1. What is the projected Compound Annual Growth Rate (CAGR) of the Semi-Autonomous Vehicles?

The projected CAGR is approximately 18.8%.

Semi-Autonomous Vehicles

Semi-Autonomous VehiclesSemi-Autonomous Vehicles by Type (Level 2 Autonomous Vehicles, Level 3 Autonomous Vehicles, World Semi-Autonomous Vehicles Production ), by Application (Passenger Vehicles, Commercial Vehicles, World Semi-Autonomous Vehicles Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global semi-autonomous vehicle market is projected for significant expansion, estimated to reach USD 58.17 billion by 2024, with a compound annual growth rate (CAGR) of 18.8%. This growth is fueled by increasing consumer demand for enhanced safety, improved driving comfort, and greater fuel efficiency. Continuous technological advancements in advanced driver-assistance systems (ADAS), sensor fusion, and artificial intelligence are expanding the capabilities of semi-autonomous vehicles, making them more attractive to a wider consumer base. Supportive government initiatives promoting smart cities and autonomous driving infrastructure are also fostering market development. The integration of advanced navigation, adaptive cruise control, lane-keeping assist, and automated parking functionalities is becoming a standard feature, driving market adoption.

The market is segmented by automation level, with Level 2 systems currently leading due to features like adaptive cruise control and lane centering. However, Level 3 automation, enabling conditional automation and driver handover, is expected to experience substantial growth. Passenger vehicles constitute the largest application segment, driven by consumer preference for superior driving experiences. Commercial vehicles, including trucks and delivery vans, are also emerging as key growth areas, promising enhanced logistics efficiency and reduced operational costs. Leading manufacturers such as Tesla, General Motors, Daimler, BMW, Audi, Volvo, and Ford are making significant R&D investments to secure a strong market position. Geographically, the Asia Pacific region, particularly China and Japan, is anticipated to be a major growth driver, followed by North America and Europe, all actively developing and adopting semi-autonomous technologies.

This report provides an in-depth analysis of the global semi-autonomous vehicle market, covering historical trends and future projections. The analysis spans the period from 2019 to 2033, with a base year of 2024. It meticulously examines market dynamics during the historical period (2019-2024) and forecasts its trajectory through the forecast period (2025-2033). The report details global semi-autonomous vehicle production, highlighting contributions from key manufacturers including Tesla, General Motors, Daimler, BMW, Audi, Volvo, and Ford. Market segmentation includes Level 2 and Level 3 autonomous vehicles, and applications such as passenger and commercial vehicles. Key industry developments and growth drivers are thoroughly investigated to offer actionable insights into this rapidly evolving sector.

