1. What is the projected Compound Annual Growth Rate (CAGR) of the Robots in Orthopaedic Surgery?

The projected CAGR is approximately 11.9%.

Robots in Orthopaedic Surgery

Robots in Orthopaedic SurgeryRobots in Orthopaedic Surgery by Type (Spine Procedures, Knee and Hip Replacement Procedures, Others), by Application (Hospitals, ASCs, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

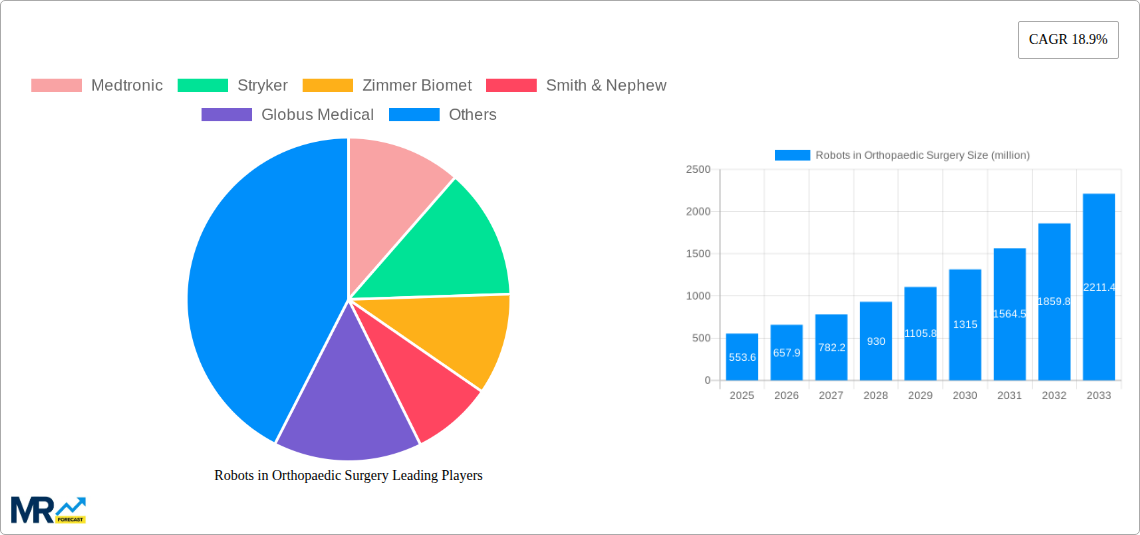

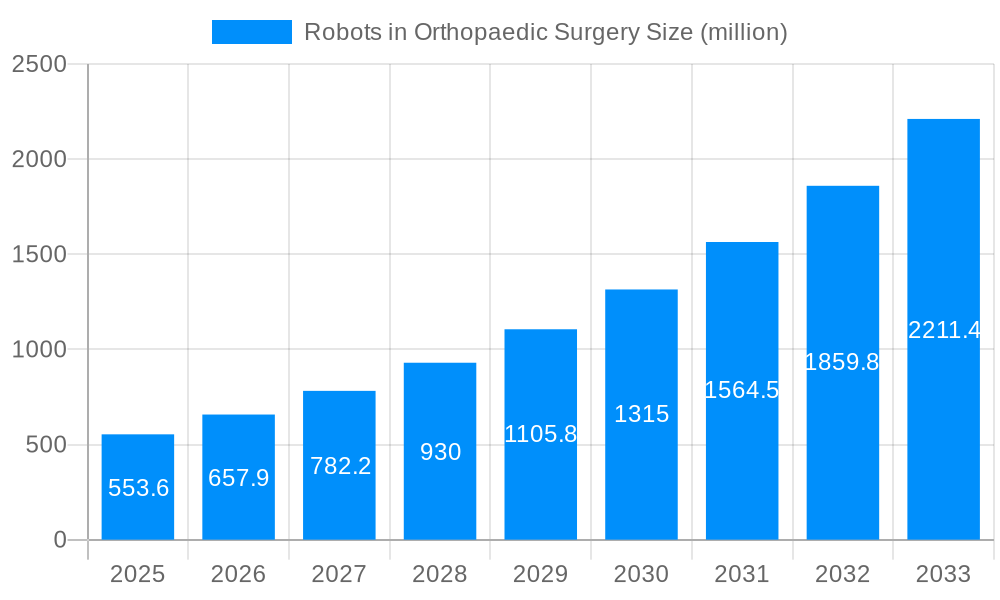

The global orthopaedic robotic surgery market is projected for significant growth, with an estimated market size of $1.27 billion by 2025. This expansion is driven by a robust CAGR of 11.9%, fueled by advancements in surgical robotics, the increasing demand for minimally invasive procedures, and the pursuit of enhanced surgical precision. Key drivers include sophisticated robotic platforms offering superior visualization, dexterity, and surgeon control, leading to improved patient outcomes and accelerated recovery. The growing application of these technologies in complex spine and joint replacement surgeries (knee and hip) significantly contributes to market penetration. Furthermore, the rising incidence of orthopaedic conditions globally, coupled with an aging population experiencing increased rates of osteoarthritis and degenerative joint diseases, sustains demand for innovative surgical solutions.

The competitive landscape features both established players and emerging innovators focusing on technological advancements and strategic collaborations. While the United States currently leads market adoption due to early investment in healthcare technology, Europe and the Asia Pacific regions are exhibiting rapid growth. The increasing utilization of robotic surgery in Ambulatory Surgery Centers (ASCs) alongside traditional hospitals indicates a trend toward more efficient and cost-effective healthcare delivery. However, high initial capital investment, the necessity for specialized surgeon and staff training, and regional reimbursement challenges may present obstacles. Despite these, the substantial benefits of robotic-assisted surgery, including reduced complications, shorter hospital stays, and enhanced long-term patient satisfaction, are expected to propel market evolution and adoption through 2033.

This comprehensive report provides an in-depth analysis of the dynamic orthopaedic robotic surgery market, covering the period from 2019 to 2033. With a base year of 2025, this analysis offers detailed insights into market trends, growth drivers, challenges, and future opportunities. The report utilizes extensive data from the historical period of 2019-2024 and provides robust forecasts for 2025-2033.

The global orthopaedic robotic surgery market is set for substantial expansion, propelled by technological innovation and a growing demand for minimally invasive interventions. The integration of artificial intelligence and advanced robotics is revolutionizing surgical precision, patient outcomes, and overall efficiency in orthopaedic specialties. This report offers a granular market view, segmented by key companies, product types, applications, and geographies, providing strategic intelligence for stakeholders navigating this critical sector.

