1. What is the projected Compound Annual Growth Rate (CAGR) of the Ship Repairing and Conversion?

The projected CAGR is approximately 4.7%.

Ship Repairing and Conversion

Ship Repairing and ConversionShip Repairing and Conversion by Type (Ship Repairing, Ship Conversion), by Application (Container Ships, Bulk Carriers, Tankers, Engineering Ships, Other Ships), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

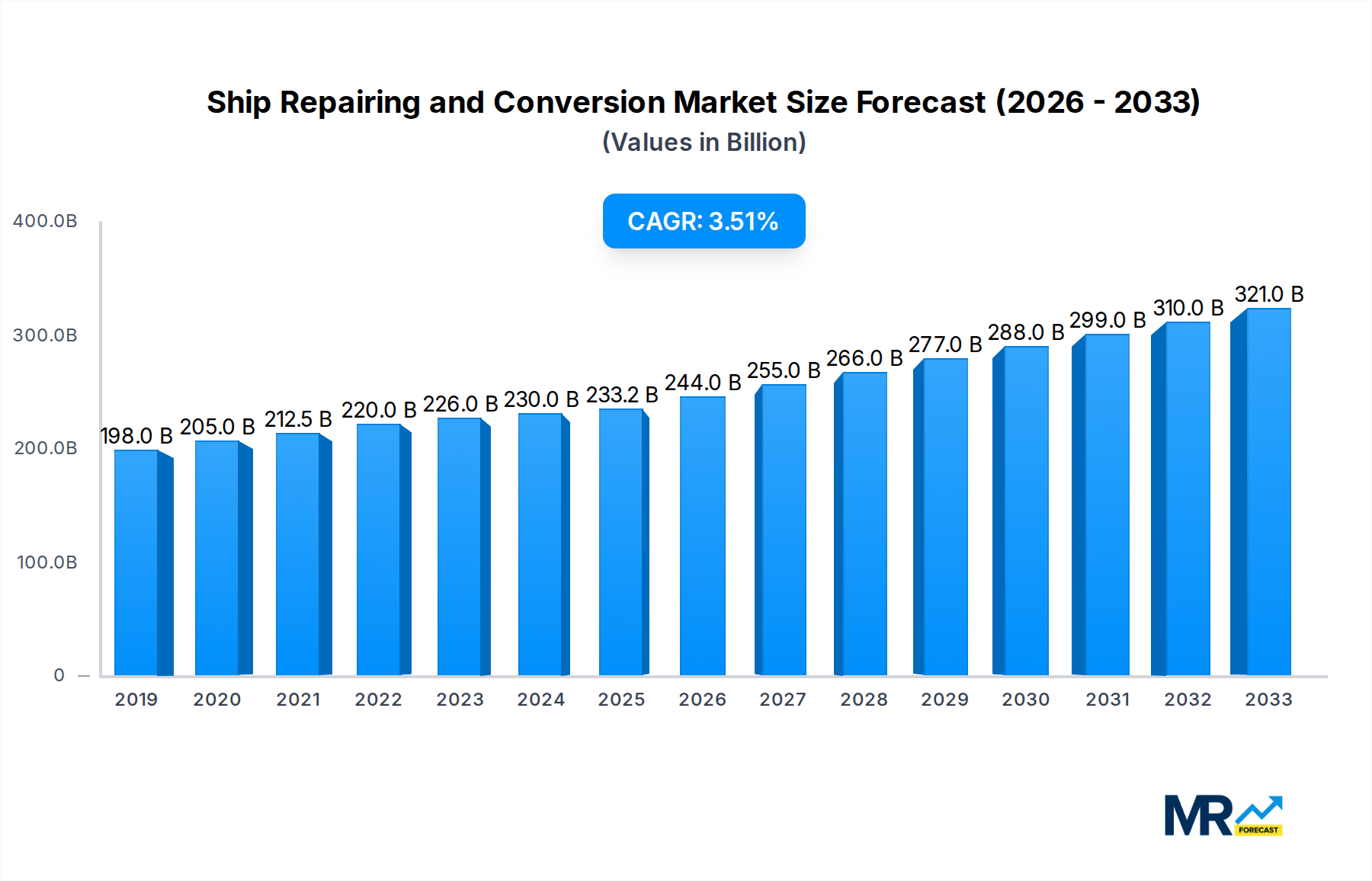

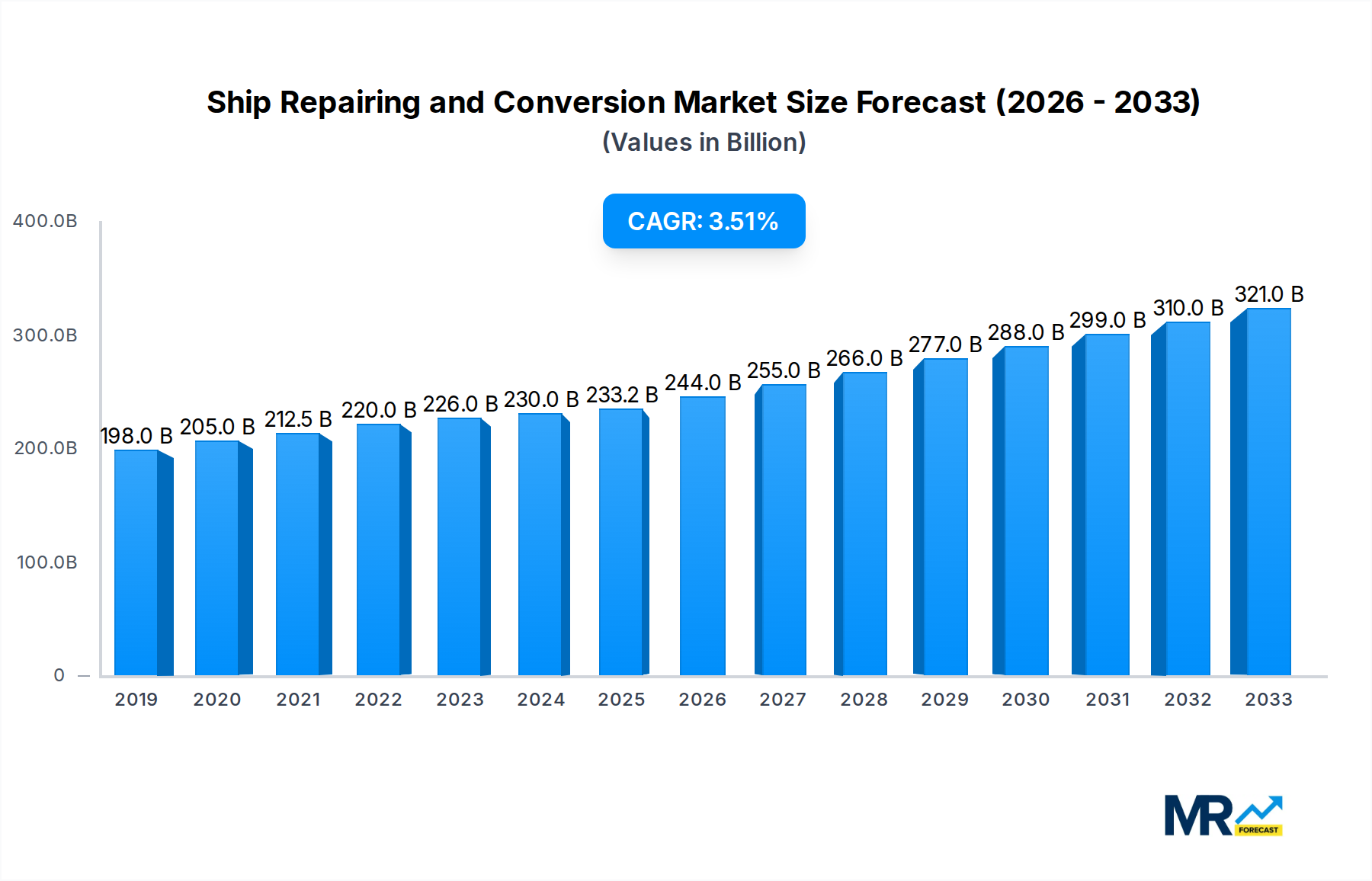

The global ship repairing and conversion market is projected for significant expansion, reaching an estimated $233.2 billion by 2025. This robust growth is driven by a compound annual growth rate (CAGR) of approximately 4.7% from 2025 to 2033. Key factors fueling this trajectory include evolving maritime regulations, particularly environmental and safety standards, necessitating upgrades and compliance. The aging global fleet requires continuous maintenance and repair for operational efficiency. The increasing demand for specialized vessels, such as offshore wind farm support and advanced logistics ships, also drives conversion projects. Sustained global trade volumes require a large merchant fleet, ensuring consistent demand for repair and maintenance services.

