1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Automatic Wafer Placement Equipment?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Semiconductor Automatic Wafer Placement Equipment

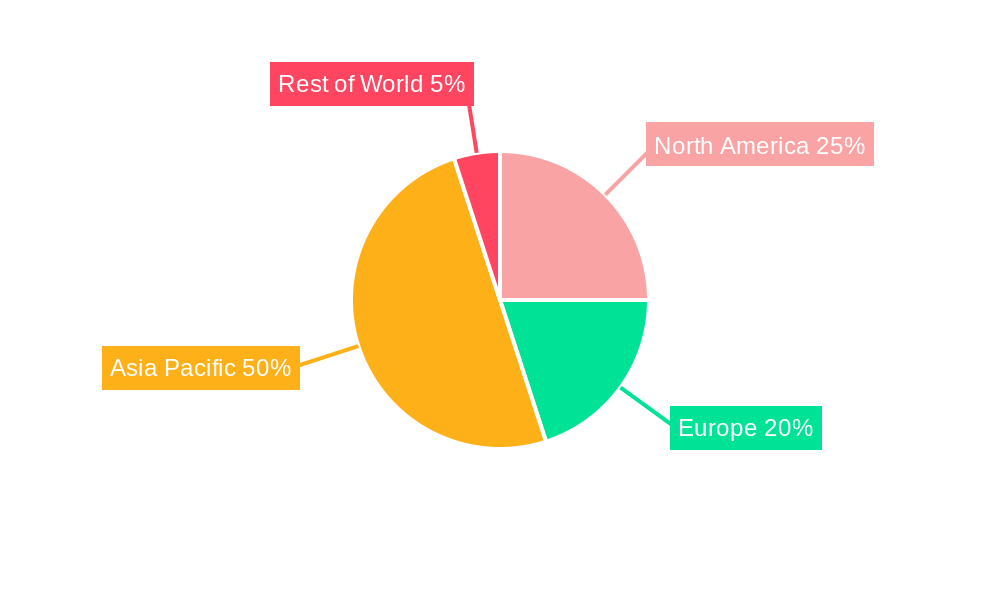

Semiconductor Automatic Wafer Placement EquipmentSemiconductor Automatic Wafer Placement Equipment by Type (Fully Automatic, Semi Automatic), by Application (Chip Manufacturing, Surface Treatment, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