XXX The robots in orthopaedic surgery market is experiencing an unprecedented surge in innovation and adoption, fundamentally reshaping how surgical interventions are performed. A significant trend is the increasing precision and minimally invasive nature of robotic-assisted procedures. This translates into reduced patient trauma, shorter hospital stays, and faster recovery times, directly contributing to improved patient satisfaction and reduced healthcare costs. The market is also witnessing a proliferation of sophisticated navigation and visualization systems that provide surgeons with real-time, high-definition imaging, allowing for unparalleled accuracy in implant placement and bone preparation. Furthermore, the ongoing development of AI-powered analytics and machine learning algorithms is further enhancing surgical planning and execution. These intelligent systems can analyze vast amounts of patient data to predict potential complications, optimize surgical pathways, and even guide instruments with a degree of dexterity and consistency that surpasses human capabilities.

The shift towards value-based healthcare models is another potent trend fueling the adoption of robotic systems. As healthcare providers are increasingly incentivized to demonstrate positive patient outcomes and cost-effectiveness, the inherent efficiencies offered by robotic surgery become highly attractive. These systems, while representing a significant upfront investment, ultimately contribute to long-term savings through reduced complications, fewer revision surgeries, and optimized resource utilization. The expansion of robotic platforms to encompass a wider array of orthopaedic specialties, beyond traditional knee and hip replacements, is also a notable trend. This includes the burgeoning application of robotics in spinal procedures, trauma surgeries, and even smaller joint interventions, indicating a broadening of the technology's reach and impact. The market is also seeing a concerted effort by leading manufacturers to develop more user-friendly and intuitive robotic interfaces, democratizing access to these advanced technologies and enabling a broader range of surgeons to benefit from their capabilities. The integration of haptic feedback and augmented reality further enhances the surgeon's sensory experience and decision-making capabilities, pushing the boundaries of surgical performance. Finally, the growing emphasis on personalized medicine is driving the development of customized surgical plans tailored to individual patient anatomy and pathology, a goal that robotic systems are ideally positioned to achieve. The increasing focus on data collection and analysis from robotic procedures is also paving the way for continuous improvement and the establishment of best practices, further solidifying the transformative role of robots in orthopaedic surgery.