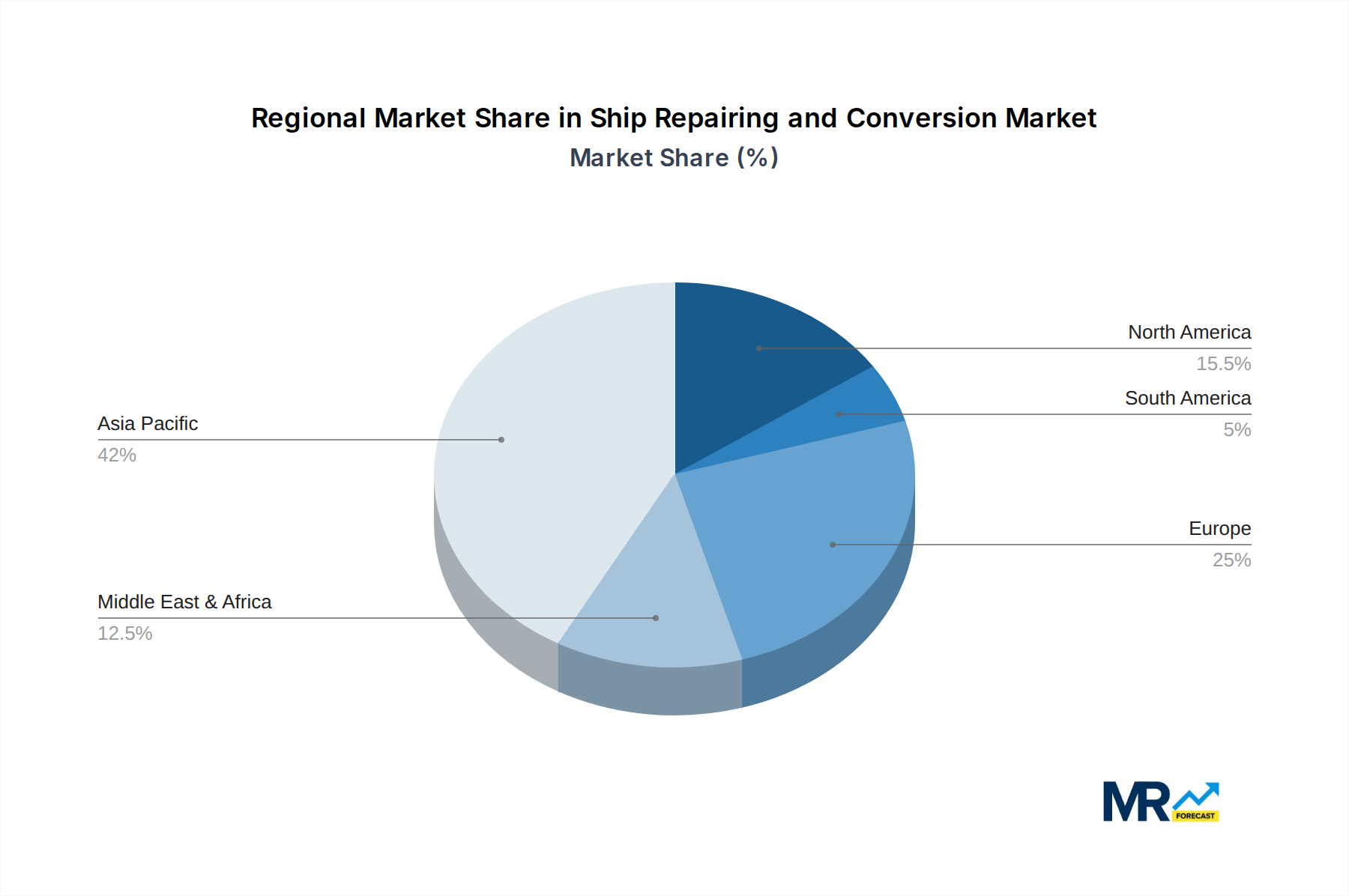

The market is segmented with ship repairing currently leading due to the ongoing need to maintain the vast existing fleet. However, ship conversion is a significant growth area, driven by the industry's adaptation to new technologies, alternative fuels (LNG, methanol), and specialized operational needs. Container ships and tankers represent the largest application segments, reflecting their importance in global trade. Asia Pacific, particularly China and South Korea, is expected to maintain its dominance as a shipbuilding and repair hub due to extensive manufacturing capabilities and cost efficiencies. Europe and the Middle East are vital markets, focusing on advanced repair technologies and specialized conversions. While fluctuating oil prices and high capital expenditure for shipyard infrastructure pose restraints, they are largely outweighed by the demand for fleet modernization and regulatory compliance.

This comprehensive report analyzes the dynamic global ship repairing and conversion market from 2019-2024, with projections extending to 2033. Based on the 2025 base year, the analysis provides critical insights into market trends, drivers, challenges, regional leadership, and growth catalysts. The estimated market valuation for 2025 is $233.2 billion.

The ship repairing and conversion market is experiencing a significant evolutionary phase, driven by a confluence of economic factors, technological advancements, and evolving regulatory landscapes. From 2019 to 2024, the sector demonstrated resilience and adaptability, navigating global supply chain disruptions and fluctuating maritime trade volumes. The estimated market size in 2025, pegged in the millions, underscores its substantial contribution to the global economy. A key trend observed is the increasing demand for advanced repair solutions, particularly for aging fleets requiring upgrades to meet stringent environmental regulations. This includes retrofitting vessels with ballast water treatment systems and scrubbers, a necessity driven by IMO 2020 and subsequent emission reduction targets.

The conversion segment is also witnessing robust growth, fueled by the need for fleet modernization and repurposing. For instance, the surge in demand for liquefied natural gas (LNG) carriers has spurred a rise in LNG conversion projects for existing vessels, offering a more sustainable and economically viable alternative to building new ones. Similarly, the growing offshore renewable energy sector is creating new avenues for conversion projects, with aging offshore support vessels being repurposed for wind farm installation and maintenance. The report anticipates that by 2033, the market will be further shaped by the adoption of digitalization and automation in repair processes, leading to enhanced efficiency and reduced turnaround times. The increasing