1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Angle Valve?

The projected CAGR is approximately XX%.

Semiconductor Angle Valve

Semiconductor Angle ValveSemiconductor Angle Valve by Type (Heated Angle Valve, Non-Heated Angle Valve, World Semiconductor Angle Valve Production ), by Application (IDM, Foundry, Others, World Semiconductor Angle Valve Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

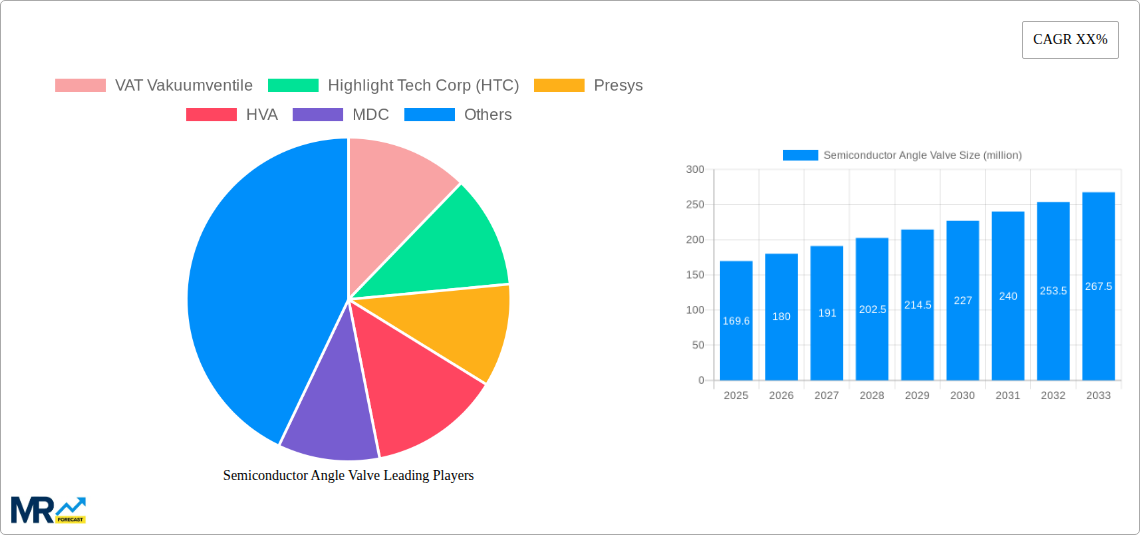

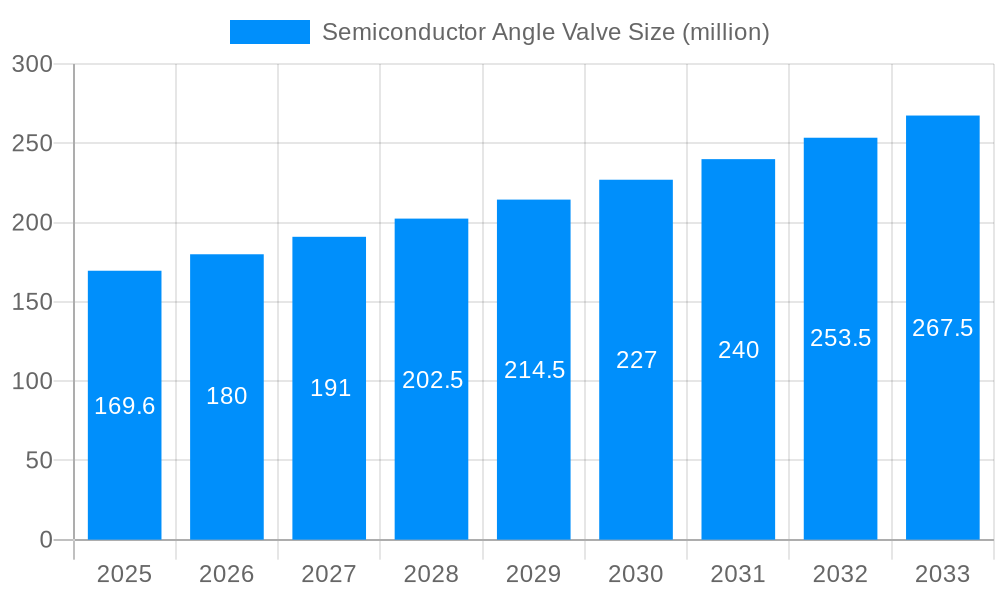

The global Semiconductor Angle Valve market is poised for substantial growth, projected to reach a valuation of $169.6 million. This expansion is fueled by the relentless demand for advanced semiconductor manufacturing processes, where precise fluid and gas control is paramount. Angle valves, with their inherent design advantages in directing flow and minimizing dead space, are indispensable components in applications ranging from wafer fabrication to sophisticated packaging. The market's trajectory is strongly influenced by the increasing complexity of semiconductor chips, necessitating higher purity environments and more intricate process control, thereby driving the adoption of specialized angle valves. Furthermore, the burgeoning demand for consumer electronics, the rapid advancement of Artificial Intelligence (AI) and machine learning, and the sustained growth in the automotive sector, all of which rely heavily on cutting-edge semiconductors, are acting as significant catalysts for market expansion.