The orthopaedic surgery robot market is experiencing robust growth, propelled by a confluence of powerful driving forces. Foremost among these is the relentless pursuit of enhanced surgical precision and patient outcomes. Robotic systems offer unparalleled accuracy in instrument manipulation and implant placement, minimizing invasiveness, reducing blood loss, and significantly decreasing the risk of complications. This translates directly into faster patient recovery times and improved long-term functionality, making these technologies highly desirable for both surgeons and patients. Accompanying this is the increasing global prevalence of orthopaedic conditions such as osteoarthritis and degenerative spine diseases, driven by an aging population and rising rates of obesity. This demographic shift creates a larger patient pool requiring orthopaedic interventions, thereby stimulating demand for advanced surgical solutions that can handle complex cases efficiently and effectively.

Furthermore, significant advancements in robotic technology itself are acting as a major catalyst. Innovations in artificial intelligence, machine learning, and advanced imaging have led to the development of more intelligent, intuitive, and versatile robotic platforms. These include sophisticated navigation systems, real-time data feedback, and improved dexterity, which empower surgeons with greater control and confidence during complex procedures. The ongoing development of smaller, more affordable, and specialized robotic systems is also broadening their accessibility across different healthcare settings, including ambulatory surgery centers (ASCs). This democratization of technology is crucial for market expansion. Finally, the growing emphasis on minimally invasive surgery (MIS) as a preferred approach in orthopaedics is a critical driver. Patients are increasingly seeking procedures with smaller incisions, less pain, and quicker return to daily activities, and robotic assistance is a key enabler of these minimally invasive techniques. The competitive landscape among major orthopaedic companies is also fostering innovation and driving down costs, further accelerating adoption.

Despite the impressive growth trajectory, the robots in orthopaedic surgery market faces several significant challenges and restraints that could temper its expansion. The most prominent hurdle is the substantial initial capital investment required to acquire and maintain robotic surgical systems. These sophisticated technologies come with a high price tag, often running into millions of dollars per system, which can be prohibitive for smaller hospitals or healthcare facilities with limited budgets, particularly in developing economies. This cost barrier extends beyond the purchase price to include ongoing expenses for maintenance, software updates, specialized training for surgical teams, and consumables. The perceived steep learning curve associated with operating these robotic platforms can also be a deterrent. Surgeons require extensive training and practice to achieve proficiency, which demands time, resources, and dedicated institutional support, potentially slowing down the rate of adoption.

Another significant restraint is the reimbursement landscape. While the benefits of robotic surgery are evident, the extent to which insurance providers cover these procedures and systems can vary widely, impacting their economic viability for healthcare institutions. Uncertainty in reimbursement policies can create hesitation among hospitals considering investment. Furthermore, the limited availability of skilled personnel, including both highly trained robotic surgeons and specialized support staff, can restrict the widespread implementation of these technologies. The integration of robotic systems into existing hospital workflows and infrastructure also presents logistical challenges, requiring adjustments to operating room setup, sterile processing protocols, and staff scheduling. Finally, concerns regarding data privacy and security, especially with the increasing integration of AI and cloud-based solutions, need to be addressed to foster trust and ensure patient confidentiality. The potential for technical malfunctions or system downtime, although rare, also poses a risk that needs careful consideration and robust mitigation strategies.