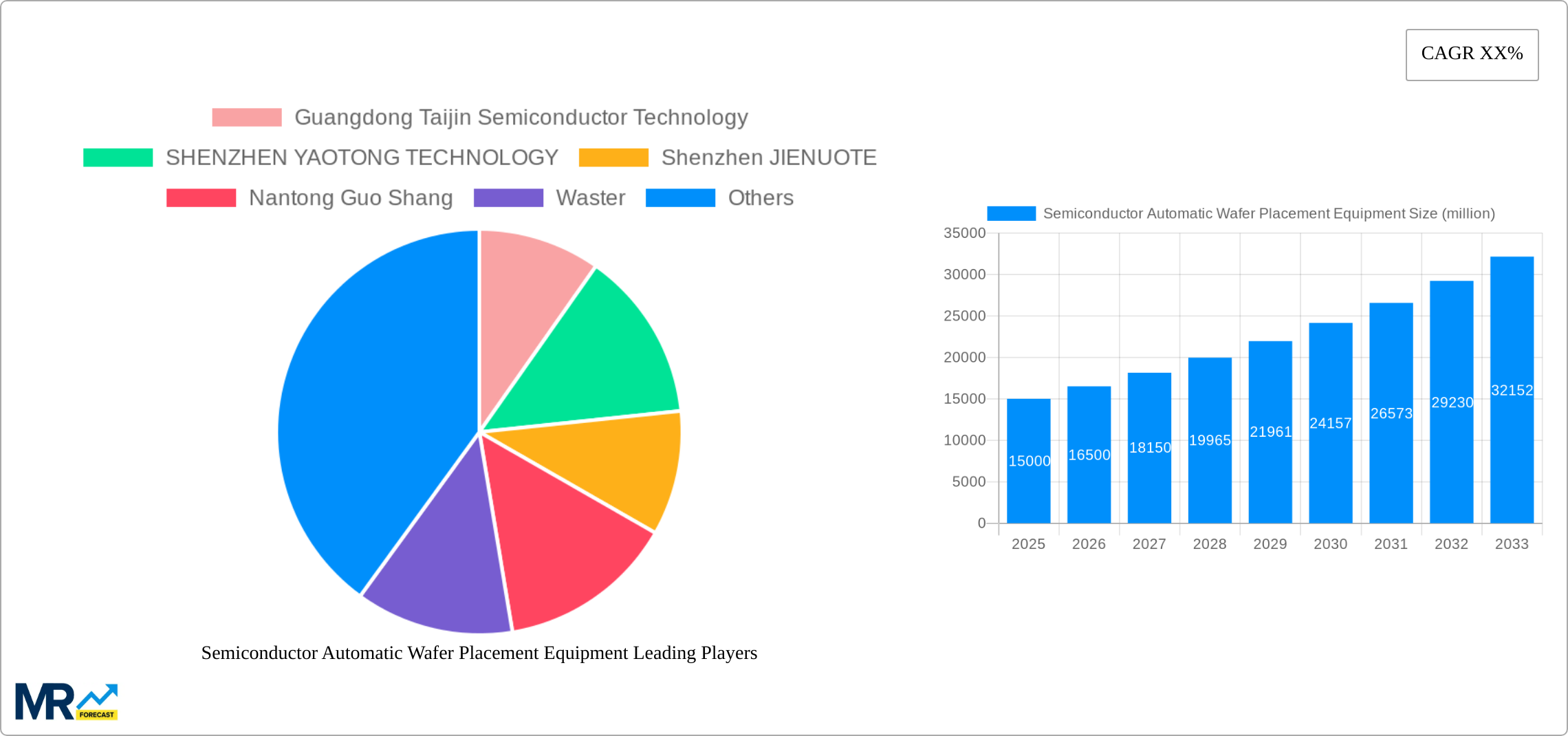

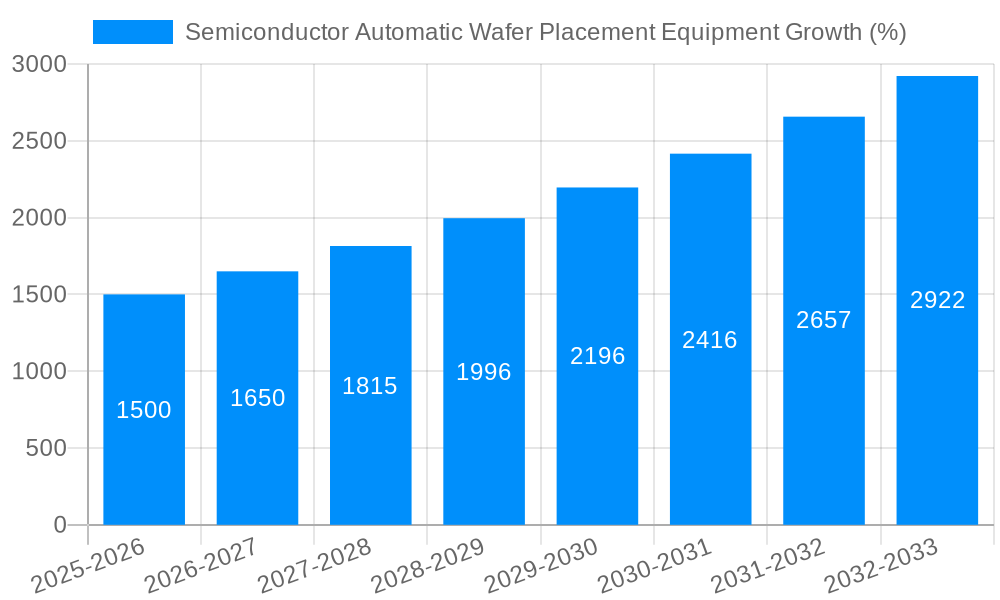

The Semiconductor Automatic Wafer Placement Equipment market is poised for substantial growth, estimated to reach approximately $1.5 billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of around 12% through 2033. This upward trajectory is primarily fueled by the escalating demand for advanced semiconductor devices across a myriad of applications, including artificial intelligence, 5G technology, autonomous vehicles, and the Internet of Things (IoT). The increasing complexity of integrated circuits and the relentless pursuit of miniaturization and higher performance necessitate highly precise and automated wafer handling solutions, making these equipment indispensable for modern chip manufacturing. Furthermore, the ongoing global investment in semiconductor fabrication facilities, driven by efforts to secure supply chains and meet burgeoning consumer and industrial electronics demand, directly translates into increased procurement of automatic wafer placement systems.

The market is witnessing a significant shift towards Fully Automatic systems, which offer superior throughput, reduced human error, and enhanced process control crucial for high-volume production. This segment is expected to dominate the market share, propelled by technological advancements in robotics, vision systems, and artificial intelligence integrated into these machines. Surface treatment applications also present a growing niche, as precise wafer handling is critical for advanced packaging and specialized coating processes. While the overall market is robust, certain restraints exist, including the high initial capital investment required for sophisticated equipment and the specialized skillset needed for operation and maintenance. However, the long-term benefits of increased yield, improved quality, and operational efficiency are compelling enough to overcome these challenges, driving widespread adoption across leading semiconductor manufacturing hubs.

The global Semiconductor Automatic Wafer Placement Equipment market is poised for substantial expansion, driven by an insatiable demand for advanced electronics and the continuous evolution of semiconductor manufacturing processes. The Study Period of 2019-2033, with a Base Year of 2025, and an Estimated Year also of 2025, sets the stage for a detailed analysis that will pinpoint the significant shifts and opportunities within this dynamic sector. Over the Historical Period of 2019-2024, the market has witnessed consistent growth, laying the groundwork for even more aggressive acceleration in the Forecast Period of 2025-2033. Key market insights reveal a pronounced shift towards Fully Automatic systems, accounting for a dominant share and projected to capture over 90 million units by 2033. This trend is directly linked to the increasing complexity and precision required in modern chip manufacturing, where human intervention introduces unacceptable levels of error and inefficiency. The miniaturization of components and the demand for higher yields necessitate automated solutions capable of handling wafers with sub-micron accuracy. Furthermore, the expanding