1. What is the projected Compound Annual Growth Rate (CAGR) of the Self-Checkout Systems?

The projected CAGR is approximately 9.8%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Self-Checkout Systems

Self-Checkout SystemsSelf-Checkout Systems by Type (Stand-alone Self-checkout Systems, Wall-mounted Self-checkout Systems, Countertop Self-checkout Systems), by Application (Hypermarket & Supermarket, Food Service, Department Stores, Grocery/Convenience Stores, Pharmacy, Autonomous Stores, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

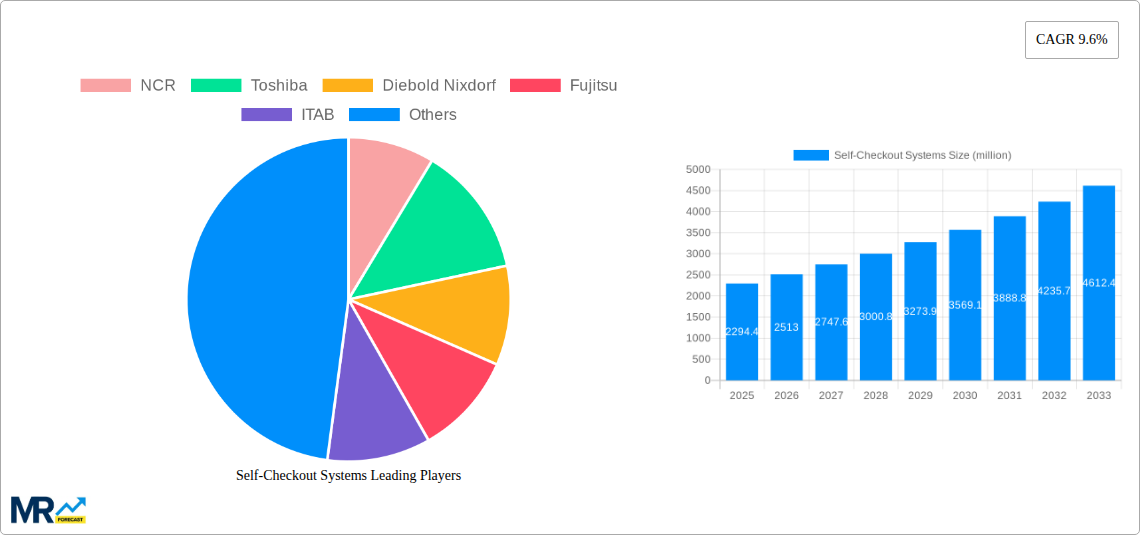

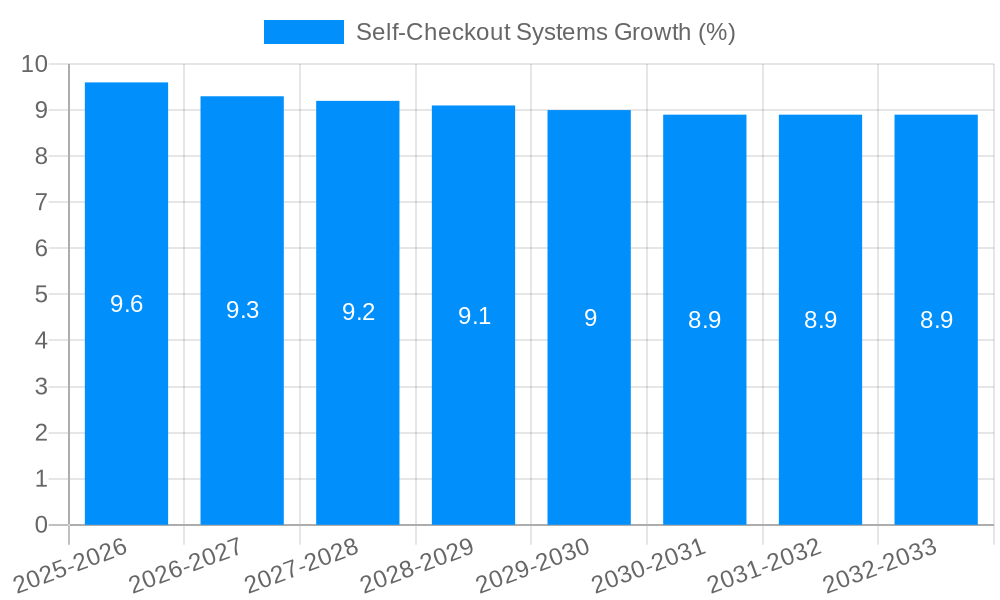

The global self-checkout (SCO) systems market is poised for significant expansion, projected to reach an estimated USD 4,849 million by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 9.8% over the forecast period of 2025-2033. This growth is primarily fueled by the increasing demand for enhanced customer convenience, reduced operational costs for retailers, and the growing adoption of frictionless retail experiences. The ongoing digital transformation in the retail sector, coupled with labor shortages and the need for efficient store operations, are compelling factors pushing businesses towards implementing