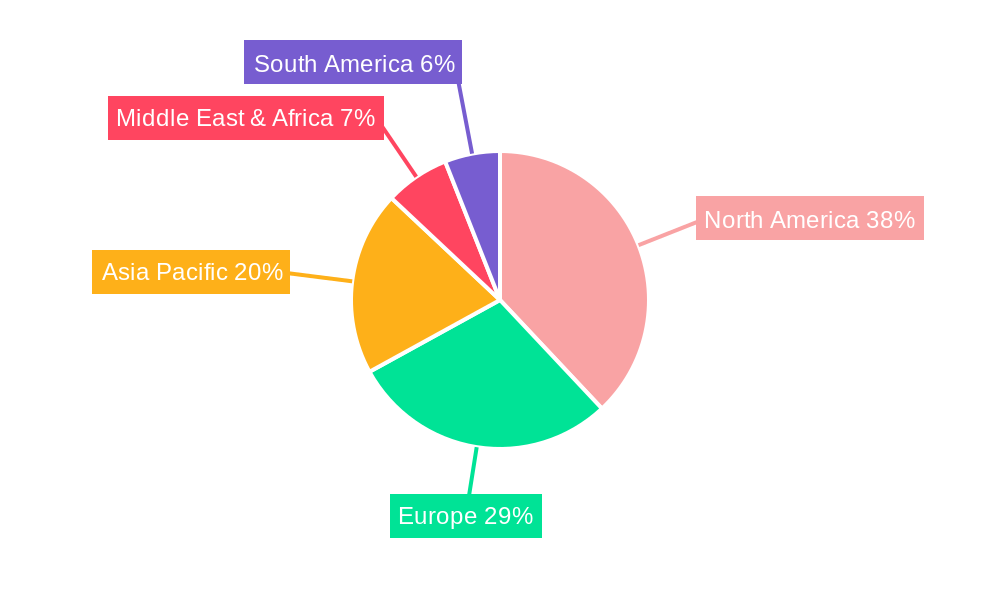

The North America region, particularly the United States, is poised to dominate the robots in orthopaedic surgery market. This dominance is driven by a confluence of factors including a highly advanced healthcare infrastructure, a strong emphasis on technological innovation, and a significant patient population with a high incidence of orthopaedic conditions. The robust reimbursement policies in the U.S. generally favor the adoption of advanced medical technologies, including robotic surgical systems, making them a more financially viable option for healthcare providers. Furthermore, the presence of leading orthopaedic device manufacturers with established research and development capabilities in North America fuels the introduction of cutting-edge robotic solutions. The region also benefits from a high level of surgeon adoption and expertise in robotic-assisted procedures, fostered by numerous training programs and academic institutions.

Within this dominant region, the Knee and Hip Replacement Procedures segment is expected to hold the largest market share. This is attributable to the high volume of these procedures performed annually, the well-established track record of robotic assistance in improving outcomes for these common orthopaedic interventions, and the availability of highly refined and specialized robotic systems tailored for total hip and knee arthroplasty. These robotic systems offer significant advantages in terms of implant alignment, bone preparation accuracy, and soft tissue balancing, leading to improved patient satisfaction and implant longevity. The increasing demand for joint replacements due to an aging population and rising obesity rates further solidifies the prominence of this segment.

Several key factors are acting as potent growth catalysts for the robots in orthopaedic surgery industry. The continuous innovation in robotic technology, including the integration of AI and machine learning for enhanced precision and predictive analytics, is a primary driver. The increasing global burden of orthopaedic diseases, fueled by an aging population and lifestyle factors, creates a persistent demand for surgical solutions. Furthermore, the growing preference for minimally invasive procedures by patients and surgeons alike, which robots excel at enabling, significantly boosts adoption. The expanding portfolio of robotic applications beyond joint replacements to spine and other orthopaedic specialties is also opening new market avenues. Finally, supportive government initiatives and increasing R&D investments by leading companies are fostering a conducive environment for market expansion and technological advancement.

This report provides a comprehensive overview of the robots in orthopaedic surgery market, offering detailed insights into market dynamics, competitive landscapes, and future projections. It meticulously analyzes the market by company, type, application, and region, providing valuable strategic intelligence for stakeholders. The report delves into key industry trends, such as the increasing adoption of AI, the growing demand for minimally invasive procedures, and the expansion of robotic applications across various orthopaedic specialties. It also scrutinizes the driving forces behind market growth, including technological advancements and the rising prevalence of orthopaedic conditions, while acknowledging and addressing the challenges and restraints that impact market expansion. The detailed regional analysis, with a focus on dominant markets like North America, and segment-specific insights, particularly on knee and hip replacement procedures, offer a granular understanding of the market's structure. Furthermore, the report highlights significant developments and leading players, providing a holistic view of the sector. This report is an indispensable resource for industry professionals seeking to navigate and capitalize on the transformative potential of robotics in orthopaedic surgery.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 11.9%.

Key companies in the market include Medtronic, Stryker, Zimmer Biomet, Smith & Nephew, Globus Medical, TINAVI, Corin Group (OMNI), THINK Surgical, Santa Medical Technology Co., FUTURTEC, .

The market segments include Type, Application.

The market size is estimated to be USD 1.27 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Robots in Orthopaedic Surgery," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Robots in Orthopaedic Surgery, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.