applications within Chip Manufacturing, which currently represents the largest segment with an estimated 75 million units in 2025, will continue to be the primary engine of growth. The integration of artificial intelligence and machine learning into these placement systems is another critical trend, enabling real-time defect detection, predictive maintenance, and optimized workflow management. This intelligent automation is not only improving throughput but also significantly reducing operational costs for semiconductor foundries. The market is also seeing a growing demand for specialized wafer placement equipment catering to emerging semiconductor technologies such as advanced packaging, power semiconductors, and microelectromechanical systems (MEMS). These niche applications, while currently smaller in volume, are expected to contribute significantly to market diversification and innovation in the coming years. The ongoing geopolitical shifts and the emphasis on supply chain resilience are also subtly influencing market dynamics, potentially leading to increased regional manufacturing and a corresponding demand for localized production of automated wafer placement solutions. Overall, the trajectory of the Semiconductor Automatic Wafer Placement Equipment market is overwhelmingly positive, characterized by technological advancements, increasing automation, and an expanding application landscape that promises sustained and robust growth.

The semiconductor industry's relentless pursuit of innovation and miniaturization is the primary engine propelling the Semiconductor Automatic Wafer Placement Equipment market forward. The increasing complexity of integrated circuits, with billions of transistors packed onto a single chip, demands an unprecedented level of precision and repeatability in every manufacturing step, with wafer placement being a critical juncture. Automated systems are indispensable for achieving these sub-micron tolerances, significantly reducing the risk of contamination and damage that could lead to costly yield losses. The exponential growth in demand for consumer electronics, automotive semiconductors, and advanced computing solutions further amplifies the need for higher production volumes and faster manufacturing cycles. As foundries strive to meet this demand, the efficiency gains offered by fully automatic wafer placement equipment become paramount. Beyond just speed, these advanced systems offer enhanced accuracy, consistency, and reduced operational costs through minimized human intervention. The integration of sophisticated vision systems, AI algorithms, and robotics allows for real-time error detection and correction, optimizing throughput and ensuring the highest quality output. Furthermore, the expanding applications of semiconductors into new frontiers such as 5G infrastructure, the Internet of Things (IoT), and artificial intelligence (AI) hardware are creating entirely new markets and driving the need for specialized wafer placement solutions capable of handling diverse wafer types and sizes. This continuous diversification of end-use applications provides a stable and growing demand base for automated wafer placement equipment manufacturers.

