volume as OEM, will contribute to sustained production as vehicles age and require replacements or upgrades, and as consumers seek to enhance the safety and functionality of older vehicles. The overall growth of the smart automotive headlights market will be reflected in a substantial increase in global production figures, reaching into the hundreds of billions of USD in market value.

Several key factors are acting as potent growth catalysts for the Smart Automotive Headlights industry. The relentless pursuit of enhanced automotive safety remains paramount, with smart headlights offering a direct solution to improve visibility and reduce accidents. The continuous technological advancements in LED and laser lighting, coupled with the decreasing costs of sensors and microprocessors, are making these sophisticated systems more accessible and efficient. Furthermore, the increasing demand for premium and connected vehicle features by consumers is driving OEMs to integrate smart lighting as a key differentiator. The growing trend towards autonomous driving necessitates advanced sensing capabilities, where smart headlights can play a complementary role in environmental perception.

This report offers a comprehensive examination of the global Smart Automotive Headlights market, providing invaluable insights for stakeholders across the automotive ecosystem. It delves deeply into market trends, meticulously analyzing the factors driving adoption and the challenges that need to be addressed. The report quantifies the market size and growth projections, presenting data in billions of USD, with a detailed breakdown by segment and region for the study period of 2019-2033. Leading companies are identified and profiled, alongside an in-depth analysis of significant technological advancements and industry developments. The report aims to equip businesses with the strategic intelligence needed to navigate this dynamic market, identify growth opportunities, and make informed decisions to capitalize on the future of automotive lighting.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 12%.

Key companies in the market include Koito, Valeo, Marelli, Hella, Stanley, ZKW Group (LG), SL Corporation, Varroc.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Smart Automotive Headlights," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Smart Automotive Headlights, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.