1. What is the projected Compound Annual Growth Rate (CAGR) of the Sinus Bradycardia Devices?

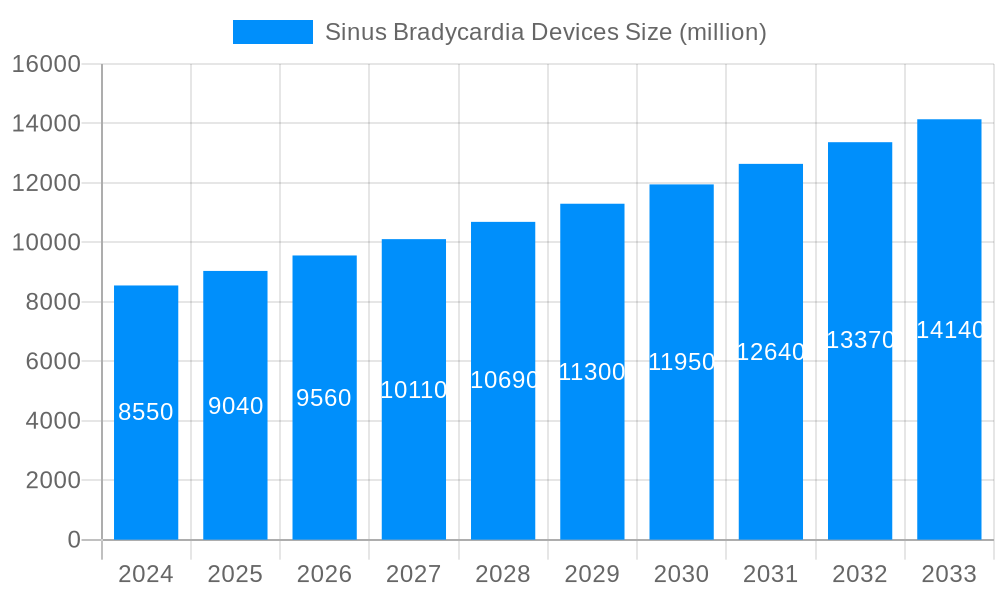

The projected CAGR is approximately 5.85%.

Sinus Bradycardia Devices

Sinus Bradycardia DevicesSinus Bradycardia Devices by Type (Pacemaker, Implantable Cardioverter Defibrillator), by Application (Sinus Cardiac arrest, Sinus Atrial Block, Sinus Node Syndrome, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global market for Sinus Bradycardia Devices is experiencing robust growth, projected to reach a valuation of approximately USD 9.04 billion by 2025. This expansion is driven by an escalating prevalence of cardiovascular diseases, particularly those affecting the heart's natural pacemaker, the sinus node. Factors such as an aging global population, increasing awareness of cardiac health, and advancements in medical technology are contributing significantly to market demand. The rising incidence of conditions like sinus cardiac arrest, sinus atrial block, and sinus node syndrome necessitates more sophisticated and effective treatment solutions, directly fueling the adoption of pacemakers and implantable cardioverter-defibrillators (ICDs). Emerging economies, with their expanding healthcare infrastructure and growing disposable incomes, are also presenting substantial opportunities for market players.

The market is characterized by a compound annual growth rate (CAGR) of 5.6%, indicating a sustained upward trajectory through the forecast period ending in 2033. This steady growth is underpinned by continuous innovation in device miniaturization, battery longevity, and remote monitoring capabilities, enhancing patient outcomes and reducing healthcare burdens. Key players are actively investing in research and development to introduce next-generation devices with improved efficacy and safety profiles. While the market exhibits strong growth, potential restraints include stringent regulatory approvals, high device costs, and the need for skilled implantation professionals. However, the increasing integration of AI and machine learning in device management, along with a growing preference for less invasive procedures, are expected to mitigate these challenges and further propel market expansion.

This report delves into the dynamic global market for Sinus Bradycardia Devices, offering an in-depth analysis from the historical period of 2019-2024 to a projected outlook extending to 2033. With a base year of 2025, the study leverages robust data and expert insights to provide a granular understanding of market trends, drivers, challenges, and future growth trajectories. The market is segmented by device type, application, and regional presence, with a particular focus on key industry developments and the competitive landscape. The total market value is projected to reach hundreds of billions of dollars by the end of the forecast period, underscoring the significant economic and healthcare impact of these life-sustaining technologies.