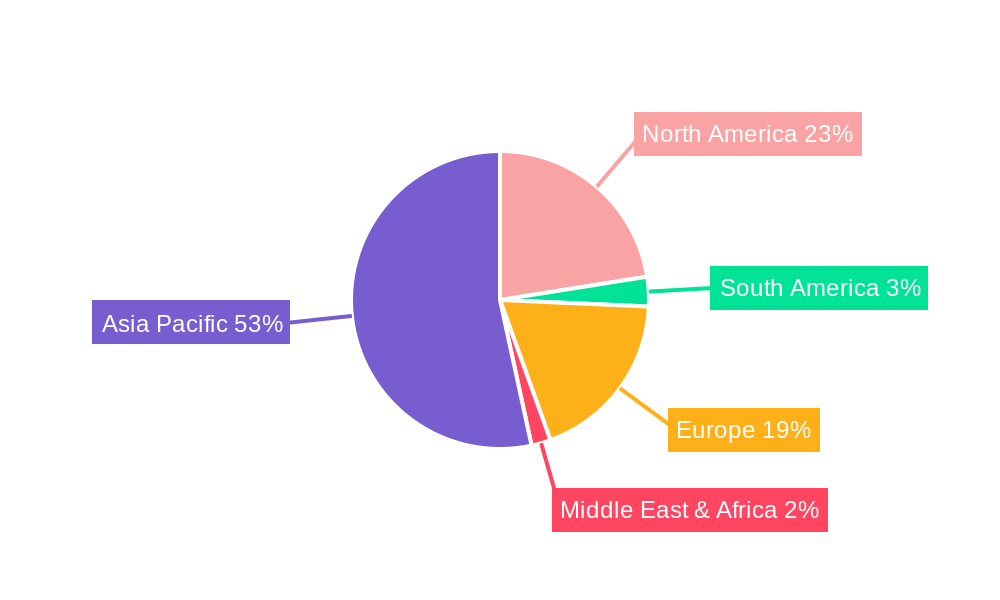

The market segmentation reveals a nuanced landscape. Within the "Type" category, the demand for Heated Angle Valves is expected to outpace Non-Heated variants, reflecting the growing need for precise temperature control in advanced etching, deposition, and cleaning processes to prevent condensation and ensure optimal performance. On the application front, both Integrated Device Manufacturers (IDMs) and Foundries represent key demand centers, with the former focusing on in-house production and the latter catering to a broad spectrum of semiconductor outsourcing. Geographically, Asia Pacific is anticipated to dominate the market, driven by its robust semiconductor manufacturing ecosystem, particularly in China, South Korea, and Taiwan. North America and Europe also present considerable opportunities, bolstered by government initiatives and investments in domestic semiconductor production capabilities. However, challenges such as stringent regulatory requirements for material purity and the high cost of specialized valve components may temper growth in certain segments.