complexity of modern vessels, with their intricate electronic systems and advanced propulsion technologies, necessitates specialized repair capabilities, a trend that will continue to define the market. Furthermore, the geographic distribution of repair activities is shifting, with emerging economies in Asia and the Middle East gaining prominence due to cost competitiveness and growing infrastructure. The proactive approach of major shipyards in investing in new technologies and expanding their service offerings will be critical in capturing market share during the forecast period. The report meticulously analyzes these trends, offering actionable insights for stakeholders across the maritime value chain, from ship owners and operators to shipyards and equipment manufacturers. The estimated market valuation in 2025, presented in millions, serves as a critical benchmark for assessing future growth trajectories and investment opportunities within this vital industry.

Several potent forces are actively propelling the ship repairing and conversion market forward. Foremost among these is the increasing global maritime trade volume, which necessitates a larger and more efficient operational fleet. As more vessels traverse the world's oceans, wear and tear become inevitable, leading to a consistent demand for maintenance and repair services. This continuous operational tempo creates a perpetual need for scheduled dry-dockings and unscheduled repairs to ensure fleet availability and safety.

Furthermore, the stringent and ever-evolving environmental regulations imposed by international bodies like the International Maritime Organization (IMO) are a significant catalyst. Regulations such as IMO 2020, which mandated a reduction in sulfur content in marine fuels, and upcoming emissions targets are forcing ship owners to invest in retrofitting their vessels with cleaner technologies. This includes the installation of ballast water treatment systems, exhaust gas cleaning systems (scrubbers), and modifications to propulsion systems to reduce their carbon footprint. The conversion of existing vessels, rather than building new ones, is often a more cost-effective and time-efficient solution to comply with these regulations, thereby boosting the conversion segment. Technological advancements in shipbuilding and repair technologies also play a crucial role. The adoption of digital tools, advanced welding techniques, and robotic systems is improving the efficiency, precision, and safety of repair operations, making them more attractive to ship owners. The growing offshore energy sector, particularly in renewables like wind energy, is creating new demand for specialized engineering vessels, often requiring significant conversions from existing platforms. This diversification of demand across various vessel types and applications is a key driver of market growth.