XXX The global Sinus Bradycardia Devices market is experiencing a significant upswing, driven by a confluence of factors including an aging global population, increasing prevalence of cardiac arrhythmias, and advancements in device technology. The market is projected to witness a compound annual growth rate (CAGR) that will propel its valuation into the hundreds of billions of dollars by 2033. This growth is not uniform across all segments. The Pacemaker segment, in particular, is expected to remain the dominant force, owing to its widespread application in managing symptomatic bradycardia. Innovations such as leadless pacemakers and closed-loop stimulation systems are enhancing patient comfort and therapeutic efficacy, thereby fueling demand. Simultaneously, Implantable Cardioverter Defibrillators (ICDs), while a smaller segment in terms of unit volume, represent a high-value market due to their complex functionality and critical role in preventing sudden cardiac death. The application segment of Sinus Node Syndrome is a primary driver of market expansion, as this condition directly necessitates the use of bradycardia-regulating devices. However, the increasing adoption of these devices for other less severe forms of bradycardia and atrial blocks, categorized under Others, is also contributing to market diversification. Industry-wide, a strong emphasis is being placed on miniaturization, enhanced battery life, and improved remote monitoring capabilities. This trend is not only making devices less invasive but also enabling better post-implantation patient management and reducing hospital readmission rates. The historical data from 2019-2024 indicates a steady growth trajectory, with the base year of 2025 serving as a crucial pivot point for projected future expansion. The forecast period of 2025-2033 is anticipated to see accelerated growth, influenced by increasing healthcare expenditure in developing economies and a growing awareness of the benefits of timely cardiac intervention. Furthermore, the integration of artificial intelligence (AI) and machine learning (ML) in device diagnostics and therapy optimization is poised to revolutionize the market, offering personalized treatment pathways and predictive analytics for patient care. The competitive landscape is characterized by intense innovation and strategic collaborations, with major players vying for market share through product differentiation and geographical expansion.

The Sinus Bradycardia Devices market is propelled by a robust set of driving forces, primarily centered around the escalating global burden of cardiovascular diseases and the consequent demand for effective treatment solutions. The aging demographic worldwide is a fundamental driver; as populations age, the incidence of age-related cardiac conditions, including various forms of bradycardia, naturally increases, leading to a higher patient pool requiring these devices. Furthermore, the rising prevalence of lifestyle-related diseases such as obesity, diabetes, and hypertension, which are significant risk factors for cardiac arrhythmias, is further amplifying the need for advanced bradycardia management. Technological innovation plays a crucial role; continuous research and development efforts are leading to the creation of smaller, less invasive, and more intelligent devices. The advent of leadless pacemakers, for instance, has significantly improved patient outcomes by reducing complications associated with traditional transvenous leads. Similarly, advancements in battery technology are extending device longevity, minimizing the need for replacement surgeries and enhancing patient quality of life. Growing awareness among both healthcare professionals and patients regarding the efficacy and benefits of cardiac rhythm management devices is also a key accelerator. Early diagnosis and timely intervention for symptomatic bradycardia can prevent serious complications and improve survival rates, prompting greater adoption of these sophisticated medical implants. The increasing healthcare expenditure in both developed and developing nations, coupled with favorable reimbursement policies for implantable cardiac devices, further fuels market growth by making these treatments more accessible.

Despite the promising growth trajectory, the Sinus Bradycardia Devices market faces several challenges and restraints that could potentially temper its expansion. A significant hurdle is the high cost of these advanced medical devices. The sophisticated technology and rigorous research and development involved in their creation contribute to substantial price tags, which can limit accessibility, particularly in resource-constrained healthcare systems and for uninsured or underinsured patient populations. This cost factor can also lead to a disparity in access between developed and developing economies. Another considerable challenge is the risk of complications associated with implantation surgery. While minimally invasive techniques are becoming more prevalent, any surgical procedure carries inherent risks such as infection, lead dislodgement, pneumothorax, and device malfunction. These potential complications can lead to patient anxiety, increased healthcare costs due to corrective procedures, and in rare cases, adverse outcomes, thus acting as a deterrent for some individuals and healthcare providers. Regulatory hurdles and stringent approval processes also present a challenge. Medical devices, especially implantable ones, undergo extensive testing and evaluation to ensure safety and efficacy. The lengthy and complex regulatory pathways in different countries can delay product launches and market penetration, thereby restricting the pace of innovation and market growth. Furthermore, limited reimbursement policies in certain regions can hinder the adoption of newer, more advanced, and consequently more expensive devices, as healthcare providers and patients may opt for more cost-effective, albeit less sophisticated, alternatives. The shortage of skilled electrophysiologists and trained healthcare professionals capable of implanting and managing these devices can also act as a bottleneck, particularly in emerging markets where healthcare infrastructure is still developing.