SCO solutions across various retail formats. Furthermore, technological advancements, including improved AI and machine learning capabilities for enhanced security and personalized customer interactions, are expected to further stimulate market penetration.

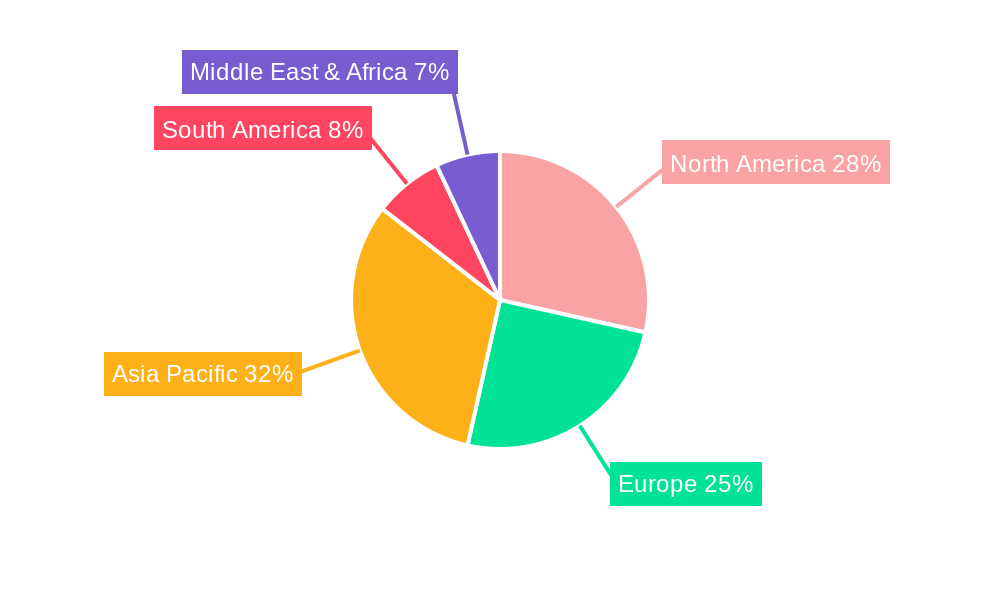

The self-checkout systems market is segmented by type, with stand-alone systems expected to dominate due to their flexibility and scalability, while wall-mounted and countertop systems cater to specific space constraints and operational needs. Application-wise, hypermarkets and supermarkets represent the largest segment, leveraging SCO for high-volume transactions and improved customer flow. The growth in food service and the emergence of autonomous stores, driven by advancements in sensor technology and computer vision, are also crucial growth areas. Geographically, the Asia Pacific region is anticipated to witness the highest growth rate, propelled by rapid urbanization, a burgeoning middle class, and a strong focus on technological adoption in retail by countries like China and India. North America and Europe will continue to be significant markets, characterized by a mature adoption of SCO and a focus on innovation and premium solutions.