Despite the robust growth drivers, the ship repairing and conversion market faces several significant challenges and restraints that could temper its expansion. One of the most pervasive issues is the intense price competition among shipyards globally. With numerous players vying for contracts, particularly in the Asian region, yards often find themselves under pressure to offer highly competitive pricing, which can impact profit margins and hinder investment in advanced technologies and infrastructure.

The cyclical nature of the shipping industry itself presents another major restraint. Fluctuations in freight rates and global economic conditions directly influence the profitability of shipping companies, which in turn affects their spending on repairs and conversions. During economic downturns or periods of oversupply in the shipping market, owners may postpone or cancel non-essential repair and conversion projects to cut costs, leading to reduced demand for services. Furthermore, the availability of skilled labor is a persistent concern. The complex nature of modern ship repair and conversion projects requires a highly trained and experienced workforce. A shortage of qualified engineers, welders, and technicians can lead to project delays, increased labor costs, and a potential decline in the quality of work. The global supply chain disruptions, exacerbated by geopolitical events and the COVID-19 pandemic, have also impacted the availability and cost of critical spare parts and materials, leading to extended repair times and increased project expenses. Regulatory complexity and the constant need to adapt to new environmental standards can also be a challenge, requiring significant upfront investment in new technologies and expertise. Finally, geopolitical instability and trade disputes can disrupt shipping routes and impact investment decisions, indirectly affecting the ship repair and conversion market.

In the global ship repairing and conversion market, Asia-Pacific is poised to continue its dominance, with China and Singapore emerging as pivotal hubs. This supremacy is underpinned by a potent combination of extensive shipyard capacity, cost-effectiveness, and a strategic location within major shipping lanes.

Asia-Pacific Dominance:

Dominant Segments:

The concentration of shipyards in the Asia-Pacific region, coupled with the high operational tempo and regulatory demands on container ships and tankers, firmly establishes these as the leading contributors to the ship repairing and conversion market's overall growth and revenue. The synergy between the repair and conversion of these specific vessel types and the manufacturing prowess of Asian shipbuilders creates a powerful market ecosystem.

The ship repairing and conversion industry is propelled by several key growth catalysts. The relentless pursuit of environmental compliance by global shipping fleets is a primary driver, pushing for retrofits of ballast water treatment systems and scrubbers. The ongoing modernization of aging vessels and the need to adapt them for new operational requirements or evolving trade demands, such as the conversion of conventional vessels into LNG carriers, are significant growth factors. Furthermore, the expanding offshore renewable energy sector is creating a demand for specialized offshore vessels, often requiring conversions from existing platforms, thereby opening new revenue streams. Technological advancements, including digitalization and automation in repair processes, enhance efficiency and attract more business.

This report provides an exhaustive analysis of the global ship repairing and conversion market, offering a detailed outlook from the historical period of 2019-2024 through to a projected forecast up to 2033. It meticulously examines market trends, identifies the key driving forces and challenges, and pinpoints the dominant regions and segments expected to lead the market. The report also highlights crucial growth catalysts and presents a comprehensive list of leading industry players. With an estimated market valuation for 2025 presented in millions, this report is an indispensable resource for stakeholders seeking to understand the current landscape, anticipate future developments, and make informed strategic decisions within this vital sector of the maritime industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.7% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.7%.

Key companies in the market include CSIC, Hyundai Mipo Dockyard, Yiu Lian Dockyards, Longshan Shipyard, Damen Shipyards Group, COSCO SHIPPING Heavy Industry, Zhoushan Xinya Shipyard, Huadong shipyard, Huarun Dadong Dockyard, Sembcorp Marine, Drydocks World Dubai, PaxOcean Engineering Zhoushan, Oman Drydock Company, Cochin Shipyard Ltd (CSL), United Shipbuilding Corporation, Arab Shipbuilding and Repair Yard, Fincantieri, Keppel Shipyard, Swissco Holdings, Egyptian Ship Repair & Building Company, .

The market segments include Type, Application.

The market size is estimated to be USD 233.2 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Ship Repairing and Conversion," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Ship Repairing and Conversion, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.