This report provides a comprehensive analysis of the global Semiconductor Angle Valve market, encompassing a study period from 2019 to 2033. The base year for estimation is 2025, with a forecast period extending from 2025 to 2033, building upon historical data from 2019 to 2024. The market is projected to witness significant growth, with estimated production volumes reaching XXX million units by 2033.

The global semiconductor angle valve market is characterized by a dynamic interplay of technological advancements, evolving manufacturing processes, and increasing demand from various end-user segments. The historical period of 2019-2024 has seen a steady ascent in the adoption of sophisticated semiconductor manufacturing techniques, leading to a parallel rise in the demand for high-precision and reliable fluid control components such as angle valves. The base year of 2025 marks a pivotal point, with the market poised for accelerated expansion driven by the burgeoning semiconductor industry, particularly in advanced node manufacturing. The forecast period of 2025-2033 anticipates a compound annual growth rate (CAGR) that will significantly contribute to the XXX million units production milestone. Key trends include the increasing preference for heated angle valves in critical process steps requiring precise temperature control, especially in deposition and etching applications. These valves are essential for maintaining process stability and wafer yield, directly impacting the quality and performance of the final semiconductor devices. Furthermore, the ongoing miniaturization of semiconductor components and the drive towards higher wafer densities necessitate smaller, more efficient, and cleaner angle valves with reduced internal volumes and improved sealing capabilities. The integration of smart features, such as real-time monitoring and diagnostics, is also gaining traction, allowing for predictive maintenance and minimized downtime. The report will delve into the nuanced shifts within the non-heated angle valve segment as well, which continues to hold significant market share due to its applicability in less temperature-sensitive processes and its cost-effectiveness. The overarching trend is towards enhanced material purity, superior sealing technology, and advanced actuation mechanisms to meet the stringent requirements of next-generation semiconductor fabrication. The market is also observing a growing emphasis on sustainable manufacturing practices, which influences the design and material selection of angle valves to minimize environmental impact and ensure compliance with evolving regulations. The increasing complexity of semiconductor chips and the demand for higher performance characteristics from electronic devices are directly translating into a more sophisticated demand for angle valves that can precisely manage the flow of various process gases and liquids with utmost accuracy and reliability. The market's trajectory is undeniably linked to the overall health and growth of the global semiconductor industry, which is itself experiencing unprecedented innovation and investment. The continuous pursuit of Moore's Law and the development of new semiconductor materials and architectures are creating new opportunities and challenges for angle valve manufacturers. The report will provide granular insights into these evolving trends, enabling stakeholders to strategize effectively for future market engagement. The demand for specialized angle valves designed for specific etch chemistries, deposition processes, and cleaning cycles is also on the rise, further segmenting the market and driving innovation in product development.

The relentless pursuit of technological advancement in the semiconductor industry serves as the primary engine driving the growth of the Semiconductor Angle Valve market. The ever-increasing demand for more powerful, smaller, and energy-efficient electronic devices fuels the need for sophisticated semiconductor fabrication processes. This, in turn, directly translates to a higher requirement for precise and reliable fluid control solutions, with angle valves playing a critical role. The ongoing expansion of wafer fabrication facilities globally, especially in response to the burgeoning demand for AI chips, 5G infrastructure, and advanced computing, is a significant catalyst. Investments in new fabs and upgrades to existing ones necessitate substantial procurement of essential components like angle valves. Furthermore, the transition towards advanced semiconductor nodes, such as those below 10nm, introduces more complex manufacturing steps that demand exceptionally high purity, precision, and control over process gases and chemicals. Heated angle valves, in particular, are becoming indispensable for maintaining stable process temperatures in critical applications like Chemical Vapor Deposition (CVD) and Atomic Layer Deposition (ALD), directly impacting wafer yield and device performance. The increasing complexity of chip architectures and the need to manage a wider array of specialized process chemicals also contribute to the demand for highly engineered and application-specific angle valves. The growing trend of outsourcing semiconductor manufacturing to foundries, coupled with the integrated device manufacturers' (IDMs) continued investment in in-house capabilities, creates a dual demand stream for these essential components. The continuous innovation in materials science for semiconductors, leading to the development of new alloys and compounds, also necessitates the development of angle valves capable of handling these novel chemistries without contamination or degradation.