This comprehensive report delves into the dynamic global Self-Checkout Systems market, providing an in-depth analysis of its historical performance, current landscape, and projected trajectory. Spanning a study period from 2019 to 2033, with a robust base year of 2025, the research offers critical insights for stakeholders seeking to understand and capitalize on market opportunities. The report meticulously examines various self-checkout system types, including Stand-alone, Wall-mounted, and Countertop configurations, while also dissecting application segments such as Hypermarkets & Supermarkets, Food Service, Department Stores, Grocery/Convenience Stores, Pharmacies, Autonomous Stores, and Others. Leveraging extensive data from the historical period (2019-2024) and the estimated year (2025), the forecast period (2025-2033) predicts significant market evolution.

XXX The global Self-Checkout Systems market is undergoing a transformative period, driven by an escalating demand for enhanced customer convenience and operational efficiency within the retail and service sectors. The increasing adoption of frictionless and contactless payment methods is a paramount trend, directly influencing the design and functionality of self-checkout solutions. Consumers, accustomed to digital interactions, are actively seeking faster and more intuitive checkout experiences, pushing retailers to invest in self-service technologies that minimize wait times and streamline the purchasing journey. This trend is particularly pronounced in densely populated urban areas and within large-format retail environments like hypermarkets and supermarkets, where transaction volumes are inherently high. Furthermore, the integration of artificial intelligence (AI) and machine learning (ML) is emerging as a significant trend, enabling self-checkout systems to offer personalized recommendations, detect potential fraud more effectively, and even facilitate sophisticated inventory management. The proliferation of mobile payment options and the growing acceptance of biometric authentication are also reshaping the self-checkout landscape, paving the way for even more seamless and secure transactions. The report anticipates a substantial shift towards self-checkout solutions that not only facilitate payment but also offer value-added services, such as loyalty program integration and personalized promotions. This evolution from a simple transactional tool to a comprehensive customer engagement platform is a key indicator of the market's future direction. The increasing focus on data analytics derived from self-checkout interactions will empower retailers to gain deeper insights into customer behavior, optimize store layouts, and personalize marketing efforts, further solidifying the strategic importance of these systems.

The self-checkout systems market is experiencing robust growth, propelled by a confluence of powerful driving forces. At the forefront is the relentless pursuit of operational efficiency by retailers. The ability of self-checkout systems to reduce labor costs, minimize checkout queues, and reallocate staff to more customer-facing roles is a significant incentive for adoption across various retail formats. Moreover, the escalating consumer demand for convenience and speed plays a pivotal role. In an era of instant gratification, shoppers are increasingly seeking self-service options that allow them to bypass traditional, often lengthy, checkout lines. This preference is further amplified by the growing familiarity and comfort consumers have with technology-driven solutions. The COVID-19 pandemic also acted as a significant catalyst, highlighting the benefits of contactless transactions and reduced human interaction, thereby accelerating the adoption of self-checkout systems. Furthermore, advancements in technology, including improved scanner accuracy, intuitive user interfaces, and robust security features, have made self-checkout systems more reliable and user-friendly, thereby increasing their appeal to both businesses and consumers. The continuous innovation in payment technologies, such as mobile wallets and contactless cards, seamlessly integrates with self-checkout platforms, further enhancing their attractiveness.

Despite the compelling growth trajectory, the self-checkout systems market is not without its challenges and restraints. A significant hurdle is the potential for increased shrinkage and theft. While self-checkout systems aim to improve efficiency, they can also present opportunities for fraudulent activities if not properly managed with robust security measures and diligent monitoring. The initial investment cost associated with implementing self-checkout systems, including hardware, software, and integration with existing retail infrastructure, can be a substantial barrier for smaller businesses or those with tight budgets. Customer adoption and user acceptance also remain a concern. While many consumers embrace self-checkout, a segment of the population may still prefer traditional cashier assistance due to technological unfamiliarity, accessibility issues, or a desire for human interaction. The need for ongoing maintenance, software updates, and technical support for these complex systems can also pose operational challenges and contribute to the total cost of ownership. Furthermore, the integration of self-checkout systems with diverse point-of-sale (POS) software and inventory management systems can be complex and time-consuming, requiring significant IT resources. Finally, concerns regarding data privacy and security, especially with the increasing collection of customer data through these systems, need to be meticulously addressed to maintain consumer trust.