Despite the robust growth trajectory, the Semiconductor Automatic Wafer Placement Equipment market faces several significant challenges and restraints that could temper its expansion. The most prominent of these is the exceptionally high capital investment required for advanced, fully automatic wafer placement systems. These sophisticated machines represent a substantial financial outlay for semiconductor manufacturers, particularly for smaller or emerging players. The cost of research and development for cutting-edge technology, coupled with the intricate manufacturing processes involved in producing these high-precision instruments, contributes to their premium pricing. This financial barrier can limit adoption rates, especially in price-sensitive markets or during periods of economic uncertainty. Another critical challenge lies in the complex integration and operational expertise required to effectively implement and maintain these automated systems. Semiconductor manufacturing environments are highly specialized, and integrating new wafer placement equipment necessitates seamless compatibility with existing infrastructure, software, and process flows. This often requires skilled technicians and engineers for setup, calibration, and ongoing maintenance, leading to increased operational expenditure and a potential shortage of qualified personnel. Furthermore, the rapid pace of technological evolution within the semiconductor industry presents a double-edged sword. While it drives demand for advanced equipment, it also means that the lifespan of even the most cutting-edge systems can be relatively short. Manufacturers must constantly invest in upgrades and next-generation technologies to remain competitive, creating a continuous need for reinvestment and potentially leading to obsolescence concerns for older equipment. Finally, global supply chain disruptions and geopolitical factors, as witnessed in recent years, can impact the availability of critical components and raw materials, leading to production delays and increased costs for equipment manufacturers, ultimately affecting market availability and pricing.

The Fully Automatic segment is poised to dominate the Semiconductor Automatic Wafer Placement Equipment market, with its market share projected to reach an impressive 90 million units by 2033. This dominance stems from the inherent demands of modern semiconductor manufacturing.

The Chip Manufacturing application segment will continue to be the primary driver of market growth.

The Semiconductor Automatic Wafer Placement Equipment industry is propelled by several key growth catalysts. The exponential growth in demand for advanced electronics across various sectors, including consumer electronics, automotive, and telecommunications, fuels the need for increased semiconductor production. This directly translates to higher demand for the equipment that enables efficient wafer handling. Furthermore, the relentless push towards miniaturization and complexity in chip design necessitates highly precise and automated placement solutions to achieve desired yields. Emerging technologies like 5G, AI, and IoT also create new application areas, requiring specialized wafer placement capabilities and driving innovation.

This comprehensive report will delve into the intricate dynamics of the Semiconductor Automatic Wafer Placement Equipment market from 2019 to 2033. It will provide an in-depth analysis of market size, segmentation, and growth projections, with a particular focus on the dominance of the Fully Automatic segment and the Chip Manufacturing application. The report will meticulously examine the driving forces and challenges shaping the industry, offering critical insights into the factors propelling its expansion. Furthermore, it will highlight the key regions and countries poised for significant market share, alongside an exhaustive overview of leading players and their contributions. The report will also trace the evolution of the sector through significant historical and projected developments, offering a forward-looking perspective.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Guangdong Taijin Semiconductor Technology, SHENZHEN YAOTONG TECHNOLOGY, Shenzhen JIENUOTE, Nantong Guo Shang, Waster, DAHUA TECHNOLOGY, WUXI XIANG HUA TECHNOLOGY, Chengdu Zhongke Precision Mould, Shenzhen Shenghe Precision Mold.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Semiconductor Automatic Wafer Placement Equipment," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Automatic Wafer Placement Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.