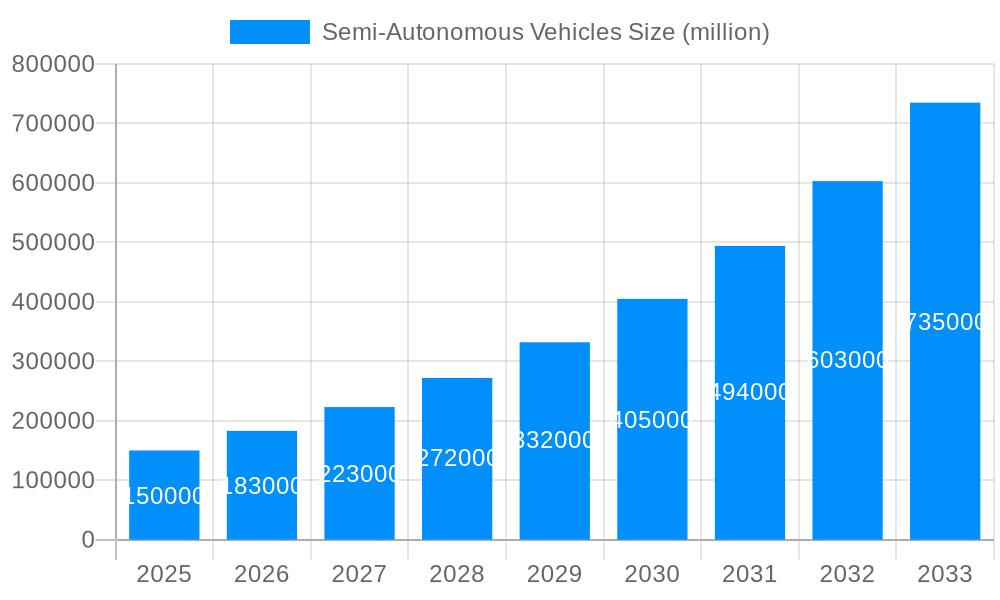

XXX The global semi-autonomous vehicle market is experiencing a seismic shift, driven by rapid technological advancements and a growing consumer appetite for enhanced driving experiences and safety features. During the Historical Period (2019-2024), the market witnessed substantial growth, primarily fueled by the widespread adoption of Level 2 Autonomous Vehicles. These systems, which offer features like adaptive cruise control and lane keeping assist, have become increasingly sophisticated and accessible, integrating seamlessly into a vast number of Passenger Vehicles. The Estimated Year of 2025 is poised to mark a significant milestone, with projections indicating a substantial increase in the World Semi-Autonomous Vehicles Production. This surge is not merely about incremental improvements but represents a foundational step towards a more automated future. The market is characterized by a fierce competitive landscape, where established automotive giants and agile tech innovators are vying for dominance. Investments in research and development have intensified, focusing on refining sensor technology, artificial intelligence algorithms, and robust cybersecurity measures. The increasing regulatory clarity and the development of standardized testing protocols are also playing a crucial role in fostering market confidence and accelerating the deployment of these advanced driver-assistance systems. Furthermore, the integration of connectivity features, such as over-the-air updates and real-time data sharing, is enhancing the functionality and intelligence of semi-autonomous vehicles, promising a more connected and intuitive driving ecosystem. As we move into the Forecast Period (2025-2033), the transition from Level 2 to Level 3 Autonomous Vehicles is expected to gain momentum. This progression, while presenting its own set of challenges, signifies a leap forward in vehicle autonomy, where the vehicle can manage most driving tasks under specific conditions, allowing drivers to disengage temporarily. This shift will undoubtedly reshape the automotive industry, influencing vehicle design, manufacturing processes, and consumer expectations. The increasing emphasis on sustainability and electrification is also intertwined with the advancement of semi-autonomous technologies, as optimized driving patterns can lead to improved energy efficiency and reduced emissions. The evolution of infrastructure, including smart roads and Vehicle-to-Everything (V2X) communication, will also be a critical enabler for the broader adoption of semi-autonomous capabilities. The sheer volume of World Semi-Autonomous Vehicles Production projected in the coming years underscores the transformative potential of this technology across diverse automotive segments and geographies.

The relentless march of semi-autonomous vehicles is propelled by a confluence of potent driving forces, each contributing to its burgeoning market presence. Foremost among these is the unwavering commitment to enhancing vehicle safety. The integration of advanced driver-assistance systems (ADAS) aims to significantly reduce the incidence of road accidents by mitigating human error, a leading cause of collisions. Features such as automatic emergency braking, lane departure warning, and blind-spot monitoring are becoming standard, demonstrating a clear industry-wide prioritization of occupant and pedestrian protection. This safety imperative is further amplified by evolving consumer expectations, as drivers increasingly seek the convenience and comfort offered by semi-autonomous features. The desire for a less fatiguing driving experience, particularly during long commutes or in congested urban environments, is a significant catalyst. Moreover, the relentless pace of technological innovation, particularly in areas like artificial intelligence, sensor fusion, and high-definition mapping, is continuously expanding the capabilities and reliability of semi-autonomous systems, making them more appealing and functional. Government initiatives and evolving regulatory frameworks, aimed at promoting the adoption of safer and more efficient transportation solutions, also play a crucial role. These often include incentives for research and development, as well as the gradual establishment of legal guidelines for autonomous driving. The burgeoning electric vehicle (EV) market also acts as a synergistic force, with many EV manufacturers integrating advanced autonomous features as a key differentiator and a pathway to future mobility solutions.

Despite the significant advancements and driving forces, the widespread adoption of semi-autonomous vehicles is not without its hurdles. A paramount challenge lies in the technological complexity and the associated cost of development and implementation. While Level 2 Autonomous Vehicles are becoming more mainstream, the progression to Level 3 Autonomous Vehicles and beyond necessitates highly sophisticated sensor arrays, powerful processing units, and robust AI algorithms, which remain expensive to produce and integrate, impacting vehicle affordability. Public perception and trust also represent a significant restraint. Consumer apprehension regarding the reliability and safety of autonomous systems, particularly in unpredictable real-world scenarios, needs to be addressed through extensive education and demonstrably safe performance. Regulatory frameworks, while evolving, are still catching up with the rapid pace of technological development, leading to a fragmented and sometimes unclear legal landscape regarding liability in the event of an accident. Cybersecurity threats pose a substantial risk; any compromise of a vehicle's autonomous system could have catastrophic consequences, necessitating stringent and continuous security measures. Furthermore, the ethical considerations surrounding decision-making in unavoidable accident scenarios remain a complex societal debate that needs to be resolved. The availability and standardization of necessary infrastructure, such as reliable GPS signals and potentially vehicle-to-infrastructure (V2I) communication, are also crucial for optimal performance and safety, and their widespread deployment is still a work in progress.

The global semi-autonomous vehicle market's dominance is poised to be shaped by a combination of influential regions and the strategic prioritization of specific segments.