The North America region is poised to maintain its dominance in the global Self-Checkout Systems market, driven by a mature retail landscape characterized by early adoption of technology, high consumer spending power, and a strong preference for convenience. The United States, in particular, is a key market within North America, with a significant presence of large hypermarkets and supermarkets that are continually investing in advanced self-checkout solutions to optimize store operations and enhance customer experience. The increasing penetration of e-commerce has also led to a greater emphasis on in-store efficiency, pushing retailers to leverage self-checkout to differentiate themselves.

Within North America, the Hypermarket & Supermarket application segment is expected to command the largest market share. These large-format retail environments handle a high volume of transactions, making self-checkout systems an essential tool for managing customer flow and reducing wait times. Retailers in this segment are actively deploying a variety of self-checkout configurations, including stand-alone units and increasingly, more compact countertop and wall-mounted systems to optimize floor space. The drive for operational efficiency and the need to provide a faster, more convenient checkout experience for a broad customer base are the primary catalysts for this segment's continued growth. The integration of advanced features like AI-powered product recognition, self-learning systems for error reduction, and seamless loyalty program integration are further solidifying the dominance of self-checkout in hypermarkets and supermarkets.

Furthermore, the Stand-alone Self-checkout Systems type is anticipated to lead the market within this dominant region and segment. These systems offer a comprehensive and often more robust solution, typically featuring larger screens, integrated scanners, payment terminals, and bagging areas. Their self-contained nature allows for flexible placement within stores, from dedicated self-checkout zones to strategic positions throughout the store. The scalability and feature richness of stand-alone units make them ideal for the high transaction volumes and diverse product ranges found in hypermarkets and supermarkets. As retailers seek to provide a complete self-service solution, stand-alone units continue to be the preferred choice for their comprehensive functionality and ability to offer an immersive self-checkout experience. The ongoing technological advancements, such as the incorporation of AI for item identification and fraud detection, will further enhance the capabilities and appeal of stand-alone self-checkout systems, ensuring their continued leadership in the market.

The self-checkout systems industry is being propelled by several key growth catalysts. The relentless pursuit of operational efficiency and labor cost reduction by retailers remains a primary driver. Consumers' increasing demand for speed and convenience, coupled with the growing acceptance of contactless payment methods, further fuels adoption. Technological advancements in areas like AI, computer vision for product recognition, and enhanced user interfaces are making these systems more intuitive and reliable, thereby attracting a wider range of businesses. The rise of autonomous stores and the need for seamless, staff-free checkout experiences also present a significant growth opportunity.

This report offers an exhaustive examination of the global Self-Checkout Systems market. It meticulously analyzes market size, segmentation, competitive landscape, and future projections across various system types and application segments. The study provides deep dives into the trends shaping the industry, the key drivers fueling its growth, and the challenges that need to be navigated. Furthermore, it highlights key regions and countries expected to dominate the market, along with specific segments that will witness substantial expansion. The report also identifies critical growth catalysts and profiles the leading industry players, offering valuable insights for strategic decision-making and investment planning within the evolving self-checkout ecosystem.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 9.8% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 9.8%.

Key companies in the market include NCR, Toshiba, Diebold Nixdorf, Shanghai Sunmi Technology, Qingdao CCL Technology, Qingdao HiStone Intelligent Commercial, Fujitsu, ITAB, Pan-Oston, Grupo Digicon (Perto), Qingdao Wintec System, Guangzhou FOUNYA, Shenzhen Sed Industry, Modern-Expo Group, HP, Guangzhou Zonerich Business Machine, Telepower Communication, Bozz Technology, Yanso Electronic, Ejeton Technology.

The market segments include Type, Application.

The market size is estimated to be USD 4849 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Self-Checkout Systems," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Self-Checkout Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.