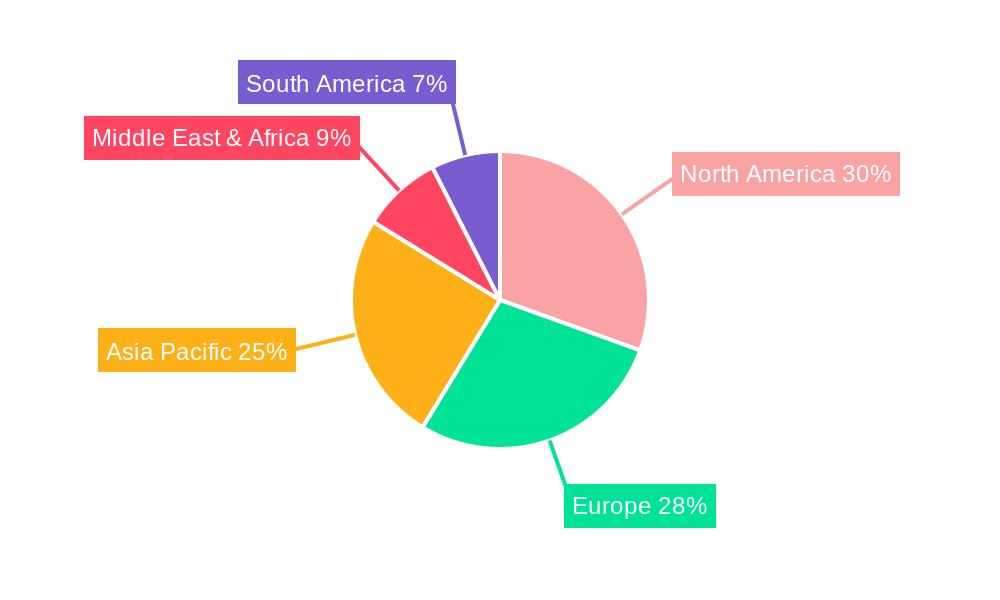

The global Sinus Bradycardia Devices market is characterized by a distinct regional and segment dominance, with North America and Europe currently leading the charge, driven by advanced healthcare infrastructure, high patient awareness, and significant R&D investments. However, the Asia Pacific region is poised for substantial growth, driven by a rapidly expanding middle class, increasing healthcare expenditure, and a growing incidence of cardiac diseases due to lifestyle changes. Within the device Type segmentation, the Pacemaker segment is projected to maintain its dominance throughout the forecast period. This is primarily attributed to the widespread application of pacemakers in managing symptomatic bradycardia, a condition directly addressed by these devices. The continuous innovation in pacemaker technology, including the development of leadless pacemakers and advanced sensing capabilities, further solidifies its market leadership. These devices offer improved patient outcomes, enhanced comfort, and reduced invasiveness, thereby driving their adoption. The Application segment of Sinus Node Syndrome is intrinsically linked to the demand for bradycardia devices and is therefore a key driver of market growth. As the understanding and diagnosis of Sinus Node Syndrome improve, coupled with an aging population experiencing its manifestations, the need for pacemakers to regulate heart rhythm intensifies. The market is also witnessing a steady rise in the application of these devices for Sinus Atrial Block and other less common forms of bradycardia, contributing to the overall expansion of the application landscape. The Others application category, encompassing various other bradycardic conditions and prophylactic uses, is also expected to grow as medical professionals identify new therapeutic avenues for these devices.

In terms of segment dominance, the Pacemaker segment, particularly for the Sinus Node Syndrome application, is expected to be the primary growth engine. The continuous evolution of pacemaker technology, focusing on miniaturization, longevity, and improved patient-specific programming, ensures its sustained demand. The development of sophisticated algorithms that can differentiate between physiological and pathological bradycardia allows for more targeted and effective therapy. Remote monitoring capabilities are also becoming increasingly integrated into pacemakers, enabling proactive management of patients and reducing the burden on healthcare systems. This trend is particularly strong in developed markets like the United States and Western Europe, where reimbursement structures and patient access to advanced technology are favorable. However, the Asia Pacific region, with its vast population and increasing focus on cardiovascular health, represents a significant future growth frontier for both pacemakers and ICDs. The rising disposable incomes and the establishment of advanced cardiac care facilities in countries like China and India are expected to drive market penetration. While ICDs represent a smaller share of the market volume, their high value and critical role in preventing sudden cardiac death make them a crucial segment, especially in regions with high cardiovascular mortality rates. The increasing prevalence of conditions like ventricular tachycardia and fibrillation, which necessitate ICD implantation, will continue to fuel growth in this segment. The synergy between technological advancements and the growing understanding of cardiac electrophysiology will ensure that both pacemakers and ICDs continue to evolve and meet the diverse needs of patients worldwide.