North America (United States and Canada): This region is a powerhouse for the adoption of semi-autonomous vehicles, particularly in the Passenger Vehicles segment. Driven by a high disposable income, a strong technological adoption rate, and a considerable focus on safety innovations by manufacturers like General Motors and Ford, North America is expected to lead in the deployment of both Level 2 Autonomous Vehicles and, increasingly, Level 3 Autonomous Vehicles. The substantial market size for new and used vehicles, coupled with early regulatory support and the presence of major automotive R&D centers, positions North America for sustained growth throughout the Forecast Period (2025-2033). The demand for advanced driver-assistance systems (ADAS) is fueled by a desire for enhanced comfort and safety during long commutes and the integration of new technologies into the daily driving experience.

Europe (Germany, France, UK): Europe, with its strong automotive manufacturing base and a keen focus on safety and environmental regulations, is another pivotal region. Countries like Germany, home to automotive giants such as Daimler, BMW, and Audi, are at the forefront of developing and integrating sophisticated semi-autonomous features. The emphasis on regulatory harmonization across the European Union will further facilitate the adoption of Level 2 and Level 3 Autonomous Vehicles. The region is also a significant market for advanced Commercial Vehicles, where semi-autonomous features can lead to improved logistics efficiency and reduced operational costs. The stringent safety standards and growing consumer awareness regarding the benefits of ADAS contribute to a robust market trajectory. The integration of these technologies within the burgeoning electric vehicle market in Europe further solidifies its leading position.

Asia-Pacific (China, Japan, South Korea): While currently experiencing a strong uptake of Level 2 Autonomous Vehicles, the Asia-Pacific region, particularly China, is rapidly emerging as a dominant force. Fueled by a massive automotive market, significant government investment in technology and infrastructure, and a high propensity for early technology adoption, China is expected to witness exponential growth in World Semi-Autonomous Vehicles Production. Companies like Tesla have established a strong presence, and local manufacturers are investing heavily in autonomous driving capabilities. Japan and South Korea, with their technologically advanced automotive sectors, are also key players, driving innovation in areas like sensor technology and AI. The application in Commercial Vehicles in this region is also gaining traction due to the sheer scale of logistics and supply chain operations. The focus here will be on scaling production rapidly and making these technologies accessible to a broader consumer base.

Segment Dominance:

Level 2 Autonomous Vehicles: Throughout the Historical Period and extending well into the Forecast Period, Level 2 Autonomous Vehicles will continue to dominate the market in terms of unit volume. Their widespread availability in a vast array of Passenger Vehicles, coupled with their relatively lower cost compared to higher automation levels, makes them the entry point for consumers into the world of semi-autonomous driving.

Passenger Vehicles: This application segment will indisputably lead in terms of World Semi-Autonomous Vehicles Production and market share. The sheer volume of Passenger Vehicles produced and sold globally, combined with the direct benefit of enhanced safety and convenience for individual drivers and their families, makes this the primary driver for semi-autonomous technology deployment.

World Semi-Autonomous Vehicles Production: The sheer scale of production expected in the coming years, particularly driven by the aforementioned regions and segments, will define the overall market landscape. As manufacturing processes become more efficient and economies of scale are realized, the World Semi-Autonomous Vehicles Production numbers are set to soar, making these vehicles a ubiquitous feature on our roads.

Several key factors are acting as potent growth catalysts for the semi-autonomous vehicle industry. The relentless pursuit of enhanced road safety remains a primary driver, as ADAS technologies demonstrably reduce accidents and fatalities. Increasing consumer demand for comfort, convenience, and a reduced driving burden, particularly in urban environments, further fuels adoption. Rapid technological advancements in AI, sensor technology, and computing power are continuously improving the capabilities and affordability of semi-autonomous systems. Furthermore, supportive government regulations and the establishment of clear legal frameworks are building confidence and encouraging investment. The growing integration of semi-autonomous features within the booming electric vehicle market also acts as a synergistic catalyst, aligning with the broader trend towards sustainable and technologically advanced mobility.

This report offers a granular and holistic view of the semi-autonomous vehicle market, covering every facet from production volumes to future market projections. It meticulously analyzes the World Semi-Autonomous Vehicles Production figures, providing insights into the manufacturing capacities and strategies of key players like Tesla, General Motors, Daimler, BMW, Audi, Volvo, and Ford. The report delves deeply into the segmentation by vehicle type, distinguishing between the prevalent Level 2 Autonomous Vehicles and the emerging Level 3 Autonomous Vehicles, while also examining the application across Passenger Vehicles and Commercial Vehicles. Beyond the quantitative data, the report provides qualitative analysis of market trends, driving forces, challenges, and growth catalysts, painting a comprehensive picture of the industry's dynamics and future potential.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 18.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 18.8%.

Key companies in the market include Tesla, General Motors, Daimler, BMW, Audi, Volvo, Ford.

The market segments include Type, Application.

The market size is estimated to be USD 58.17 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Semi-Autonomous Vehicles," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semi-Autonomous Vehicles, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.