Despite the robust growth trajectory, the Semiconductor Angle Valve market is not without its challenges and restraints. One of the most significant hurdles is the extremely stringent purity requirements of the semiconductor manufacturing environment. Any particulate contamination or outgassing from valve components can lead to wafer defects, resulting in substantial financial losses. This necessitates the use of advanced, high-purity materials and meticulous manufacturing processes, which in turn increases production costs. The long qualification cycles for new semiconductor components are another considerable challenge. Before an angle valve can be integrated into a production line, it must undergo rigorous testing and validation by semiconductor manufacturers, a process that can take several months to a couple of years, thereby delaying market entry for new products. The volatility in semiconductor capital expenditure (CapEx), influenced by global economic conditions and geopolitical factors, can also lead to fluctuations in demand. A downturn in the broader semiconductor industry can directly impact the order volumes for angle valves. Furthermore, the increasing complexity of semiconductor processes requires angle valves to be increasingly sophisticated, often with integrated sensors and advanced control mechanisms. This elevates the research and development (R&D) costs for manufacturers and requires a highly skilled workforce. Supply chain disruptions, as witnessed in recent years, can also impact the availability of critical raw materials and components needed for angle valve production, leading to production delays and increased lead times. The fierce competition among established players and emerging manufacturers also puts pressure on pricing and profit margins, requiring companies to continuously innovate and optimize their cost structures. The need for specialized training for maintenance personnel to handle advanced valve technologies can also be a barrier for end-users, indirectly impacting adoption rates. Moreover, environmental regulations regarding the handling and disposal of certain process chemicals used in semiconductor fabrication can necessitate the development of specialized, often more expensive, valve solutions, adding another layer of complexity and cost.

The Semiconductor Angle Valve market is poised for significant growth driven by key regions and segments that are at the forefront of semiconductor manufacturing innovation.

Dominant Segments:

Dominant Regions:

Several key factors are acting as potent growth catalysts for the Semiconductor Angle Valve industry. The relentless demand for advanced semiconductor devices, driven by AI, 5G, IoT, and high-performance computing, necessitates continuous investment in new wafer fabrication facilities and upgrades to existing ones. This expansion directly fuels the demand for angle valves. Furthermore, the global push towards greater semiconductor self-sufficiency is leading to significant government initiatives and private sector investments in building domestic manufacturing capabilities, particularly in emerging semiconductor hubs. The increasing complexity of semiconductor manufacturing processes, especially at advanced nodes, requires higher precision and reliability in fluid control, driving the adoption of more sophisticated and often heated angle valves.

This comprehensive report delves into the intricacies of the Semiconductor Angle Valve market, providing an in-depth analysis of its current landscape and future trajectory. It meticulously examines market trends, identifying key drivers and challenges that shape the industry's evolution. The report offers detailed insights into the dominant market segments, such as Heated and Non-Heated Angle Valves, and analyzes their specific growth prospects. Furthermore, it highlights the critical role of end-user applications, including IDM, Foundry, and Others, in driving demand. A significant portion of the report is dedicated to regional market analysis, identifying the key regions and countries that are poised to lead the market's expansion, with a particular focus on the dominant Asia Pacific region. The report also meticulously tracks significant developments and innovations within the sector, providing stakeholders with crucial information for strategic decision-making. This comprehensive coverage ensures that industry participants gain a holistic understanding of the market dynamics, enabling them to navigate the complexities and capitalize on future opportunities. The report aims to equip stakeholders with the necessary intelligence to understand the estimated XXX million units production volume by 2033 and formulate effective strategies for growth.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include VAT Vakuumventile, Highlight Tech Corp (HTC), Presys, HVA, MDC, .

The market segments include Type, Application.

The market size is estimated to be USD 169.6 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Semiconductor Angle Valve," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Angle Valve, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.