The Sinus Bradycardia Devices industry is experiencing a surge in growth catalysts. Key among these is the increasing global prevalence of age-related cardiac arrhythmias and cardiovascular diseases, directly correlating with the growing elderly population. Technological advancements, particularly the development of smaller, more sophisticated, and minimally invasive devices such as leadless pacemakers, are significantly expanding the patient pool and improving treatment efficacy. Furthermore, growing awareness among healthcare providers and patients regarding the benefits of early diagnosis and intervention for bradycardic conditions is driving adoption rates. Favorable reimbursement policies in key markets and increasing healthcare expenditure also play a crucial role in making these life-saving devices more accessible.

This comprehensive report on Sinus Bradycardia Devices offers an unparalleled look into the market's trajectory from 2019 to 2033. It meticulously dissects the market by device type, including Pacemakers and Implantable Cardioverter Defibrillators, and by application, such as Sinus Cardiac Arrest, Sinus Atrial Block, and Sinus Node Syndrome. The analysis delves into the industry's current state and future potential, providing critical insights into market trends, driving forces, and prevailing challenges. With a detailed examination of key regions and dominant segments, the report equips stakeholders with the knowledge to navigate this complex market. Furthermore, it highlights significant industry developments and identifies the leading players, offering a holistic understanding of the competitive landscape and future growth catalysts.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.85% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.85%.

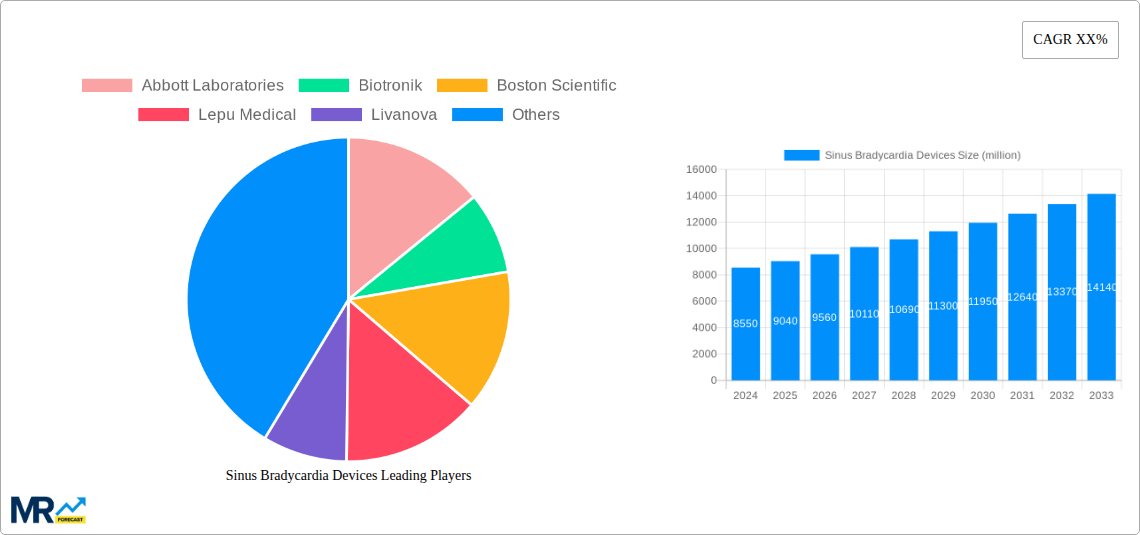

Key companies in the market include Abbott Laboratories, Biotronik, Boston Scientific, Lepu Medical, Livanova, Medico, Medtronic, Oscor, Osypka Medical, Shree Pacetronix, Cook Medical, Spectranetics, Abbott, Nihon Kohden, PHILIPS HEALTHCARE, Sorin Group, ZOLL Medical Corporation, Galix Biomedical Instrumentation, Integer Holdings Corporation, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Sinus Bradycardia Devices," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Sinus Bradycardia Devices, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.